Written by

Eric

Share this article

.svg)

Subscribe to updates

Last checked and updated on July, 2026.

I still remember squinting at a loan officer's business card years ago, trying to figure out what "NMLS #12345" meant. I assumed it was some kind of internal employee code, maybe even a typo. It took me an embarrassingly long conversation to learn it was neither.

If you're a homebuyer trying to verify a lender, or you're thinking about becoming a loan officer yourself, you've probably run into that same string of numbers and wondered the same thing. It isn't random. It's one of the few things standing between you and a mortgage industry with zero accountability. This guide walks through what NMLS actually means, what the license covers, and why that number matters more than most people realize.

What is NMLS?

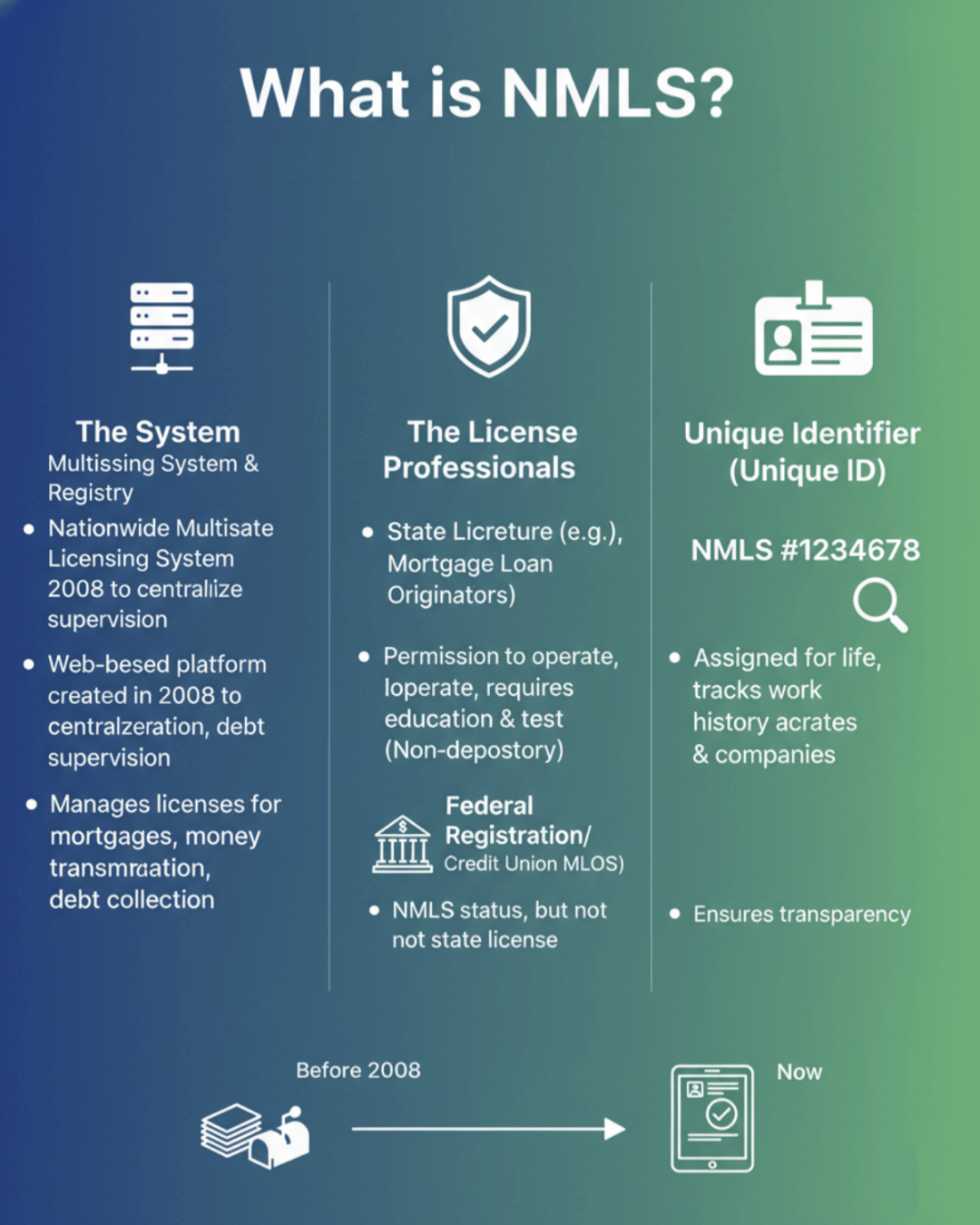

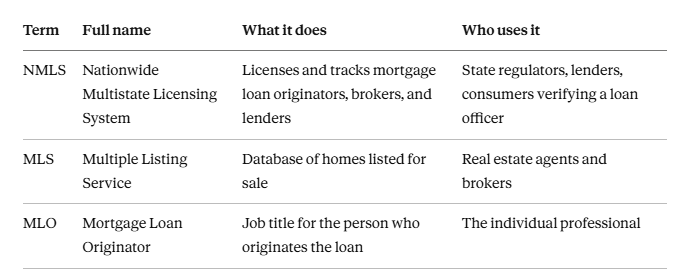

Here's where a lot of confusion starts: "NMLS" doesn't refer to just one thing. Depending on who's talking, it could mean the licensing system itself, the professional license someone holds, or the personal ID number tied to that license for life.

NMLS (Nationwide Multistate Licensing System & Registry) is the official U.S. system that state regulators use to license, register, and track mortgage loan originators, brokers, and lending companies. Everything else in this guide builds on that one definition, so keep it in mind as we go section by section.

You might also see it written as NLMS or MNLS. Those are just common typos, not different systems, and NMLSR is an older shorthand for the same registry.

What Does NMLS Stand for?

Officially, NMLS stands for the Nationwide Multistate Licensing System and Registry. Older folks in the industry sometimes still call it the "Nationwide Mortgage Licensing System" out of habit. That's not wrong exactly, it's just the earlier name, since the system's scope has grown well beyond mortgages into money transmission, debt collection, and other non-bank lending.

The timeline here is more interesting than most articles let on. State regulators spent from 2003 to 2007 building a shared licensing platform, and NMLS itself went live in January 2008, months before Congress got involved. The federal SAFE Act was signed into law on July 30, 2008, giving every state two years to plug into NMLS and adopt consistent licensing standards. So NMLS wasn't created by the SAFE Act; it already existed, and the SAFE Act is what forced every state to actually use it.

I think of the "Registry" half of the name as the quieter, less-talked-about piece. It's the track that covers loan officers who work for banks and credit unions rather than independent brokerages, which we'll get into next.

What is an NMLS License?

An NMLS license is your legal permission to originate mortgages. A state regulatory agency issues it, and the process runs through the NMLS system, but the license itself always comes from the state, not from NMLS directly.

Here's the part that trips up almost everyone new to this:

- State Licensure. If you work for a mortgage broker or an independent, non-bank lender, you have to pass a tough exam and hold an actual state license.

- Federal Registration. If you work for a bank like Wells Fargo or a credit union, you're federally registered instead. You show up in NMLS and have a valid ID, but you don't carry the same state-issued license.

That second path is exactly what the "Registry" part of the name covers, since it's tracking federally regulated employees rather than state licensees.

If you're planning to become a loan officer, the license is your proof that you cleared the education, testing, and background-check requirements everyone else in the field had to clear too.

Also Read: NMLS License Cost Breakdown 2026: Know Your Every Penny

What is an NMLS Number?

Picture it as a Social Security number, but for your mortgage career. It's the unique ID assigned to you the first time you set up an NMLS account, and it never changes, even if your job does.

Numbers usually run five to eight digits long, no letters involved, and you'll often see them written as "NMLS #443495" or just "NMLS# 443495" on a business card or website footer. Whatever format you see it in, it's the same ID.

One thing worth clearing up: your NMLS number is not a bank account number, and it's not tied to any account balance. It's purely an identity and licensing record.

What I find genuinely useful about this number is how portable it is. I've watched colleagues move from a bank job in New York to a brokerage role in Texas, and their NMLS number followed them without changing at all. For regulators and consumers, that portability is the whole point: it lets anyone trace a loan officer's full work history across companies and states, so a bad actor can't just relocate and start over with a clean slate.

What Does NMLS Mean in Banking?

If you spotted "NMLS" on a bank statement or in your bank's app disclosures, you're not imagining things, and it's not your account number. Employees at banks and credit unions who originate mortgages are required to register in NMLS too, just through the federal registration track instead of state licensing.

This same requirement now stretches beyond traditional banks. Fintech apps that offer lending features, including cash-advance or "buy now, pay later"-style products, generally need their lending entity registered in NMLS as well. You'll usually find that disclosure tucked into the app's terms or a footer link, and you can always confirm it yourself through Consumer Access, which we'll cover shortly.

NMLS in Real Estate: Do Realtors Need One?

Short answer: no. This is one of the more common mix-ups I run into, so it's worth spelling out clearly.

Real estate agents use a completely different system called MLS, or Multiple Listing Service, to list and search homes for sale. NMLS licenses loan originators, not real estate agents. The two acronyms are one letter apart and get confused constantly, but they serve entirely different corners of a home purchase.

So a realtor won't have an NMLS number unless they also happen to be a licensed loan originator on the side, which does happen but isn't the norm.

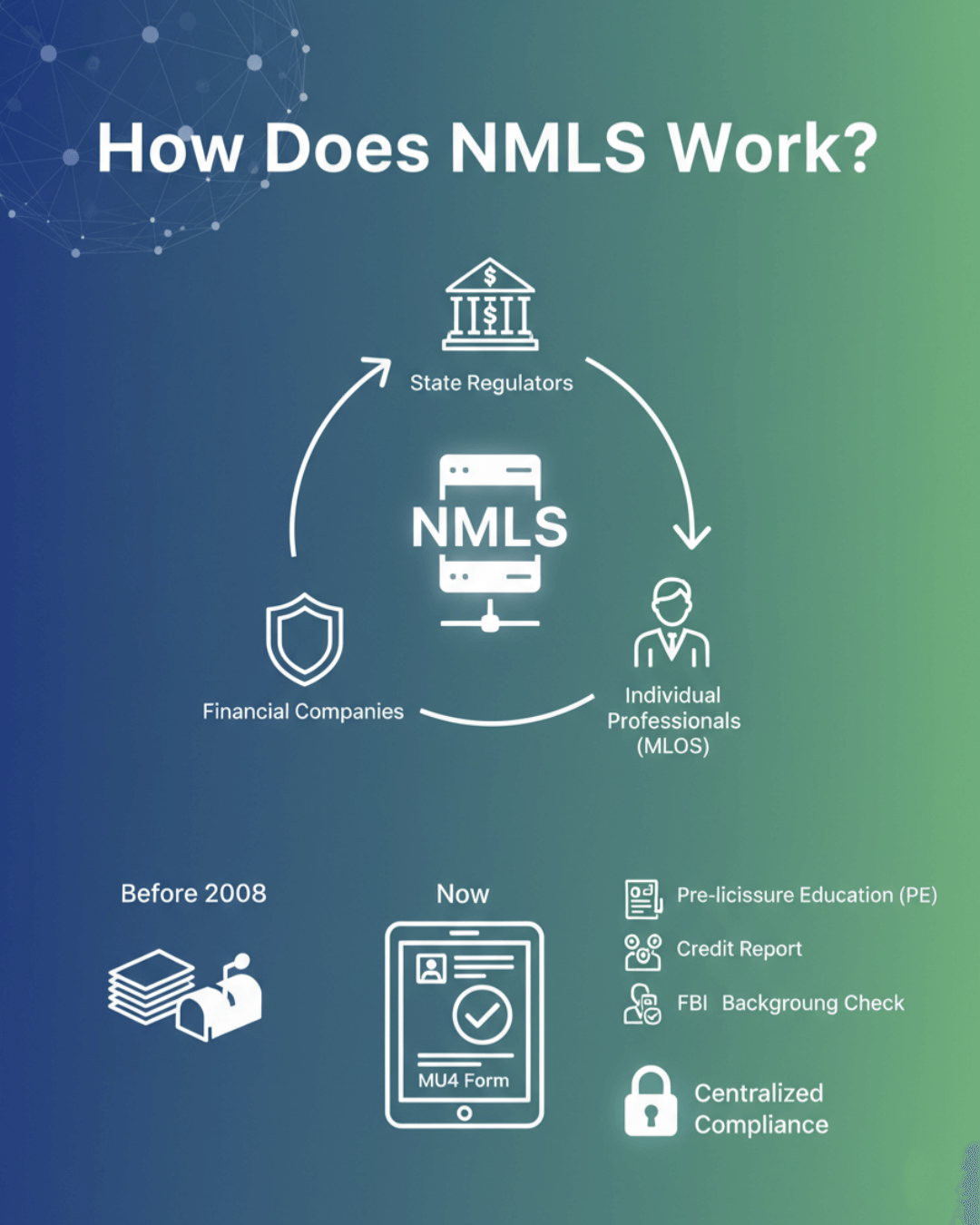

How Does NMLS Work?

So, how does this massive machine actually function? The NMLS acts as a secure, web-based hub that connects three groups: state regulators, financial companies, and individual professionals like Mortgage Loan Originators (MLOs).

From an operational standpoint, it simplifies what used to be a paperwork nightmare. Before 2008, if I wanted to work in five different states, I would have to mail five distinct paper applications to five different government offices. Now, everything is done through a single digital form called the MU4 Form.

The system records everything. It tracks your:

- Pre-licensure education (PE) hours.

- Credit report.

- FBI background check results.

- Annual continuing education.

It basically centralizes compliance, ensuring that every professional you deal with is monitored in real-time.

Why is NMLS Important?

The importance of the NMLS cannot be overstated, especially when we look back at the 2008 financial crisis. The system was born out of the SAFE Act of 2008 (Secure and Fair Enforcement for Mortgage Licensing Act) to stop the "wild west" behavior that caused the market collapse.

Here is why it matters, specifically for you:

- For Borrowers (Fraud Prevention): It is your shield. You can verify if your loan officer is legitimate or if they have a history of disciplinary actions. It creates accountability.

- For the Industry: It levels the playing field. By enforcing uniform standards for testing and education, it weeds out unqualified individuals, raising the professional reputation of everyone else in the business.

Who is Required to Have an NMLS Number?

It's not just the person sitting across the desk from you who needs a number. The requirement covers a broad range of entities in the lending world.

Generally, the following must have an NMLS Unique ID:

- Mortgage Loan Originators (MLOs): Anyone who takes a loan application or negotiates terms for compensation.

- Mortgage Lenders and Brokers: The companies themselves must be licensed.

- Branches: Even specific office locations often have their own branch NMLS numbers.

- Independent Contractors: Contract underwriters or processors who work for multiple companies often need their own license number to operate legally.

How Do I Get an NMLS License?

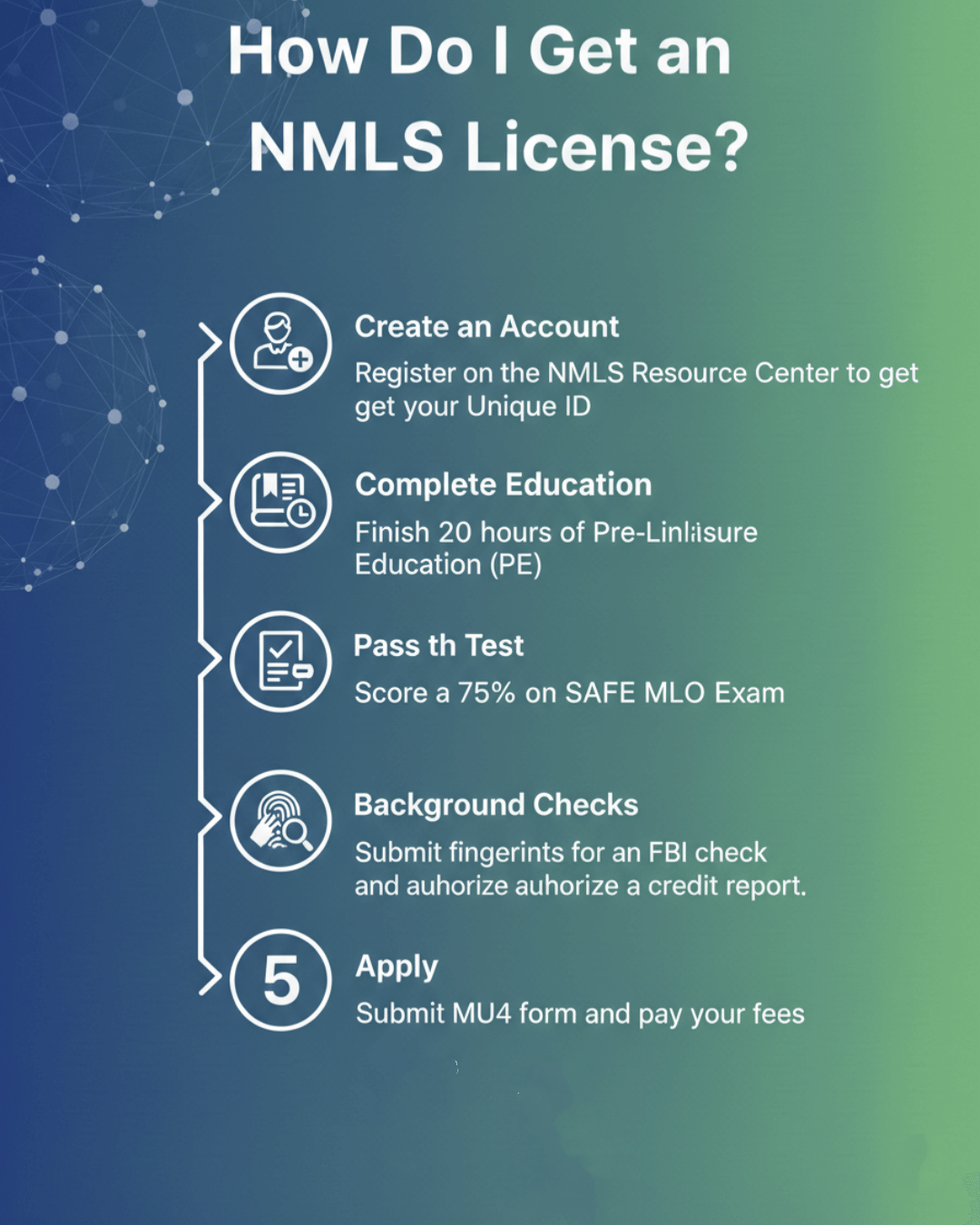

The process is fairly structured, and while small details shift by state, the core path looks the same everywhere:

- Create an account. Register on the NMLS Resource Center to get your Unique ID.

- Complete pre-licensure education. Finish at least 20 hours of NMLS-approved coursework. That's the federal floor, and some states tack on a few extra hours of their own, so check your state's requirement before assuming 20 is the finish line.

- Pass the SAFE MLO Test. You need a 75% score to pass. Nationally, the first-time pass rate sits somewhere around 53% to 58%, so treat the studying seriously rather than skimming the material.

- Clear your background check. Submit fingerprints for an FBI check and authorize a credit report pull.

- Submit the MU4 form and pay your fees.

Getting licensed is only half the work, though. Once you're active, you'll need 8 hours of continuing education every year to keep your license valid, and you'll renew it annually during the NMLS renewal window, which runs November 1 through December 31. Miss that window and your license lapses, which means starting the reinstatement process instead of a simple renewal.

For a more detailed breakdown of the study strategies and application costs, I recommend checking out this guide on how to get an NMLS license.

FAQs About NMLS Meaning

Q1. How to look up the NMLS number?

This is the most useful tool for consumers. You can verify any loan officer or company by visiting NMLS Consumer Access. It is a free, official website. Simply type in the name or number, and you will see their employment history, regulatory actions, and valid licenses. I always tell clients: "Trust, but verify."

Q2. Is the NMLS test hard?

I won't sugarcoat it—yes, it is difficult. The SAFE MLO Test typically has a first-time pass rate hovering around 54% to 65% (based on recent national averages), depending on the testing provider and year. It's not just a memory test. You need to understand how to apply federal laws to real-life scenarios. If you are preparing for it, study hard.

Q3. What is the difference between NMLS and MLO?

This is a common mix-up. NMLS is the database/system. MLO (Mortgage Loan Originator) is the job title of the person. You can think of it this way: The NMLS is the DMV (Department of Motor Vehicles), and the MLO is the driver.

Q4. Is an NMLS a professional license?

Technically, "NMLS" is the system, but when people ask this, they mean the credential. Yes, holding a state-issued license via the NMLS is a professional license. It requires ongoing education, credit checks, and adherence to federal law, similar to how CPAs or Realtors are licensed.

Q5. Is my NMLS number the same as a bank account number?

No. Your NMLS number is a licensing and identity record, not a financial account. It won't show up on a bank statement tied to your balance, and no one can access funds using it.

Q6. Do realtors have NMLS numbers?

Generally, no. Real estate agents work through MLS (Multiple Listing Service), a completely separate system for listing homes. NMLS applies to loan originators and lenders, not real estate agents, unless someone happens to hold both roles.

Q7. What is NMLSR?

It's an older abbreviation for the same registry, standing for essentially the same thing as NMLS. You'll still see it referenced in some older regulatory documents, but it isn't a separate or newer system.

Q8. How do I find a specific company's NMLS number?

Search the company name directly on NMLS Consumer Access. Most licensed lenders also print their NMLS number in the footer of their website or in loan disclosure documents. This applies to fintech lenders too. If an app offers a loan or cash-advance feature, its lending partner should have a findable NMLS number somewhere in the fine print.

Q9. How long does it take to get an NMLS license?

Most people finish the 20 hours of pre-licensure education within a week or two of steady study, then need additional weeks to prepare for the SAFE exam itself. Between coursework, studying, background checks, and state processing time, budgeting one to three months from start to an active license is realistic for most first-time applicants.

Conclusion

Whether you are navigating the exciting journey of buying a home or launching a new career in finance, understanding the NMLS is crucial.

- For homebuyers, that unique number is your safety net. Always use Consumer Access to check who you are working with.

- For aspiring professionals, your NMLS ID is a symbol of trust and competence. It proves you have put in the work, passed the background checks, and earned your place in the industry.

People Also Read

- [Tips] Where to Buy Mortgage Leads? Warm Leads for LOs

- 6 Best Loan Origination Software for LOs/Brokers in 2026

- Best CRM for Loan Officers 2026: Which One Suits You Most?

- Best Mortgage Loan Officer Training in 2026: Which to Pick?

- Mortgage Loan Officer Salary: How Much Do Loan Officers Make?

- Best NMLS Test Prep Course: Which to Choose from?