Written by

Eric

Share this article

.svg)

Subscribe to updates

As a loan officer, I've lost count of how many times a lucrative deal stalled simply because checking the guidelines took too long. The demand for Foreign National Mortgage Guidelines is skyrocketing as international investors flock to the US real estate market. However, navigating the maze of differing requirements across lenders can be a nightmare. You don't want to spend hours reading PDFs only to find out your borrower's visa type isn't accepted.

To stay competitive, you need a way to verify eligibility instantly. In my workflow, I've started using tools like Zeitro Scenario AI, which allows me to chat with an AI to cross-reference different lenders' guidelines in seconds. It's a game-changer for efficiency.

People Also Read:

- What Are FHA Mortgage Guidelines? Verify FHA & Overlays Quickly

- Conventional Mortgage Guidelines: What and How to Check Quickly?

- Jumbo Mortgage Guidelines: Check Eligibility Quickly and Accurately

- VA Mortgage Guidelines: What Are They and How to Check Them Quickly?

- Mortgage Guidelines 2026: What Are They? How to Verify?

- Should Mortgage Lender and Broker Build In-House AI Tools?

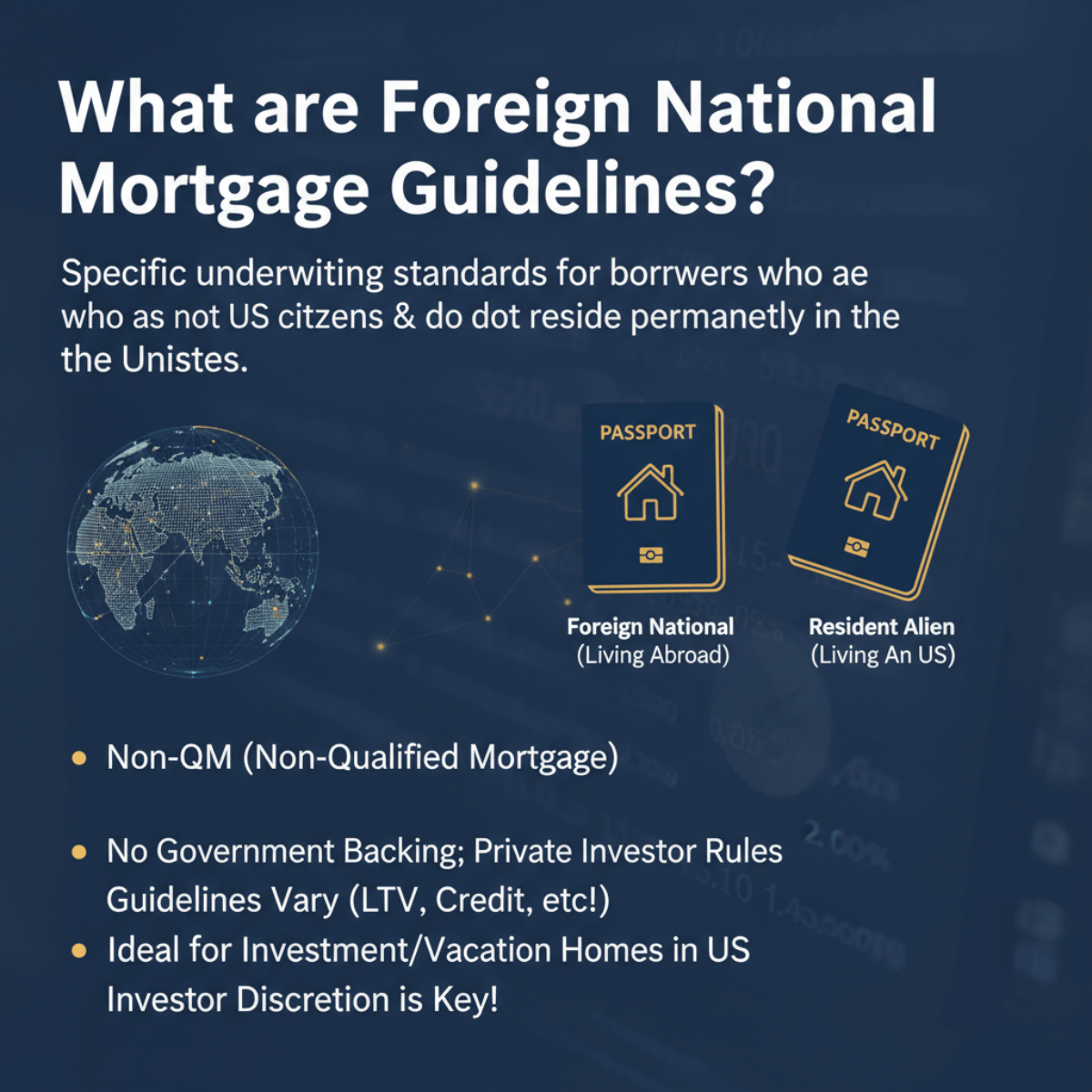

What are Foreign National Mortgage Guidelines?

Foreign National Mortgage Guidelines are the specific underwriting standards used by lenders to approve borrowers who are not US citizens and do not reside permanently in the United States. Unlike standard Conventional loans backed by Fannie Mae or Freddie Mac, these loans almost always fall under the Non-QM (Non-Qualified Mortgage) category.

Since there is no government backing, private investors and wholesale lenders set the rules. This means the guidelines, ranging from allowed LTVs (Loan-to-Value) to credit requirements, vary wildly from one lender to another. As brokers, we must understand that "Foreign National" is distinct from "Resident Alien." These guidelines are specifically designed for borrowers living abroad who want to purchase investment properties or vacation homes in the US. The key here is realizing that investor discretion plays a huge role. What gets denied by one wholesale lender might be a perfect fit for another.

Why Offer Foreign National Mortgages?

You might be wondering, "Why should I complicate my pipeline with these complex loans?" The answer is simple: Information Gain. This is a massive, underserved market with high ROI. Many originators shy away from it because it's "too hard," leaving more commission on the table for those of us who know how to navigate it.

Here are the main reasons why mastering these guidelines is a must:

- Real Estate Investment Growth: Foreign investors love US real estate for its stability. They are often looking for rental properties, which pairs perfectly with DSCR (Debt Service Coverage Ratio) loan programs.

- Vacation Home Purchases: High-net-worth individuals from Canada, Europe, and Asia frequently buy vacation homes in states like Florida, California, and Texas.

- Relocation Scenarios: Executives moving to the US often need to buy before their US credit is established.

- Diversification: When the conventional refi market dries up, Non-QM foreign national loans keep your volume high.

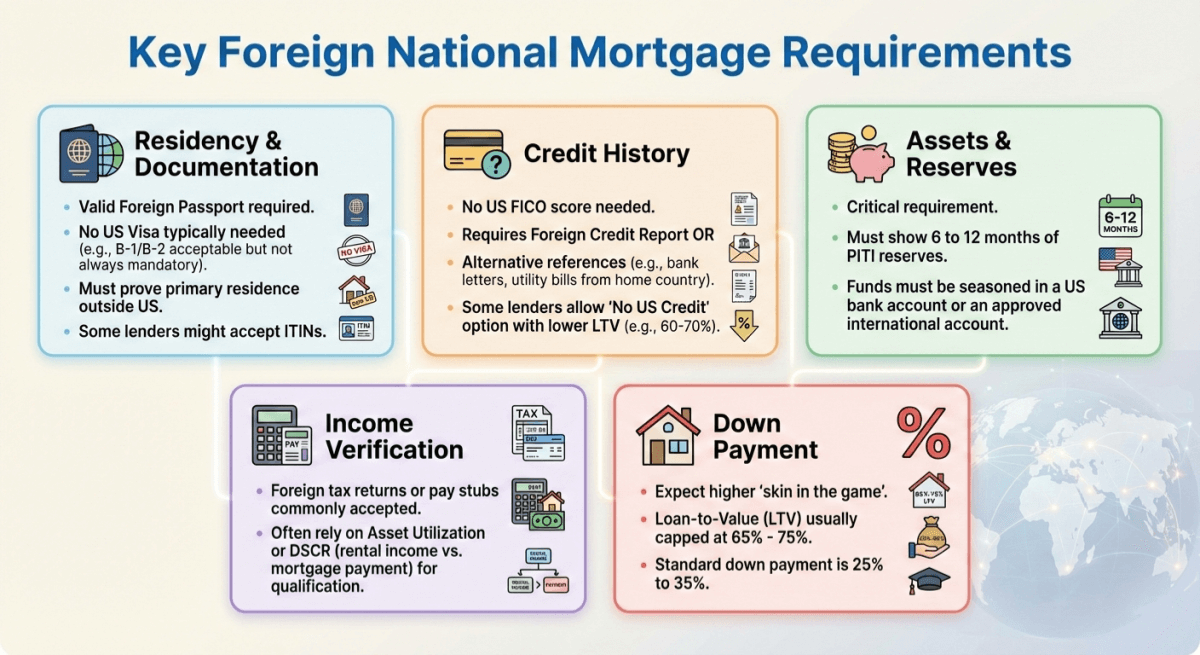

Key Foreign National Mortgage Requirements

While I mentioned that every lender has their own "flavor" of guidelines, there are common denominators you need to look out for. When I'm pre-qualifying a client, these are the pillars I check first:

- Residency & Documentation: The borrower typically needs a valid foreign passport. Importantly, no US visa is required. Many lenders accept borrowers with no US visa at all, while others may require specific types like B-1/B-2 for business/tourism or even ITINs. They must prove they live primarily outside the US.

- Credit History: Since they lack a US FICO score, most guidelines require a Foreign Credit Report or alternative credit references (like letters from their home country's bank or utility company). Some lenders offered by Zeitro allow for "No US Credit" options if the LTV is lower (e.g., 60-70%).

- Assets & Reserves: This is critical. Lenders typically require 6 to 12 months of reserves (PITI) seasoned in a US bank account or an approved international account.

- Income Verification: Foreign tax returns or pay stubs are commonly accepted by many lenders, alongside Asset Utilization or DSCR. Instead, we rely on Asset Utilization or DSCR (rental income vs. mortgage payment) to qualify the loan.

- Down Payment: Expect to ask for more skin in the game. LTVs are usually capped at 65% - 75%, meaning a 25% to 35% down payment is standard.

Pro Tip: Tool to Quickly Check Foreign National Mortgage Guidelines?

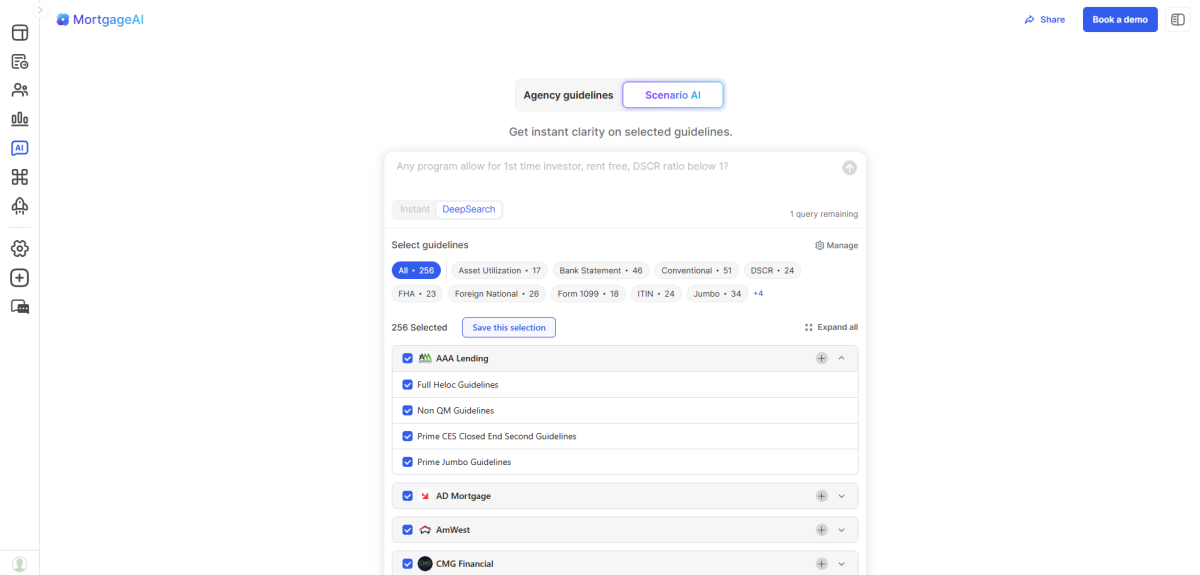

Here is the reality of our job: skimming through 300-page PDF guides for 15 different lenders is inefficient. It kills your momentum. This is where Zeitro Scenario AI has become an essential part of my tech stack.

It is an AI-Powered Mortgage Guideline Assistant specifically designed for loan professionals. Instead of manually searching, I just type a query like, "Which lenders allow 75% LTV for a foreign national with no US credit?" and it gives me an answer based on actual data.

Why It Shines Through?

- Massive Coverage: It covers nearly 300 guidelines, including 18 specific Foreign National guidelines from major lenders like AD Mortgage, Greenbox, and Lux.

- Deep Search Capability: You can customize the search scope. I can select 5 specific lenders and ask the AI to compare their reserve requirements instantly.

- Citations for Trust: This is the most important feature for me. It doesn't just give an answer. It provides citations (source links). I can click through to verify the exact page in the guideline, giving me the confidence to quote terms to my client.

- Handle "Fuzzy" Scenarios: You don't need perfect phrasing. Whether asking a broad question or checking specific eligibility, the AI understands mortgage context.

- Cost-Effective: It costs as little as $8/month. Considering the commission on one Foreign National deal, the ROI is unbeatable.

FAQs About Foreign National Mortgage Guidelines

Q1. What is a foreign national mortgage loan?

It is a mortgage loan designed for non-US citizens who reside outside of the United States. These loans allow foreign borrowers to purchase investment properties or second homes in the US without having a US credit history or Social Security Number.

Q2. Can a foreign national get a mortgage in the US?

Yes, absolutely. While they cannot typically use conventional financing, they can obtain loans through Non-QM lenders. hese loans usually require a larger down payment (typically 25-35%+, with LTVs capped at 65-75%) and use the property's cash flow (DSCR) or the borrower's assets to qualify, rather than US-based income.

Q3. Does Fannie Mae allow foreign nationals?

This is a common misconception. Fannie Mae allows loans for non-US citizens who are lawful residents (e.g., Green Card holders or those with valid work visas like H1B) and have US credit. However, for a true "Foreign National" who lives overseas and has no US credit history, Fannie Mae is generally not an option. You must look toward Non-QM products.

Final Word

Navigating Foreign National Mortgage Guidelines doesn't have to be a guessing game. The opportunity in this market is huge for us as Loan Officers and Brokers, provided we have the right information at our fingertips. The key to closing these deals is speed and accuracy, knowing exactly which lender accepts your client's unique scenario before you even submit the file.

Stop wasting hours digging through outdated PDFs. I highly recommend you try Zeitro Scenario AI. It brings clarity to the chaotic world of Non-QM guidelines and gives you the citations you need to underwrite with confidence. It's time to work smarter, not harder.

![[Ultimate Guide] How Do I Analyze Self-Employed Tax Returns?](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/6a48809aea04f502e012dac9_analyze-self-employed-tax-returns-banner.png)