![[2026 Update] Best No Income Verification Mortgage Lenders](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/69aa3ee7443901c427060cf3_best-no-income-mortgage-lenders-banner.png)

Written by

Eric

Share this article

.svg)

Subscribe to updates

Last checked and updated: June 2026 by Eric

I still remember the first time a self-employed client sat across from me, visibly frustrated, holding two years of tax returns that made his business look like it was barely surviving — even though his bank account told a completely different story. That's the write-off problem every freelancer, 1099 contractor, and small business owner eventually runs into. Traditional underwriting reads your Schedule C, not your actual cash flow.

That gap is exactly why no income verification loans exist. I want to clear up one thing right away: the true "no income, no job, no assets" loans that helped trigger the 2008 crash are gone. Since federal Ability-to-Repay rules took effect in 2014, every legitimate lender has to confirm you can realistically afford the payment — they just don't have to do it with a W-2. Today's programs, grouped under the Non-QM umbrella, use bank deposits, liquid assets, or a rental property's own cash flow instead. Below are six lenders I'd actually point a client toward in 2026, based on their published guidelines, licensing records, and how they've performed for borrowers with non-traditional income.

If you're unsure which lender fits your unique financial profile, use Bluerate free AI Chat to instantly match with the best loan officer for your exact needs.

What "No Income Verification" Actually Means in 2026?

If you've searched for a mortgage loan without income proof, it helps to know what you're really shopping for. There are three main structures behind nearly every no-doc-style program on the market:

Bank statement loans replace tax returns with 12–24 months of business or personal bank deposits, which is how most lenders qualify a self employed mortgage no proof of income. DSCR (Debt Service Coverage Ratio) loans skip personal income entirely and qualify the deal based on whether the property's rent covers its own mortgage payment — a common fit if you're wondering what financing options exist for rental properties that don't require income verification. Asset depletion loans convert your savings, investments, or retirement accounts into a qualifying "income" figure, which works well for retirees or high-net-worth buyers without a regular paycheck.

None of these skip verification altogether, they just verify a different data source than a pay stub.

What No Income Mortgage Loan is Good for You?

Let's clear up a major misconception right away: the pure "NINJA" (No Income, No Job, No Assets) loans from 2008 no longer exist. Today, a "no income verification" mortgage actually means using alternative documentation to prove your ability to repay.

Depending on your situation, here are the main paths you can take:

- Bank Statement Loans: Best for the self-employed or gig-workers. Lenders review 12 to 24 months of your personal or business bank deposits to calculate an average qualifying cash flow.

- DSCR Loans (Debt Service Coverage Ratio): Best for real estate investors. The property's projected rental income must cover the monthly mortgage debt. Your personal income isn't even part of the equation.

- Asset Depletion Loans: Best for retirees or high-net-worth individuals. Banks divide your total liquid assets by the loan term to create a monthly "income" figure.

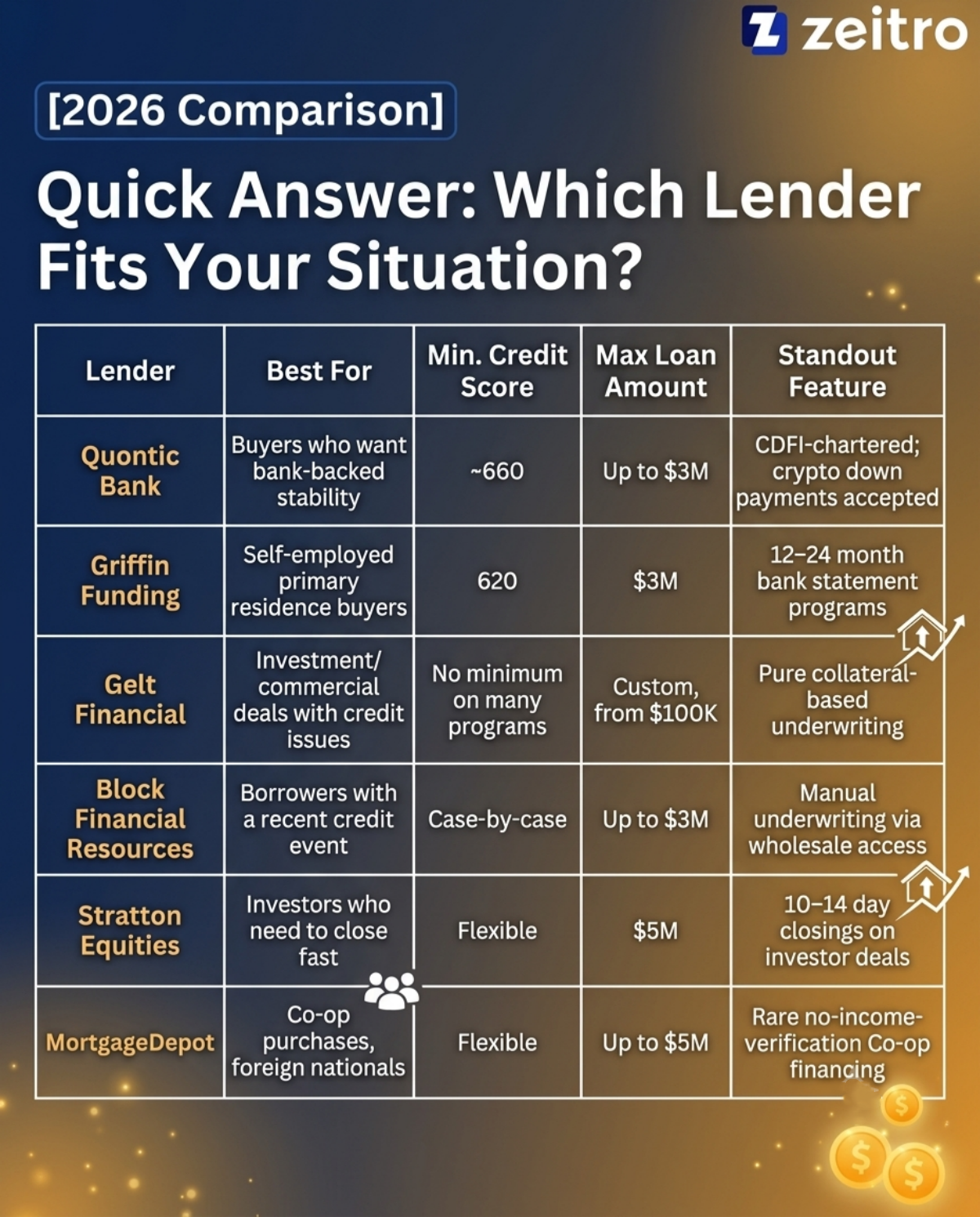

Quick Answer: Which Lender Fits Your Situation?

6 Best No Income Mortgage Lenders to Choose from

Over the past few weeks, I analyzed dozens of mortgage companies. I selected these six based on their maximum loan-to-value (LTV) limits, alternative documentation flexibility, processing speed, and solid reputation in the 2026 Non-QM market.

1. Quontic Bank — Best for Bank-Backed Stability

NMLS: 403503

Suitable for: Best for non-traditional earners seeking an established, flexible community bank.

Pros: Highly regulated bank offering safety; excellent products for self-employed home buyers.

Cons: Rates can be slightly higher than conventional products; requires a solid down payment (often 20% or more).

Quontic is a rare breed in today's market. As a certified Community Development Financial Institution (CDFI), they actually have a mission to serve underbanked communities. I really appreciate their Non-Traditional Loan program, which bypasses standard tax verification and focuses on your broader financial health. While you do need a decent credit history, they are incredibly open-minded regarding how you make your living.

Features:

- Certified CDFI offering dedicated Non-QM and bank statement mortgage options .

- No-doc streamline refinance options available for up to $3 million .

- Minimum FICO score requirement is typically 660 or higher for Non-QM loans.

- No W2s or standard tax returns are required to get approved .

- Crypto-friendly, allowing Bitcoin to be used for down payments.

2. Stratton Equities — Best for Fast-Moving Investors

NMLS: 1795154

Suitable for: Best for real estate investors needing fast approvals and hard money options.

Pros: Incredibly fast funding times; massive variety of nationwide loan programs under one roof.

Cons: Primarily geared toward investment properties, including NON-QM for one-to-four family properties; interest rates reflect the speed and higher risk.

If you are flipping houses or building a rental portfolio, speed is everything. Stratton Equities operates as a direct private money and Non-QM lender, meaning they don't get bogged down in institutional red tape. I've noticed they can often close a deal in just a few weeks. They focus heavily on the asset itself rather than your personal W-2, making them a powerhouse for landlords.

Features:

- Massive library of direct DSCR loans, Fix and Flip, and private money products.

- Loan amounts range from $100,000 up to a massive $5 million.

- No upfront junk fees and absolutely no tax returns needed for their investor programs.

- Blazing fast closing timelines, often within 10 to 14 days.

- LTV ratios up to 80% on certain investment property purchases.

3. Griffin Funding — Best for Self-Employed Buyers

NMLS: 1120111

Suitable for: Best for self-employed business owners and veterans looking for alternative financing.

Pros: Very forgiving credit score minimums; highly transparent alternative income processes.

Cons: Does not offer loans for vacant land or ground-up construction; geographically limited in a few states.

Griffin Funding leans hard into bank statement and asset-based lending, and I've noticed they're more willing than most to work with a slightly lower credit profile if you bring strong compensating factors, like large reserves. Their national footprint makes them accessible almost anywhere, which matters if you're comparing best no doc mortgage lenders outside a major metro.

Features:

- Accepts 12 to 24 months of bank statements to qualify your cash flow.

- Credit scores as low as 620 are accepted.

- Loan amounts ranging from $100,000 to $3,000,000.

- Down payments as low as 10% with credit score of 660+.

- Provides Non-QM cash-out refinance options.

4. Gelt Financial — Best for Collateral-Based Deals

NMLS: Not applicable (direct private commercial lender, non-bank portfolio lender).

Suitable for: Best for commercial real estate investors facing bank rejections or severe credit hurdles.

Pros: Supreme flexibility with damaged credit; extremely fast "common sense" underwriting.

Cons: Short-term focus (bridge loans usually 1-5 years); strictly for investment and commercial properties, not primary homes.

Gelt Financial has operated as a direct balance-sheet lender since 1989, and their whole model is built around one idea: if the deal makes sense on paper, they'll fund it. Because they underwrite almost entirely against the property's value rather than your paycheck, they're one of the clearest answers to what lenders focus on property value instead of my income. They're a strong option when a deal is too unconventional for a standard broker to place — vacant land and new construction are the two carve-outs they won't touch.

Features:

- No minimum credit score on many products — a rare true example of private mortgage lenders no credit check.

- No personal income qualification on most commercial programs.

- Offers blanket loans to pull equity from multiple properties for a down payment.

- Appraisals and environmental checks are sometimes waived to speed up funding.

- Loan amounts generally start at $100,000 with highly customized terms.

5. Block Financial Resources (BFR) — Best for Recent Credit Events

NMLS: 132830

Suitable for: Best for East Coast borrowers with complex financial histories requiring manual underwriting.

Pros: The broker model means they shop multiple banks for you; excellent at handling complex, manual underwriting files.

Cons: Geographically limited to a handful of states; you are subject to the final wholesale lender's timeline.

Based out of New York, Block Financial Resources is a mortgage broker rather than a direct bank. I included them because they have incredible access to niche Non-QM loans via wholesale channels. If you've experienced a major credit event recently, BFR knows exactly which banks will manually underwrite your file and accept alternative income proofs.

Features:

- Access to loans up to $3 million using 12 to 24 months of bank statements.

- Forgiving on past credit events (accepts 1 major event in the past 3 years).

- Offers interest-only payment structures to help buyers free up monthly cash flow.

- Accepts expanded debt-to-income (DTI) ratios up to 55%.

- Expert local knowledge in the NY, NJ, and FL real estate markets.

6. MortgageDepot — Best for Co-ops and Foreign Nationals

NMLS: 1133788

Suitable for: Best for self-employed buyers in diverse markets looking for high-value Non-QM and Co-op financing.

Pros: Phenomenal niche products (like Co-op financing); very accommodating to foreign buyers and diverse communities.

Cons: High down payment requirements (often 30% down payment) for their top-tier no-doc loans; broker origination fees may apply.

MortgageDepot is another powerhouse broker that really understands out-of-the-box financing. I'm particularly impressed by their ability to arrange "no income verification" loans for Co-ops, which is notoriously difficult in places like New York. They cater heavily to a culturally diverse crowd, offering streamlined digital processes for both local and foreign buyers.

Features:

- No tax return required programs with high limits up to $5 million.

- Unique no-income verification options designed specifically for Co-op properties.

- Reduced seasoning requirements on major credit events (eligible just 12 months after a short sale or foreclosure).

- Accepts foreign nationals and ITIN borrowers.

- Offers interest-only options to increase initial purchasing power.

Which to Pick? Considerations Here

Choosing the right partner from this list ultimately boils down to your specific financial reality. Self-employed home loan products carry unique risks for lenders, so I always advise readers to carefully evaluate these key factors before signing anything:

- Rate premium. Because these loans fall outside CFPB Qualified Mortgage protections, lenders price in extra risk. As of late June 2026, Freddie Mac's benchmark 30-year conventional rate sat at 6.49%, and most Non-QM and bank statement programs are running roughly 50 to 200 basis points above that, depending on your credit and loan-to-value. DSCR loans tend to price closest to conventional investor loans, sometimes within half a point, while bank statement products usually carry the bigger premium because of the added underwriting work.

- Down payment. Plan on at least 15–20% down for most programs. A few lenders will go as low as 10% for borrowers with excellent credit, but a bigger down payment consistently unlocks better pricing and approval odds across every lender on this list.

- Credit score. 620 is roughly the floor across the market, but the difference between a 620 and a 700+ score can swing your rate by more than a full point on some pricing sheets.

- How the lender documents your income. A 12-month bank statement review and a 24-month review can produce very different qualifying income numbers for the same business, so ask each lender which window they'll use before you commit to an application.

- State availability. Several lenders on this list, including Gelt Financial and Block Financial Resources, concentrate their strongest guidelines in specific regions like the Northeast. Always confirm licensing in your state before you fall in love with a rate quote.

FAQs About Top No Income Mortgage Lenders

Q1. Can I get a mortgage loan with strictly no income?

No. The days of getting a mortgage with absolutely zero proof of cash flow are gone due to "Ability to Repay" regulations. Today's Non-QM loans require you to prove your repayment capacity through bank deposits, liquid assets, or property rental income (DSCR).

Q2. What not to say to a mortgage lender?

Never lie or exaggerate your assets. Additionally, avoid telling them you plan to quit your business soon, take on massive new auto debt, or open several credit cards before closing. Total transparency and financial stability are your best friends during underwriting.

Q3. What is the minimum down payment for a no-income verification loan?

You should prepare for a minimum of 10% to 20% down. However, for true alternative documentation or investment DSCR loans, many wholesale lenders will ask for 25% or even 30% to secure the best possible interest rate.

Q4. Do I need a high credit score for a non-QM loan?

Not necessarily, but it helps immensely. Some lenders accept scores as low as 600 or 620. However, having a higher score (like 680+) proves your financial responsibility, compensating for the lack of traditional tax returns and significantly lowering your rate.

Q5. Do no income verification loans still exist legally in 2026?

Yes, but not in the pre-2008 sense. Every lender still has to make a good-faith determination that you can repay the loan, per federal Ability-to-Repay requirements. What's changed is the documentation — lenders now accept bank statements, assets, or rental income instead of tax returns, which is why these are usually called Non-QM loans rather than true no-doc loans.

Q6. What lenders focus on property value instead of my income?

Collateral-based and DSCR lenders do. Gelt Financial underwrites almost purely against the asset for commercial and investment deals, while DSCR programs from Stratton Equities and similar lenders qualify the loan based on whether the rent covers the mortgage payment, not your personal earnings.

Q7. What financing options exist for rental properties that don't require income verification?

DSCR loans are the standard answer. The lender divides the property's monthly rent by its monthly mortgage payment — a ratio at or above 1.0 generally clears underwriting without touching your personal income or employment history at all.

Q8. Which of the following loan types doesn't require a borrower to prove income: conventional, FHA, or DSCR?

DSCR loans come closest to skipping personal income entirely, since qualification runs on the property's cash flow instead. Conventional and FHA loans both still require full income documentation under their respective agency guidelines.

Q9. How do I find a home loan with flexible income verification?

Start with lenders that openly advertise bank statement, DSCR, or asset depletion programs, since these are built around alternative documentation from day one. A mortgage broker who works with multiple Non-QM wholesalers, like Block Financial Resources, can also shop your specific file across several guideline sets at once.

Q10. What are the alternatives to traditional income verification for a mortgage?

The three main alternatives are bank statement loans (12–24 months of deposits), asset depletion loans (savings and investments converted into a qualifying income figure), and DSCR loans (property cash flow instead of personal income). Which one fits depends on whether you're buying a primary residence or an investment property.

Q11. Are there private mortgage lenders with no credit check?

True no-credit-check mortgages are rare and mostly limited to collateral-heavy commercial or hard-money lenders, like some of Gelt Financial's programs. Most residential Non-QM products still pull credit, though minimums can run as low as 600–620 depending on the lender and loan type.

Final Word

Securing a property as a freelancer, business owner, or investor in 2026 doesn't have to be an uphill battle. No-income verification mortgages have evolved beautifully, offering realistic, flexible pathways to homeownership and portfolio expansion. Just keep in mind that these Non-QM products come with stricter down payment rules and higher rates, making comparison shopping absolutely critical.

Don't navigate the complex Non-QM market alone. Head over to Bluerate and use the free AI Chat to seamlessly connect with a top-rated loan officer tailored to your exact scenario today. Let the technology do the heavy lifting so you can focus on finding your dream property.

People Also Read

- 8 Best Non-QM Mortgage Lenders: Which to Choose?

- Best DSCR Loan Lenders: Which to Choose from?

- DSCR Mortgage Guidelines Explained: What and How to Verify?

- Check ITIN Mortgage Guidelines: How to Verify Eligibility in Seconds?

- What are Asset Utilization Mortgage Guidelines? How to Verify in Seconds?

- Bank Statement Mortgage Guidelines: What Is It? How to Verify?