Written by

Eric

Share this article

.svg)

Subscribe to updates

In the Non-QM space, ITIN loans present a fantastic opportunity, but let's be honest, they can be a massive headache to process. Unlike the limited ITIN options under Fannie Mae or Freddie Mac, which follow their standardized guidelines, Non-QM ITIN loans from most lenders have no universal rulebook.

Every lender has its own quirks, making manual guideline checks painfully slow and prone to errors. I used to spend hours digging through massive PDFs just to pre-qualify a single client.

That's why I want to introduce you to Zeitro's Scenario AI. This chat-based assistant lets you verify complex mortgage guidelines across multiple lenders in literal seconds, completely transforming how we work and boosting efficiency.

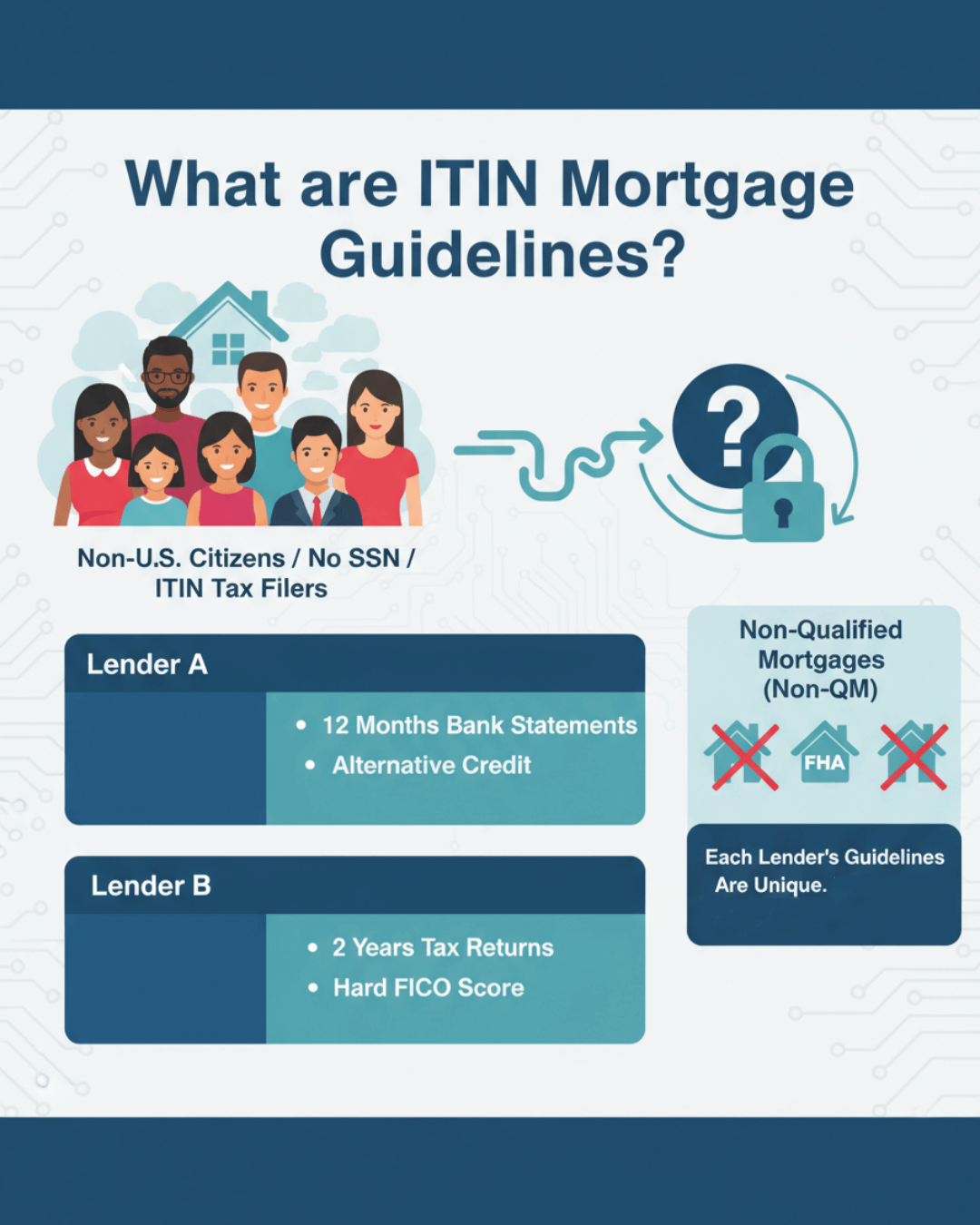

What are ITIN Mortgage Guidelines?

So, what exactly are we dealing with here? ITIN mortgage guidelines are specific lending criteria designed for non-U.S. citizens or individuals who don't have a Social Security Number (SSN) but do file taxes using an ITIN. This demographic typically includes new immigrants, foreign nationals, and expatriates striving for homeownership.

Most ITIN loans are Non-Qualified Mortgages (Non-QM) not backed by federal agencies like the FHA or purchased by government-sponsored enterprises like Fannie Mae or Freddie Mac. This brings us to the biggest challenge: each lender's ITIN guidelines are entirely unique. One institution might accept 12 months of bank statements for income verification, while another strictly demands two full years of tax returns. Some are perfectly fine with alternative credit histories, whereas others require a hard FICO score. This lack of standardization means you can't just memorize a single set of rules. You have to verify the exact criteria for every single deal.

Why Do You Need to Verify Mortgage Guidelines?

Since every institution makes up its own risk matrices, skipping a thorough guideline check is a recipe for disaster. I've seen too many deals fall apart at the last minute because a minor detail was overlooked. Here is why meticulous verification is non-negotiable:

- Prevent Denials: Catching a lender-specific nuance early stops a loan from being rejected in underwriting.

- Save Valuable Time: You need to stop blindly scrolling through hundreds of pages of PDF manuals just to answer a simple eligibility question.

- Protect Your Commission: A smooth, fast close means you get paid faster, maintaining a high ROI for your business.

- Ensure Accuracy: Manual searches often lead to human error. Double-checking ensures your borrower is actually matched with the right program from day one.

Who Needs to Check ITIN Mortgage Guidelines?

You might think checking guidelines is strictly an underwriter's job, but in reality, anyone touching a Non-QM file needs quick access to accurate information.

- Loan Officers & Brokers: You need fast answers to accurately pre-qualify clients and match them with the right wholesale lender without keeping them waiting.

- Account Executives: When brokers call you with weird scenario questions, you must provide instant, correct answers to win their business.

- Loan Processors: You must verify that every piece of alternative documentation perfectly aligns with the target lender's stipulations before submitting the file.

- Underwriters: You are the final gatekeeper. Having a quick way to cross-reference rules ensures compliance and a confident final sign-off.

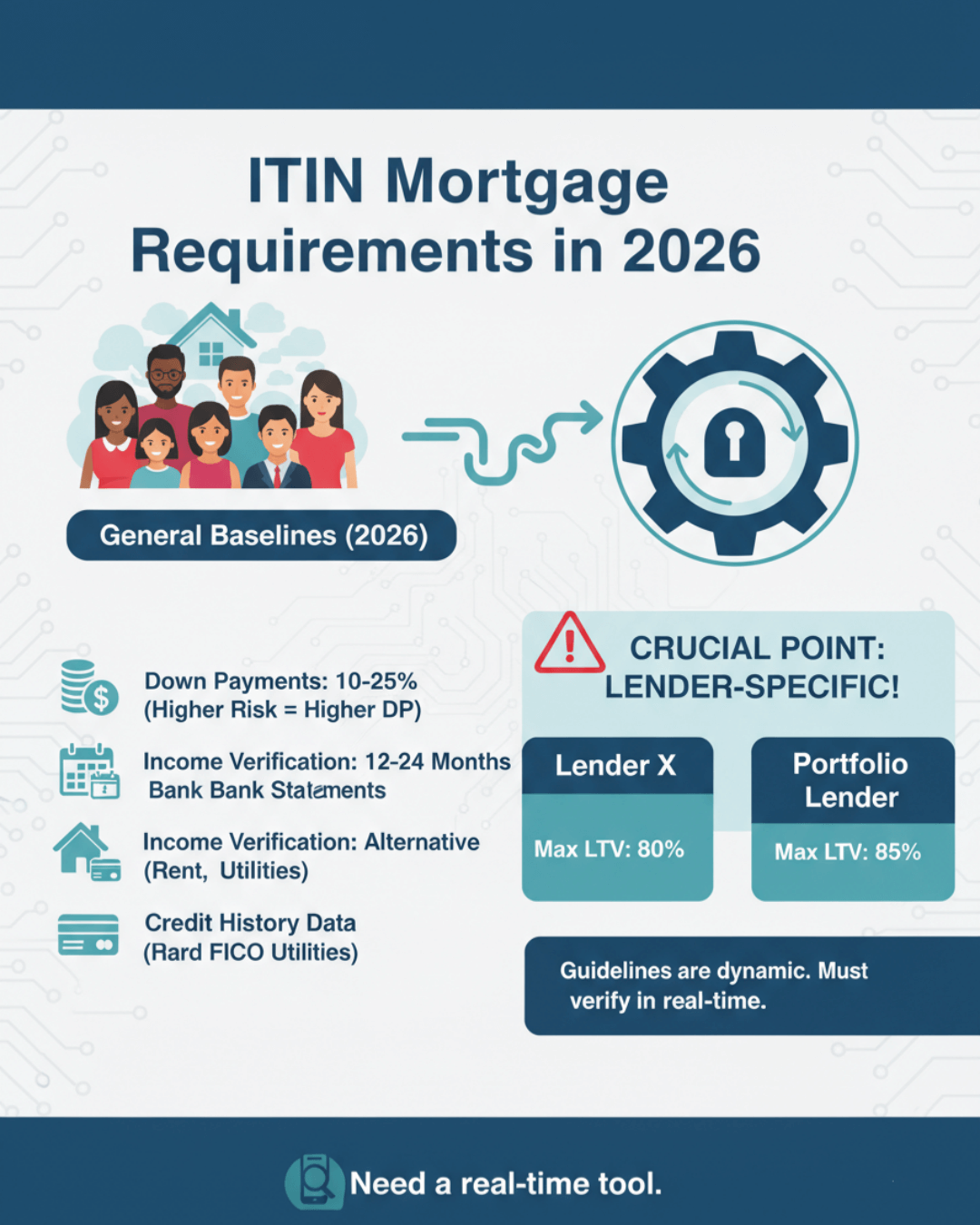

ITIN Mortgage Requirements in 2026

As we navigate the 2026 housing market, ITIN loans are becoming more accessible, but the criteria remain stringent. Generally, you can expect higher down payments, typically ranging from 10% to 20%, and sometimes up to 25% depending on the borrower's risk profile. Since many applicants lack a standard FICO score, lenders often rely on alternative credit, like 12 months of canceled rent checks or utility bills. For income verification, 12 to 24 months of personal or business bank statements are frequently used instead of traditional W-2s.

However, I must emphasize a crucial point: these are just general baselines. A maximum DTI or required reserve amount today might change tomorrow, and it is entirely lender-specific. One bank might cap LTV at 80%, while a portfolio lender pushes it to 85%. This constant shifting is exactly why relying on memory or outdated cheat sheets is dangerous. You need a real-time, dynamic tool to navigate these moving targets.

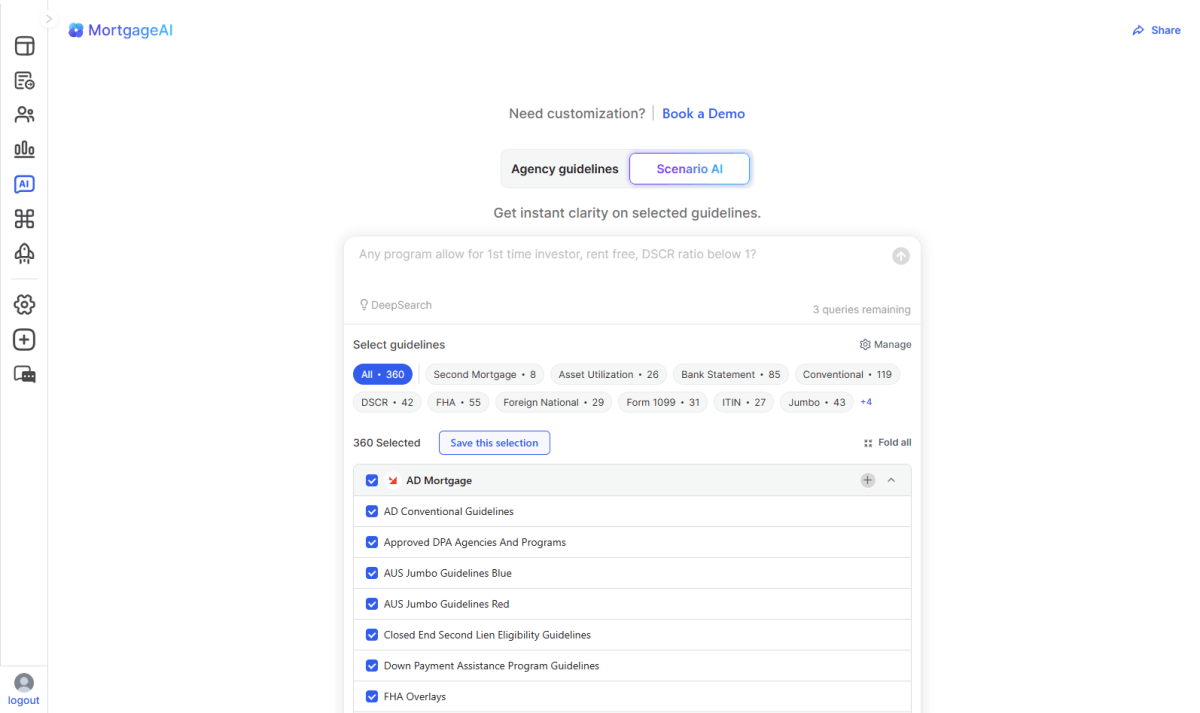

Zeitro Scenario AI: The Smart Way to Verify ITIN Mortgage Guidelines

Instead of wrestling with outdated PDFs, I highly recommend using Zeitro Scenario AI. It is an AI-powered mortgage guideline assistant built specifically to handle the complexities of Non-QM loans like ITIN, DSCR, and Bank Statement programs. The platform currently covers nearly 300 guidelines from major U.S. lenders, including AD Mortgage, AmWest, and AAA Lending, and the database is constantly expanding.

What makes it a game-changer for mortgage professionals? Let me break down the top features:

- Lightning-Fast & Accurate: You can ask anything from broad questions like "What is an ITIN loan?" to hyper-specific eligibility scenarios. It searches through massive guideline databases in seconds, giving you precise answers so you can pre-qualify clients on the spot.

- Verifiable Citations: As loan officers, we naturally distrust AI hallucinations. Zeitro solves this by providing direct citations. Every answer links back to the original source document, giving you 100% confidence that the information is factual and actionable.

- Explain Function: If a specific rule seems confusing, you don't have to start over. You can use the Explain feature to run a secondary query, diving deeper into the selected context for instant clarification.

- Cost-Effective & Multilingual: At just $8 a month, it's incredibly affordable. Plus, it supports multiple languages, including Chinese and English, which is perfect for serving diverse immigrant communities.

- LOS Integration & High ROI: By integrating directly with your Loan Origination System (LOS), it cuts out tedious manual labor, minimizes human error, and speeds up the entire loan lifecycle. Faster approvals mean happier clients and a better bottom line.

FAQs About ITIN Mortgage Guidelines

Q1: Can a borrower get an ITIN loan without a traditional credit score?

Yes, many lenders accept alternative credit history, such as proof of consistent rent or utility payments. However, the exact acceptable documentation varies by institution, so you must verify the specific guidelines.

Q2: Are ITIN loan requirements the same across every lender?

Absolutely not. Because ITIN loans fall under the Non-QM umbrella, every lender creates their own risk matrices. Down payment, LTV limits, and DTI ratios will differ wildly from one bank to another.

Q3: Does Zeitro Scenario AI only handle ITIN loans?

No, it is a comprehensive tool. It covers over 300 different guidelines, including DSCR, Bank Statement, WVOE, Conventional, FHA, and more.

Q4: How reliable is an AI tool for checking complex mortgage rules?

Zeitro is exceptionally reliable because it doesn't just guess. It provides exact citations and source links to the original lender PDFs, ensuring you always have verifiable proof for your loan structuring.

Conclusion

In the 2026 mortgage market, speed and accuracy are what win deals. While Non-QM products like ITIN loans offer a massive opportunity to tap into underserved markets, the sheer volume of conflicting, ever-changing guidelines can slow you down. You simply cannot afford to lose hours cross-referencing PDFs or risking a denial due to an outdated requirement.

It is time to ditch the manual searches and let technology do the heavy lifting. I highly encourage you to give Zeitro Scenario AI a try. It will dramatically boost your underwriting efficiency and give you the confidence to structure complex deals flawlessly. Since they offer 3 free queries every day, there's no risk in testing it out. Head over to Zeitro's website today and see how fast you can verify your next loan scenario!

People Also Read

- 8 Best Non-QM Mortgage Lenders in 2026: Which to Choose?

- Foreign National Mortgage Guidelines: Verify Eligibility Fast

- DSCR Mortgage Guidelines Explained: What and How to Verify?

- 6 Best Loan Origination Software for LOs/Brokers