Written by

Eric

Share this article

.svg)

Subscribe to updates

When I bought my first vacation home, I realized that predicting short-term rental earnings is nothing like calculating steady, long-term leases. The income fluctuates with tourist seasons, varying booking rates, and unexpected operational fees. To protect your investment, you need an accurate forecasting method. In this guide, I will walk you through a clear, step-by-step approach to calculating your true rental income.

Key Takeaways

- Calculate true profit by subtracting operating costs from gross nightly and ancillary revenues.

- For many Fannie Mae-style rental income calculations, lenders may use 75% of gross monthly rent, with the remaining 25% reserved for vacancy, maintenance, and management costs.

- Properties with an average guest stay of seven days or less may qualify for the short-term rental exception under the passive loss rules, but deductibility against active income still depends on material participation and other IRS requirements.

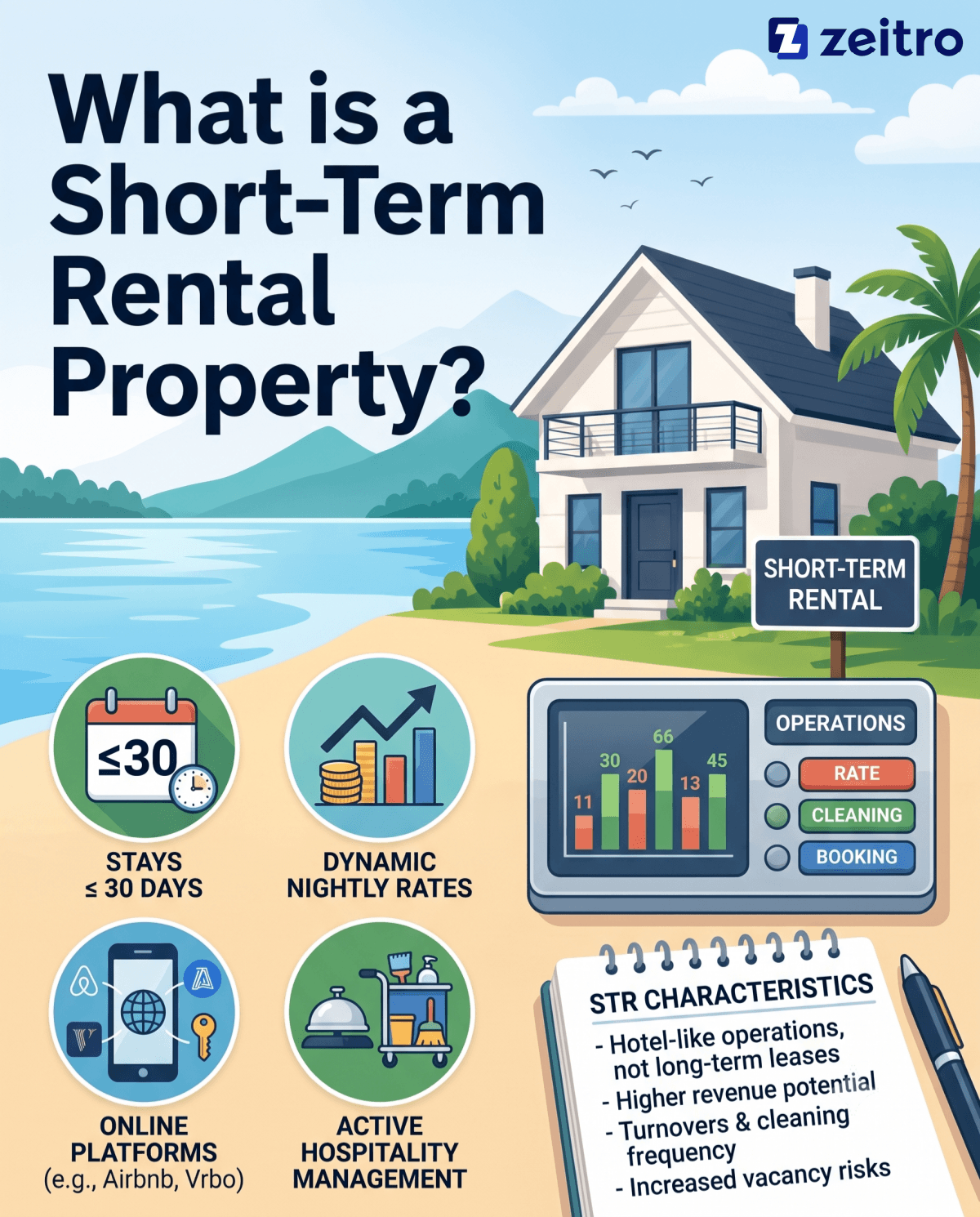

What is a Short-Term Rental Property?

In practice, short-term rentals are commonly defined by stays of 30 days or less, but tax and mortgage treatment in the United States depends on the specific program, lender, and IRS rules. Unlike traditional year-long leases, these properties function more like boutique hotels.

They rely heavily on vacation platforms such as Airbnb and Vrbo to attract travelers. The primary differences lie in booking frequency and operational hands-on management. Instead of receiving a fixed monthly check, I must manage fluctuating nightly rates, high guest turnover, and continuous cleaning requirements.

While this dynamic model offers much higher revenue potential, it also comes with increased vacancy risks and demands active hospitality management to keep the property profitable.

How to Calculate Income for a Short-Term Rental Property?

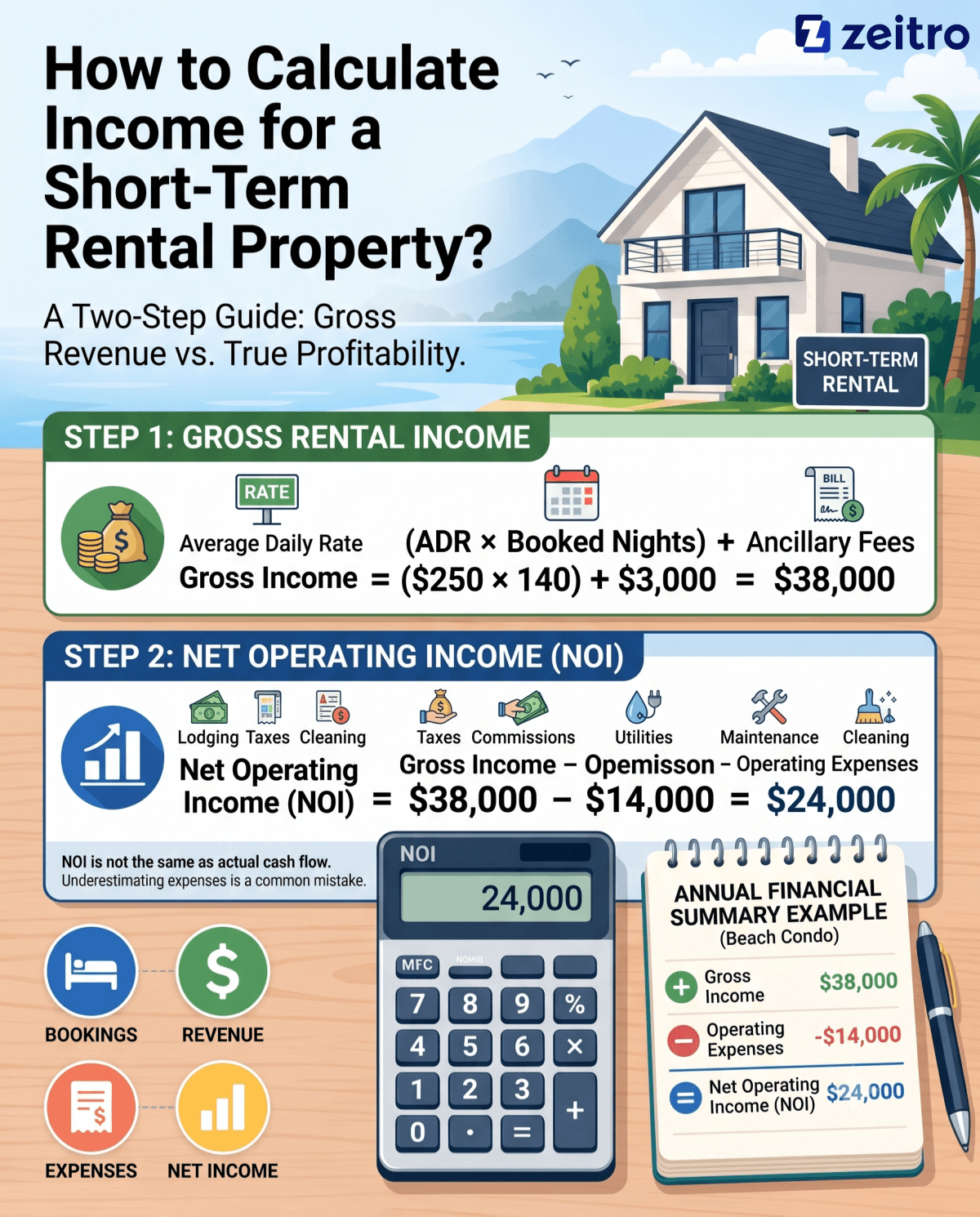

To find your property's actual financial performance, you must look beyond top-line revenue. I break this calculation down into two steps: finding gross rental income and determining net operating income. Gross income includes your nightly room rates plus all extra fees guests pay.

Net Operating Income (NOI) measures operating performance before debt service and income taxes, so it is not the same as actual cash flow. Subtracting expenses like local lodging taxes, platform commissions, insurance, utilities, and property maintenance from your gross earnings reveals your true profitability. Underestimating these operational expenses is a common mistake that can easily turn a promising investment into a monthly liability.

- Gross Income=(ADR×Booked Nights)+Ancillary Fees

- Net Operating Income (NOI)=Gross Income−Operating Expenses

Example:Let's look at a real-world scenario. Suppose your beach condo has an Average Daily Rate (ADR) of $250 and is booked for 140 nights a year, generating $35,000 in base revenue. You also collect $3,000 in cleaning and pet fees, bringing gross income to $38,000. If your annual operating expenses, including cleaning services, utilities, and Airbnb fees, total $14,000, your Net Operating Income is $24,000.

Tip: If you need help predicting occupancy rates or average daily rates in your market, try utilizing the AirDNA Airbnb Calculator to get accurate, hyper-local projections.

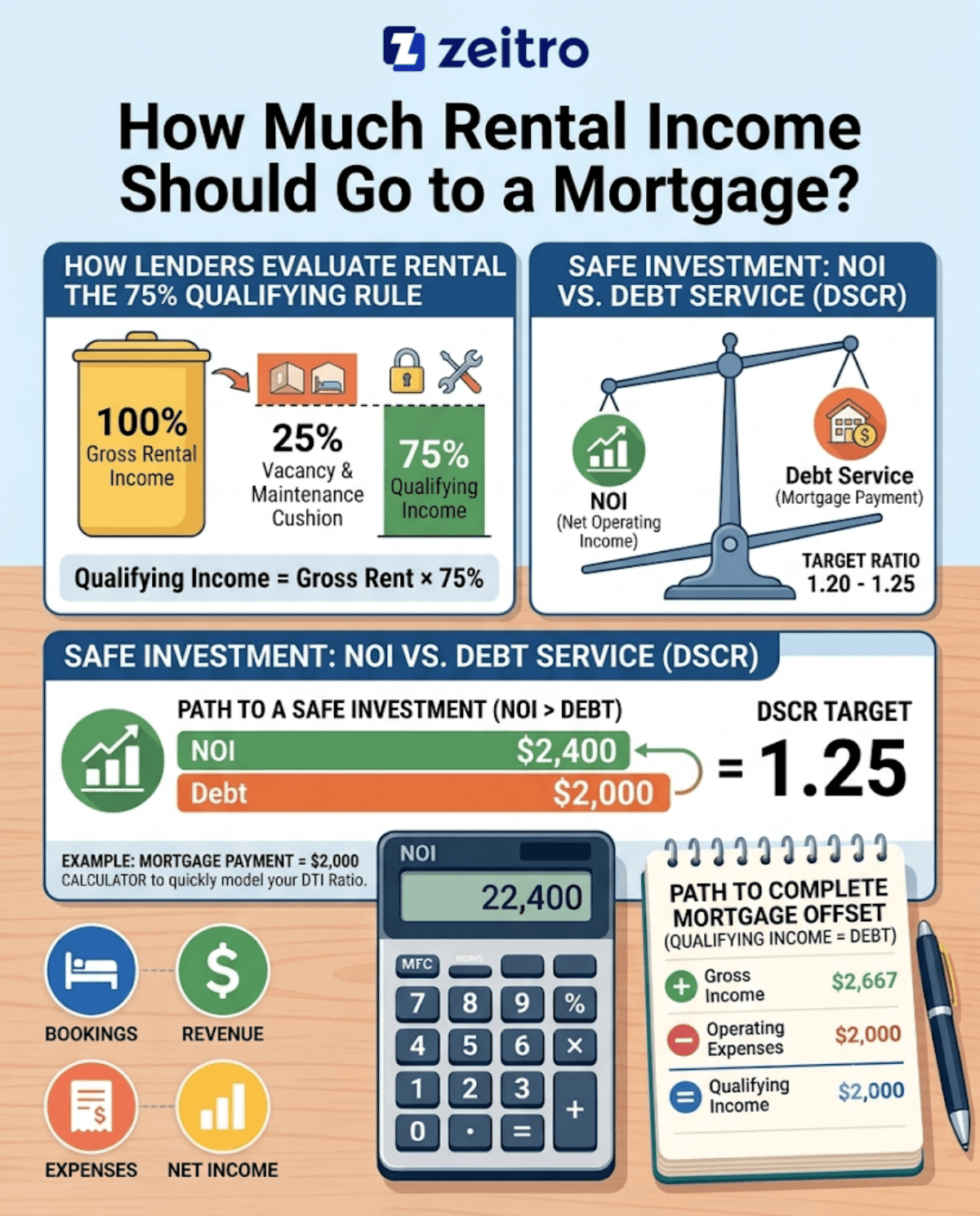

How Much Rental Income Should Go to a Mortgage?

When financing a property, I have to look at how lenders evaluate my rental income. For standard conventional loans in the United States, underwriting guidelines like those from Fannie Mae typically apply a 75% factor to your projected rental revenue.

Lenders deduct a 25% cushion to account for potential vacancy and ongoing property maintenance. This means only 75% of your projected gross rent can be used to offset your mortgage payment during the qualification process. Many lenders look for a DSCR around 1.20 to 1.25, but the exact threshold varies by lender and loan program.

Example:For example, if your monthly mortgage payment is $2,000, your property needs to generate at least $2,400 in net monthly operating income to be considered a safe investment. Meanwhile, a lender applying the 75% qualifying rule would require a gross projected rent of $2,667 to completely offset that $2,000 mortgage payment on your loan application.

Tip: To quickly model how lenders will calculate your qualifying debt-to-income ratio, you can use the Zeitro Mortgage Rental Income Calculator.

What is the Loophole for Short-term Rental Income?

The short-term rental tax loophole is one of the most powerful strategies I use to minimize tax burdens in the United States. Under IRS regulations, rental activities are generally classified as passive, meaning you cannot use rental losses to offset active W-2 or business income. However, if your property qualifies as a business rather than a rental activity, you can deduct non-cash losses like depreciation directly against your active income. To qualify for this tax benefit, you must meet specific federal requirements:

- The 7-Day Rule: The average stay of your guests over the tax year must be seven days or fewer.

- Material Participation: You must actively manage the property, spending at least 100 hours on it annually and more than anyone else, or 500 hours overall.

- Accurate Logging: Accurate logging is strongly recommended, because contemporaneous records help substantiate material participation if the IRS reviews the return.

FAQs About Short-Term Rental Property Income Calculation

Q1. How do I estimate the average occupancy rate for a new short-term rental?

I look at comparable local listings on platforms like Airbnb or Vrbo, analyzing their booking calendars over different seasons to calculate a conservative average.

Q2. Are cleaning fees considered taxable income?

Yes, any fee you charge guests is part of your gross taxable revenue. Fortunately, you can deduct the actual payments made to your cleaners as business expenses.

Q3. What is a healthy Debt Service Coverage Ratio (DSCR) for a rental property?

Most investment property lenders look for a DSCR of 1.20 or higher, indicating the property generates 20% more net income than its mortgage payments.

Q4. Can I use short-term rental income history to qualify for a new home loan?

Documentation requirements vary by transaction type and lender. Some loans may rely on Schedule E, while others use lease agreements or market rent documentation.

Q5. Does the standard 50% rental expense rule apply to short-term properties?

No. Operating expense ratios vary widely by property and market, so investors should model actual expenses rather than rely on a fixed percentage rule.

Conclusion

Calculating income for a short-term rental requires a detailed approach, but getting the numbers right is incredibly rewarding. By shifting focus from simple gross revenue to actual net operating income, you can make smarter investment choices.

Remember to account for strict mortgage lending rules and take advantage of available tax strategies like the seven-day loophole. I always recommend using data-driven tools and consulting with a specialized CPA to back up your math. With a solid financial foundation, your vacation rental can become a highly profitable addition to your real estate portfolio.

People Also Read

- How Do Loan Officers Calculate Rental Income from Schedule E?

- Can Rental Income Offset a Mortgage? Lender Rules & Requirements

- Can Projected Rental Income be Used for a Mortgage?

- How Much Rental Income Can Be Used for Qualification?

- How Do Underwriters Treat Rental Losses? An Ultimate Guide