Written by

Eric

Share this article

.svg)

Subscribe to updates

Quick answer: Most new loan officers spend somewhere between $600 and $1,500 to get fully licensed, and that range comes down to your state, your course provider, and how many times you sit the exam. Below, I've broken every single charge into plain English so nothing catches you off guard.

When I first decided to become a Loan Officer, I thought I'd just pay a single application fee and get started. Boy, was I wrong. The NMLS website felt like a maze, and every time I turned a corner, there seemed to be another charge waiting for me. If you are eyeing a career change in 2026, you need to know what you are actually signing up for. It is not just one check. It is a whole stack of them. Here is the real cost breakdown so your bank account doesn't get a nasty surprise.

People Also Read:

- 8 Best Mortgage Lead Generation Companies: Don't Miss

- How to Generate Mortgage Leads for Free? 6 Methods

- Best CRM for Loan Officers: Which One Suits You Most?

- Mortgage Loan Officer Salary: How Much Do Loan Officers Make?

- What Does a Loan Officer Do? Duties, Pros, Cons, and Outlook

- Best NMLS Test Prep Course: Which to Choose from?

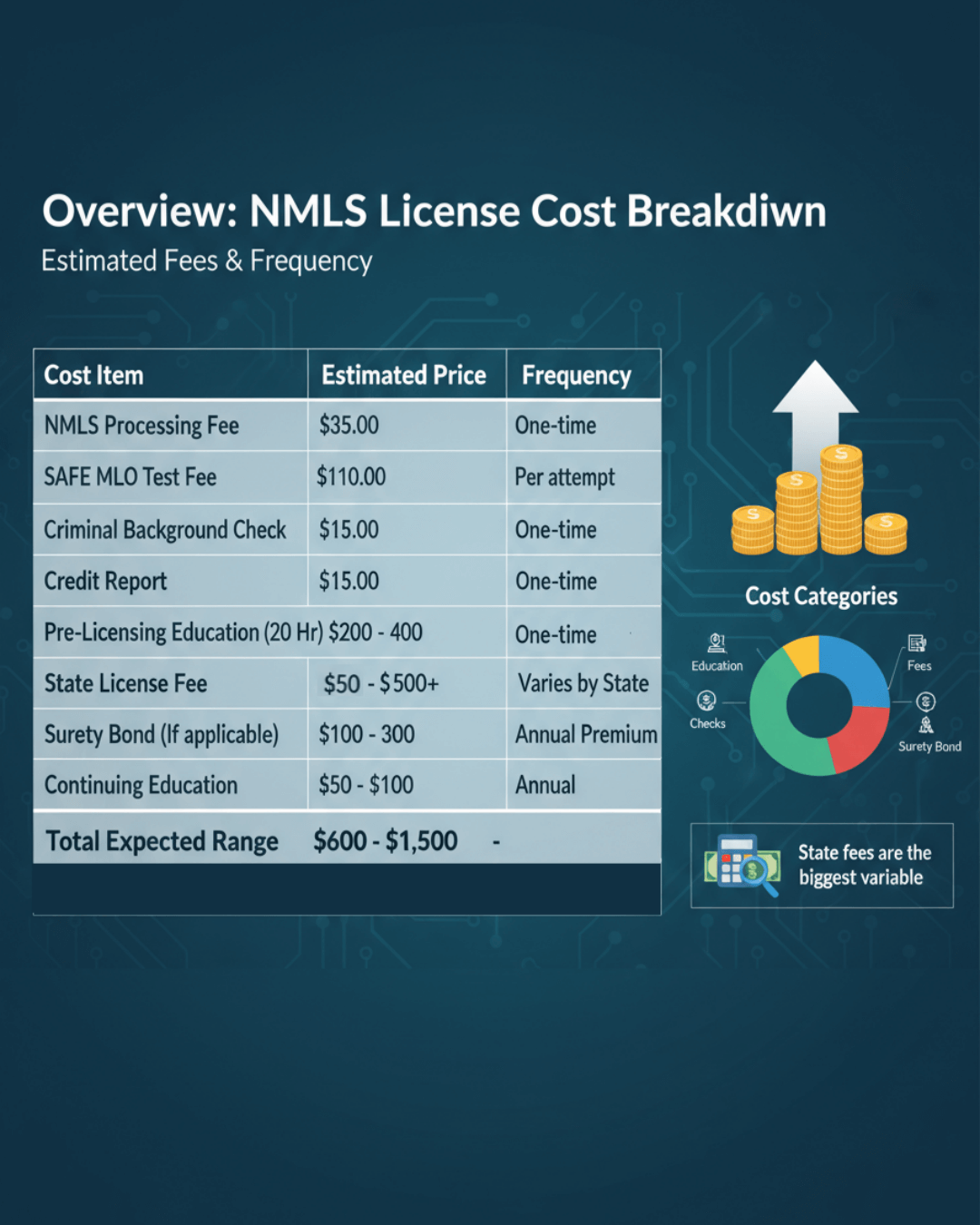

Overview: NMLS License Cost Breakdown

Let's cut to the chase. You need to have roughly $600 to $1,500 ready to go.

Why the big range? It depends entirely on which state you are in and whether you choose a "budget" online class or a premium one. Below is the cheat sheet of the fees I encountered (and you will too). These are the 2026 estimates based on the NMLS Resource Center.

- NMLS Processing Fee: $35.00

- SAFE MLO Test Fee: $110.00

- Criminal Background Check: $36.25 - $39

- Credit Report: $15.00

- Pre-Licensing Education (20 Hr): $200 - $400

- State License Fee: $50 - $500+

- Surety Bond (If applicable): $100 - $300

- Continuing Education: $50 - $100

Total Expected Range: $600 - $1,500

Introduction to Every NMLS License Cost

Now, let's look at the receipt line-by-line. It's important to understand that the NMLS collects money for two different people: themselves (for processing) and the state regulators.

NMLS Processing Fee

Think of this as the cover charge just to get into the club. You will pay a $35 initial set-up fee when you file your Form MU4. It's not much, but here is the kicker: even if your license gets denied later, the NMLS generally keeps this money. It is strictly a fee for using their software system.

SAFE MLO Test Fee

This one hurts the most if you aren't prepared. The National Test costs $110. The catch? You pay that every single time you take it. I know people who had to pay this three times because they underestimated the difficulty. Don't be that person. Study hard so you only have to pay this $110 once.

Criminal Background Check

You can't handle people's mortgage money without proving you are trustworthy. The NMLS FBI criminal background check fee is $36.25 for Live Scan (digital fingerprints). You will usually have to go to a third-party vendor (like Fieldprint) to get your fingerprints scanned digitally. Note that some states, like California, charge $39 via NMLS fingerprints, and third-party vendors may add fees. Sometimes those vendors tack on their own small service fee, so keep a credit card handy for that appointment.

Credit Report

The NMLS will pull your credit report for $15.00. Don't panic if your score isn't perfect. They aren't looking for an 800 FICO score. They are looking for "financial responsibility." Basically, as long as you don't have open fraud judgments or ignored government liens, you should be okay. It's about integrity, not wealth.

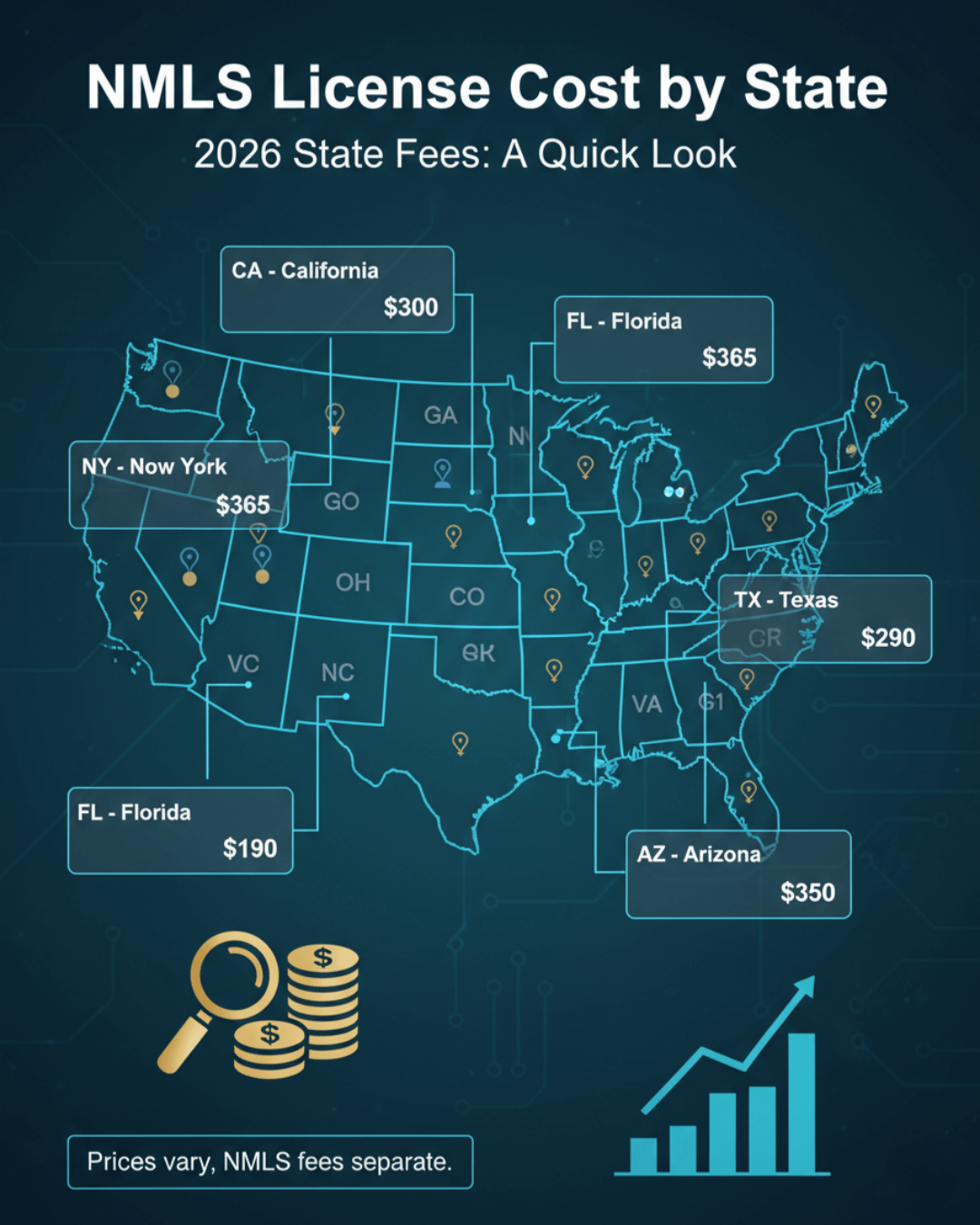

State-Specific License Fee

This is the wild card. Every state charges whatever they want. I've seen fees as low as $30 and some well over $500. Also, watch out for the double-dip: some states charge an "Application Fee" and a separate "License Fee." You absolutely have to check the state-specific page on the NMLS site to see what your local regulator charges.

- Georgia: $100

- Tennessee: $100

- North Carolina: $125

- Virginia: $130

- Ohio: $150

- Texas: $190

- Florida: $195

- Illinois: $250

- California: $300

- Arizona: $350

- New York: $365

Based on state fees alone, Georgia and Tennessee sit at the low end of this list at roughly $100. That said, "cheapest" isn't the whole story — education requirements, exam difficulty, and continuing education rules are federal and don't change no matter where you're licensed. A cheaper state application won't save you money if you fail the exam twice because you skimped on your course.

Pre-Licensing Education (20 hours)

You cannot skip this. You need 20 hours of approved education, and it is the biggest ticket item, usually $200 to $400. The self-paced online slides are cheaper, but if you snooze through them, you will fail the exam. Personally? I'd spend a bit more on a course that actually teaches you, not just one that clicks "next" for you.

Surety Bond Costs

This is a hidden cost many guides forget. If you are an independent broker, you likely need a Surety Bond. You don't pay the full bond amount (e.g., $25,000). You pay a premium, usually $100-$300 a year based on your credit. However, if you work for a lender or bank, they typically cover this for you.

Annual Renewal Fee

Getting licensed is only round one. Every year, between November 1 and December 31, you're required to renew. The NMLS annual processing fee for your license sits at $35, and most states charge a renewal fee close to what you paid initially. Miss the December 31 deadline and you're looking at reinstatement penalties, so mark your calendar early.

Staying active also means completing 8 hours of continuing education annually, usually running $50 to $150 depending on your provider. One rule trips people up here: the "successive years" rule means you can't retake the exact same course two years running, so you'll need fresh material each cycle.

Continuing Education

To keep that license active, you need 8 hours of class every year. Budget about $50 to $100 for this. And no, you can't take the exact same course two years in a row. the "Successive Year Rule" stops that, so you'll be buying fresh content annually.

NMLS License Cost by State

Since the state fee is the biggest variable, here is a quick look at the price tags for the most popular spots in 2026. Keep in mind, this is just what you pay the state. You still have to add the NMLS fees on top of these.

- California (DFPI): Expect around $300 (Application + Investigation fees).

- Florida: About $195 total for the license and guaranty fund.

- Texas (SML): Roughly $190.

- New York: One of the pricier ones at $365 (Investigation + License).

- Georgia: A reasonable $100.

- Illinois: Around $250.

- Ohio: Approximately $150.

- North Carolina: About $125.

- Virginia: Around $130.

- Arizona: On the higher end at $350.

FAQs About NMLS License Cost

Q1. How much does the NMLS exam cost?

The test itself is $110. You pay this directly through the NMLS portal before you can schedule a date with Prometric. Just be careful. if you cancel or reschedule within 2 days of your slot, you might lose that money.

Q2. Is the NMLS license fee refundable?

Generally, no. Once the money leaves your account for background checks, credit reports, or processing fees, it is gone. Even if your state rejects your application, they rarely refund the application fees. Make sure you are eligible before you pay.

Q3. How much is the NMLS renewal fee?

It depends on your state, but the base NMLS processing fee is $30. Most states then add their own renewal fee, which is often the same as (or slightly less than) the initial license fee. Expect to pay this every single winter.

Q4. Does my employer pay for my NMLS license?

This is the industry norm for banks and direct lenders. Many companies will reimburse you for the test and classes once you pass. However, if you are going independent (working as a broker), you are usually on the hook for these costs yourself.

Conclusion

So, what is the final damage? Realistically, you should put aside $800 to $1,000 to be safe to get an NMLS license. It sounds like a lot upfront, but compared to the startup costs of opening a restaurant or a store, it is actually quite low.

Plus, in this industry, one decent commission check usually covers your entire startup cost. My best advice? Don't try to save $50 on a cheap education provider. Spend the money on good prep materials so you pass the test on the first try. That is the best way to save money in the long run. Good luck!