Written by

Eric

Share this article

.svg)

Subscribe to updates

Are you gearing up to buy a home? You need to understand one crucial number before falling in love with a property. Your mortgage debt-to-income ratio (DTI) is the ultimate measuring stick lenders use to evaluate your financial health. Simply put, it compares your monthly earnings to your monthly debt obligations.

In my experience, many buyers hyper-focus on their credit scores while completely ignoring this metric. But here is the truth: this percentage is arguably the most critical factor deciding your loan approval. Read on to discover exactly how to calculate your own ratio and see if you meet the latest guidelines.

What is a Debt-to-Income Ratio for a Mortgage?

When I sit down with a prospective buyer, the first thing I explain is that a debt-to-income ratio is simply a personal finance measure. It compares your gross monthly income to your required monthly debt payments. Lenders split this into two distinct categories:

- Front-end ratio (Housing Ratio): This strict metric only looks at your expected housing expenses. It includes the PITI—Principal, Interest, Taxes, and Insurance—along with any HOA fees.

- Back-end ratio (Total Debt Ratio): This is the broader picture. It adds your projected housing payment to all other recurring monthly debts, such as credit card minimums, auto loans, and student loans.

I always emphasize to my clients that while both numbers matter, lenders care significantly more about your back-end ratio. It gives us the truest picture of your overall financial burden.

How to Calculate Debt-to-Income Ratio?

You don't need a finance degree to figure out your standing. Grab a calculator and follow a simple set of steps. First, tally up all your minimum required monthly debt payments. Next, divide that total by your gross monthly income, which is the money you make before taxes and deductions are taken out. Finally, multiply the result by 100 to get your percentage.

The formula looks like this: DTI = (Total Monthly Debt Payments / Gross Monthly Income) x 100

One crucial thing I always point out: do not use your total outstanding loan balances. You only need to calculate the minimum monthly payments due. If you owe $10,000 on a car but your monthly bill is $300, you only use the $300 for this math.

Debt-to-Income Ratio for a Mortgage Example

Let's look at a realistic scenario. Meet John, a client who wants to purchase his first house. His gross monthly income before taxes is $8,000.

Now, let's add up his monthly obligations:

- Auto loan payment: $400

- Credit card minimums: $200

- Estimated new mortgage payment (PITI): $2,200

John's total monthly debt payments equal $2,800. To find his back-end percentage, we divide his total debt ($2,800) by his gross income ($8,000), which equals 0.35. Multiply that by 100, and you get 35%.

Because John's ratio sits comfortably at 35%, he is in a fantastic position to secure loan approval with competitive interest rates. Doing this exact math at home will instantly reveal your purchasing reality.

Key DTI Ratios for Mortgages

Once you know your number, where do you stand? Different percentages indicate different levels of financial health to an underwriter. Here is the general breakdown I share with borrowers:

- Ideal (36% or less): You are in excellent financial shape. Borrowers in this tier rarely struggle with approval and typically snag the absolute best interest rates.

- Acceptable (37% - 43%): This is the normal range. Most lenders will approve your application here without too much friction.

- High (Above 44%): Approval gets trickier. You will likely need compensating factors, such as an excellent credit score or substantial cash reserves, to push your file through.

- The 28/36 Rule: This is a classic industry benchmark. It suggests your front-end housing costs should never exceed 28% of your income, while your back-end total debt stays under 36%.

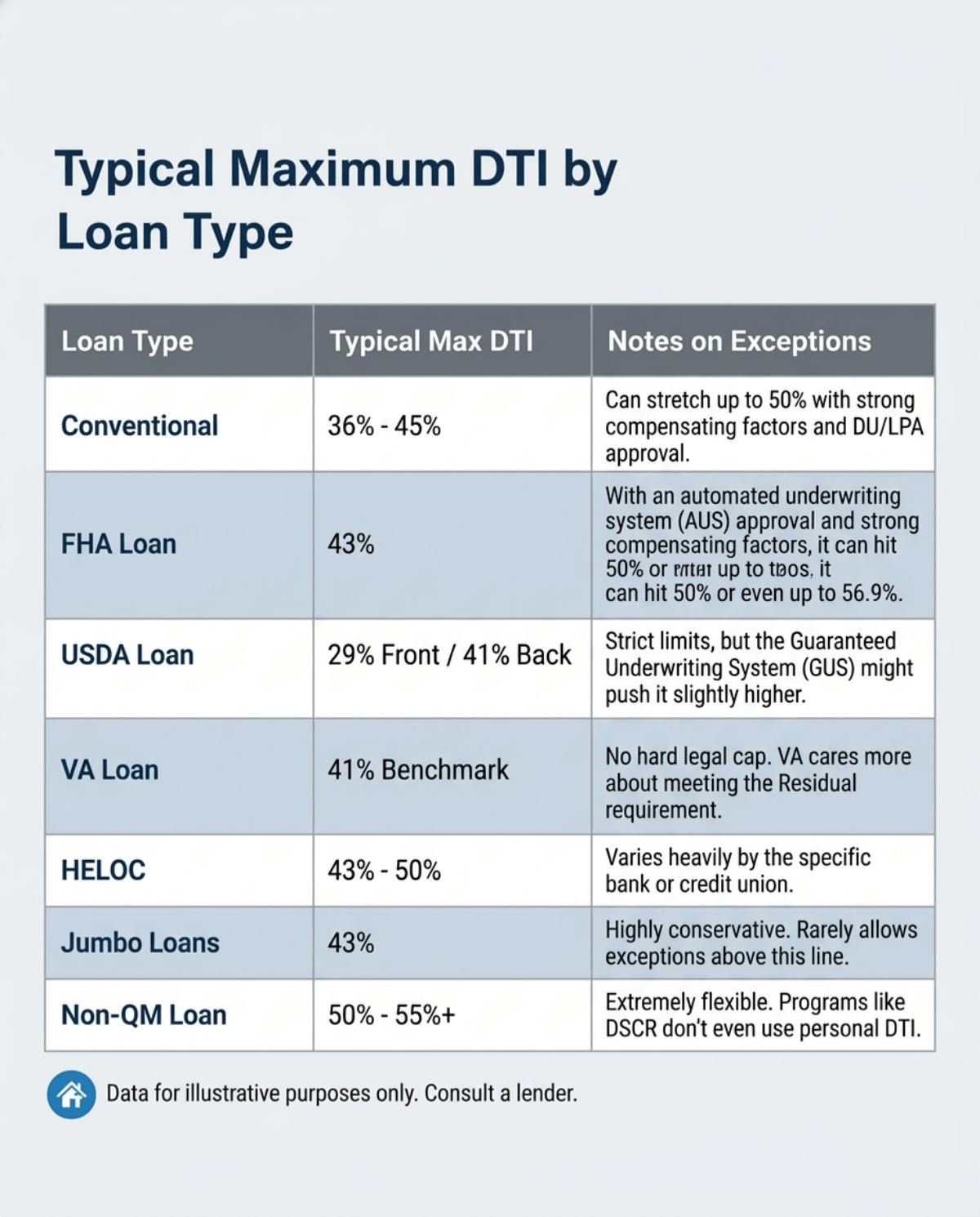

Max DTI Requirements by Loan Types

Every mortgage program has different tolerances for debt. Government-backed loans usually offer more flexibility compared to standard conventional products. Here is a quick look at the typical maximum DIT limits for the US market:

- Conventional Loan: 45% - 50% (with strong automated approval)

- FHA Loan: 43% - 50%+ (with compensating factors)

- VA Loan: No hard cap. 41% guideline (flexible with strong residual income and compensating factors).

- USDA Loan: 41% - 44% (with waiver/compensating factors)

Pro Tip: Mortgage guidelines frequently update based on market conditions. To ensure your max DTI perfectly aligns with the latest lender overlays, loan officers and mortgage professionals can quickly verify current guidelines using Zeitro Strata. It's an internal tool I highly recommend for staying perfectly compliant.

Why Does Mortgage Debt-to-Income Ratio Matter?

From a risk management perspective, a high debt load directly correlates with a higher risk of default. If you lose your job or face an emergency, heavily indebted borrowers are historically the first to miss payments. That is why this metric is deeply woven into the underwriting process.

Here is exactly how it dictates your homebuying journey:

- Loan Approval: It is the ultimate gatekeeper. If your percentage exceeds the program's cap, your application will be denied, regardless of a flawless credit history.

- Interest Rates: Lower ratios signal lower risk, allowing lenders to reward you with cheaper interest rates and better terms.

- Loan Options: Keeping your debts minimal opens up the entire market. You won't be restricted to specific high-cost government programs and can freely choose the product that best fits your long-term wealth strategy.

How Does DTI Affect Mortgage Affordability?

Beyond simple approval, your debt profile directly controls your actual purchasing power. It literally dictates how expensive of a house you can buy.

I often see high-earning professionals get frustrated because they cannot get approved for their dream home. They might make $15,000 a month, but if they have massive student loans and two luxury car leases eating up $4,000 monthly, their "effective budget" is severely compressed. The bank will strictly cap the new housing payment to ensure the total back-end ratio stays within limits.

Simply put, for every extra dollar you owe in recurring consumer debt, your maximum allowable mortgage payment shrinks. Controlling your outside liabilities is the fastest way to increase how much house you can afford.

How to Lower Mortgage Debt-to-Income Ratio?

If your math came out higher than expected, don't panic. You can actively improve your financial profile before applying. Here are the most effective strategies I advise my clients to implement:

- Pay off existing debt: Target small balances or high monthly payment loans first. Eliminating a $300 car payment drastically improves your ratio.

- Increase your gross income: Ask for a raise, pick up a side hustle, or document your freelance income. A higher denominator instantly lowers the percentage.

- Avoid taking on new credit: This is crucial. Never finance a new car, buy furniture on credit, or open new credit cards in the months leading up to a home purchase.

- Consider a co-signer: Adding a non-occupant co-borrower with strong income and zero debt can significantly dilute a high DTI.

FAQs About Mortgage DTI

Q1. What is included in debt-to-income ratio?

Your calculation includes the projected mortgage payment, credit card minimums, auto loans, student loans, personal loans, and mandatory child support. However, everyday living expenses like groceries, utility bills, cell phone plans, and health insurance are completely excluded from this formula.

Q2. What is a good debt-to-income ratio for a mortgage?

A good DTI is 36% or lower. Keeping your total debt beneath this threshold signals excellent financial stability to underwriters. It easily helps you secure the absolute best interest rates, requires fewer compensating factors, and grants you the widest variety of loan program choices.

Q3. What is the 28-36 rule for mortgages?

The 28-36 rule is a standard financial guideline used by lenders. It dictates that a household should spend a maximum of 28% of its gross monthly income on total housing expenses, and no more than 36% on all total combined debt obligations.

Q4. How much debt-to-income ratio can you have to buy a house?

Depending on the specific loan type, you can typically have a maximum ratio between 43% and 50%. While conventional loans prefer lower numbers, government-backed options like FHA and VA loans are far more forgiving, occasionally allowing limits to stretch past 50% with strong credit.

Q5. Is rent included in the debt-to-income ratio for mortgage?

If you are buying a primary residence, your current rent is not included because the new mortgage will replace it. However, if you plan to keep your current rental apartment while buying an investment property, that monthly rent will absolutely be factored into your total liabilities.

Conclusion

Wrapping things up, your mortgage debt-to-income ratio is the undisputed foundation of your loan approval process. While credit scores get all the hype, your DTI proves to the bank that you can actually afford the monthly payments. Ideally, keeping your total obligations under 36% will ensure the smoothest transaction and the best rates possible.

I strongly encourage you to review your debts several months before ever submitting a loan application. Pay down those high-balance credit cards and avoid taking out any new loans. If you are unsure where you stand, use an online calculator to run your numbers today. And for my fellow mortgage professionals working on tricky files, don't forget to leverage tools like Zeitro Strata to cross-check those ever-changing maximum guidelines!

People Also Read

- Are Mortgage Rates Expected to Go Down in 2026? Expert Forecasts

- Full Guide: What is a non-QM Loan? Everything to Learn

- Guide: What is NMLS? Definitions, FAQs, More

- 1099 Form vs W2: What's the Difference? Details Here

- Why Have Mortgage Rates Risen When Oil Prices Increase?

- [Solved] What Debt-to-Income Ratio is Needed for a Mortgage?