Written by

Eric

Share this article

.svg)

Subscribe to updates

If you have watched a Super Bowl in the last decade or simply scrolled through social media, you have likely seen Rocket Mortgage. They are everywhere. But is the "Push Button, Get Mortgage" hype actually real? As we head into 2026, many first-time homebuyers and tech-savvy borrowers are asking if the convenience is worth the price tag. I was curious, too. That is why I decided to dive deep into exactly what this company offers today. In this complete review, I will break down their real ratings, new loan programs, and whether their digital-first approach is right for you.

What is Rocket Mortgage?

To understand where Rocket Mortgage is today, you have to look at where they started. Founded in 1985 by Dan Gilbert as Rock Financial, the company eventually rebranded to Quicken Loans before fully embracing the "Rocket" identity we know now. They are headquartered in Detroit, Michigan, and have grown into the largest mortgage lender in the United States, according to Wiki.

What makes them different is their obsession with technology. In 2015, they launched the Rocket Mortgage app, which completely revolutionized the industry by allowing borrowers to apply for a home loan entirely online. It wasn't just a marketing gimmick; it shifted how we think about financing homes. Today, Rocket is a massive fintech company (NYSE: RKT) that handles everything from conventional loans to FHA and VA products. They focus heavily on speed and user experience, aiming to cut out the paperwork headaches that usually plague the mortgage process. While they are a non-bank lender—meaning they don't offer checking or savings accounts—their digital footprint is arguably bigger than most traditional banks combined.

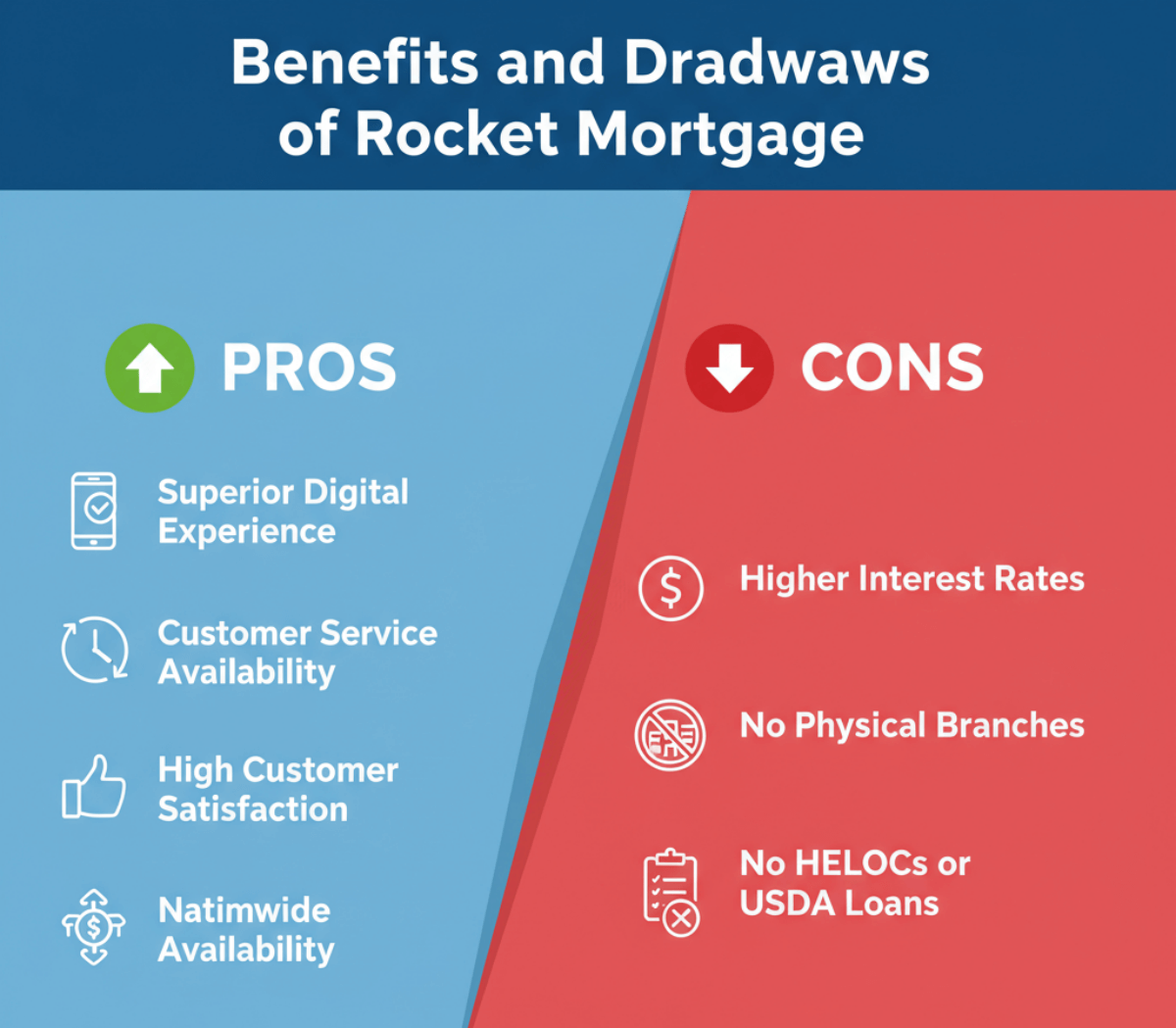

Benefits and Drawbacks of Rocket Mortgage

No lender is perfect, and while Rocket Mortgage offers an incredibly slick experience, it is not the best fit for every single borrower. I dug into the details to see where they shine and where they might fall short compared to the competition.

Pros:

- Superior Digital Experience: Their app and website are industry leaders. You can upload documents, sign papers, and track your loan status 24/7 without needing to call anyone.

- Customer Service Availability: Unlike traditional banks that close at 5 PM, Rocket has loan officers available on weekends and evenings, which is huge when you are making offers in a hot market.

- High Customer Satisfaction: They consistently rank near the top in J.D. Power studies for mortgage origination satisfaction.

- Nationwide Availability: They are licensed to lend in all 50 states.

Cons:

- Higher Interest Rates: Convenience often comes with a cost. Their advertised rates are frequently higher than average unless you pay "points" to buy the rate down.

- No Physical Branches: If you prefer sitting across a desk from a human to discuss your finances, you are out of luck. Everything is remote.

- No HELOCs or USDA Loans: While they offer home equity loans, they generally do not offer Home Equity Lines of Credit (HELOCs) or USDA rural development loans

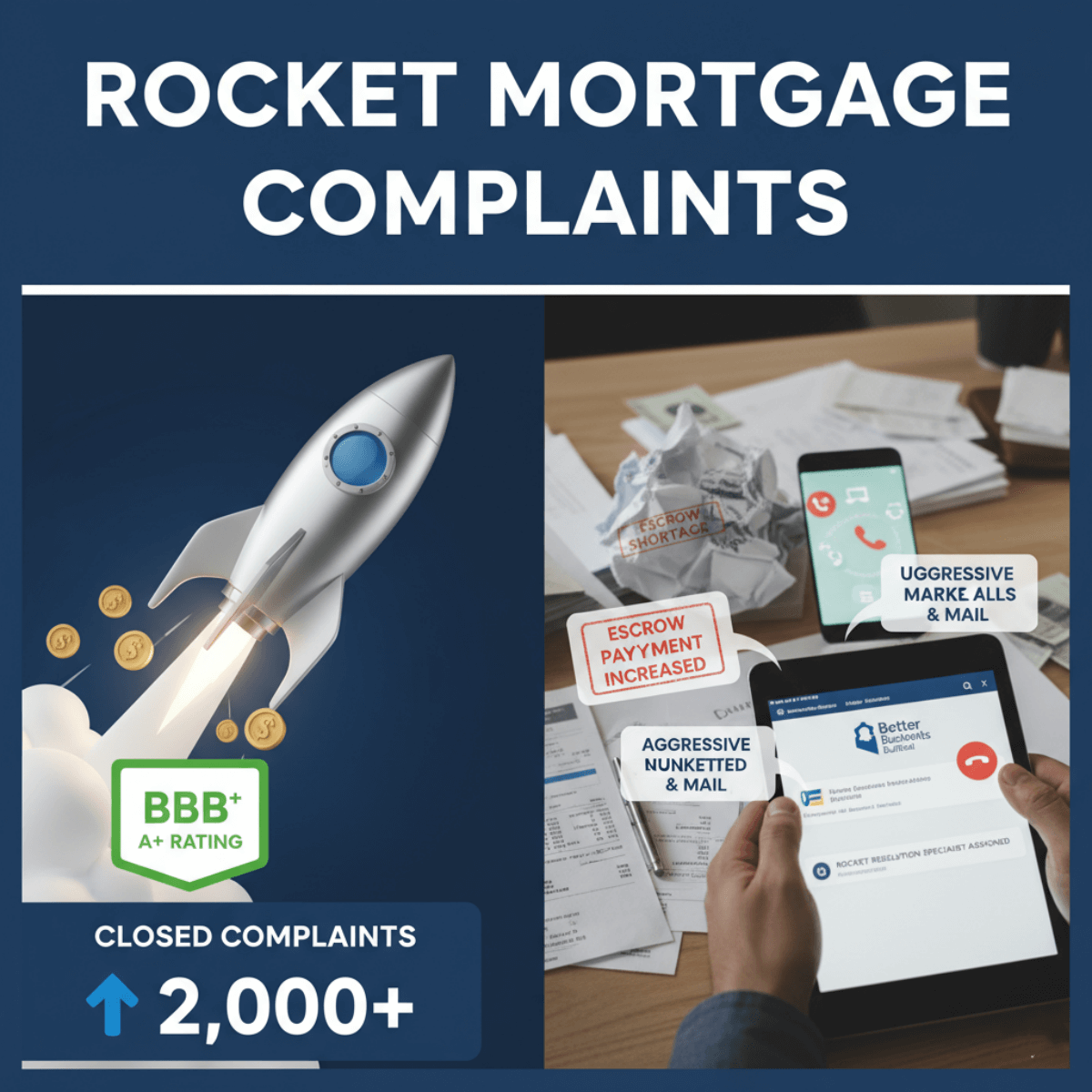

Rocket Mortgage Complaints

While their marketing is glossy, real-world experiences can sometimes be messy. I looked at Rocket Mortgage's Better Business Bureau (BBB) profile to see what actual customers are complaining about. Currently, Rocket Mortgage holds an A+ rating, but they have faced a volume of closed complaints.

The most common complaints revolve around escrow and servicing issues. Many borrowers reported confusion after closing, specifically regarding escrow shortages that caused their monthly payments to jump unexpectedly. Others mentioned frustration with the billing process after their loan was sold to or serviced by Rocket. There are also reports of aggressive marketing; once you inquire, you might receive a flood of calls and junk mail, which some users found overwhelming. However, it is worth noting that Rocket is generally responsive on the BBB platform, often assigning specialists to resolve these disputes quickly.

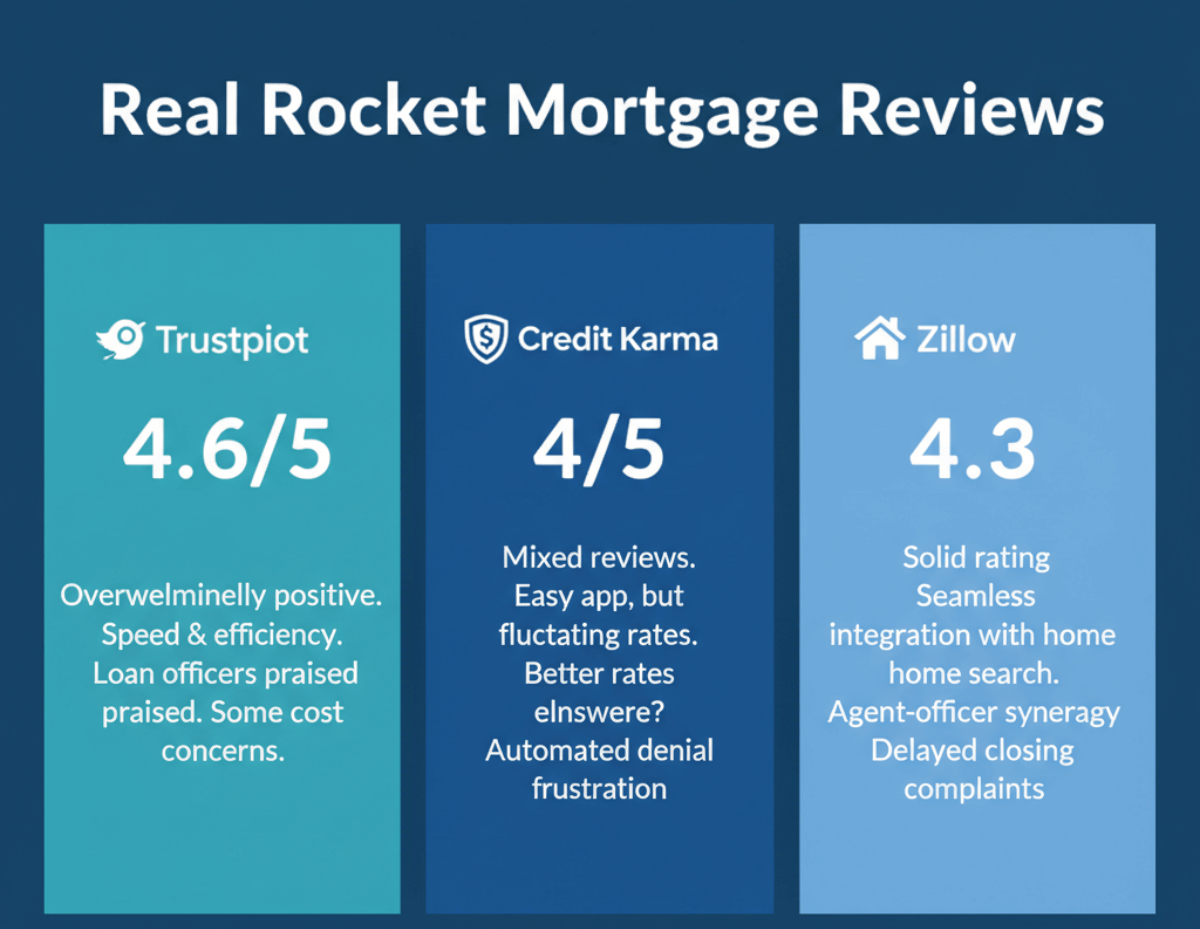

Real Rocket Mortgage Reviews

To get the full picture, I didn't just rely on official complaints. I scoured the most popular review platforms to see what everyday users are saying right now.

Trustpilot

On Trustpilot, Rocket Mortgage generally maintains a strong reputation, often scoring 4.6 out of 5 stars or higher. The reviews here are overwhelmingly positive regarding the speed and efficiency of the process. Users frequently mention specific loan officers who "went above and beyond" to close loans in under 30 days. However, the negative reviews here echo the cost concerns. Some users felt the closing costs were higher than estimated, or that the initial rate quoted wasn't what they ended up with at the locking stage.

Credit Karma

The vibe on Credit Karma is often a bit more mixed, with a rating of 4 out of 5. While many users praise the app's interface and the ease of uploading documents, the rating here can fluctuate. A recurring theme in the lower-rated reviews is affordability. Several members noted that while the process was easy, they found better interest rates at local credit unions or smaller banks. If you have a lower credit score, you might find some frustration here, as some users felt Rocket's automated pre-approval system gave them false hope before a human underwriter denied the file.

Zillow

Zillow creates an interesting contrast. Rocket Mortgage often has a high volume of reviews here, with a generally solid rating (often hovering around 4.34 stars). Homebuyers on Zillow appreciate the integration. Since many people search for homes on Zillow, the transition to financing with Rocket feels natural. Positive reviews highlight the synergy between agents and loan officers. Conversely, negative reviews here often come from people whose closing dates were missed or delayed due to last-minute document requests, which can be incredibly stressful when a move-in date is on the line.

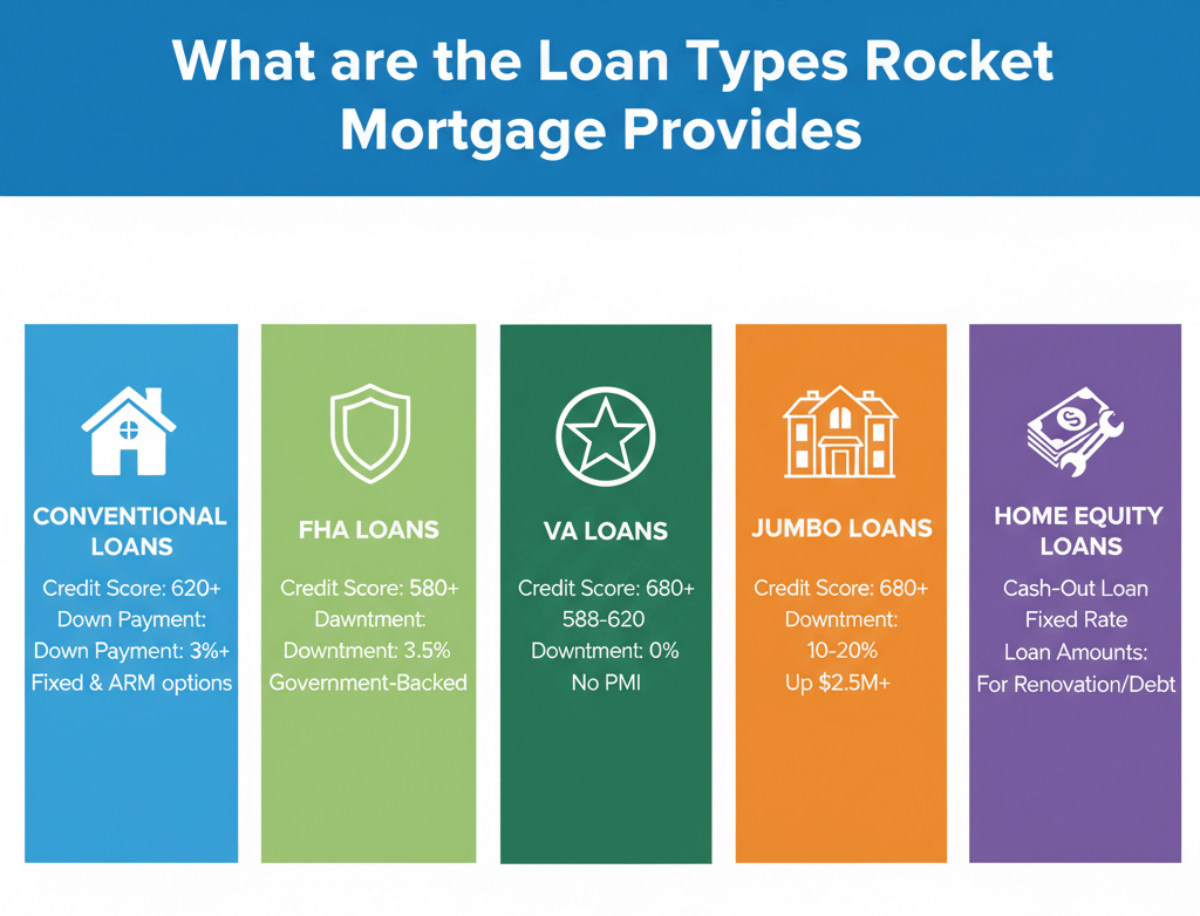

What are the Loan Types Rocket Mortgage Provides

Rocket Mortgage covers the majority of standard loan products that American homebuyers need. They focus on "conforming" loans that fit government guidelines.

Conventional Loans

This is their bread and butter. You typically need a credit score of at least 620 to qualify. Rocket offers fixed-rate mortgages (15-year and 30-year) and adjustable-rate mortgages (ARMs). Down payments can be as low as 3% for first-time buyers.

FHA Loans

Great for those with smaller down payments or lower credit scores. Rocket Mortgage accepts scores as low as 580 for FHA loans, which require a 3.5% down payment. These are government-backed and very popular for first-time buyers who might have a higher debt-to-income ratio.

VA Loans

If you are an eligible veteran or active-duty service member, this is likely your best option. Rocket is a large VA lender. These loans usually require 0% down payment and have no monthly mortgage insurance (PMI). The credit score requirement is generally around 580 to 620 depending on the overall file.

Jumbo Loans

For homes that exceed the conforming loan limits (which change annually), you need a Jumbo loan. Rocket offers these for loan amounts up to $2.5 million (or sometimes higher). Because these are riskier for the lender, they require a higher credit score, typically 680 or higher, and a larger down payment, usually at least 10-20%.

Home Equity Loans

It is important to note that Rocket Mortgage primarily offers Home Equity Loans, which are lump-sum cash-out loans with a fixed interest rate. This is different from a HELOC (Line of Credit), which works like a credit card. A Home Equity Loan is great if you need a specific amount for a big renovation or debt consolidation.

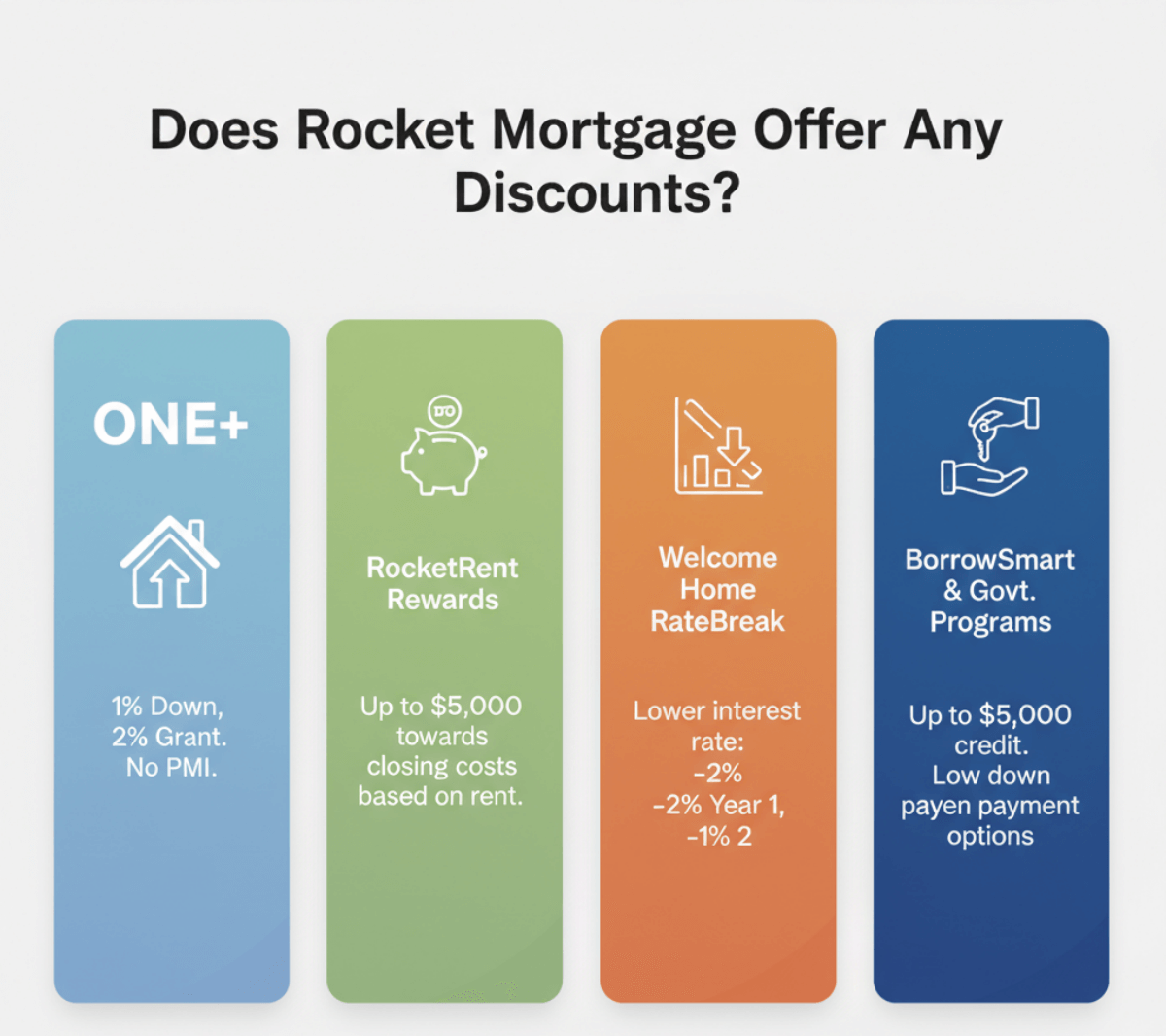

Does Rocket Mortgage Offer Any Discounts?

Yes, they do. In fact, Rocket has launched several aggressive affordability programs to combat high interest rates and home prices.

ONE+

This is a game-changer for low-to-moderate-income buyers. With the ONE+ program, you put down just 1% of the purchase price, and Rocket Mortgage covers the other 2% as a grant (which you don't have to pay back). Even better, they eliminate the monthly Private Mortgage Insurance (PMI) cost. You generally must earn less than 80% of your Area Median Income (AMI) to qualify.

RocketRentRewards

Launched recently to help renters transition to owners, RocketRentRewards allows you to earn closing cost credits based on your rental history. If you use their specific program, you can get 10% cash back on your last 12 months of rent payments, up to $5,000, applied directly to your closing costs. This rewards you simply for paying your rent on time.

Welcome Home RateBreak

This is a "temporary buydown" program funded by the lender. With RateBreak, Rocket lowers your interest rate by 2% in the first year and 1% in the second year. For example, if your note rate is 7%, you pay 5% in year one and 6% in year two. This gives you significant monthly savings while you settle into your new home.

BorrowSmart

This is a program in partnership with Freddie Mac. If you qualify based on income and location, BorrowSmart provides a credit of up to $3,000 specifically for your down payment and/or closing costs. It is designed to help buyers in underserved communities or those with limited savings get their foot in the door of homeownership.

HomeReady and Home Possible mortgages

These are the standard Fannie Mae (HomeReady) and Freddie Mac (Home Possible) programs that Rocket supports. They allow for a 3% down payment and have reduced mortgage insurance rates. They are designed for creditworthy, low-income borrowers. Rocket creates a smooth interface to check your eligibility for these government-sponsored enterprise options.

FAQs About Rocket Mortgage

Q1. Is Rocket Mortgage a good company to go with?

Yes, especially if you value speed and digital convenience. They are excellent for straightforward loan files (W-2 employees with good credit). However, if you have a very complex financial situation or are hunting for the absolute lowest interest rate regardless of service quality, you might want to shop around.

Q2. What bank is behind Rocket Mortgage?

There isn't a traditional "bank" behind them. Rocket Mortgage is a non-bank lender and is part of Rocket Companies (NYSE: RKT). They fund their own loans and often sell them to government-sponsored entities like Fannie Mae or Freddie Mac after closing, though they typically retain the "servicing" (meaning you still pay them).

Q3. What credit score is needed for Rocket Mortgage?

Generally, you need a minimum credit score of 620 for a conventional loan. However, for FHA loans and VA loans, Rocket Mortgage can often work with scores as low as 580. Keep in mind that a higher score will always get you a better interest rate.

Conclusion

Rocket Mortgage continues to dominate the market in 2026 for a reason: they make getting a mortgage incredibly easy. Their app is top-tier, and programs like ONE+ and RocketRentRewards show they are actively trying to solve affordability issues for modern buyers. However, that convenience can come with higher rates compared to local credit unions.

If you are a borrower looking to ensure you get the best deal, I highly suggest you don't stop here. You can compare rates from multiple lenders instantly on Bluerate to see how Rocket stacks up against the competition. Additionally, speaking directly with a local loan officer can often unlock deals that aren't advertised online. Do your homework, compare the numbers, and choose the option that saves you the most money in the long run.

People Also Read

- [Proven] How to Generate Mortgage Leads for Free? 6 Methods

- 8 Best Mortgage Lead Generation Companies in 2026: Don't Miss

- 6 Best Loan Origination Software for LOs/Brokers in 2026

- 6 Best Mortgage CRM for Brokers, Lenders, MLOs in 2026

- [Tips] Where to Buy Mortgage Leads? Warm Leads for LOs

![[Proven] How to Generate Mortgage Leads for Free? 6 Methods](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/69329d01f2ad175a87d0d88b_how-to-generate-mortgage-for-free.png)