Written by

Eric

Share this article

.svg)

Subscribe to updates

As a Loan Officer or Broker, few things are as frustrating as navigating the labyrinth of government loan requirements. You think you know the rules, but then a specific lender's overlay throws a wrench in your deal. VA Mortgage Guidelines are the rulebook set by the Department of Veterans Affairs, detailing how we originate, process, and underwrite loans for our service members.

But here is the catch: knowing the "VA Handbook" isn't enough. You also need to know how each lender interprets it. How do you quickly verify if a borrower with a 580 FICO score qualifies with Lender A versus Lender B without reading endless PDFs?

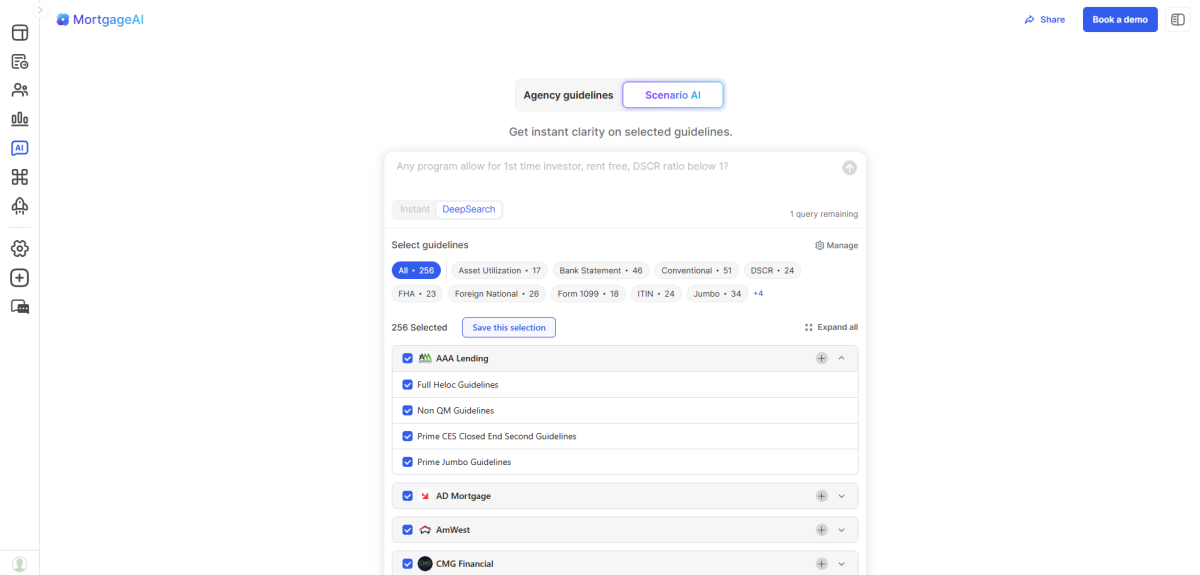

In this guide, I'll break down the essentials of VA guidelines and share a workflow hack I've recently adopted: using Zeitro's Scenario AI. It's a chat-based tool that lets me verify guidelines across different lenders instantly, saving me hours of manual research.

People Also Read:

- What Are FHA Mortgage Guidelines? How to Verify FHA & Overlays Quickly?

- Conventional Mortgage Guidelines: What and How to Check Quickly?

- Jumbo Mortgage Guidelines: Check Eligibility Quickly and Accurately

- Should Mortgage Lender and Broker Build In-House AI Tools

- Mortgage Guidelines 2026: What Are They? How to Verify?

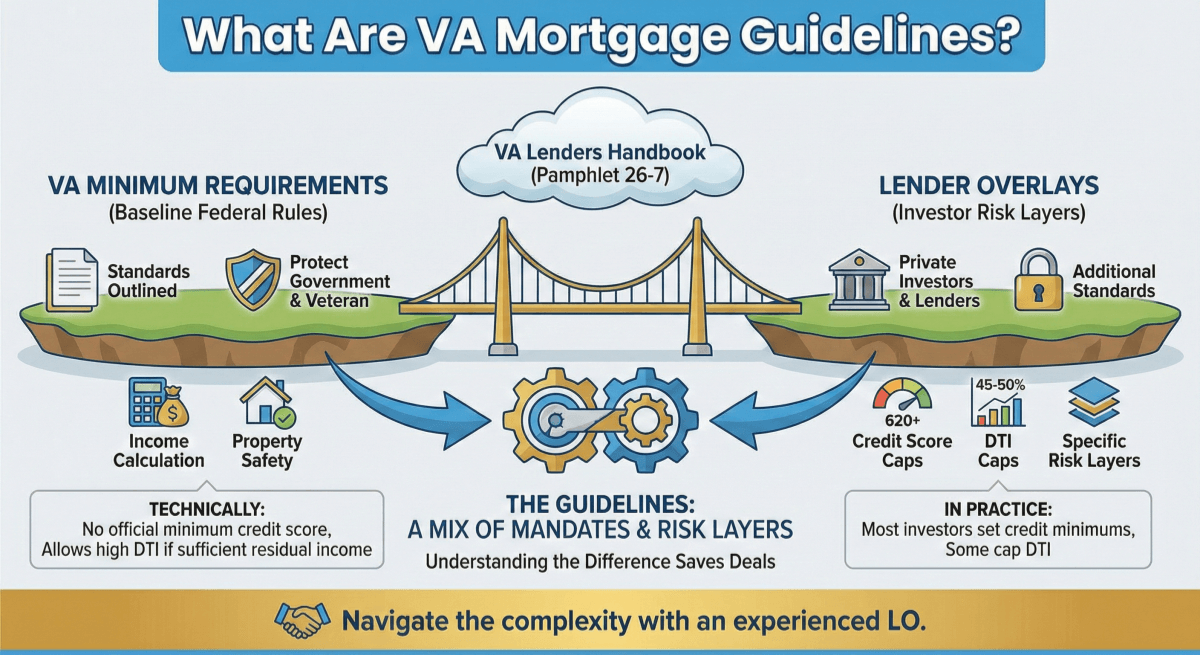

What Are VA Mortgage Guidelines?

At their core, VA Mortgage Guidelines are the standards outlined in the VA Lenders Handbook (Pamphlet 26-7). These rules dictate everything from income calculation to property safety. They exist to protect the government (which guarantees a portion of the loan) and the veteran.

However, from my experience in the trenches, there is a critical distinction between "VA Minimum Requirements" and "Lender Overlays."

While the VA technically doesn't set a minimum credit score, most investors do. While the VA allows for high Debt-to-Income (DTI) ratios if there is sufficient residual income, some lenders cap it at 45% or 50%. This is where the confusion often lies. The "Guidelines" generally refer to the baseline federal rules, but in practice, you are always dealing with a mix of federal mandates and specific investor risk layers. Understanding this difference is what separates an average LO from a top producer who can save a deal that others denied.

Who Do VA Mortgage Guidelines Apply To?

These guidelines are not for everyone. They are strictly for eligible borrowers who have served our country. Before we even look at credit or income, we must establish eligibility through a Certificate of Eligibility (COE).

Generally, the guidelines apply to:

- Veterans: Those who have served the required length of time and were discharged under conditions other than dishonorable.

- Active-duty Service Members: Currently serving personnel, usually after 90 days of continuous service.

- National Guard and Reserve Members: Typically require 6 years of service, though 90 days of active duty (Title 10 or 32) can also qualify them.

- Surviving Spouses: Unremarried spouses of veterans who died in service or from a service-connected disability.

If your client doesn't fit one of these buckets, the VA guidelines and the zero down payment benefit won't apply.

Why Are VA Mortgage Guidelines Important?

You might ask, "Why can't we just wing it and ask the underwriter later?" As professionals, strictly adhering to these guidelines is non-negotiable for three massive reasons:

- The VA Guaranty: The primary selling point of this loan is that the VA guarantees 25% of the loan amount against default. If we miss a guideline, say, we miscalculate Residual Income or ignore a Minimum Property Requirement (MPR), the VA can void that guaranty. That is a disaster for the lender.

- Secondary Market Salability: Most lenders don't keep loans on their books. They bundle them into Ginnie Mae securities. If a loan doesn't meet the guidelines, it becomes "unsalable." This leads to forced buybacks, which can bankrupt smaller mortgage shops.

- Veteran Protection: These guidelines are designed to stop predatory lending. Rules regarding fees (like the 1% origination cap) and strictly regulated closing costs ensure the veteran isn't being taken advantage of. Following the rules isn't just about compliance. It's about ethics.

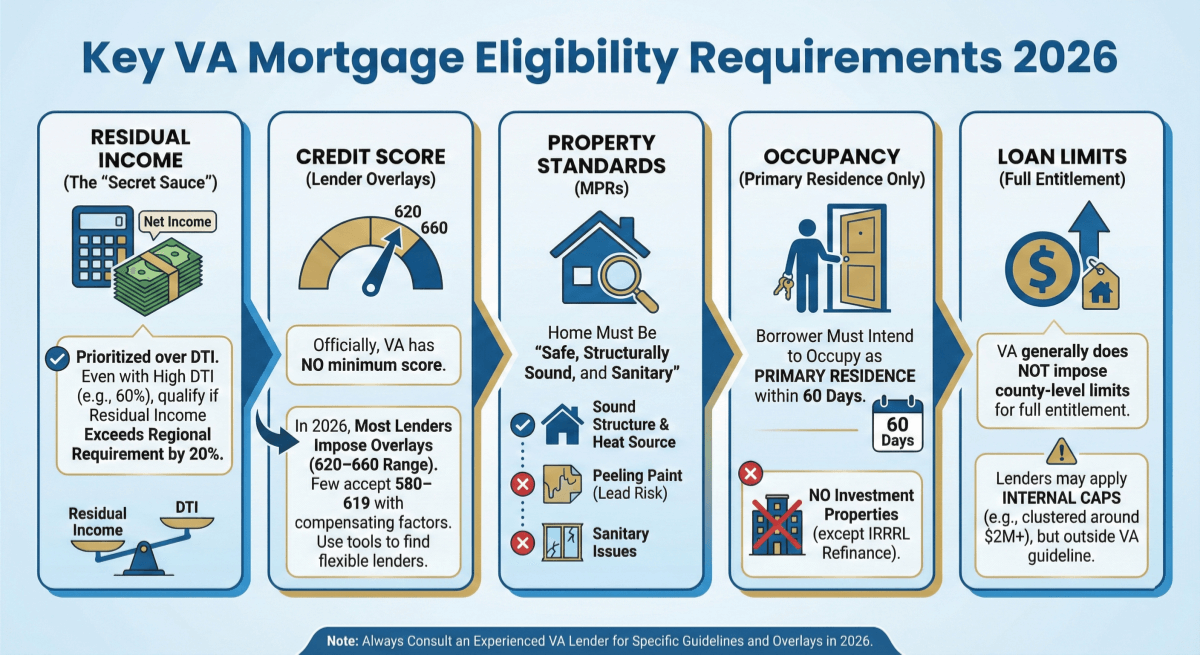

VA Mortgage Eligibility Requirements 2026

As we move through 2026, the fundamental pillars of VA lending remain stable, but attention to detail is key. Here is what you need to focus on to get your files clear-to-close:

- Residual Income (The "Secret Sauce"): Unlike Conventional or FHA loans that obsess over DTI, VA guidelines prioritize Residual Income (net income remaining for family expenses). Even with a high DTI (e.g., 60%), a borrower can qualify if their residual income exceeds the regional requirement by 20%.

- Credit Score: Officially, the VA does not set a minimum credit score. However, in 2026, most lenders impose overlays typically in the 620–660 range. A few may approve 580–619 with compensating factors. Use tools or lender‑board overlays to identify banks that allow lower‑score files.

- Property Standards (MPRs): The home must be "safe, structurally sound, and sanitary." This isn't just a cosmetic inspection. Issues like peeling paint (lead risk) or lack of a permanent heat source are deal-killers.

- Occupancy: The borrower must intend to occupy the property as their primary residence within 60 days. Investment properties are a no-go unless it is an IRRRL (refinance).

- Loan Limits: For borrowers with full entitlement, VA generally does not impose county‑level loan limits, so lenders can finance high loan amounts with zero‑down as long as the veteran qualifies on income, credit, and appraisal value. Many lenders will still apply internal or investor‑level ceilings (for example, clustered around $2M+), but those fall outside the VA guideline itself.

Pro Tip: How to Verify VA Mortgage Guidelines in Seconds with AI?

Here is the reality of our job: You have a client who is a borderline approval. You need to know, "Which lender allows a Chapter 13 bankruptcy buyout with 0x30 payment history?"

In the past, I would log into five different lender portals (Allregs), download massive PDFs, and Ctrl+F my way through hundreds of pages. It was exhausting and prone to human error.

Recently, I started using Zeitro's Scenario AI, and it has completely changed my workflow.

Zeitro is an AI-powered assistant specifically built for mortgage guidelines. It covers nearly 300 guidelines, including 22 specific VA Mortgage Guidelines from major lenders like Freedom Mortgage, AD Mortgage, CMG Financial, and HomeXpress.

More Amazing Features to Explore:

- Deep Lender Coverage: It doesn't just give you generic VA rules. I can ask specific questions about specific lenders. For example, "Does Freedom Mortgage require a lower DTI than the standard VA guideline?"

- Citations for Confidence: As an underwriter or LO, you can't just trust a chatbot. Zeitro provides citations (sources) for every answer. I can click the link and see the exact page in the guideline. This is crucial for E-E-A-T.

- Handles Specific Scenarios: Whether it's a blurry eligibility question or a complex prequal scenario, the AI understands the context.

- Incredible Speed: It scans hundreds of documents in seconds.

- Cost-Effective: It starts at just $8/month. Considering one saved deal pays for a lifetime subscription, the ROI is a no-brainer.

- Explain Feature: If a guideline is confusing (legalese is hard!), the "Explain" feature breaks it down into plain English for me.

Instead of calling an Account Executive and waiting 4 hours for a call back, I get the answer in 10 seconds.

FAQs About VA Mortgage Guidelines

Q1. What disqualifies a house from a VA loan?

The house must meet Minimum Property Requirements (MPRs). Common disqualifiers include severe structural damage, a leaking roof, broken windows, lack of a permanent heating system, or peeling paint (due to lead risks in homes pre-1978). If it's not "safe, sound, and sanitary," it won't pass.

Q2. What is the VA 5-year rule?

The "5‑year rule" language is frequently used by originators, but it is not an official VA term for VA loan eligibility itself. In the context of surviving‑spouse benefits, VA's Dependency and Indemnity Compensation (DIC) criteria include situations where a veteran was rated totally disabled for at least 10 years before death, or since release from active duty and for at least 5 years immediately before death, under certain conditions.

For VA purchase‑loan underwriting, lenders apply their own lookbacks. For example, a foreclosure may require around 2 years seasoning, but VA itself does not publish one uniform "5‑year rule" applicable across all VA‑loan scenarios.

Q3. What is the VA 1% fee rule?

The VA's 1% rule caps a lender's origination fee at 1% of the loan amount. When lenders charge a flat 1% origination fee, they generally may not separately itemize lender‑overhead charges (processing, underwriting, document preparation, etc.) within the same fee bucket.

Many third‑party costs, for example, appraisal, title, recording, and certain administrative services, can still appear on the Closing Disclosure as separate, itemized charges, even when the 1% cap is used.

Q4. What is the downside of a VA loan?

The main downside is the VA Funding Fee, which can be as high as 3.3% for subsequent use (unless the veteran has a service-connected disability, which waives the fee). Additionally, strict property requirements make buying "fixer-uppers" difficult, and the loan is for primary residences only.

Final Word

Mastering VA Mortgage Guidelines is a superpower in this industry. It allows you to serve those who served us, often getting them into homes when other loan types fail. However, the sheer volume of lender overlays can be overwhelming.

Don't let manual research bottleneck your pipeline. Efficiency is the name of the game in 2026.

I highly recommend trying Zeitro's Scenario AI. Whether you are working on a tricky Non-QM deal or a standard VA file, it gives you accurate, cited answers from over 15 mainstream lenders in seconds. You can even try it for free (3 queries/day).

Stop guessing, stop searching, and start closing more loans with confidence.