Written by

Eric

Share this article

.svg)

Subscribe to updates

Last checked and updated on July, 2026

I still remember sitting across from my loan officer a few years back, watching him shake his head at my file. I had the cash flow. I had savings sitting in the bank. But because I wrote off a big chunk of my business expenses on my tax returns, the number on my 1040 didn't match reality and the conventional bank said no.

That story isn't rare. Heading further into 2026, self-employment and gig work keep growing, but agency underwriting still leans hard on W-2s and tax transcripts. That gap is exactly where Non-QM (Non-Qualified Mortgage) lending steps in. These loans aren't the reckless "no-doc" products that helped tank the market in 2008. They're a regulated, common-sense path for borrowers whose income doesn't fit a standard box — self-employed professionals, real estate investors, and people rebuilding after a credit event. Below is my own working list of the lenders I'd point a borrower toward, built from what I've seen in the field, borrower feedback, and public industry rankings.

8 Top Non-QM Mortgage Lenders

Not every Non-QM lender solves the same problem. Some are built for investors who qualify off rental income alone; others exist to give someone a second shot after bankruptcy. I've grouped these eight by what they actually do best — product depth, underwriting flexibility, and how willing they are to look past a credit score.

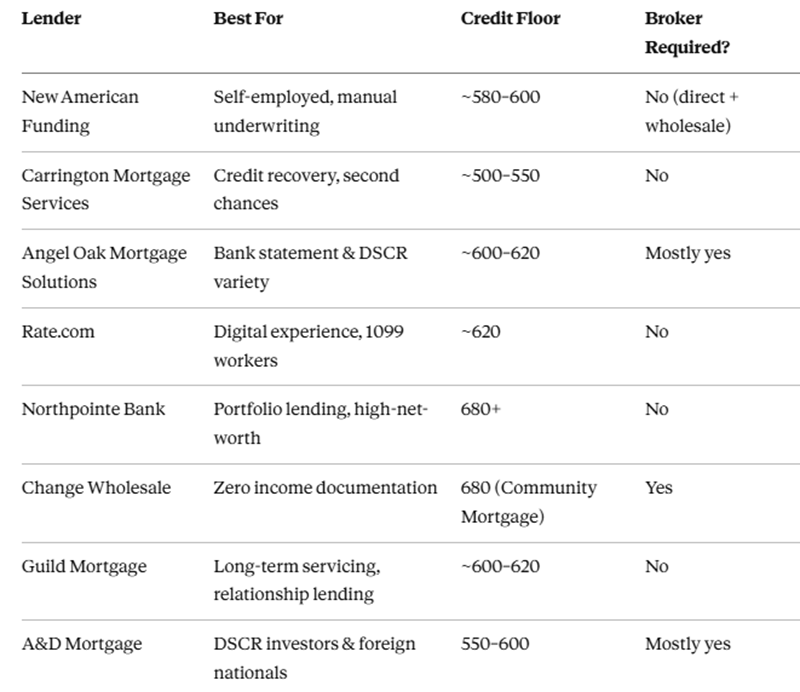

#1 New American Funding

Best For: Manual Underwriting & Self-Employed Flexibility

New American Funding has built a name around treating borrowers as more than a FICO number. They're one of the larger lenders still doing genuine manual underwriting — a real underwriter reads your file instead of an algorithm spitting out a decline. Their self-employed mortgage programs let business owners qualify off 12 or 24 months of bank deposits instead of net income from a tax return, which matters a lot if your accountant is good at their job and your taxable income looks smaller than your real cash flow.

Pros

- Willing to weigh the full financial picture, not just a credit score

- Strong reputation for bilingual, culturally aware service in Hispanic communities

- Flexible on credit if compensating factors, like a larger down payment, are present

Cons

- Rates run higher than a standard conforming loan, as with any Non-QM product

- Manual underwriting takes longer and can carry higher origination fees

#2 Carrington Mortgage Services

Best For: Credit Challenges & Second Chances

If a foreclosure or bankruptcy is sitting on your credit report, Carrington is usually near the top of my list to check first. They've built their reputation serving borrowers other lenders turn away, and their risk tolerance goes lower than most — some programs will consider scores in the 500s where competitors cap out around 620 to 640, provided you bring a meaningful down payment to the table.

Pros

- One of the more forgiving underwriting shops in the industry

- Can often approve sooner after a Chapter 13 bankruptcy than agency guidelines allow

- Deep bench in manual FHA underwriting alongside Non-QM

Cons

- Higher rates and closing costs reflect the added risk they're taking on

- Expect closer scrutiny of your ability to repay given the lower credit bar

#3 Angel Oak Mortgage Solutions

Best for: Bank statement loans and product variety

Angel Oak has been in the wholesale Non-QM space since it rebuilt after 2008, and among mortgage brokers, the name is close to shorthand for Non-QM itself. Their bank statement loan lets self-employed borrowers qualify off 12 or 24 months of personal or business deposits with no tax returns required, and their Investor Cash Flow program qualifies rental properties on the property's own cash flow rather than the borrower's paycheck — the DSCR model.

Pros

- Underwriters who specialize in complex files tend to move faster than a generalist bank

- Non-QM Jumbo options for loan amounts well above standard county limits

- Long track record in the space adds a layer of funding stability

Cons

- Almost entirely wholesale — you'll need a broker with an existing relationship, not a retail branch

- Guidelines are followed rigidly since their loans get securitized

#4 Rate.com

Best For: Technology & Digital Experience

If uploading documents to a portal beats faxing paperwork for you, Rate.com (formerly Guaranteed Rate) is worth a look. Their online platform remains one of the smoother mortgage experiences around, and while they're best known for conventional volume, their Non-QM menu now includes solid 1099-only programs built for freelancers and gig workers who don't have a stack of traditional pay stubs.

Pros

- Real-time loan tracking and a genuinely intuitive interface

- Deep capital relationships give access to a wide product menu

- A good fit for tech-comfortable borrowers who want speed

Cons

- A messy or unusual file can get lost in a large, high-volume operation

- Credit overlays can run a bit tighter than a specialist like Carrington

#5 Northpointe Bank

Best For: Portfolio Lending & Medical Professionals

Northpointe keeps many of the loans it originates on its own books instead of selling them off right away, which gives it room to make exceptions a lender bound to secondary-market rules simply can't. I've seen them work well for physicians and residents who need student loan debt excluded from their debt-to-income calculation, and for borrowers with complex assets but modest taxable income.

Pros

- More room to tailor a loan to an unusual financial picture

- Higher loan-to-value options for qualified professional borrowers

- Competitive Non-QM pricing for borrowers with strong credit

Cons

- Program availability shifts by state

- Prefers borrowers with good credit (680+) rather than credit-repair cases

#6 Change Wholesale

Best for: Zero income documentation

Change Wholesale, part of The Change Company, holds a CDFI (Community Development Financial Institution) certification from the U.S. Treasury, first granted in 2018. That status lets it offer programs regular banks legally can't. Its flagship Community Mortgage requires no income or employment documentation at all — a real echo of pre-2008 "no-doc" lending, done within today's compliance framework. Current guidelines call for a 680 minimum credit score, up to 80% loan-to-value, and at least six months of reserves, so it's built for a creditworthy borrower with an unconventional income trail rather than someone with damaged credit.

Pros

- Minimal paperwork if you fit the target profile

- Mission-driven focus on borrowers historically overlooked by traditional banks

- Qualification leans on collateral and credit history over income

Cons

- Wholesale-only, so you'll need a broker to access it

- Program isn't available in every state, and eligibility is narrower than it first appears

#7 Guild Mortgage

Best for: Long-term relationship and servicing

Guild has been around for decades and, unlike many lenders that sell off servicing rights, tends to keep the loan on its own books after closing, meaning the company you applied with is likely still the one you're mailing payments to years later. For Non-QM borrowers, Guild offers flexible options for the self-employed and asset-rich borrowers, and its loan officers generally push to verify income upfront so you walk in with a real pre-approval instead of a rough pre-qualification letter.

Pros

- Consistently strong customer satisfaction scores in industry surveys

- Wide branch network for borrowers who want an in-person relationship

- A stable lender that rarely shifts guidelines mid-process

Cons

- Digital tools lag behind a lender like Rate.com

- Somewhat more conservative on credit than Carrington or Angel Oak

#8 AD Mortgage

Best for: Real estate investors and foreign nationals

A&D Mortgage has climbed fast in this space. Scotsman Guide's own rankings show A&D moving from the No. 7 spot on its Top Non-QM Lender list in 2022 to the No. 1 position by 2024 — a jump that reflects real production growth, not just marketing. Their core strength is DSCR lending, where the loan qualifies off a rental property's own cash flow instead of the borrower's personal income, which makes them a natural fit for investors scaling a portfolio. They're also active in the foreign national space, working with non-U.S. citizens buying American real estate, and among the smaller group of Non-QM lenders willing to count verified cryptocurrency holdings toward reserve requirements.

Pros

- Fast closings and light personal documentation for investment properties

- Open to crypto assets for reserves and creative use of 1099 income

- High loan amounts available for larger investment properties

Cons

- Rates and guidelines can move quickly with market conditions

- Wholesale-heavy, so finding a broker who knows their programs matters

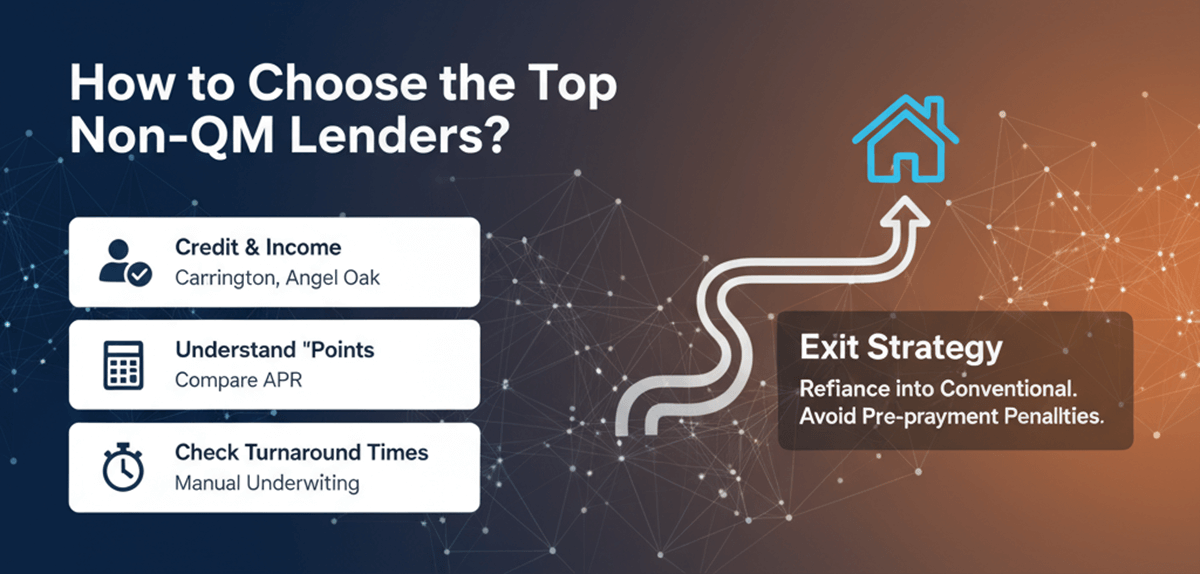

How to Choose the Top Non-QM Lenders?

Chasing the lowest advertised rate is the wrong starting point here, since Non-QM pricing depends almost entirely on your specific risk profile. This is the checklist I actually use:

- Name your real obstacle first. Rejected for credit? Start with Carrington. Rejected for how your income is documented? Look at Angel Oak or New American Funding.

- Compare APR, not just rate. Non-QM loans often carry discount points , upfront fees that buy down your rate, so the APR tells you the true cost, not the headline number.

- Ask about turnaround time. Manual underwriting takes longer than an automated approval. If you're on a tight 30-day closing, ask the lender directly whether that's realistic.

- Plan your exit. Non-QM is usually a bridge, not a forever loan. Ask about prepayment penalties before you sign, since you'll likely want to refinance into a conventional loan once your financials look cleaner on paper.

- Check if you need a broker. Several of the strongest Non-QM lenders, including Angel Oak, Change Wholesale, and A&D Mortgage, sell mainly through wholesale channels. A retail-facing lender like New American Funding or Rate.com may be simpler if you'd rather work directly with the lender.

Finding a Non-QM Lender Near You

Non-QM availability isn't uniform across the country. Some programs are licensed in every state, others in a handful. Rather than cold-calling brokers off a map search, it helps to search for a loan officer who lists Non-QM or self-employed lending as an actual specialty in your state, whether you're in Texas, Florida, South Carolina, or anywhere else. Bluerate lets you do exactly that, filtering by state and specialty so you're not stuck with whichever broker answers the phone.

FAQs About Best Non-QM Lenders

Q1. What credit score do you need for a non-QM loan?

There is no single answer, but generally, the floor is lower than conventional loans. While most lenders prefer a score of 620 to 680, specialists like Carrington Mortgage Services can go as low as 500 to 580. However, keep in mind: the lower your score, the larger the down payment required (often 20-30%) and the higher your interest rate will be.

Q2. Where to find the best non-QM mortgage lenders near me?

This is where things have changed in 2026. In the past, I would have told you to call random brokers from Google Maps. But the problem is, many local loan officers are "assigned" to you and may not have deep experience with Non-QM products.

I recently discovered Bluerate, and it's a game-changer. Instead of being stuck with whoever picks up the phone, Bluerate allows you to search for local non-QM loan officers who specifically list "Non-QM" or "Self-Employed" as their specialty. You can view their profiles, compare their expertise, and book a free consultation directly. It puts the power back in your hands to choose an expert who actually understands your niche.

Q3. Can you refinance out of a non-QM loan?

Absolutely, and you should plan to! I always advise treating a Non-QM loan as a "bridge". You use it to secure the house now. Then, after 12 to 24 months, when your tax returns show more income or your credit score has healed, you refinance into a Conventional or FHA loan to get a lower rate. Just watch out for those pre-payment penalties I mentioned earlier (usually effective for the first 1-3 years).

Q4. What is the 3-7-3 rule in mortgage?

This is a compliance rule meant to protect you, but it can delay your closing if you aren't careful.

3: You must receive your Loan Estimate within 3 business days of applying.

7: You must wait at least 7 business days after receiving that estimate before you can sign the final closing docs.

3: If the APR on your loan changes by more than 0.125% (which happens often in Non-QM if terms are tweaked), a new 3-day waiting period is triggered before you can close.

Conclusion

A "no" from a big bank in 2026 isn't the end of the road to homeownership. Whether you're an entrepreneur working with New American Funding, an investor building a portfolio through A&D Mortgage, or someone rebuilding credit with Carrington, there's very likely a lender built for your exact situation.

My honest advice: don't try to shop eight lenders on your own. The Non-QM landscape shifts by state and by lender, sometimes month to month. Use a tool like Bluerate to find a loan officer who specializes in exactly this kind of file, compare real terms side by side, read the fine print on prepayment penalties, and pick the lender that's actually built around your situation — not just your tax return.

People Also Read

- Best CRM for Loan Officers 2026: Which One Suits You Most?

- 6 Top Loan Origination Systems 2026: Close More Loans Quicker

- 8 Best Mortgage Lead Generation Companies in 2026: Don't Miss

- [Tips] Where to Buy Mortgage Leads? Warm Leads for LOs