Written by

Eric

Share this article

.svg)

Subscribe to updates

Last checked and updated on July, 2026

People assume real estate finance only rewards those chasing sales quotas. But if you want the financial upside of housing without the cold calls, underwriting is the quiet alternative. A quick note before we dive in: this guide covers mortgage underwriters, the people who evaluate home-loan risk. If you landed here looking for insurance underwriting pay, that's a different field with its own licensing path and salary curve.

As of 2026, a mortgage underwriter earns a solid national average somewhere between $65,000 and $90,000, depending on which data source you trust and how much experience is behind the number. I've watched underwriters with a few years and the right certifications clear six figures without ever touching a sales pipeline. Below is the real data, pulled straight from job boards and government wage reports, plus how the pay structure actually works and whether the desk suits you.

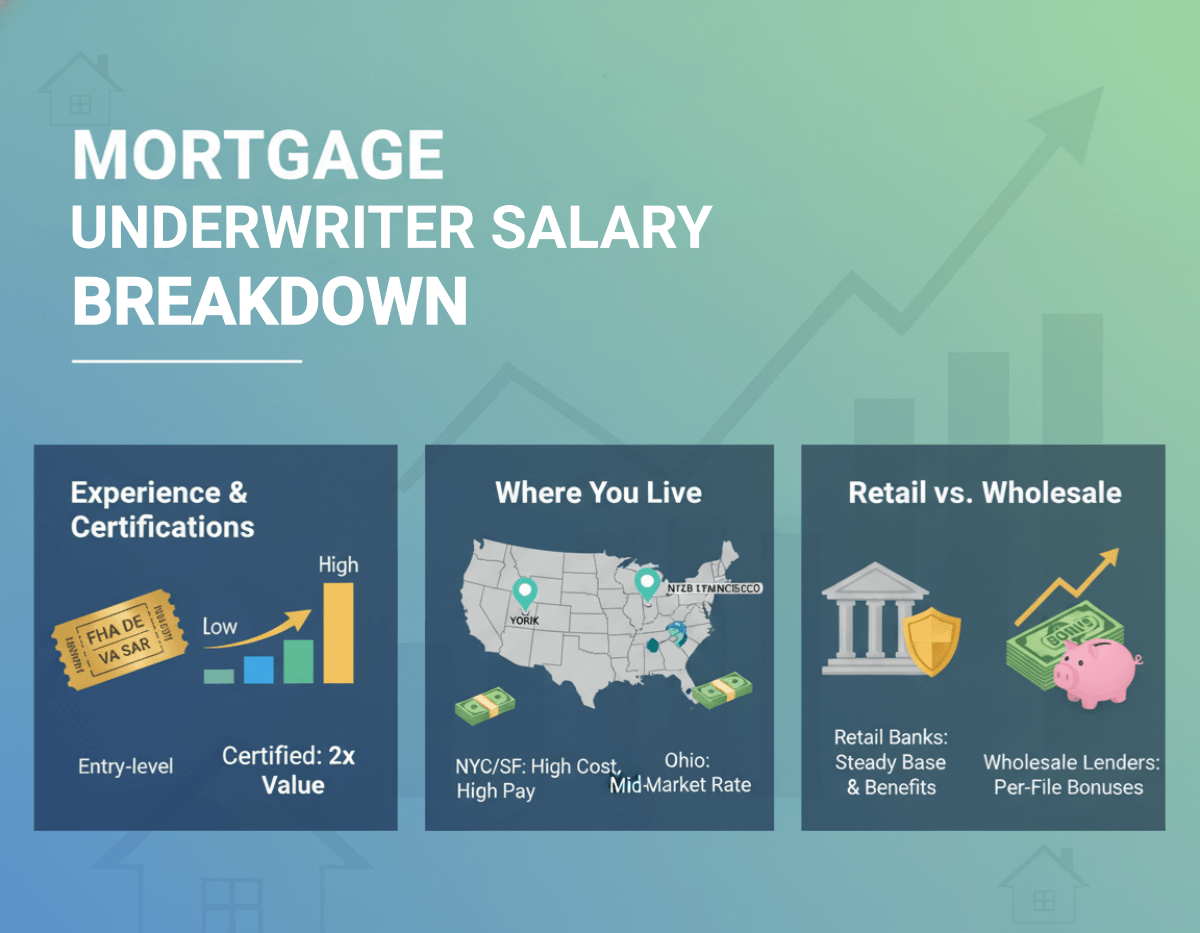

Mortgage Underwriter Salary Breakdown

A national average hides more than it reveals. Talking with hiring managers over the years, I've found your actual offer usually comes down to three things.

- Experience and government sign-off authority: This is the real lever. Entry-level hires start modestly, but once you pass the exams for FHA Direct Endorsement (DE) or VA Staff Appraisal Reviewer (SAR) authority, your market value jumps almost overnight.

- Where you're based: A shop in New York or the Bay Area pays more just to offset rent. A mid-market lender in Ohio or Kansas won't match that, but the cost of living gap often cancels out the difference anyway.

- Retail bank vs. wholesale lender: Large retail banks tend to offer steadier base pay and richer benefits. Independent wholesale shops often lean on per-file bonuses that spike hard during refinance booms.

Average Mortgage Underwriter Salary

Every job board uses a slightly different formula to calculate pay. Some rely entirely on self-reported employee surveys (which often include bonuses), while others scrape base salaries straight from active job postings. To give you a realistic picture, I've averaged out the latest 2026 data from the four biggest platforms. Expect a middle-ground baseline hovering right around $65,000 to $85,000.

Indeed

Let's look at Indeed. Based on thousands of recently aggregated job postings as of early 2026, their data shows an average base salary of around $79,637 a year for U.S. underwriters. What I find interesting about Indeed's numbers is the spread. The bottom 10%, mostly total beginners, sit closer to $53,902. Meanwhile, the top end stretches well past $117,659, especially in major metro markets. Since this data pulls directly from employer listings rather than employee memories, it's a highly accurate reflection of what companies are currently willing to pay a mid-level hire.

Salary.com

If you literally have zero experience, Salary.com is the best benchmark. They specifically track the "Mortgage Underwriter I" title. Right now, in 2026, they peg the median base pay at roughly $65,000. The typical range sits tight between $58,000 and $75,000. I always tell newcomers to look at this tier first so they don't get unrealistic expectations. The good news? Salary.com also shows that once you hit the Level III or IV tier a few years later, jumping into the $95,000 to $110,000 bracket is the standard progression.

Glassdoor

Over on Glassdoor, things look a little different. Because workers self-report their total take-home pay here, the average sits higher, pushing close to $95,000 annually. Of that total, about $75,000 represents the fixed base salary, while the remaining $20,000 comes from cash bonuses and extra compensation. I completely trust this breakdown. Anyone who has survived a busy mortgage season knows that those monthly production bonuses significantly pad your W-2. Glassdoor essentially reveals the "hidden" upside that standard job listings rarely advertise upfront.

ZipRecruiter

Finally, ZipRecruiter shows extreme real-time wage fluctuations. For 2026, they report an entry-level national average of about $62,000. However, their data shows a massive spread. The 25th percentile is scraping by at $41,000, while the 75th percentile is already hitting $72,000 for the exact same job title. To me, this proves that negotiating your starting offer is crucial. The huge variance means some lenders are trying to lowball new talent, while others are aggressively paying up for smart, analytical candidates. Don't settle for the bottom of that barrel.

Mortgage Underwriter Salary by Experience Level

Job boards rarely break this down cleanly, so here's the typical career ladder I've seen play out across lenders, retail banks, and credit unions.

- Entry-Level / Underwriter I: roughly $45,000 to $65,000. You're learning guidelines, shadowing senior staff, and working smaller or simpler files.

- Underwriter II: roughly $65,000 to $85,000. You're handling a full file load independently, often with DE or SAR authority in progress.

- Senior / Underwriter III: roughly $90,000 to $115,000. You carry complex files — jumbo, non-QM, or investment property loans — and often mentor junior staff.

- Chief or Lead Underwriter: often $115,000 and up, especially with management duties or specialized product oversight like commercial or SBA lending.

These bands shift with location and lender type, but the pattern holds everywhere: certifications and file complexity move you up faster than tenure alone.

What Top Lenders Actually Pay Underwriters

Company-level pay varies more than most people expect. At Rocket Mortgage, Glassdoor's reported range for underwriters runs from about $75,000 at the 25th percentile to over $120,000 at the 75th percentile, with averages commonly cited between $77,000 and $95,000 depending on title and location. At United Wholesale Mortgage (UWM), reported averages land closer to $67,000 to $91,000, with wide variation by role level and tenure. Smaller regional banks and credit unions typically sit below the big wholesale lenders on base pay but often make up ground with better work-life balance and lower file quotas. Always check a specific employer's current listings before comparing offers — self-reported data shifts month to month.

Highest-Paying States for Mortgage Underwriters

Location swings pay more than almost any other factor. Indeed's regional data shows underwriters in New York earning closer to $87,000 on average, well above the national figure. California, Texas, Florida, and Arizona also show up consistently among the higher-paying and higher-demand states, largely because of loan volume and cost-of-living adjustments. If you're early in your career and open to relocating, targeting one of these markets can add real money to your first offer.

How Does a Mortgage Underwriter Get Paid?

A common myth: people assume underwriters get a cut of every loan they approve. They don't, and structuring pay that way would be a serious compliance problem. Under Regulation Z, which implements the Dodd-Frank Act, underwriters are specifically excluded from the legal definition of a "loan originator" because they don't negotiate loan terms with borrowers. That distinction matters — it's exactly why their pay can't be tied to a loan's interest rate, size, or approval outcome. Doing so would blur the line and risk reclassifying them as loan originators, which triggers a whole separate set of licensing rules.

Instead, compensation comes from three legitimate sources.

- Base Salary: your guaranteed W-2 income and the bulk of your annual pay.

- Production or Quality Bonus: if your monthly quota is 40 files, your employer might pay a flat bonus for every file cleared beyond that, provided your accuracy stays high.

- Overtime Pay: when rates drop and refinance volume spikes, mandatory overtime is common and can noticeably boost a single paycheck.

For context on how this compares to the broader financial sector, the U.S. Bureau of Labor Statistics doesn't track "mortgage underwriter" as its own category, but its closest adjacent roles — financial examiners — carried a median annual wage of $90,400 in 2024, a category projected to grow much faster than average. That's a useful sanity check against the job-board figures above, even if it's not a perfect one-to-one match.

Loan Officer VS Underwriter Salary

A lot of folks debate whether to go into sales as a Loan Officer (LO) or stay behind the scenes as a Mortgage Underwriter. The money structures are night and day. LOs eat what they kill, and they hunt for borrowers and live off commissions. Underwriters get paid just for doing the math, whether the loan closes or not.

An LO might make $300,000 during a refinance boom and then struggle to pay rent when rates spike. An underwriter's income is much more insulated from those wild market swings.

Also Read: Mortgage Underwriter vs Loan Officer: Which Career Is Best?

Where Do Processors and Funders Fit In?

Two related roles get lumped into underwriter searches, so it's worth a quick distinction. Loan processors gather and organize paperwork before it reaches underwriting, and typically earn less than underwriters, often in the $40,000 to $60,000 range. Funders handle the final disbursement once a loan clears underwriting and closing, with pay that tends to land close to processors. Underwriters sit in the middle of that pipeline as the risk decision-makers, which is a big part of why their ceiling is higher.

Home Loan Underwriter or Officer: Which to Choose?

Choosing between these two paths shouldn't just be about who makes more on paper. It boils down to how your brain is wired.

- Become a Mortgage Underwriter if: You are naturally analytical, love diving into complex tax returns, and genuinely care about the tiny details. If the idea of a stable, predictable income lets you sleep at night, and you hate the thought of networking or managing angry clients, stay at the underwriting desk.

- Become a Loan Officer if: You have thick skin, serious hustle, and are highly extroverted. If you don't mind sacrificing your weekends to take calls from real estate agents, and you are perfectly fine with an unpredictable paycheck in exchange for uncapped earning potential, sales is where you belong.

Also Read:

- Best Mortgage Underwriter Training Online: Improve Your Expertise

- Best Mortgage Underwriter Certifications: Everything to Know Here

FAQs About Home Loan Underwriter Salary

Q1. Do mortgage underwriters make good money?

Yes. The median pay easily beats the national average. A mid-level underwriter typically earns around $75,000, while seasoned pros with specialized government credentials like DE or SAR regularly clear $100,000 or more a year when factoring in their volume bonuses.

Q2. Is being a mortgage underwriter stressful?

Yes, especially at the end of the month. While you don't have the stress of finding clients, you are strictly graded on your speed and accuracy. Trying to clear a heavy pipeline of loans before rate locks expire can definitely raise your blood pressure.

Q3. Do mortgage underwriters get a commission?

No. Federal regulations completely ban underwriters from earning commission based on loan amounts or interest rates. You are paid to assess risk objectively. However, lenders can and do reward underwriters with flat cash bonuses based on the sheer volume of files completed accurately.

Q4. Can mortgage underwriters work from home?

Yes. Remote work is massive in this industry right now. Most major lenders currently offer hybrid schedules, and many allow 100% remote underwriting. Honestly, skipping the daily commute is a huge financial perk that effectively increases your real take-home pay.

Q5. Is there a high demand for mortgage underwriters?

Yes, though it fluctuates. When interest rates drop, the surge in refinancing creates a desperate shortage of underwriting talent. But even during slower, higher-rate markets, experienced underwriters holding specialized FHA or VA sign-off authority remain incredibly hard for companies to replace.

Conclusion

Mortgage underwriting remains one of the better-kept secrets in finance. It offers a rare combination: solid, stable pay without the grind of commissioned sales. You get paid to analyze data, manage risk, and help people close on homes. If you learn the guidelines and pursue DE or SAR certification early, six figures is a realistic target within a few years, not a decade.

If this path sounds like a fit, don't just take it from me. Pull up Indeed or ZipRecruiter and search entry-level underwriting roles in your state. Look at what's actually being offered right now. The opportunity is there for anyone willing to put in the study time.

People Also Read

- Best CRM for Loan Officers: Which One Suits You Most?

- Best Mortgage Loan Officer Training: Which to Pick?

- Mortgage Loan Officer Salary: How Much Do Loan Officers Make?

- Best Mortgage Companies for New Loan Officers

- Best Mortgage Underwriter Software: AI & Guideline Verification