Written by

Eric

Share this article

.svg)

Subscribe to updates

Buying a house in 2026 feels like a wild rollercoaster. One minute you're browsing dream kitchens, and the next, your stomach drops looking at mortgage rates. Trust me, I know that mix of excitement and sheer panic. When I bought my first place, I was terrified of making a massive financial mistake.

That's why I put together these practical, no-nonsense tips. Forget the generic checklists. As someone who has been exactly where you are right now, I want to share the real-world advice you actually need to protect your wallet and keep your sanity intact.

Key Takeaways

- Your monthly payment is just the baseline. Don't forget property taxes, maintenance, and insurance.

- Never skip the home inspection. Even if the market is crazy, waiving this can bankrupt you.

- Compare at least three lenders. Loyalty to your current bank usually means paying higher interest rates.

- Check your "first-time" status. You might qualify for rookie perks even if you've owned property before.

Basic Requirements: What Qualifies You as a First-Time Home Buyer?

Before we jump into the tips, let's clear up a massive misconception. A lot of folks think "first-time buyer" strictly means you've never owned real estate in your entire life. That's actually not true. The U.S. Department of Housing and Urban Development (HUD) uses something called the "three-year rule."

Basically, if you haven't owned a primary residence in the past three years, the government considers you a first-timer again. This same rule applies to single parents or displaced homemakers who only owned a place with an ex-spouse. Why does this technicality matter? Because fitting this definition unlocks access to serious perks, think lower down payments, special grants, and tax breaks. Don't assume you don't qualify just because you had a house a decade ago.

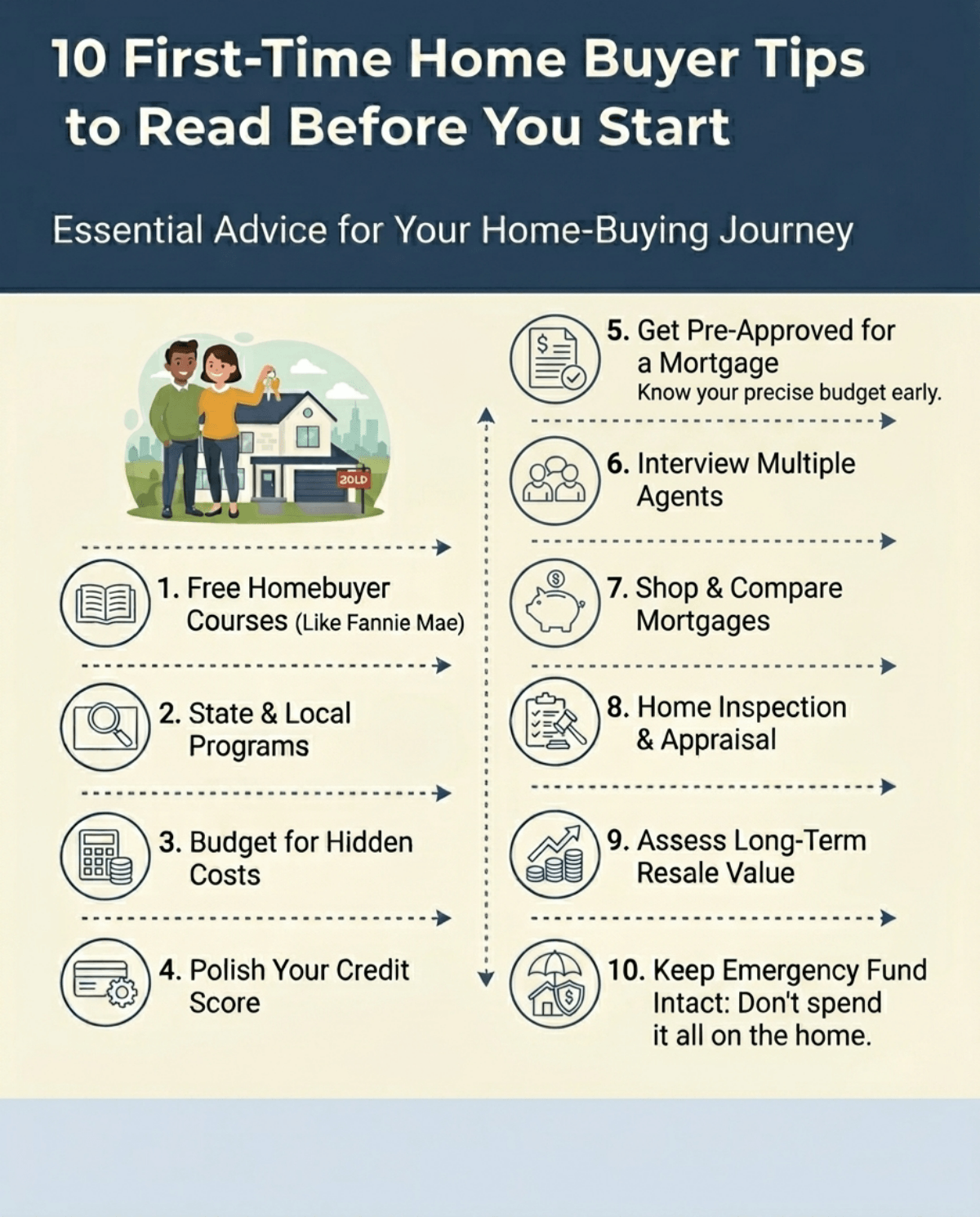

10 First-Time Home Buyer Tips to Read Before You Start

Now, let's walk through 10 tips below one after one.

Tip 1: Take Advantage of Free Homebuyer Education Courses (Like Fannie Mae)

I get it. Homework sounds boring when you just want to go look at open houses. But spending a Saturday afternoon on a free course will literally save you thousands. Fannie Mae offers a fantastic, totally free program called HomeView.

It breaks down all the confusing mortgage jargon, explains the closing process, and teaches you how to spot red flags. You can knock it out in about three hours. Here is the best part: simply completing this course actually helps you qualify for specific mortgage assistance programs or even snag a lower interest rate. I wish someone had told me this earlier. Taking the time to educate yourself is the easiest way to stop feeling intimidated by real estate agents and loan officers.

Tip 2: Research State and Local First-Time Homebuyer Programs

Please, whatever you do, don't leave free money sitting on the table. Almost every state, and even specific counties, run programs heavily subsidizing first-time buyers. They want you to buy a house!

You can find Down Payment Assistance (DPA) grants, reduced interest rates, or even tax credits just for living in a specific zip code. Some places offer zero-interest loans that cover your entire down payment, and if you stay in the house for a few years, they forgive the debt completely. It's basically free cash.

Of course, there's a catch. These perks usually have strict income caps and purchase price limits, meaning you probably won't qualify if you're pulling in a massive salary or trying to buy a mansion. Do yourself a favor: spend an hour Googling your state's local Housing Finance Agency (HFA). Dig into their website and see what you qualify for. Finding the right grant could literally cover your closing costs.

Also Read:

- Best First-Time Home Buyer Programs: Get the Right Choice

- What is Down Payment Assistance? Everything to Learn Here

- Guide: How to Apply for Down Payment Assistance?

Tip 3: Look Beyond the Mortgage: Budget for Hidden Costs

If you're only looking at the monthly principal and interest on a mortgage calculator, you're setting yourself up for a nasty surprise. Homeownership comes with a mountain of hidden fees that renters never see.

First off, if your down payment is under 20%, the bank will likely slap you with Private Mortgage Insurance (PMI)—a monthly fee that protects them, not you. Then add in property taxes, which can jump up wildly depending on the area, plus homeowners insurance and pesky HOA fees. Oh, and when the dishwasher floods the kitchen? That repair bill is 100% on you now.

I always tell friends to use the old 28/36 rule. Keep your total housing expenses under 28% of your gross monthly income, and make sure your total debt (including student loans and car payments) stays below 36%. Sticking to this ratio keeps you breathing comfortably instead of becoming completely "house poor" the second you move in.

Tip 4: Polish Your Credit Score Before Pre-Approval

Your credit score dictates almost everything in real estate. Even a tiny 0.5% bump in your interest rate can bleed tens of thousands of extra dollars out of your pocket over a 30-year loan.

So, long before you talk to a lender, you need to babysit your credit. Pull your free report to check for weird errors. Pay your bills early and try to get your credit utilization under 30%.

But here is the most important advice I can give you: once you decide to buy a house, put your financial life in a deep freeze. Do not finance a new car. Do not open a Home Depot credit card to buy a lawnmower. Do not close your oldest credit card account. Any sudden change messes up your debt-to-income ratio. I've personally seen friends lose their dream house a week before closing because they bought a new truck on finance and the lender pulled their loan. Keep it boring.

Tip 5: Strategize Your Down Payment and Closing Costs

Let's kill the biggest real estate myth right now: you do not need a 20% down payment. Sure, putting 20% down lets you dodge that annoying mortgage insurance, but it's unrealistic for most people today. Conventional loans actually allow first-timers to put down as little as 3%. An FHA loan lets you get in with just 3.5% down if your credit score is 580 or higher (or 10% down if it's 500-579).

But here is the part that catches rookies off guard—closing costs. You might scrape together your down payment, only to find out you need thousands more to actually finalize the deal. Closing costs cover things like the title search, appraisal fees, and local taxes. In 2026, expect these to run somewhere between 2% and 5% of your total loan. So, if you're eyeing a $350,000 place, you need an extra $7,000 to $17,500 sitting in the bank just to hand over the keys. Don't let this blindside you.

Tip 6: Interview Multiple Real Estate Agents to Find Your Advocate

Trying to buy a house without an agent is like representing yourself in court—just a really bad idea. You need a dedicated buyer's agent fighting in your corner. They aren't just tour guides who unlock doors. A great agent points out a sagging roof, knows what a fair price is, and handles the brutal negotiations.

Recently, the rules around who pays the buyer's agent commission have shifted, so you'll need to hash out how they get paid right off the bat. Because of this, you absolutely must shop around. Treat it like a job interview. Call up at least three different agents. Ask them how many first-timers they've worked with and see if they actually know your target neighborhoods. You want someone who has the guts to tell you, "This house is a money pit, let's leave," not a yes-man who just wants a quick paycheck. Take your time finding the right fit.

Tip 7: Shop Around and Compare Mortgage Lenders

A lot of people just walk into the local branch of their checking account bank and ask for a mortgage. Big mistake. Banks rarely offer you a "loyalty discount," and their first offer is almost never the best one. You have to pit them against each other.

Make it a goal to apply with at least three different lenders: try a big bank, a local credit union, and an online mortgage broker. When they hand you their official Loan Estimates, don't just look at the big, bold interest rate. Look closely at the APR (Annual Percentage Rate).

The APR tells you the actual cost of borrowing the money because it bakes in all those sneaky underwriting fees and origination charges. Sometimes a loan with a slightly lower rate has ridiculous hidden fees attached. Comparing these documents side-by-side gives you massive leverage to negotiate away junk fees and lock in the cheapest possible loan.

Tip 8: Never Skip the Home Inspection and Appraisal

Once your offer gets accepted, you face two big hurdles. An appraisal is when the bank sends someone to confirm the house is actually worth the $400,000 they are lending you. A home inspection, on the other hand, is entirely for your own safety.

You pay a pro to crawl under the house, poke the roof, and find out if the electrical wiring is a fire hazard. Sometimes, in a crazy hot market, real estate agents might hint that you should waive the inspection to make your offer look stronger. Do not do it. Ever. Waiving your inspection means you are buying the place totally "as-is." I've seen people do this and get hit with a $15,000 foundation repair bill the week they moved in.

I also suggest bringing your own checklist during the tour. Run the taps, look under sinks for water damage, and flush the toilets. Protect yourself first.

Tip 9: Assess the Long-Term Resale Value and Financial Impact

It's super easy to fall head over heels for a place just because it has a stunning kitchen island. But you have to think like an investor. Life happens fast. You might change jobs, have kids, or just outgrow the space, which means you could be slapping a "For Sale" sign in the yard five years from now.

To make sure you don't lose money later, obsess over the location. Check out the local school districts, even if you don't plan on having kids, buyers in the future will care. Look up crime maps and see what's being built nearby. A slightly outdated house in an amazing school district is a way better investment than a gorgeous flip in a declining neighborhood.

Also, try to buy the ugliest house on a great street, rather than the fanciest house on a bad one. Your home's value is dragged up, or down, by your neighbors.

Tip 10: Keep Your Emergency Fund Intact After Closing

Emptying your entire bank account just to cover the down payment and closing costs is incredibly dangerous. Being "house rich and cash poor" is a miserable way to live.

The second you get those keys, I promise you, money will start flying out the window. You'll need cash for movers, maybe a lawnmower, new locks, and a couple of paint cans. And that's before things start breaking. During my first month in my new place, the water heater completely died on a Sunday night. If I hadn't saved a financial cushion, I would have had to put a massive emergency plumbing bill on a credit card at 24% interest.

When you are doing your budget math, make sure that after you sign all the closing papers, you still have at least three to six months' worth of living expenses sitting untouched in a high-yield savings account. That cash is your ultimate peace of mind.

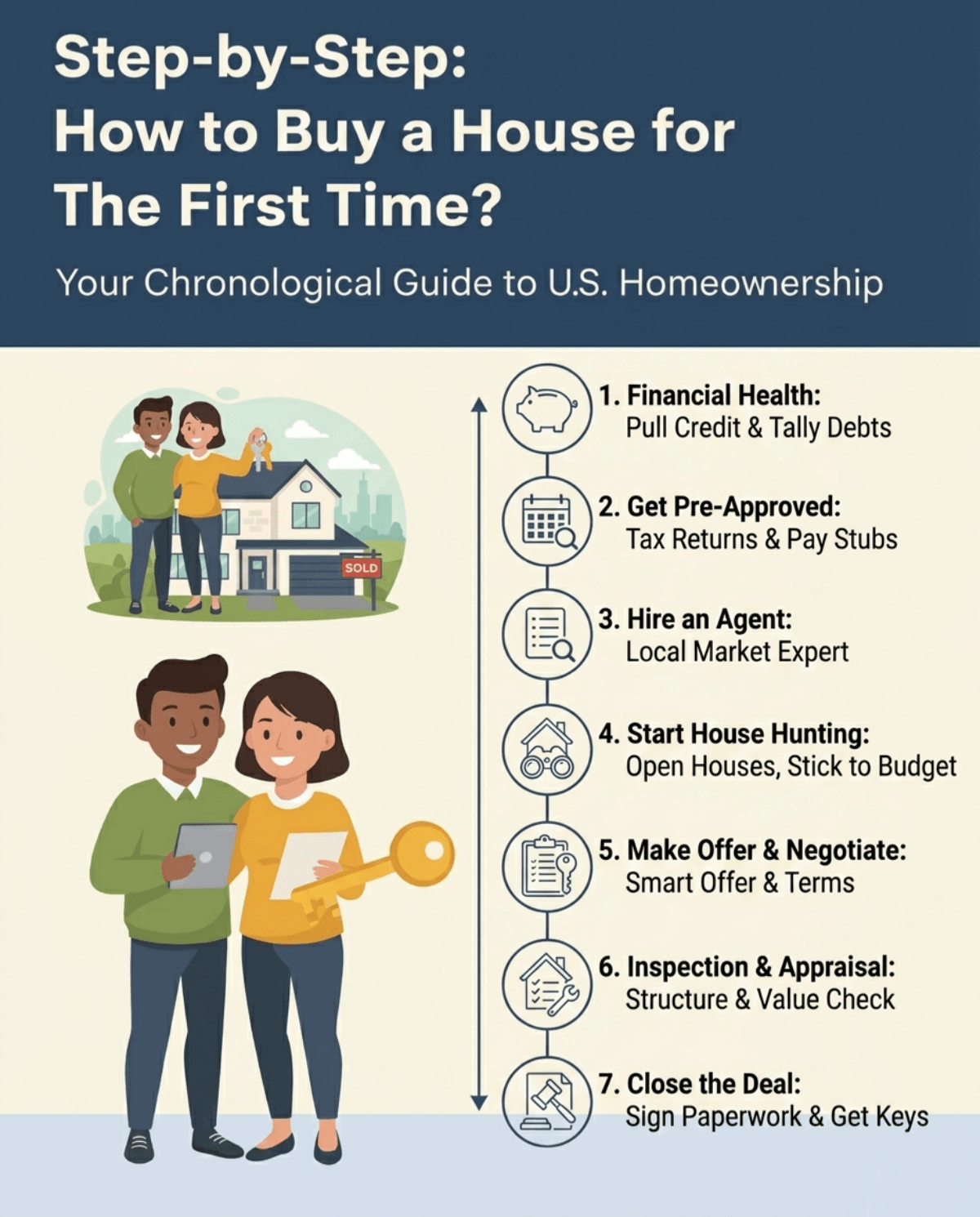

Step-by-Step: How to Buy a House for the First Time?

Figuring out the order of operations can cure half of your home-buying anxiety. Here's a clear, chronological breakdown of how the process actually works in the U.S.:

Also Read: Ultimate Guide: How to Buy a House for the First Time?

- Check your financial health: Pull your credit score, tally up your debts, and figure out a monthly payment you won't lose sleep over.

- Get a rock-solid pre-approval: Hand over your tax returns and pay stubs to a lender so they can officially tell you how much they'll let you borrow.

- Hire an awesome real estate agent: Find someone who knows your local market inside and out.

- Start house hunting: Hit the open houses, but stick to your budget.

- Make an offer and negotiate: Found the one? Work with your agent to write a smart offer.

- Do the inspection and appraisal: Make sure the house isn't falling apart and the bank agrees on the price.

- Close the deal: Sign a huge stack of paperwork, wire the closing funds, and grab your keys!

FAQs for First-Time Homebuyers

Q1. What are the biggest first-time home buyer mistakes?

The absolute biggest mistake is draining your savings account down to zero, leaving nothing for sudden repairs. Another huge trap is looking only at the monthly mortgage payment while ignoring taxes, HOA fees, and upkeep. Finally, never ruin your loan approval by financing a new car or opening credit cards right before closing.

Q2. What is the first thing you should do when you buy a new house?

Before buying, your very first move should be getting a mortgage pre-approval so you know your actual budget. But physically? The very first thing you do the moment you get the keys is change all the exterior locks. You have no idea how many neighbors or contractors still have spare keys from the previous owners.

Q3. What is the best advice for buying a house?

Keep your emotions in check. It's incredibly easy to fall in love with a backyard and overlook a rotting roof, or get dragged into a nasty bidding war because you feel competitive. Treat this like a strict business deal. Stick to your budget, rely on your inspection report, and be willing to walk away.

Q4. How much of a down payment do I really need?

You definitely don't need 20%. While putting 20% down avoids Private Mortgage Insurance (PMI), conventional loans allow first-timers to buy with just 3% down. Government-backed FHA loans only require a 3.5% down payment. If you qualify for VA or USDA loans, you might even be able to put 0% down.

Q5. What is the minimum credit score for a first-time home buyer?

It really depends on the loan. For an FHA loan with a 3.5% down payment, you generally need a minimum score of 580 (or 500-579 with 10% down). Standard conventional loans usually require at least a 620. That said, aiming for a 700 or higher will unlock much better interest rates, saving you serious money over the long haul.

Conclusion

I'm not going to lie to you, buying a house is a stressful, exhausting process. There will be days when you want to throw your hands up and just rent forever. But pushing through that frustration is worth it. As long as you stick to your budget, don't skip the inspections, and lean on a solid real estate agent, you're going to be just fine.

The secret to a smooth transaction is getting your ducks in a row early. Don't wait until you find a house you love to check your credit. Take action right now. Pull your credit report today, figure out how much you can really afford, or go sign up for that free Fannie Mae course. Your future self will definitely thank you for the head start!

People Also Read

- Mortgage Rates Impact Affordability: The Lower, The Better

- [Tutorial] How to Estimate What Mortgage You Can Afford?

- How to Calculate Mortgage Interest: Manually & Automatically

- Ultimate Guide: How to Calculate Monthly Mortgage Payment?

- Must-Read Tips for Paying Off Mortgage Early

- Make Extra Payments on Mortgage: Is It Worth It?