Written by

Eric

Share this article

.svg)

Subscribe to updates

I remember when I first decided to look into becoming a Mortgage Loan Originator (MLO). I searched Google for a simple roadmap, but 90% of the results were just ads trying to sell me a $300 course or confusing government jargon that didn't make sense. It was frustrating.

That is why I am writing this guide. I want to cut through the noise. This is the exact, no-nonsense roadmap to obtaining your NMLS license in 2026. Whether you are looking to work for a mortgage broker or a direct lender, the core process is federal, but the execution requires attention to detail. This guide is not selling you a course. It is designed to help you navigate the NMLS Resource Center, pass the "beast" of an exam, and actually get your license active so you can start your career.

People Also Read

- Best Mortgage Loan Officer Training in 2026: Which to Pick?

- 8 Best Mortgage Lead Generation Companies in 2026: Don't Miss

- [Proven] How to Generate Mortgage Leads for Free? 6 Methods

- 6 Best Loan Origination Software for LOs/Brokers in 2026

What is an NMLS License?

First, let's clear up a common misconception. The NMLS (Nationwide Multistate Licensing System) is just the database, and it doesn't actually "issue" the license. Your specific state government, like the DRE or DFPI in California, or the DFS in New York, issues the license through this system.

If you want to originate loans for a non-bank lender like a mortgage broker, you are required by the federal SAFE Act to be state-licensed. This is different from working at a big bank like Chase or Wells Fargo, where you only need to be "registered."

When you start this process, you will be assigned an NMLS Unique Identifier (NMLS ID). Think of this like a "Social Security Number" for your mortgage career. It stays with you for life, regardless of which company you work for or which state you move to. It allows consumers to look you up and verify your history, which is a key part of maintaining public trust in our industry.

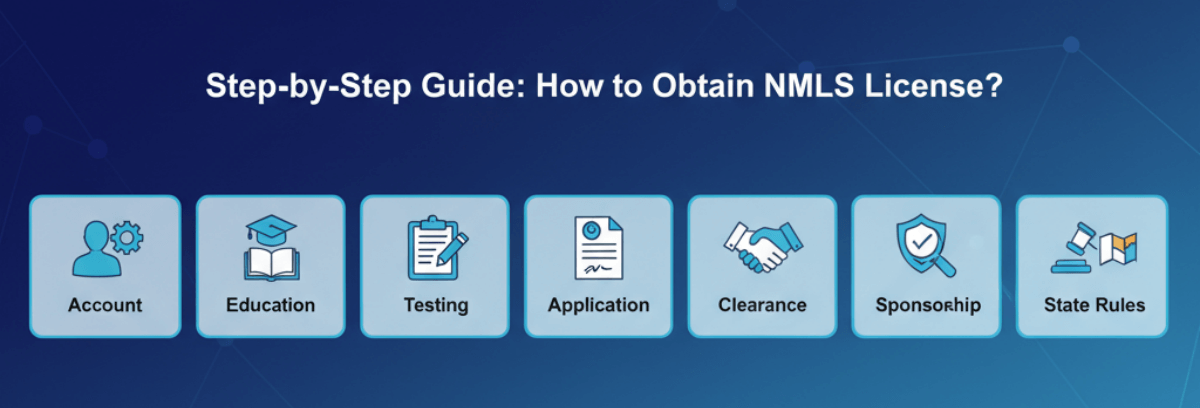

Step-by-Step Guide: How to Obtain NMLS License?

Getting licensed involves a mix of federal mandates and state-specific rules. It can feel overwhelming, so I have broken it down into a logical 7-step roadmap.

The Roadmap at a Glance:

- Account: Create NMLS Login & Get ID

- Education: Complete 20-Hour Pre-License Course

- Testing: Pass the SAFE MLO Exam

- Application: Submit Form MU4

- Clearance: Background Checks (Fingerprints/Credit)

- Sponsorship: Find an Employer

- State Rules: Complete specific state requirements

STEP 1. Create an NMLS Account & Get Your ID

Your journey begins at the NMLS Resource Center. You need to request an account to get into the system. When you visit the site, look for the "Log in to NMLS" button and select "Request an Account."

You will be filing as an Individual. The system will ask for your personal information to generate your account. Once you complete this, you will immediately receive your NMLS ID number. Write this number down. You will need it for everything: signing up for classes, scheduling your exam, and eventually printing it on your business cards.

During this setup, ensure your name matches your government ID exactly. If your driver's license says "Jonathan" but you register as "John," you will be turned away at the testing center later.

STEP 2. Complete Pre-License Education (PE)

Before you can even touch the exam, federal law requires you to complete 20 hours of Pre-Licensure Education (PE). You cannot just read a book. You must take a course from an NMLS-Approved Course Provider.

The 20 hours are strictly structured:

- 3 Hours: Federal Law

- 3 Hours: Ethics (Fraud, Consumer Protection)

- 2 Hours: Non-Traditional Mortgage Lending

- 12 Hours: Electives

Most people take this online. You can choose "Online Instructor-Led", similar to a Zoom class, or "Online Self-Study." Be warned: NMLS requires a security measure called BioSig ID. You will have to draw a password with your mouse every time you log in to prove it is really you taking the course. It's annoying, but mandatory for compliance.

STEP 3. Pass the SAFE MLO Exam

This is the biggest hurdle. The SAFE MLO Test with Uniform State Content (UST) is not easy. It consists of 125 multiple-choice questions (115 scored, 10 unscored experimental), and you are given 190 minutes to finish." You need a score of 75% to pass.

Do not underestimate this test. The questions are designed to be tricky, often using double negatives or asking for the "BEST" answer among four "correct" looking options. It covers federal laws (TILA, RESPA, ECOA), ethics, and general mortgage knowledge.

What if I fail? Don't panic. You can retake it after waiting 30 days for the first three attempts. After failing a third time, you must wait 180 days before a fourth attempt. Study hard so you don't get stuck in that 6-month penalty box.

STEP 4. Apply for Your License

Once you pass your exam, you need to formally ask the state for your license. This is done by filing Form MU4 (Individual Form) inside the NMLS portal.

Log in, go to the "Filing" tab, and pay the fees. The fees usually include an NMLS processing fee around $30, a credit report fee, and the specific application fee for your state. For example, if you are applying in California via the DRE or DFPI, the state fee will be added here.

Once you submit the MU4, your license status will likely show as "Pending-Incomplete" or "Pending-Review." This is normal. It just means the state regulators are now looking at your file.

STEP 5. Complete Background Checks

Technically, you often initiate this step while filing your MU4, but it is a distinct requirement. You must authorize a Criminal Background Check (CBC) and a Credit Report.

- Fingerprints: You cannot just go to a local police station. You must schedule an appointment through the NMLS-approved vendor Fieldprint, which links directly to the NMLS system, to send your prints to the FBI.

- Credit Report: Regulators aren't necessarily looking for a perfect 800 credit score. They are looking for "financial responsibility." If you have current tax liens, government debt, or recent foreclosures, you might have to provide a detailed letter of explanation.

- Disqualifiers: A felony conviction involving fraud, dishonesty, or money laundering at any time is an automatic ban. Other felonies within the last 7 years are also usually disqualifiers.

STEP 6. Find an Employer

Here is the catch that trips up many new LOs: You can pass the test and pay the fees, but your license will not become "Active" until a licensed employer sponsors you.

Until you are hired, your status will sit as "Approved - Inactive." You need to interview with Mortgage Brokers or Lenders. Once you accept an offer, their compliance manager will log into NMLS and request "Sponsorship" of your license. Once the state approves that relationship, your license flips to "Active," and you can officially start originating loans.

Also Read: Best Mortgage Companies for New Loan Officers in 2026

STEP 7. Meet State-Specific Rules

While the "Uniform State Test" (UST) covers most states, some regulators have extra homework.

For instance, to obtain a DRE MLO endorsement in California, you must hold an active DRE real estate license. Under the DFPI for CRMLA or CFL, you obtain a separate individual MLO license without needing a real estate license, but you might need specific education. Other states like Texas or Florida may have their own specific education modules (e.g., a 2-hour state law course) that must be taken in addition to the standard 20-hour PE. Always check the State Licensing Requirements Checklist on the NMLS website for your specific target state.

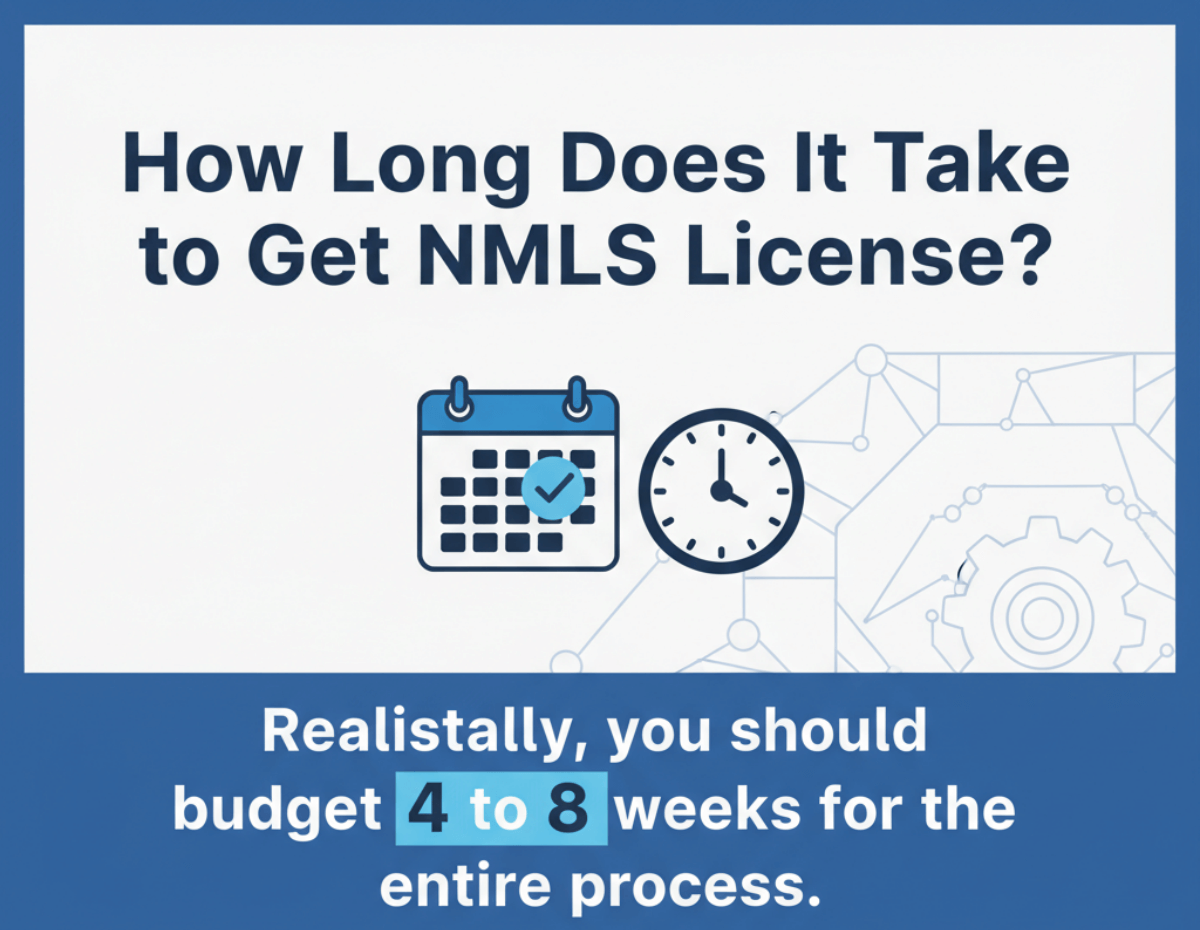

How Long Does It Take to Get NMLS License?

Realistically, you should budget 4 to 8 weeks for the entire process.The 20-hour course can be done in a week if you treat it like a full-time job. Studying for the exam typically takes another 2 weeks. Once you pass, the background check and state review can take anywhere from a few days to a month, depending on how backed up the FBI or state regulators are. If you have a "clean" history (no criminal hits, clear credit), the approval is usually faster.

How Hard Is It to Get NMLS?

I won't lie to you. The exam is difficult. The first-time pass rate for the SAFE MLO test is around 58%. It is generally considered harder than the Real Estate Agent exam because it is less about common sense and more about memorizing specific federal regulations and timelines (e.g., "How many days does a lender have to send a Loan Estimate?"). However, the process itself isn't "hard" technically. It's just bureaucratic. If you follow the steps and actually study for the test, it is 100% achievable.

FAQs About Getting an NMLS License

Q1. How much does it cost to take the NMLS?

National Exam fee (typically $110), NMLS processing fee ($30), Credit Report ($15), FBI Background Check (around $36.25), plus 20-hour course ($200–$400) and state fees. Total often $600–$1,000, depending on state.

Also Read: NMLS License Cost Breakdown 2026: Know Your Every Penny

Q2. How long does it take to study for NMLS?

Most successful candidates spend 2 to 4 weeks preparing. I recommend taking the exam immediately after your course while the laws are fresh in your mind.

Q3. Can I take a NMLS test online?

Yes. You can take the test online from home through the approved remote proctoring service, such as ProProctor by PSI, with strict security like room inspections via webcam. However, the security is intense. They will inspect your room via webcam, and you cannot have paper, pens, or even a watch near you.

Q4. What is the NMLS exam pass rate?

The national pass rate for first-time test takers is typically in the mid-50% range. It drops to the mid-40% range for subsequent attempts, which highlights the importance of studying correctly the first time.

Q5. Is getting a mortgage loan officer license worth it?

If you are self-driven, absolutely. The income potential is uncapped (commission-based), and with interest rates predicted to stabilize in 2026, demand for refinancing and purchases is expected to rise.

Q6. How many times can I take the NMLS test?

You can take it 3 times, with a 30-day wait between each attempt. If you fail the 3rd time, you must wait 180 days before you can book a 4th attempt.

Final Word

Obtaining your NMLS license is the barrier to entry for a lucrative career in financial services. It protects consumers and ensures you know the laws. My advice? Do not rush the education part. The laws you learn in that 20-hour course are the same ones that will keep you out of trouble when you start signing loans.

If you are ready to start, head over to the NMLS Resource Center today and create your account. The process might seem long, but ticking off that first box is the most important step you will take. Good luck!