Written by

Eric

Share this article

.svg)

Subscribe to updates

Have you ever looked at a house, wondering how people afford it, or sat across from someone at a bank and thought, "What do you actually do all day?" I get that question a lot. When I tell people I'm a Loan Officer, they often imagine I just stamp "APPROVED" or "DENIED" on stacks of paper like a cartoon banker.

But the reality is far more dynamic. Being a loan officer isn't just about math. It's about being a detective, a therapist, and a project manager all rolled into one. Whether you are curious about the career or just looking for a new path in 2026, I'm going to pull back the curtain and show you exactly what this job entails, the good, the bad, and the paycheck.

What is a Loan Officer?

Simply put, I am the bridge between a borrower's dream and the bank's money. A Loan Officer (often called a Mortgage Loan Originator or MLO in the housing world) assists borrowers in applying for loans. We evaluate their financial history to determine if they qualify and for how much.

While you can find loan officers in commercial banking or consumer lending (think car loans), most of the buzz, and the money, is in mortgage lending. We work in commercial banks, credit unions, and independent mortgage companies.

Let's talk about the average salary of a loan officer, because that's probably why you're here. According to the U.S. Bureau of Labor Statistics (BLS) data from May 2024, the median annual wage for loan officers was $74,180. However, that number is misleading.

Why? Because this is a sales job. Top producers who work on commission easily clear $100,000 to $200,000+ a year, while those who treat it like a passive 9-to-5 might struggle. If you are a "people person" who loves crunching numbers and has a high tolerance for pressure, this might just be your calling.

Also Read:

- Mortgage Underwriter vs Loan Officer: Which Career Is Best?

- 11 Best Loan Officer Schools for Newbies: Online & Local

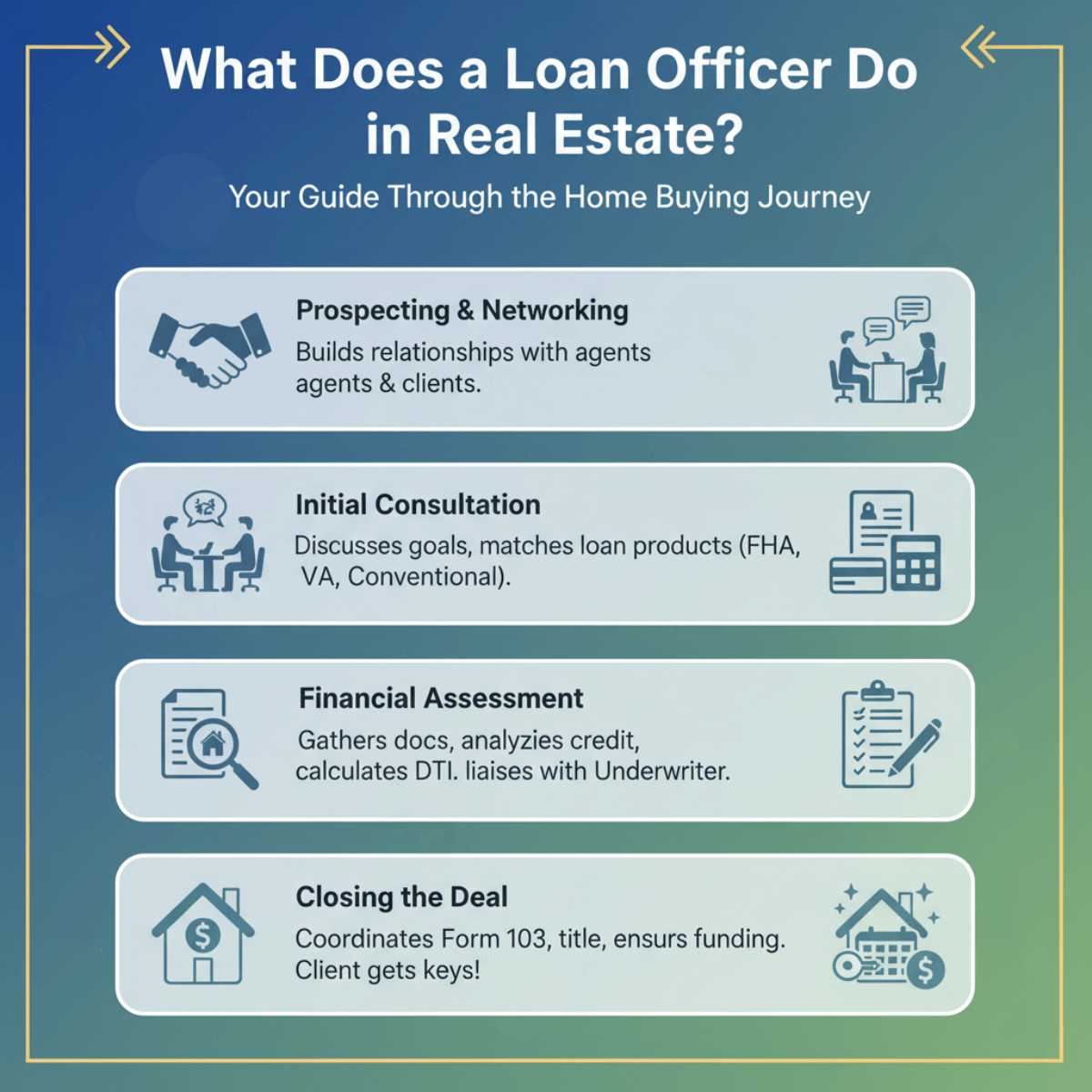

What Does a Loan Officer Do in Real Estate?

This is the core of the job. If you decide to join me in this industry, here is what your day-to-day life will actually look like. It's a cycle of five main duties of loan officers:

Prospecting and "Hunting"

I don't just sit at my desk waiting for the phone to ring. A huge part of my week is spent building relationships. I meet with real estate agents, builders, and past clients to generate referrals. If I don't bring in business, I don't eat. In 2026, this also means maintaining a strong digital presence on social media.

The Initial Consultation

This is where the "therapist" part comes in. I sit down with clients or Zoom with them to discuss their goals. Do they want a lower monthly payment? Are they first-time buyers? I have to listen carefully to match them with the right product, whether that's a conventional loan, an FHA loan for lower credit scores, or a VA loan for veterans.

Financial Assessment & Qualification

Now, I put on my detective hat. I collect the "docs": W-2s, tax returns, and bank statements. I analyze their credit report and calculate their Debt-to-Income (DTI) ratio. This is critical. If I miscalculate income here, the loan will blow up weeks later, and everyone will be furious. My job is to "pre-qualify" them so they can shop for homes with confidence.

The Application (Form 1003) & Processing

Once they find a house, we fill out the Uniform Residential Loan Application (Form 1003). I gather every piece of paper required and submit the file to a "Processor." But my job isn't done. I have to oversee the process, answering questions from the Underwriter, the person who makes the final decision. If the Underwriter asks for a letter explaining a large bank deposit, I have to get it from the client immediately.

Closing the Deal

This is the best part. I coordinate with the title company to ensure the money is wired on time. When the client gets the keys, and I get that "Thank You" text (and my commission check), all the stress feels worth it.

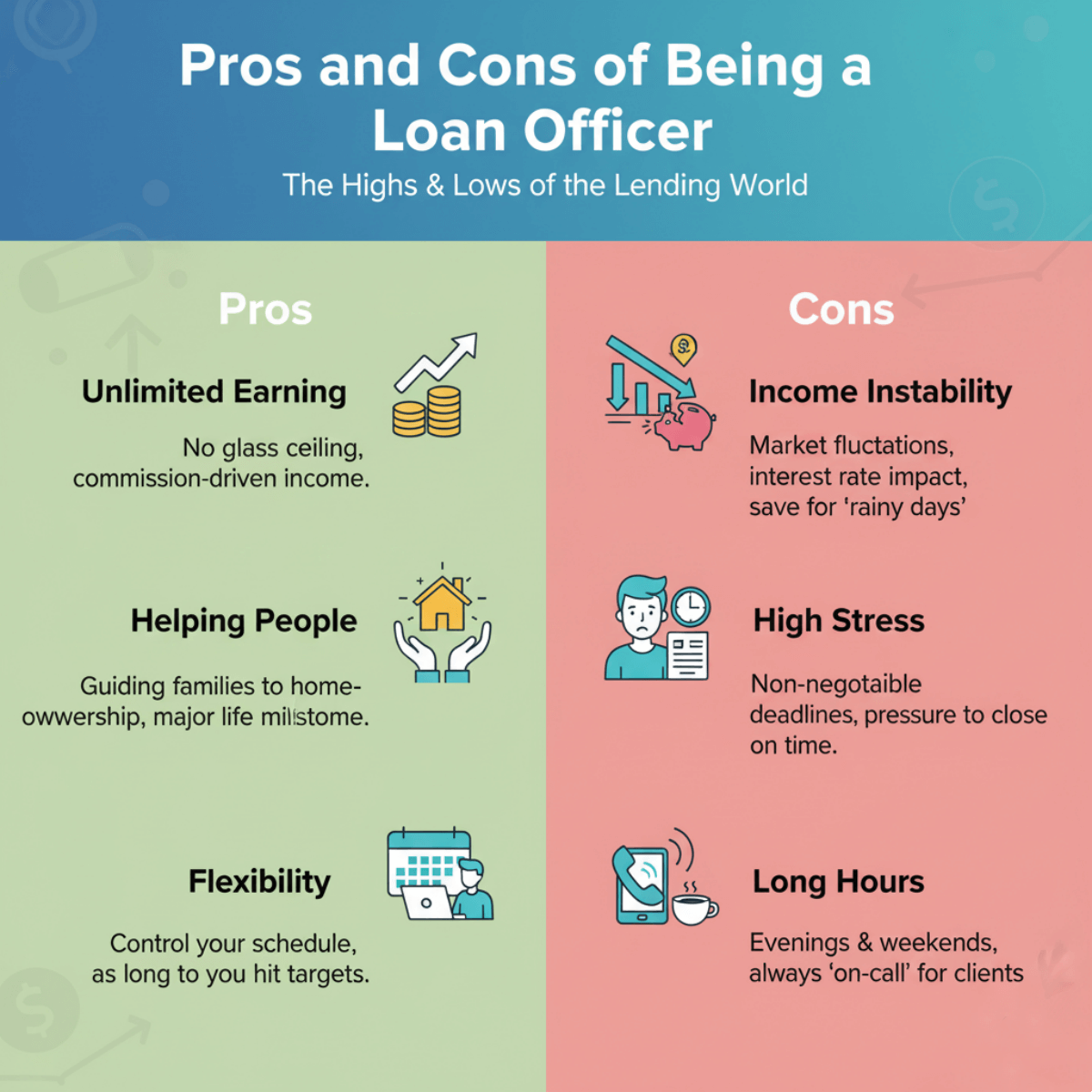

Pros and Cons of Being a Loan Officer

Like any relationship, my relationship with this career has its ups and downs. Here is an honest look:

Pros:

- Unlimited Earning Potential: There is no glass ceiling. If you close more loans, you make more money. It's that simple.

- Helping People: There is a genuine emotional reward in helping a family buy their first home. You are part of a major life milestone.

- Flexibility: I control my schedule. If I need to go to the dentist or pick up my kids, I can, as long as I am hitting my numbers.

Cons:

- Income Instability: If interest rates spike, like they did a few years ago, or the market slows down, your income drops. You have to be good at saving money for rainy days.

- High Stress: Deadlines are non-negotiable. If a loan doesn't close on Friday, a family might have nowhere to sleep. That pressure falls on you.

- Long Hours: Real estate happens on weekends and evenings. You will likely be answering calls at 8 PM on a Tuesday or during Sunday brunch.

How to Become a Loan Officer?

If you are still reading and thinking, "I can do this," here is your roadmap. Unlike becoming a doctor or lawyer, you don't need years of grad school, but you do need a MLO license.

- Meet Basic Requirements: You generally need to be 18 years old and have a high school diploma.

- Pre-Licensing Education: You must complete 20 hours of NMLS (Nationwide Multistate Licensing System) approved education. This covers federal law, ethics, and lending standards.

- Pass the SAFE MLO Exam: This is the big hurdle. It's a tough test with a national pass rate that often hovers around 50-60%. You need a score of 75% to pass.

- Find a Sponsor: You cannot hold an active license on your own. You must be hired or sponsored by a lender or mortgage broker to activate your license.

For a deeper dive into these steps, I recommend checking out this guide on how to become a loan officer.

What Skills Does a Loan Officer Need?

The license gets you in the door, but skills keep you in the room.

- Communication: You must be able to explain complex financial terms like "amortization" or "escrow" in plain English.

- Sales & Persuasion: You are selling yourself as much as the money. Why should they trust you over an online algorithm?

- Attention to Detail: One wrong digit on a social security number can delay a closing by days.

- Tech Savviness: This is non-negotiable now. In 2026, the old-school LOs are retiring. The new generation uses technology to speed up the boring stuff.

Efficiency is the name of the game. I use a CRM (Customer Relationship Management) system to track every lead so no one falls through the cracks. If you want to know what tools the pros are using to automate follow-ups and stay organized, take a look at the best CRM for loan officers. Using the right software is often the difference between closing 5 loans a month and closing 15.

Loan Officer Outlook in 2026

So, is it too late to join? Absolutely not, but the landscape has changed.

According to the BLS, employment for loan officers is projected to grow 2% from 2024 to 2034. While that sounds slow, it translates to about 20,300 job openings each year, mostly due to older officers retiring.

As we head into 2026, we are seeing a "rebound" market. After the high rates of 2023 and 2024, rates have stabilized, and pent-up demand from homebuyers is releasing. However, lenders are being pickier. They want LOs who are self-sufficient and tech-savvy. The days of being an "order taker" are over. The future belongs to the "expert advisor" who uses AI and automation to deliver a faster, smoother experience than the big banks can offer.

Conclusion

Being a Loan Officer is one of the few careers where you can earn a CEO-level salary without a CEO-level degree, if you are willing to work for it. It requires hustle, thick skin, and a genuine desire to serve others.

If you are just starting out, my best advice is to embrace technology immediately. Don't drown in paperwork. Tools like Zeitro can help you automate the heavy lifting, keeping your clients happy and your pipeline full. In this business, your efficiency is your income. Good luck!

![[Solved] How to Calculate Commission Income for Mortgage?](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/6a3ce1b02009d0aba39b3174_how-to-calculate-commission-income-banner.png)