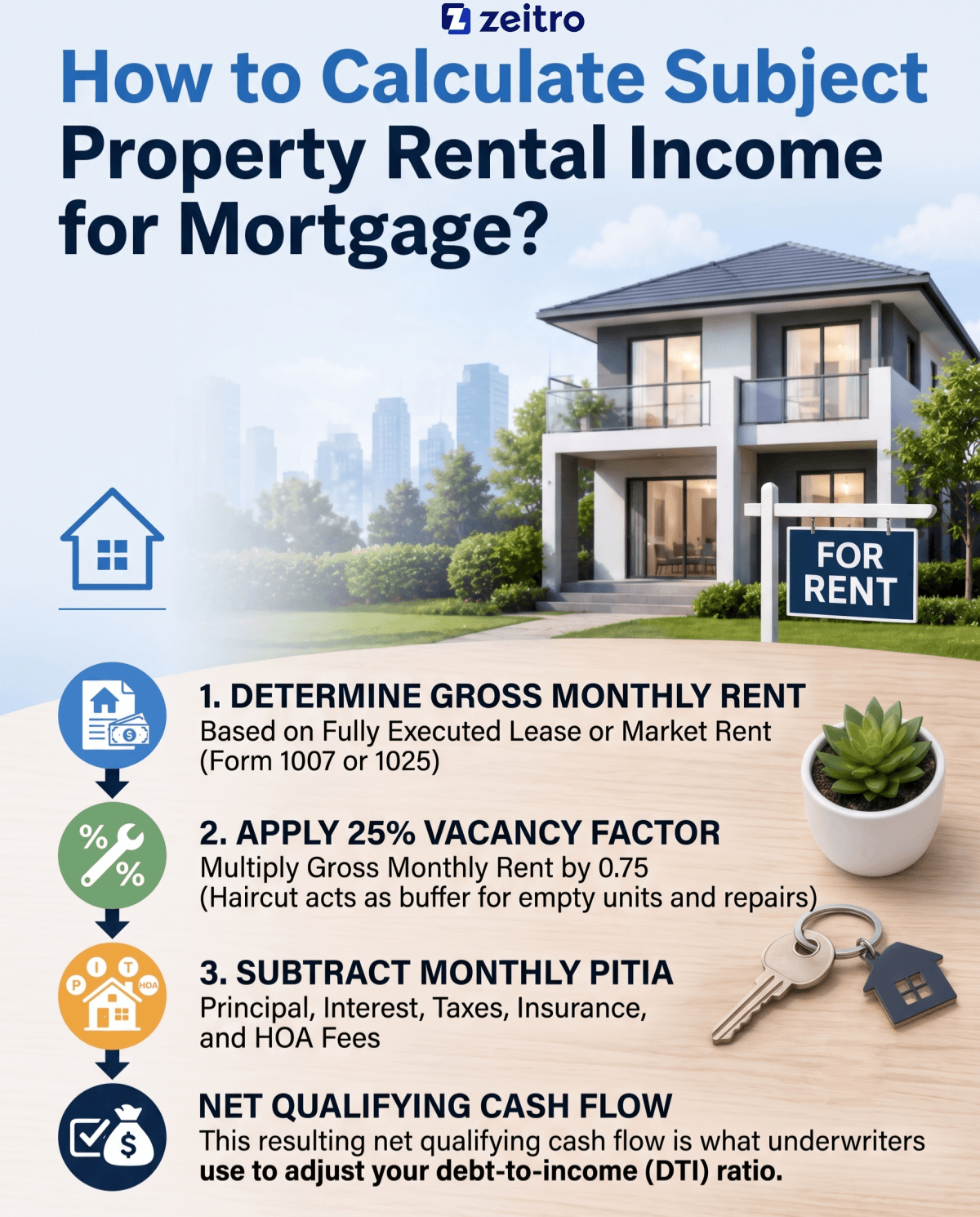

As a senior loan officer, borrowers routinely walk into my office asking, "Can I buy a home if my only income is Social Security?" My answer is always a resounding yes. Under the federal Equal Credit Opportunity Act, lenders cannot deny your mortgage or treat your funds differently solely because your income comes from public assistance, including Social Security. Your Social Security income can count as qualifying income when it meets the lender's standard underwriting guidelines.

Key Takeaways

- Acceptable: Social Security income (retirement, disability, or survivor benefits) is generally accepted as qualifying income across all major U.S. mortgage programs, as long as it is properly documented and expected to continue for at least three years.

- Equal Protection: Federal law prevents lenders from discounting or discriminating against your public assistance income.

- Income Boosting: Non-taxable Social Security benefits can often be "grossed up" by around 15% to 25%, depending on the loan program and lender, to increase your qualifying income.

- Simple Paperwork: Qualification requires your SSA Award Letter and recent bank statements showing direct deposit.

- Continuance Rules: For retirement or long-term disability benefits based on your own work record, agencies often treat the income as likely to continue, as long as your Social Security documentation does not show an upcoming end date within three years.

Can I Get a Mortgage with Just Social Security Income?

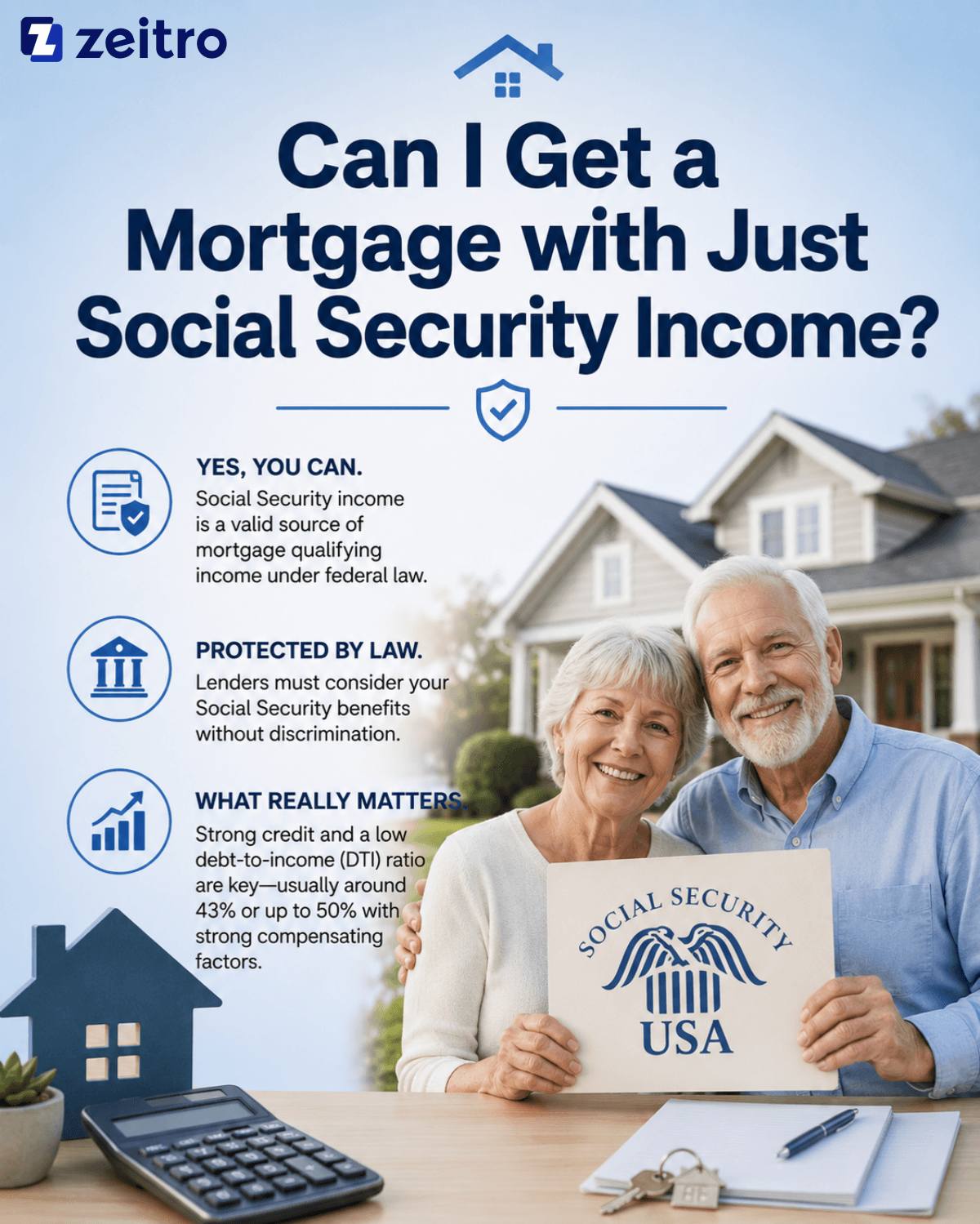

Yes, you can buy a home using only Social Security income. Over my years in mortgage underwriting, I have helped dozens of retirees and disabled individuals secure home loans without a traditional paycheck. Under federal law, specifically the Equal Credit Opportunity Act, mortgage lenders are legally prohibited from discriminating against public assistance benefits.

Lenders are required to evaluate your Social Security checks as legitimate qualifying income and may not discount them simply because they come from public assistance, although the documentation they request can differ from what is needed for a traditional salary.

The real deciding factors aren't where your money comes from, but your credit score and Debt-to-Income ratio. If your monthly debts and proposed mortgage payment keep your Debt-to-Income (DTI) ratio near 43%, and in some cases up to around 50% with strong compensating factors or automated underwriting approval, you may be able to qualify.

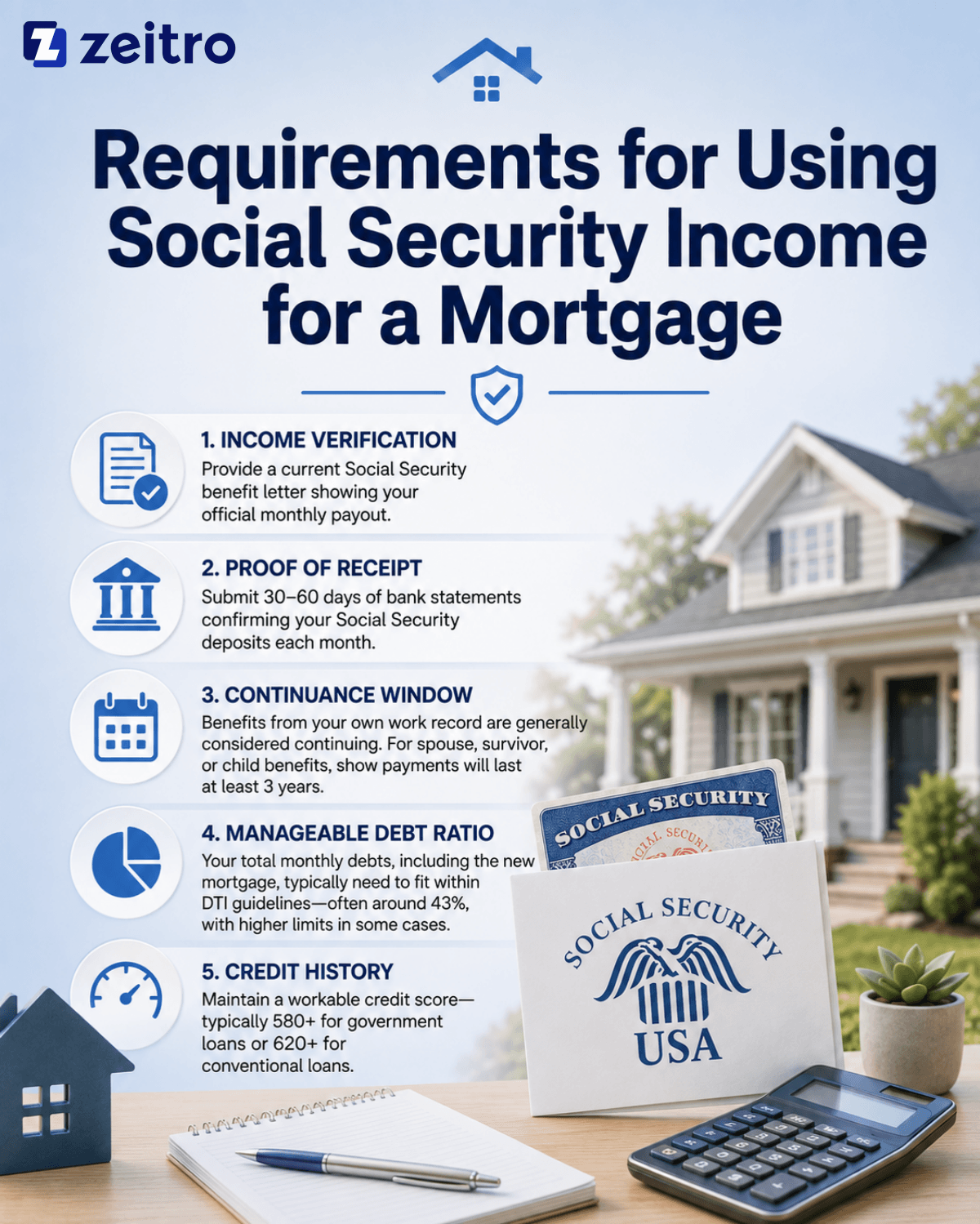

Requirements for Using Social Security Income for a Mortgage

Qualifying for a home loan with Social Security comes down to showing stability and meeting standard agency underwriting guidelines. Here is what lenders evaluate when reviewing your file:

- Income Verification: You must prove your official monthly payout amount using a current benefit letter.

- Proof of Receipt: Lenders need 30 to 60 days of bank statements confirming the money lands in your account each month.

- Continuance Window: If you draw benefits on your own work record, agencies such as Fannie Mae and FHA generally treat the income as continuing, provided your SSA documentation does not indicate it will end within three years. However, if benefits come from a spouse, survivor, or dependent child, or show a defined expiration date, you must document that payments will last at least three years.

- Manageable Debt Ratio: Your total monthly obligations, including your new mortgage, generally need to fit within standard DTI guidelines, often targeting about 43%, with higher limits sometimes allowed depending on the loan program and underwriting findings.

- Credit History: You still need a workable credit score, typically starting at 580 for government programs or 620 for conventional loans.

What Mortgage Loan Types Can You Pick?

You are not restricted to niche products just because you receive Social Security. You can choose from the same top loan programs available to traditional wage earners:

- Conventional Loans: Backed by Fannie Mae and Freddie Mac, these loans typically require at least a 620 credit score and may allow non-taxable Social Security income to be grossed up by about 15%, with higher gross-up percentages possible when supported by additional tax documentation.

- FHA Loans: Insured by the government, FHA loans are ideal for fixed incomes because they accept credit scores down to 580 and offer lower 3.5% down payment options.

- VA Loans: Available to eligible military veterans and surviving spouses, offering zero down payment and flexible credit benchmarks.

- Reverse Mortgages (HECM): For homeowners aged 62 and older, a Home Equity Conversion Mortgage eliminates monthly mortgage payments entirely, though you must still cover property taxes and home insurance.

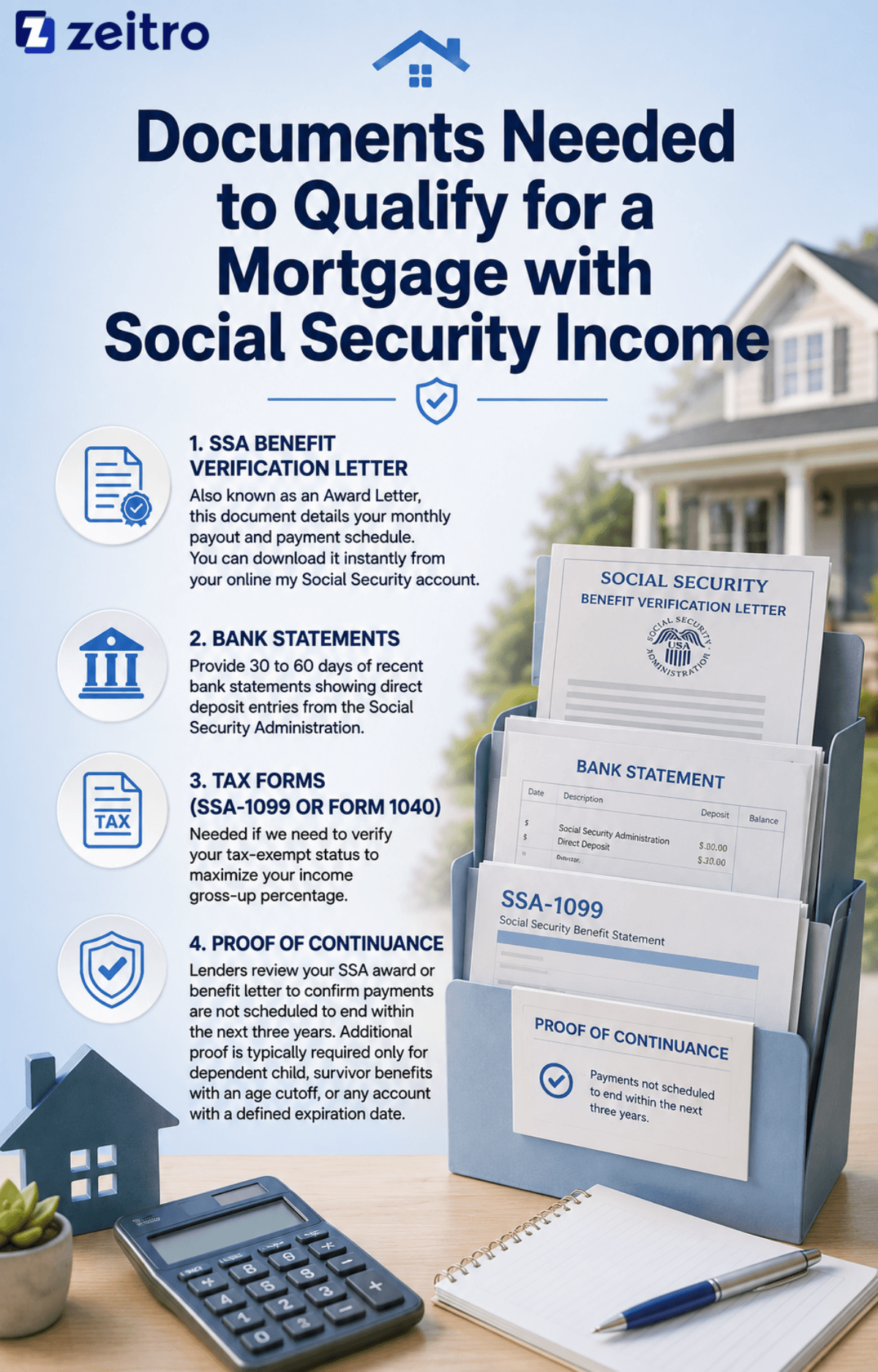

Documents Needed to Qualify for a Mortgage with Social Security Income

Gathering paperwork for a Social Security mortgage is surprisingly straightforward compared to traditional self-employed or hourly applications. In my client consultations, I always ask borrowers to bring these key items:

- SSA Benefit Verification Letter: Also known as an Award Letter, this document details your monthly payout and payment schedule. You can download it instantly from your online my Social Security account.

- Bank Statements: Provide 30 to 60 days of recent bank statements showing direct deposit entries from the Social Security Administration.

- Tax Forms (SSA-1099 or Form 1040): Needed if we need to verify your tax-exempt status to maximize your income gross-up percentage.

- Proof of Continuance: For all Social Security income, lenders review your SSA award or benefit letter to confirm that payments are not scheduled to end within the next three years. Additional proof is typically required only when the benefits are tied to a dependent child, survivor benefits with an age cutoff, or any account that shows a defined expiration date.

FAQs About Using Social Security Income for a Mortgage

Q1. How to calculate Social Security income for mortgage?

When calculating Social Security income, lenders look at whether your benefits are taxed. If your income is non-taxable, mortgage guidelines allow underwriters to "gross up" that amount by 15% to 25%. For example, if you receive $1,500 a month in non-taxable benefits, a 15% gross-up increases your qualifying income to $1,725. This boosts your purchasing power without adding actual cash out of your pocket.

Also Try: Zeitro Mortgage Income Calculator for Loan Pros

Q2. Can you get an FHA loan on Social Security?

Yes, FHA loans are one of the best mortgage choices for individuals relying on Social Security. Under FHA Handbook guidelines, lenders accept Social Security retirement, SSDI, and SSI benefits. FHA offers flexible underwriting, allowing down payments as low as 3.5% and accepting lower credit scores than conventional loans.

Q3. Can you buy a house on Social Security disability (SSDI/SSI)?

Yes. Both SSDI (disability insurance) and SSI (supplemental income) count as valid income. One insider tip for SSI recipients: if family members pay for your housing costs directly, the Social Security Administration might reduce your monthly SSI checks, which could alter your loan qualification. Always check your net benefit before applying.

Q4. Do I need to prove my Social Security income will continue for 3 years?

Not always. For retirement or long-term disability benefits based on your own work record, major agencies like Fannie Mae and FHA generally treat the income as likely to continue as long as your SSA award or benefit letter does not show an end date within the next three years. You typically must document a three-year continuance only when the benefit is tied to someone else's record or has a clearly defined expiration date.

Q5. Does non-taxable Social Security income help me qualify for a larger mortgage?

Yes, significantly. Because non-taxable income gives you more net spending power, lenders artificially raise your qualifying income through the gross-up rule. By turning $2,000 of untaxed income into $2,300 or $2,500 on paper, your Debt-to-Income ratio lowers, helping you qualify for a higher loan amount.

Conclusion

Using Social Security income to buy a home is completely legal, highly manageable, and very common. As long as your income covers your debts and your credit score meets minimum guidelines, you can secure a great loan. Start by downloading your Social Security Award Letter and pulling your latest bank statements. Then, reach out to a trusted loan officer who understands how to properly gross up your benefits and guide you home.

People Also Read

- Can I Use Trust Income for a Mortgage? Learn Here

- Can I Use Foreign Income to Qualify for a Mortgage?

- Can I Use Child Support Income for a Mortgage?

- Biggest Condo Rule Change in a Decade: Guide for Mortgage Pros