Written by

Eric

Share this article

.svg)

Subscribe to updates

A Reddit thread in r/Mortgages titled "Ask the Underwriter: Can I use future rental income?" caught my attention recently. Many home buyers are surprised to learn that lenders do allow you to use expected rental income to qualify for a home loan. Yes, you can use projected rent, but as an underwriter, I can tell you that the rules are strict. Let's dive in.

Key Takeaways

- The 75% Rule: For many conventional loans, lenders use 75% of gross market rent or lease rent to account for vacancy and ongoing expenses, but the exact treatment depends on the loan program and property type.

- Professional Appraisal Required: Lenders commonly use market rent supported by an appraisal, such as Fannie Mae Form 1007 for 1-unit properties or Form 1025 for 2–4-unit properties.

- Experience & Reserves Matter: Landlord history and liquid cash reserves strongly influence how much of this income lenders will credit to you.

- Loan Types Vary: Conventional, FHA, and DSCR loans have very different standards for future rental income.

Can I Use Future Rental Income to Qualify for a Mortgage?

Yes, you can absolutely use future rental income to qualify for a mortgage. When you purchase an investment property or a multi-unit home, lenders understand that the property will generate cash flow. By allowing you to use projected rent, we can offset the property's monthly mortgage payment (PITI). This effectively lowers your Debt-to-Income (DTI) ratio, making it much easier for you to qualify for a larger loan or secure the mortgage on your new investment.

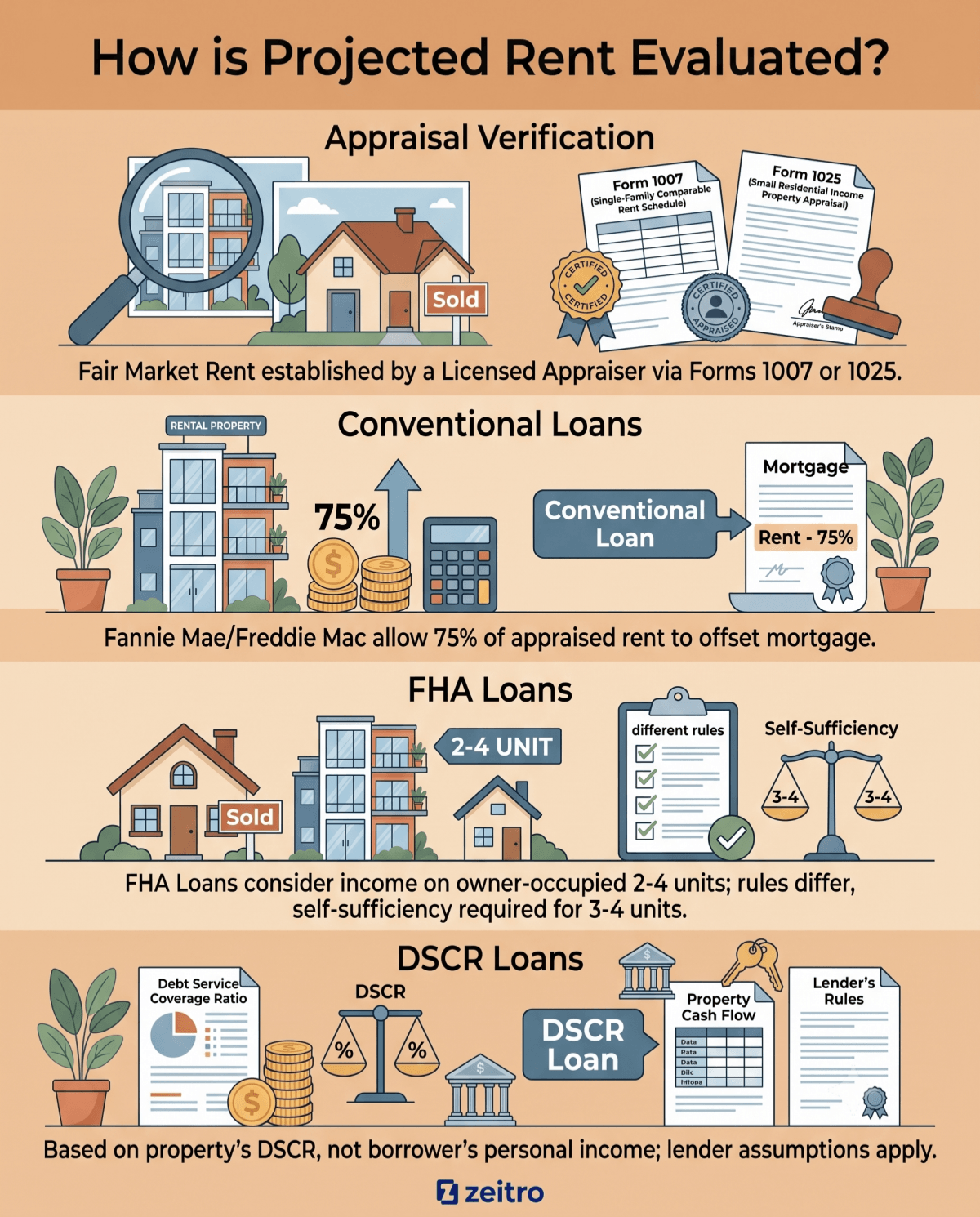

How is Projected Rent Evaluated?

To determine how much projected rent can be credited to your application, lenders rely on a formal valuation rather than your personal estimates. Here is how we evaluate it:

- Appraisal Verification: A licensed appraiser must complete a Single-Family Comparable Rent Schedule (Fannie Mae Form 1007) for 1-unit properties, or Form 1025 for 2-to-4-unit properties to establish fair market rent.

- Conventional Loans: Fannie Mae and Freddie Mac allow 75% of this appraised market rent to offset the mortgage payment.

- FHA Loans: For FHA loans, rental income may be considered on owner-occupied 2–4 unit properties, but the documentation and underwriting rules are different from conventional loans, and 3–4 unit properties may also be subject to self-sufficiency requirements.

- DSCR Loans: DSCR loans typically underwrite based on the property's debt service coverage ratio rather than the borrower's personal income, and lenders may apply their own rent and expense assumptions.

What Do Lenders Require for Projected Rental Income?

While projected rent is incredibly helpful, underwriting guidelines are built to mitigate risk. Lenders look closely at two major requirements:

- Liquid Reserves: Reserve requirements vary by loan program, occupancy type, and borrower profile. Lenders may require anywhere from a few months of PITIA reserves to much more in certain cases.

- Landlord Experience: Under Fannie Mae guidelines, rental-income treatment depends on the borrower's housing payment, the property type, and documentation of rental history or management experience. Without rental management experience, some lenders may limit how much projected rent can be counted, but the exact treatment depends on the loan program and supporting documentation

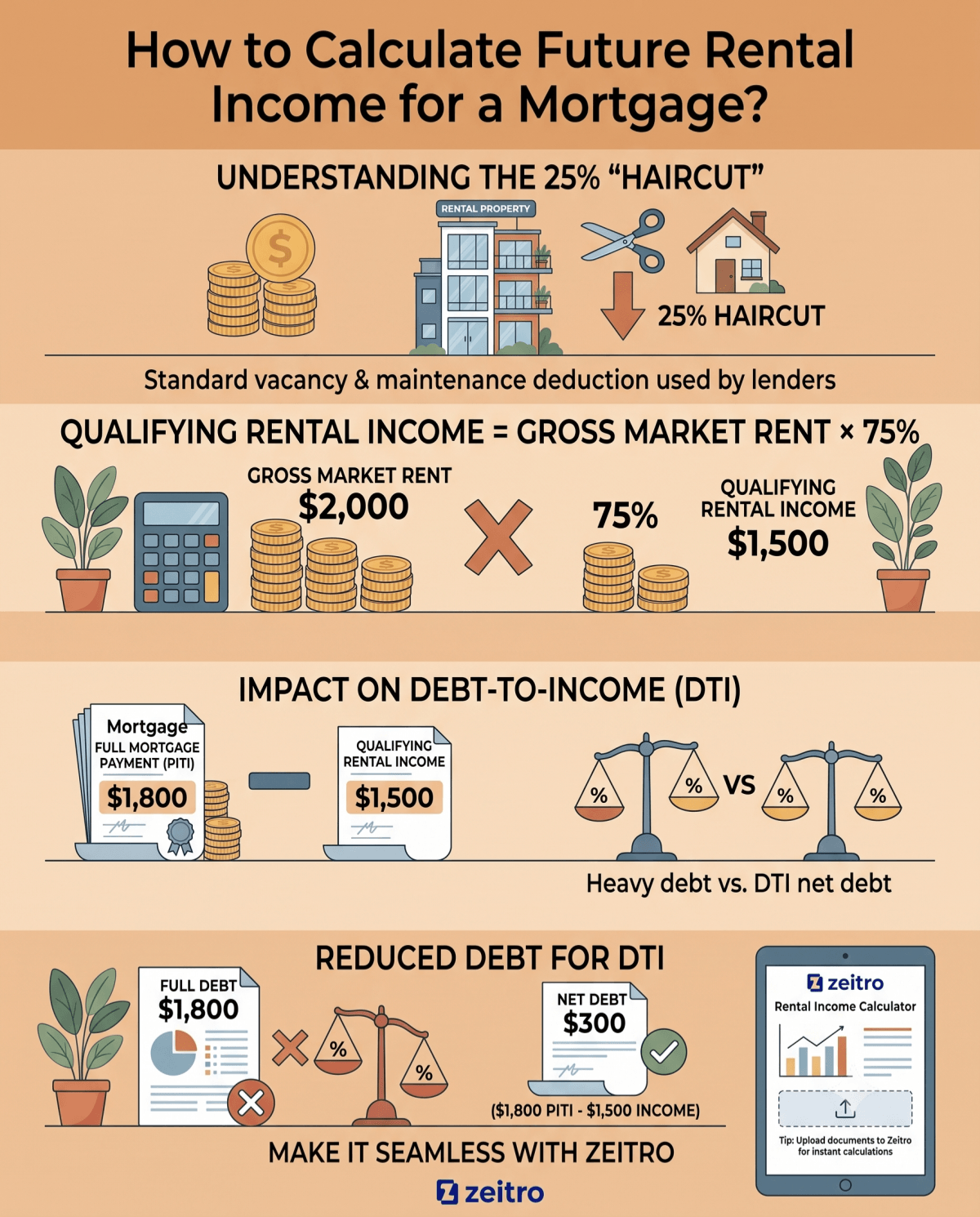

How to Calculate Future Rental Income for a Mortgage?

Calculating your qualifying rental income is straightforward. Lenders apply a standard 25% haircut to cover potential vacancies and maintenance costs:

A simplified conventional guideline is Qualifying Rental Income = Gross Market Rent × 75%, but actual DTI treatment also depends on the property's housing expenses and the applicable underwriting rules.

For example, if your appraiser establishes the fair market rent at $2,000 per month, your qualifying income is:

$2,000×0.75=$1,500

If your monthly mortgage payment (PITI) is $1,800, we subtract the $1,500 qualifying rent, leaving only a $300 net debt to count against your DTI, rather than the full $1,800.

Tip: To make this process seamless, you can upload your financial documents to the Zeitro Rental Income Calculator. It instantly handles these complex DTI calculations and gives you a clear picture of your qualifying power.

FAQs About Projected Rental Income

Q1. What is the 2% rule for rental income?

The 2% rule is a quick screening tool used by investors. It suggests that a rental property's monthly rent should equal at least 2% of its total purchase price. While a great benchmark for cash flow, it is incredibly difficult to find in today's high-priced U.S. markets, and lenders do not use this rule for formal mortgage qualification.

Q2. What is the 50% rule in rental income?

The 50% rule states that you should expect a property's operating expenses, like taxes, insurance, maintenance, and property management, to consume about half of its gross rental income, excluding the mortgage payment itself. Lenders don't use this rule to qualify you, but it is a wise way for you to budget for real-world costs.

Q3. Do I need a signed lease agreement to use projected rental income?

Not always. If you are buying a vacant investment property, a licensed appraiser's Form 1007 is usually enough to establish projected income. Documentation requirements vary by scenario. Some cases require a fully executed lease, while others rely on appraised market rent from Form 1007 or 1025.

Q4. Can I use projected rental income from my departing primary residence?

Yes, you can. If you are converting your current home into a rental to buy a new primary residence, you can use the projected rent to offset the old mortgage. You will need a signed lease agreement and proof of a security deposit. Fannie Mae does not apply a universal 25% equity requirement to all departing residences. Eligibility depends on the borrower's housing payment, documentation, and rental-management history.

Q5. Can I qualify if I have zero landlord experience?

Absolutely. While having at least one year of property management experience is ideal and unlocks better treatment of surplus rental income, first-time landlords are welcome. If you have zero experience, the projected rent can still be used to offset the new property's mortgage payment to zero, preventing it from hurting your personal DTI.

Conclusion

Leveraging projected rental income is one of the smartest ways to scale your real estate portfolio without letting your DTI hold you back. However, navigating the strict requirements of appraisals, reserves, and landlord history requires careful preparation.

By understanding how underwriters view these numbers, you can set yourself up for a smooth approval. I highly recommend consulting a licensed mortgage broker who specializes in investment properties to review your specific scenario and map out the best path forward.

People Also Read

- How Do Loan Officers Calculate Rental Income from Schedule E?

- Can Rental Income Offset a Mortgage? Lender Rules & Requirements

- How Much Rental Income Can Be Used for Qualification?

- How Do Underwriters Treat Rental Losses? An Ultimate Guide