Written by

Eric

Share this article

.svg)

Subscribe to updates

Let's be real: the NMLS SAFE MLO exam is a beast. I've seen incredibly smart people, people with finance degrees, fail this test simply because they underestimated how tricky the questions are. With the national pass rate for first-timer. I've seen incredibly smart people, people with finance degrees, fail this test simply because they underestimated how tricky the questions are.

With the national pass rate for first-timers at 53%, relying solely on your mandatory 20-hour class is a massive gamble. You need a strategy to bridge the gap between "sitting in class" and "passing the exam." After digging through the noise, I've broken down the best prep courses for 2026 that actually teach you how to beat the test, not just memorize definitions.

People Also Read:

- Best Mortgage Loan Officer Training: Which to Pick?

- Guide: What is NMLS? Definitions, FAQs, More

- NMLS License Cost Breakdown: Know Your Every Penny

- Mortgage Loan Officer Salary: How Much Do Loan Officers Make?

- Best Mortgage Companies for New Loan Officers

What are the NMLS Exam Requirements?

Before you drop money on a prep course, make sure you understand the rules. A lot of rookies confuse the Pre-Licensing Education (PE) with Exam Prep. They are not the same. You must take the 20-hour PE class to be legal. You should take an Exam Prep course to actually pass.

To qualify for the National Test with Uniform State Content (UST), here is the checklist you strictly need to follow:

- Finish the PE: Complete your 20 hours of NMLS-approved education.

- Get your NMLS ID: Create an account on the NMLS Resource Center.

- Pay to Play: The exam fee is currently $110.

- Sign the Agreement: You have to accept the Candidate Agreement before you can even look at a calendar.

6 Top-Rated NMLS Test Prep Course in 2026

I didn't just look for the cheapest options. I looked for courses that mimic the anxiety of the real test and offer tools to calm you down. Here is how the top players stack up this year.

The CE Shop: Exam Prep Edge

Price: Around $119 (Look for promo codes)

Access Duration: 6 Months

Course Format: Adaptive online assessments, flashcards, dynamic dashboard.

Best for: Students who want a smart, customized study plan without fluff.

I've used a lot of learning platforms, and The CE Shop's "Exam Prep Edge" feels the most modern. The standout feature here is the initial assessment. It doesn't force you to waste time studying things you already know. If you are already a wizard at Ethics but suck at Federal Law, the system adapts and throws more law questions at you.

The dashboard is slick. It gives you a real-time competency score, so you know exactly when you are ready to take the real thing. It's fully optimized for mobile, so studying on the go is easy. Just note: it's very self-directed. If you need a teacher holding your hand, this might feel a bit too isolated. But for efficiency? It's hard to beat.

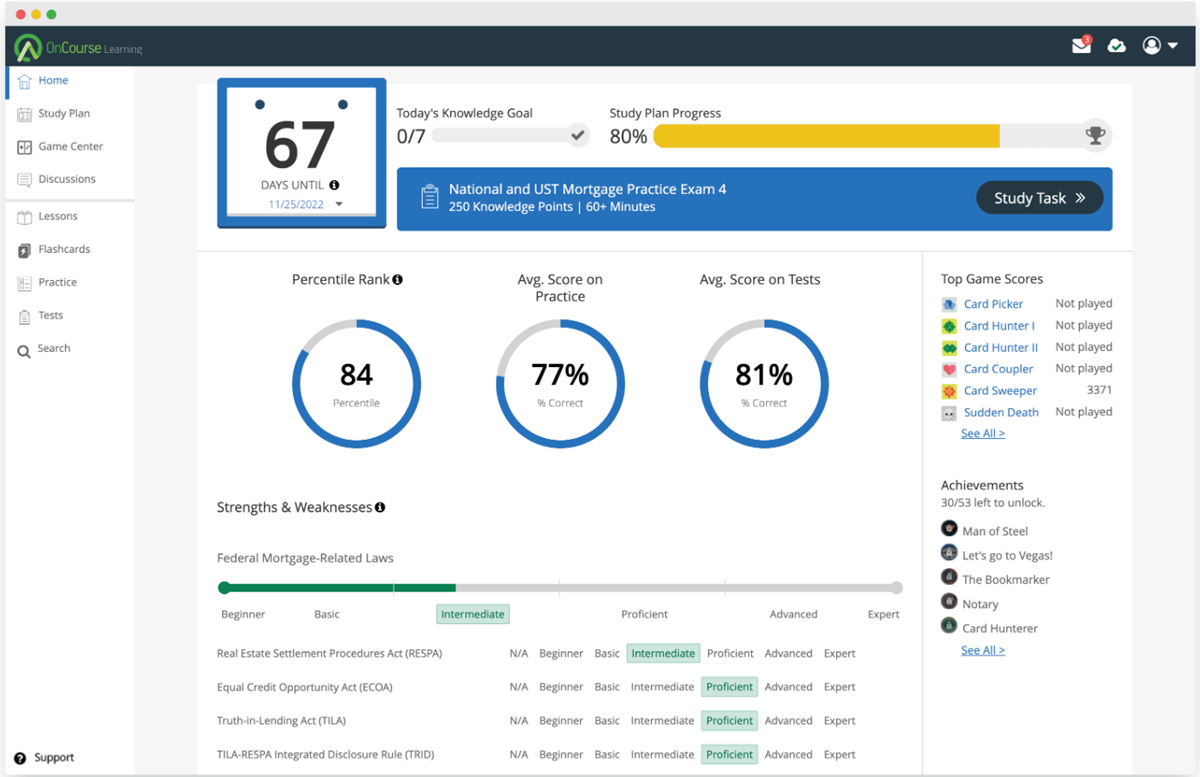

OnCourse Learning: PrepXL

Price: $79 - $149 (Depends on the package)

Access Duration: 1 Year

Course Format: Heavy focus on exam simulation and flashcards.

Best for: People who get nervous about the test interface and want a realistic dry run.

If you have test anxiety, OnCourse Learning's PrepXL is my top recommendation. Why? Because their simulator looks almost identical to the Pearson VUE interface you'll see on exam day. The fonts, the timer, the layout. It's all designed to make you feel comfortable when it counts.

I also appreciate their "explanations." When you get a question wrong, they don't just give you the right answer. They tell you exactly why your choice was wrong. That's where the real learning happens. It's less flashy than The CE Shop, but the bank of 1,000+ questions is rigorous. It's a workhorse of a course.

Mortgage Educators (MEC)

Price: ~$100 - $150

Access Duration: 6 - 12 Months

Course Format: Engaging video lectures, PDF guides, practice quizzes.

Best for: Visual learners who can't stand reading walls of text.

Mortgage law is dry. There's no way around it. But MEC does a fantastic job of making it bearable, largely thanks to their lead instructor, David Luna. The guy is a legend in the industry. He uses humor, costumes, and stories to explain TRID and RESPA rules, which helps the info actually stick in your brain.

This course is perfect if you are an auditory or visual learner. Reading a textbook might put you to sleep, but watching David explains concepts keeps you engaged. The tech platform isn't the newest, but the content quality is top-tier. If you need a human element to keep you motivated, this is the one.

Affinity Mortgage Services: Artricia Woods

Price: $250 - $399 (Premium pricing)

Access Duration: Varies

Course Format: Live webinars, "The Owl" strategy, intensive coaching.

Best for: Retakers. If you've failed before, this is the fix.

I call Affinity the "Bootcamp" option. Artricia Woods is famous for getting people to pass after they've failed 2, 3, or even 4 times. This isn't just a generic question bank. She teaches you how to read the questions. The NMLS exam loves trick wording, and Artricia teaches you to spot the traps.

Her "MLO Exam Prep Master Course" is intense and expensive compared to others, but it works. She breaks down the complex legalese into plain English. If you are struggling and just want to get this over with, the extra cost is worth the investment.

CompuCram

Price: ~$109

Access Duration: 180 Days

Course Format: Vocabulary drills, practice testing, readiness meter.

Best for: Students who want a clear "Green Light" before scheduling.

I'm listing CompuCram here because their system is incredibly binary: Red means stop, Green means go. They have a "Readiness Indicator" on the dashboard that tracks your vocabulary and test scores. My advice? Don't schedule your exam until that bar hits the green zone.

They put a huge emphasis on vocabulary, which is smart because half the battle is just knowing what terms like "hypothecation" mean. The interface is simple and distraction-free. It's not as entertaining as MEC, but it's highly effective for rote memorization and speed drills.

Mometrix NMLS Test Prep Course

Price: $60 - $90 (Book or Monthly Sub)

Access Duration: Lifetime (Book) / Monthly (Online)

Course Format: Physical study guide, e-book, standard practice questions.

Best for: Self-starters on a tight budget.

Sometimes you just want a book. Mometrix is the old-school choice. You can grab their "Secret Study Guide" off Amazon or use their online portal. It's significantly cheaper than the full courses listed above.

It covers all the content, but be warned: it lacks the interactive "adaptive" features of The CE Shop or the realistic simulations of PrepXL. I see this as a great supplement, maybe buy the book to read offline, but pair it with a better digital question bank if you can afford it.

How to Choose the Best NMLS Test Prep Course?

Don't just pick the cheapest one. You need to match the course to your brain. Here is what I tell people when they ask me for a recommendation:

- Know Your Style: If you fall asleep reading, buy MEC for the videos. If you just want to grind questions until your eyes bleed, get CompuCram or PrepXL.

- Check the Guarantee: Look for a "Pass Guarantee." Even if you don't use it, it shows the company backs their product. Just read the fine print. Some require you to score 90% on their practice tests first.

- Mobile Matters: You'll likely be studying in 15-minute bursts on your lunch break. Make sure the site works on your phone.

- Update Frequency: Laws change. Ensure the course explicitly mentions the 2026 UST update.

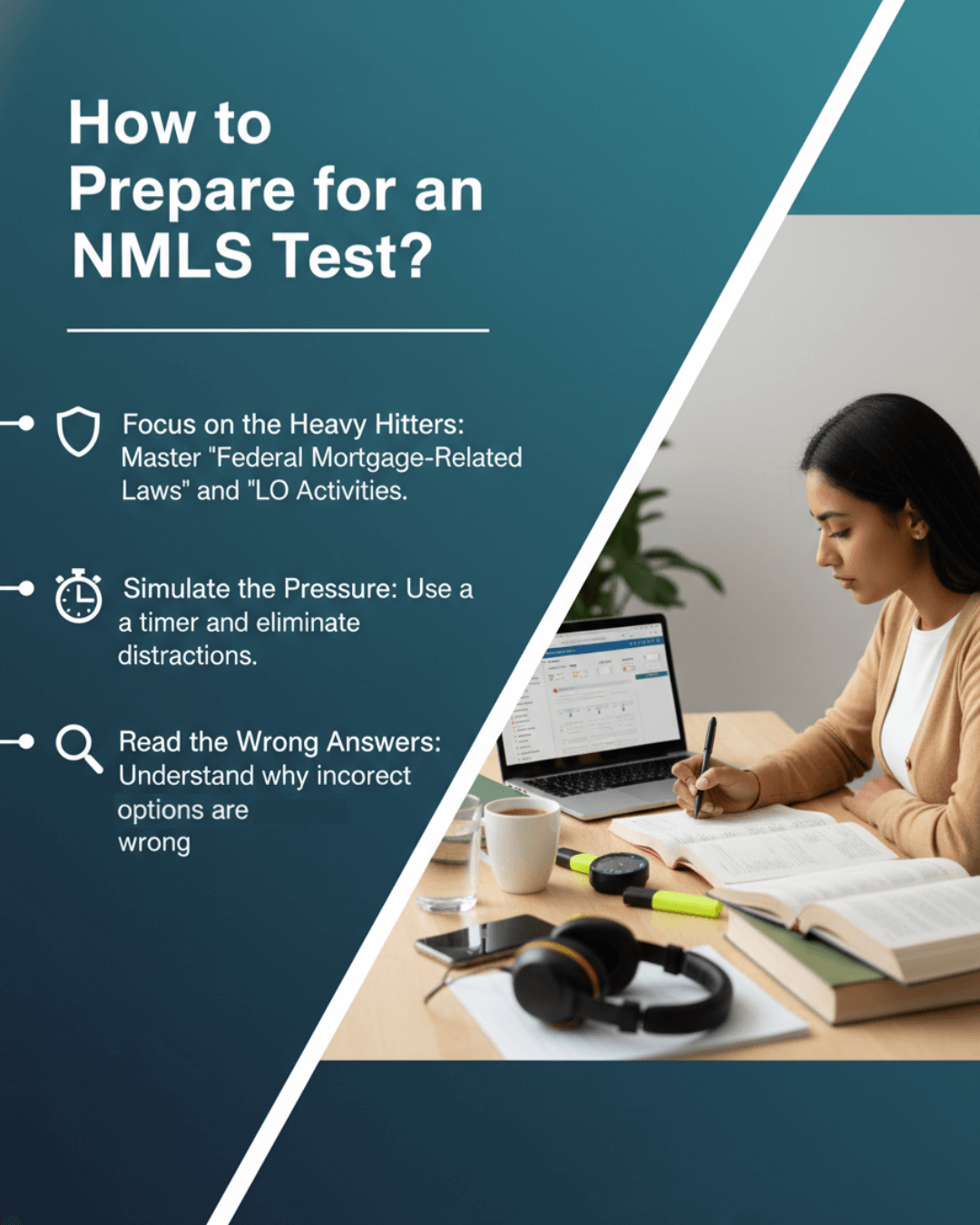

How to Prepare for an NMLS Test?

Buying the course is easy. Doing the work is hard. The biggest mistake I see? People memorize answers instead of learning concepts.

- Focus on the Heavy Hitters: "Federal Mortgage-Related Laws" and "LO Activities" make up nearly 50% of the exam. Master those sections first.

- Simulate the Pressure: When you take practice exams, turn off the TV, put your phone in another room, and use a timer. You need to get used to the stress.

- Read the Wrong Answers: When you review your practice tests, study the wrong answers. Understanding why a distracter is incorrect is more valuable than knowing the right answer.

How to Schedule NMLS Test?

Once your practice scores are consistently hitting 80% or higher, stop procrastinating and book the test.

- Log into the NMLS Resource Center.

- Click the "Composite View" tab and manage your test enrollment.

- Pay the fee (it's non-refundable, so be ready).

- You will then be directed to the Prometric website to pick your seat.

Centers fill up fast. Book at least 2 weeks out to get a morning slot when your brain is fresh.

How Hard Is It to Pass the NMLS Test?

It's tough. I won't lie to you. The first-time pass rate sits around 53%.

The difficulty isn't just the material. It's the question design. You will see questions where two answers look "right," but one is "more right" based on federal law. It tests your ability to apply the law in a scenario, not just recite a definition.

How Many Hours to Study for NMLS?

Your 20-hour PE class is just the appetizer. To actually pass, you need to put in overtime.

I recommend an additional 20 to 40 hours of dedicated study time. Don't cram this into one weekend. Spread it out over 2 to 3 weeks, doing 2 hours a night. This gives your brain time to absorb the acronyms and regulations.

Conclusion

Getting your MLO license is a game-changer for your career, but you have to clear this hurdle first. Don't try to wing it.

- If you want the best tech, go with The CE Shop.

- If you need the most realistic practice, grab OnCourse Learning.

- If you've failed before and need a rescue mission, hire Affinity.

Pick the tool that works for you, put in the hours, and go crush that exam. You've got this.