Written by

Eric

Share this article

.svg)

Subscribe to updates

I've spent years in the mortgage industry, and if there's one thing that constantly drains our time, it's manual underwriting. You know the drill: cross-checking hundreds of pages of investor guidelines, verifying complex borrower data, and praying you didn't miss a tiny overlay. It is exhausting and highly prone to human error.

But in 2026, AI-powered software is changing the game. Tools like Zeitro are now essential. Not only do they instantly verify guidelines with precise citations, but they also streamline the entire loan origination process. Plus, with a highly cost-effective freemium plan, finding the best mortgage underwriter software is no longer a luxury—it's a necessity for survival.

What to Consider to Choose a Top Mortgage Underwriter Software?

Before jumping into the software sea, remember that not every platform will fit your specific business model. Based on my experience, choosing the right tool comes down to evaluating a few core metrics:

- Guideline Coverage & Accuracy: Does the system support both QM and Non-QM loans? More importantly, can it provide exact source citations for its answers? You need to trust the data.

- Integration & Workflow: A top-tier tool must talk to your existing LOS or POS. Look for features like seamless FNM 3.4 data exports.

- Security & Compliance: We are handling sensitive financial data. Enterprise-grade security, specifically SOC 2 Type II certification, is non-negotiable.

- Cost-Effectiveness: Is there a trial or a freemium model? For mid-sized brokerages or individual LOs, you want a platform that proves its ROI before requiring a massive upfront investment.

6 Top-Rated Software for Mortgage Underwriter in 2026

There are dozens of tools on the market, but after testing them for real-world efficiency, features, and actual ROI, I've narrowed it down. Here are the 6 best software options tailored for different mortgage underwriters' needs, from guideline AI and auto-decisioning to document processing.

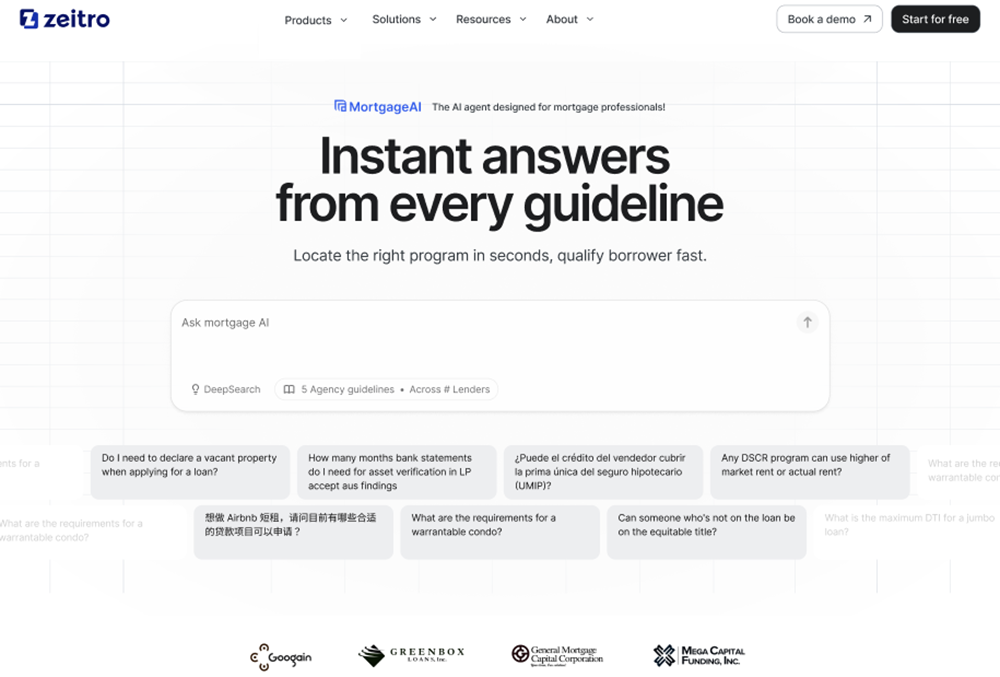

#1 Zeitro - Best for Guideline Verification and Automated Process

Why Choose: The ultimate mortgage AI agent that turns hours of manual guideline research into seconds with exact citations.

Zeitro is a neutral, AI-native mortgage technology company founded in 2018, with a team that includes leaders from Google and Apple alongside mortgage industry veterans. It directly attacks our biggest daily headache: the endless search through loan manuals. Zeitro operates with total neutrality and boasts SOC 2 Type II certification, ensuring top-tier data security. I recommend it because it literally cuts research time from 30 minutes to a few seconds.

Features:

- AI Guideline Verification: It instantly cross-checks over 100 investors and 300+ guidelines (covering Non-QM, DSCR, ITIN, Jumbo, etc.). You can ask vague questions and get highly accurate answers backed by direct citations. There's even an "Explain" function for deeper clarity.

- Automated Digital 1003 (POS): Borrowers can complete their application in 5 minutes. The AI accurately calculates DTI (85%+ accuracy), and you can seamlessly export the data in FNM 3.4 format.

- Competitive Pricing Engine: Get rapid quotes for both conventional and Non-QM products, complete with flexible overlay adjustments.

- High ROI: It saves professionals 7+ hours per loan file, speeds up pre-qualifications by 2.5x, and boosts closing rates by 30%.

- Pricing: Zeitro offers an incredibly generous Freemium model. The free Explorer plan includes 3 daily AI queries and 10 lifetime FNM exports, while the premium tier is just $8/month.

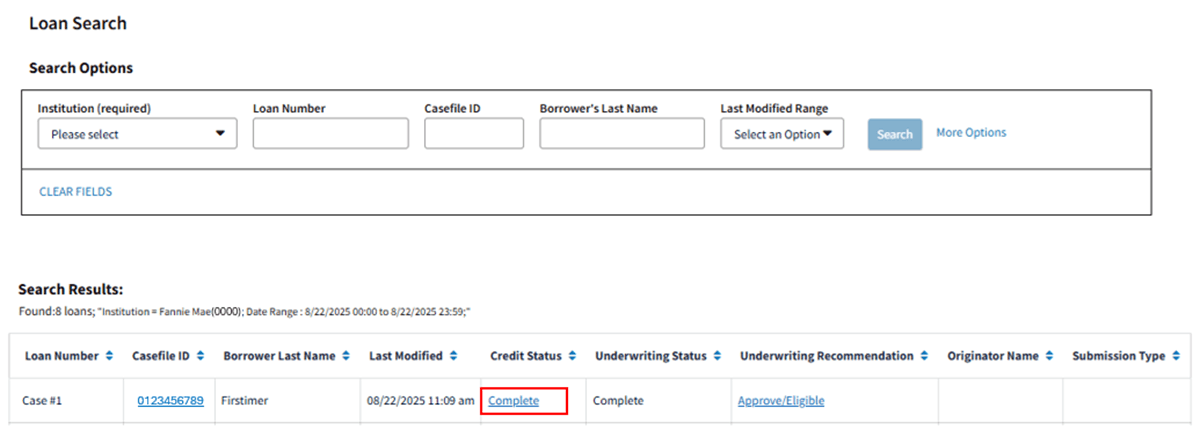

#2 Fannie Mae Desktop Underwriter (DU) - Best for Conventional Automated Underwriting

Why Choose: The absolute industry standard for conventional loan automated decision-making.

You simply cannot talk about mortgage processing without mentioning Fannie Mae's Desktop Underwriter (DU). It is the official automated underwriting system (AUS) for conventional loans and practically a mandatory tool in our industry. DU analyzes a borrower's credit risk, income, and assets to deliver a comprehensive risk assessment. I always rely on DU when handling standard Agency loans because an "Approve/Eligible" finding is the gold standard for moving a file forward.

Features:

- Comprehensive Risk Assessment: Evaluates credit history, debt-to-income ratios, and loan-to-value metrics instantly to determine conventional eligibility.

- Day 1 Certainty: This is a massive lifesaver. It provides rep and warrant relief by digitally validating borrower income, assets, and employment, drastically reducing buyback risks.

- Deep Integrations: DU integrates seamlessly with virtually every major Loan Origination System (LOS) on the market, making data transfer completely frictionless.

- Continuous Updates: Fannie Mae constantly updates its risk models to reflect current macroeconomic conditions and housing market trends, keeping your decisions compliant.

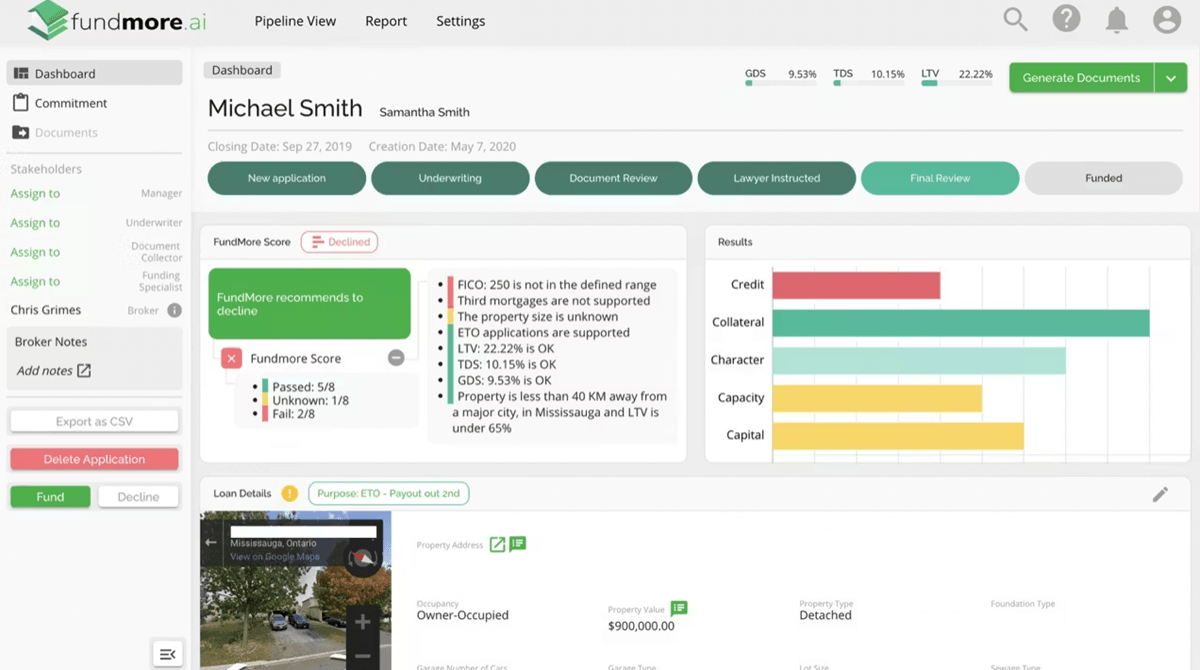

#3 FundMore.ai - Best for Automated Document Processing & Risk Assessment

Why Choose: Streamlines the underwriting process through AI-driven document recognition and automated conditions.

FundMore.ai is a cloud-based automated underwriting platform that leans heavily on machine learning to speed up the loan origination cycle. If your team is drowning in paperwork, this tool is a game-changer. It helps underwriters by automating the tedious task of reading and sorting through piles of borrower documents. It's highly effective at reducing the manual workload, which is why I consider it a top pick for risk assessment and document ingestion.

Features:

- Advanced OCR Technology: Automatically captures, classifies, and extracts critical data from uploaded borrower documents, eliminating manual data entry.

- Automated Stipulations: The system instantly generates loan conditions based on the extracted data and the lender's specific credit guidelines.

- FundMore Score: Provides an intelligent decision recommendation, giving underwriters a clear visual cue on whether to approve, decline, or manually review a file based on predefined risk rules.

- Secure POS Portal: Offers a modern, user-friendly portal for borrowers to easily upload their IDs and financial documents, keeping everyone on the same page.

#4 Freddie Mac Loan Product Advisor® (LPA) - Best for Streamlining Freddie Mac Loan Deliveries

Why Choose: The essential automated underwriting system for loans destined for Freddie Mac.

Just like DU is for Fannie Mae, Loan Product Advisor (LPA) is the proprietary AUS for Freddie Mac. If you plan on delivering loans to Freddie, using LPA is non-negotiable. It evaluates the risk of the loan against Freddie Mac's specific purchase standards. What I appreciate most about LPA is how it simplifies complex scenarios and gives underwriters a clear path to loan approval, running neck-and-neck with DU as an industry giant.

Features:

- Automated Collateral Evaluation (ACE): This feature can potentially waive the requirement for a traditional appraisal, saving borrowers time and hundreds of dollars.

- Asset and Income Modeler (AIM): Automates the assessment of a borrower's income and assets, making it much easier to handle self-employed borrowers or complex tax returns.

- Actionable Feedback: The system doesn't just give a yes or no. It provides incredibly detailed, easy-to-read feedback messages so you know exactly what conditions need to be cleared.

- Broad System Compatibility: LPA works flawlessly within major LOS platforms, ensuring that your origination workflow remains uninterrupted.

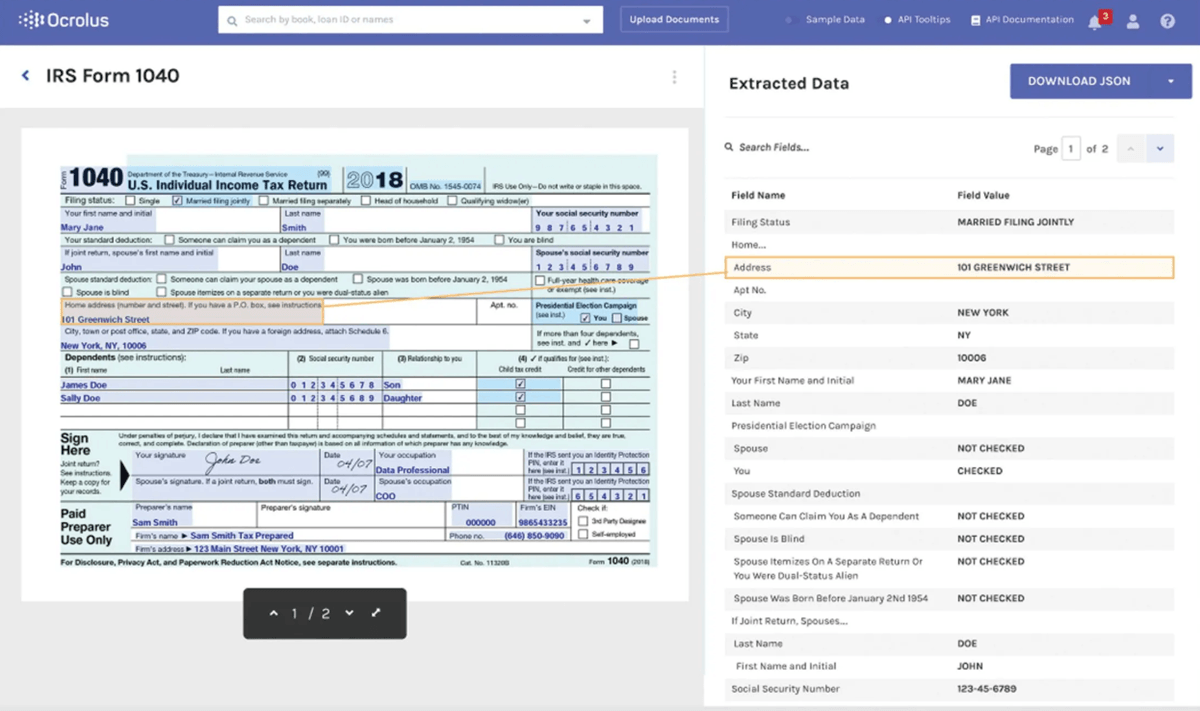

#5 Ocrolus - Best for Financial Document Automation and Income Calculation

Why Choose: Extremely accurate AI and human-in-the-loop document processing for tricky income calculations.

Calculating income for non-traditional borrowers can be a nightmare. Ocrolus solves this by serving as a premier document automation and analysis tool. It is my go-to recommendation when dealing with messy bank statements, W-2s, and complex tax returns. It is especially useful for self-employed individuals or those applying for Non-QM loans. By blending AI with human verification, Ocrolus ensures your income numbers are spot-on.

Features:

- Ultra-Accurate OCR: Captures data from almost any document type, regardless of quality, with over 99% accuracy.

- Automated Income Calculation: Instantly calculates wages, rental income, and self-employed earnings using various methods (YTD, multi-year averages). Ocrolus provides accurate income analysis for GSE loans but does not integrate directly with Fannie Mae's Income Calculator. It supports workflows compatible with major LOS systems like Encompass.

- Fraud Detection: Automatically flags tampered documents or suspicious inconsistencies, protecting lenders from fraudulent applications.

- Income Summary Dashboard: Provides underwriters with a clean, consolidated view of all borrower income sources, making it easy to toggle between applicants and adjust values on the fly.

#6 Floify - Best for Point-of-Sale (POS) and Borrower Communication

Why Choose: A highly customizable POS that keeps borrowers, LOs, and underwriters perfectly synced.

Floify is a robust digital mortgage portal that acts as the bridge between the borrower and the underwriting team. While it doesn't make credit decisions itself, it dramatically improves the environment in which we work. By simplifying document collection and centralizing communication, Floify eliminates the back-and-forth emails that usually slow down the clear-to-close process.

Features:

- Automated Document Requests: Sends automatic reminders to borrowers when stipulations are missing, ensuring underwriters get what they need without having to chase people down.

- Native eSignature Capabilities: Allows borrowers to legally sign disclosures and loan documents directly within their secure portal, speeding up compliance steps.

- Milestone Updates: Automatically texts or emails borrowers and real estate agents when a file moves from "In Underwriting" to "Clear to Close".

- Customizable Mobile App: Offers white-labeled mobile applications, giving your lending business a modern, branded feel while letting clients upload photos of documents straight from their phones.

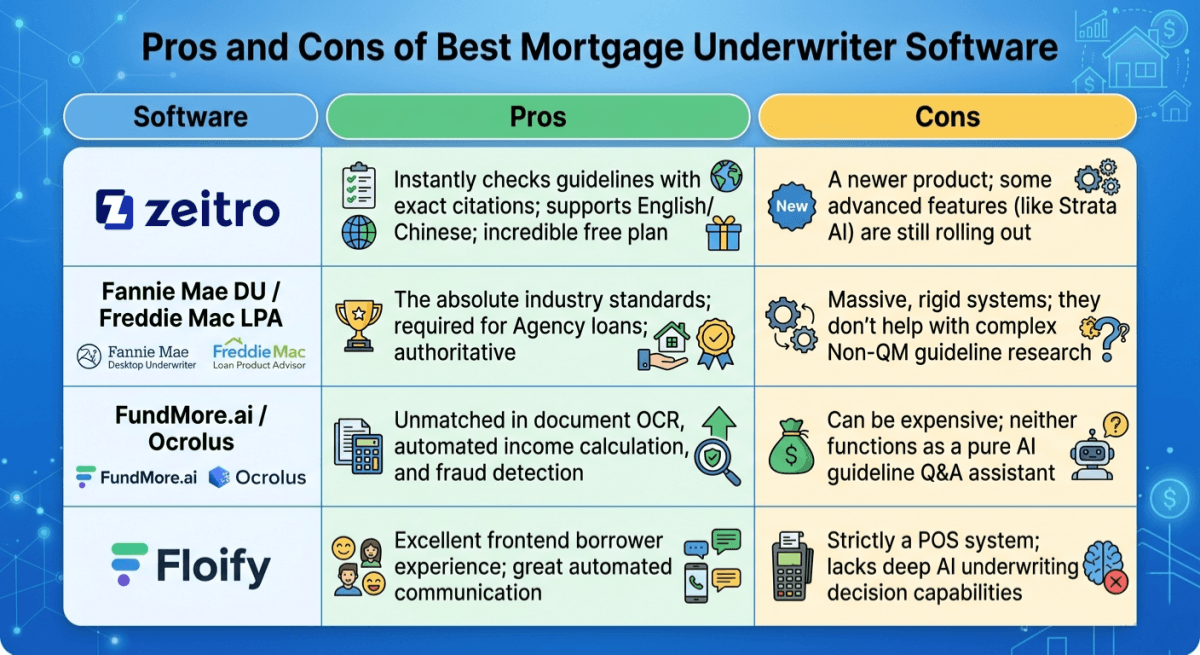

Pros and Cons of Best Mortgage Underwriter Software

One size absolutely does not fit all in this business. The most effective strategy I've found is to combine foundational systems, like DU or LPA, with powerful AI efficiency tools like Zeitro. To help you visualize, here is a breakdown of the pros and cons of these top solutions:

FAQs About Mortgage Underwriter Software

Q1. Do underwriters use Python?

Not usually. Most of us rely on ready-made automated systems like DU, LPA, or Zeitro rather than writing code ourselves. However, the backend engineers and data scientists who build these powerful AI mortgage platforms definitely use Python extensively to train their machine learning models.

Q2. What are the 4 types of underwriting?

The four main categories are mortgage, insurance, securities, and medical underwriting. In our specific field—mortgage—the process is further divided into manual underwriting (human analysis) and automated underwriting, using software to analyze risk based on algorithms.

Q3. What is the best CRM for mortgage?

Popular choices include Jungo, Total Expert, and BNTouch. However, the "best" mortgage CRM is one that seamlessly integrates with your other tools. An ideal setup allows your CRM to connect effortlessly with POS systems and pricing engines like Zeitro for a smooth workflow.

Q4. What is underwriting software?

It is a digital tool that helps lenders automatically analyze a borrower's credit, income, debt, and assets, like DTI and LTV. The software cross-checks this data against investor guidelines to quickly determine if a home loan should be approved or denied.

Q5. Are there any free mortgage underwriter software?

Yes! Zeitro offers a highly robust Freemium plan. Their Free Explorer Plan allows you to use the AI Guideline assistant 3 times a day and gives you 10 FNM exports. It is easily the most cost-effective entry point for industry professionals today.

Conclusion: Which One to Choose?

Wrapping things up, your choice heavily depends on your daily bottleneck.

- If you are strictly processing conventional Agency loans, Fannie Mae DU and Freddie Mac LPA are your unavoidable baselines.

- If messy tax returns and bank statements are slowing you down, Ocrolus is the way to go.

- If you—whether a Loan Officer, Broker, or Underwriter—are exhausted by manually hunting through confusing QM and Non-QM guidelines, Zeitro is unequivocally the top choice. It is entirely neutral, SOC 2 certified, and designed to save you over 7 hours per file while boosting your closing rates.

People Also Read

- Best CRM for Loan Officers: Which One Suits You Most?

- 6 Best Loan Origination Software for LOs/Brokers

- [Tips] Where to Buy Mortgage Leads? Warm Leads for LOs

- [Proven] How to Generate Mortgage Leads for Free? 6 Methods

- [NO Experience] How to Become a Mortgage Underwriter?