Written by

Eric

Share this article

.svg)

Subscribe to updates

I still remember staring at the massive pile of rules when I first decided to become a loan officer. It felt incredibly overwhelming back then. If you're currently trying to decode the exact requirements and qualifications to break into this industry, you're not alone. I put this guide together to share my own journey and outline the practical steps you need to take to get started.

Key Takeaways

- Education: A high school diploma or GED is the absolute baseline.

- Credentials: Mortgage loan originators must register with the NMLS. Those working for non-bank lenders are required to pass the SAFE MLO exam and obtain a state license.

- Background: Certain criminal convictions, especially those involving fraud or financial dishonesty, can disqualify you, along with serious issues in your financial history.

- Tools: Modern professionals rely heavily on AI and lead-generation platforms like Zeitro to scale.

What Does a Loan Officer Do?

Before jumping into the regulations, you should know what your day-to-day actually looks like. I spend my time acting as a financial puzzle-solver for home buyers. I don't just push paper. I connect real people with the capital they need. On any given Monday or Thursday, the loan officer's task list usually includes:

- Sitting down with clients to review or pull credit reports with proper authorization and talk through their budgets.

- Digging through stacks of tax forms, pay stubs, and bank statements to verify income.

- Comparing different mortgage programs to find the best fit for a buyer's unique financial situation.

- Holding hands with stressed-out clients from pre-approval all the way to closing day.

- Grabbing coffee with local real estate agents to keep my referral pipeline healthy.

Loan Officer Requirements

To write loans in the United States, you've got to meet some tight federal and state rules. Here's exactly what you'll have to check off.

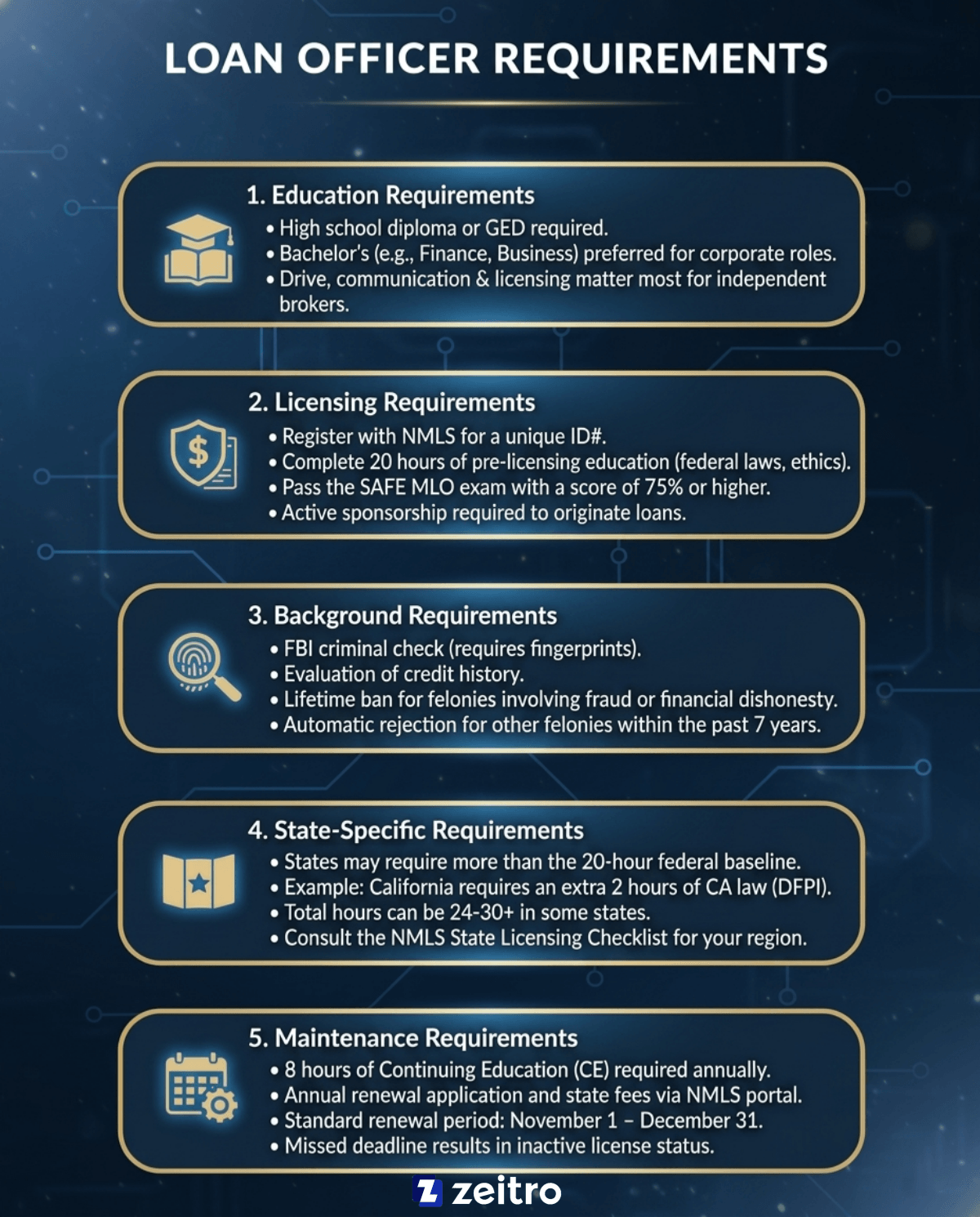

Education Requirements

You don't need an Ivy League degree to succeed here. The law only requires a high school diploma or a GED. I've worked alongside incredibly successful mortgage brokers who never set foot on a college campus.

That said, if you want a corporate job at a commercial bank, their HR departments usually look for a bachelor's degree in finance, business, or economics. But if you're planning to work as an independent broker, your drive, communication skills, and licensing matter way more than a piece of paper. Don't let the lack of a degree hold you back from applying.

Licensing Requirements

If you plan to deal with residential mortgages, you'll need a state-issued license under the SAFE Act. First, you register with the Nationwide Multistate Licensing System (NMLS) to get your ID. Then comes the coursework, 20 hours of pre-licensing classes covering federal laws and ethics.

After that, you have to face the national SAFE MLO exam. It's a tough test, and you need a 75% or higher to pass. Once you pass, you can't just go out and sell loans on your own. Your license must be associated with (or sponsored by) a licensed mortgage company before you can originate loans.

The following below breaks down these core licensing phases:

- Stage 1. Registration (Sign up on the NMLS portal): Generates your unique ID number

- Stage 2. Education (Complete 20 hours of PE): Covers federal lending law & ethics

- Stage 3. Testing (Pass the SAFE MLO exam): Score a 75% or higher to pass

- Stage 4. Sponsorship (Get hired by an active broker): Officially activates your loan officer license

Background Requirements

We handle people's life savings, so the state doesn't take background checks lightly. You'll have to submit your fingerprints for an FBI criminal check and authorize an evaluation of your credit history.

Some things are instant dealbreakers. For example, a felony involving fraud, money laundering, or financial dishonesty typically results in a lifetime ban, while other felonies may disqualify you if they occurred within the past seven years.

Any other felony within the past seven years is also an automatic rejection. They want to make sure you have the personal integrity and financial responsibility to handle millions of dollars in client funds.

State-Specific Requirements

Don't forget that states have their own quirks. While the federal baseline is 20 hours of education, some states demand more. If you're in California seeking a license under the Department of Financial Protection and Innovation (DFPI), you have to take an extra 2 hours of California-specific mortgage law.

Other states might require 24 or even 30 hours total. Before you spend a single dollar on test prep or classes, always pull up the NMLS State Licensing Checklist for your specific region. It will save you from expensive mistakes and wasted study hours.

Maintenance Requirements

Getting your NMLS license is one thing, but keeping it is another. Every single year, you must take 8 hours of Continuing Education (CE) to stay sharp on updated lending regulations. You also have to submit a renewal application and pay your state fees through the NMLS portal.

The standard renewal period runs from November 1 to December 31, though many states allow a late renewal period into the following year. If you forget or miss this deadline, your license instantly goes inactive, and you won't be allowed to write loans until you pay a fine and go through a painful reinstatement process.

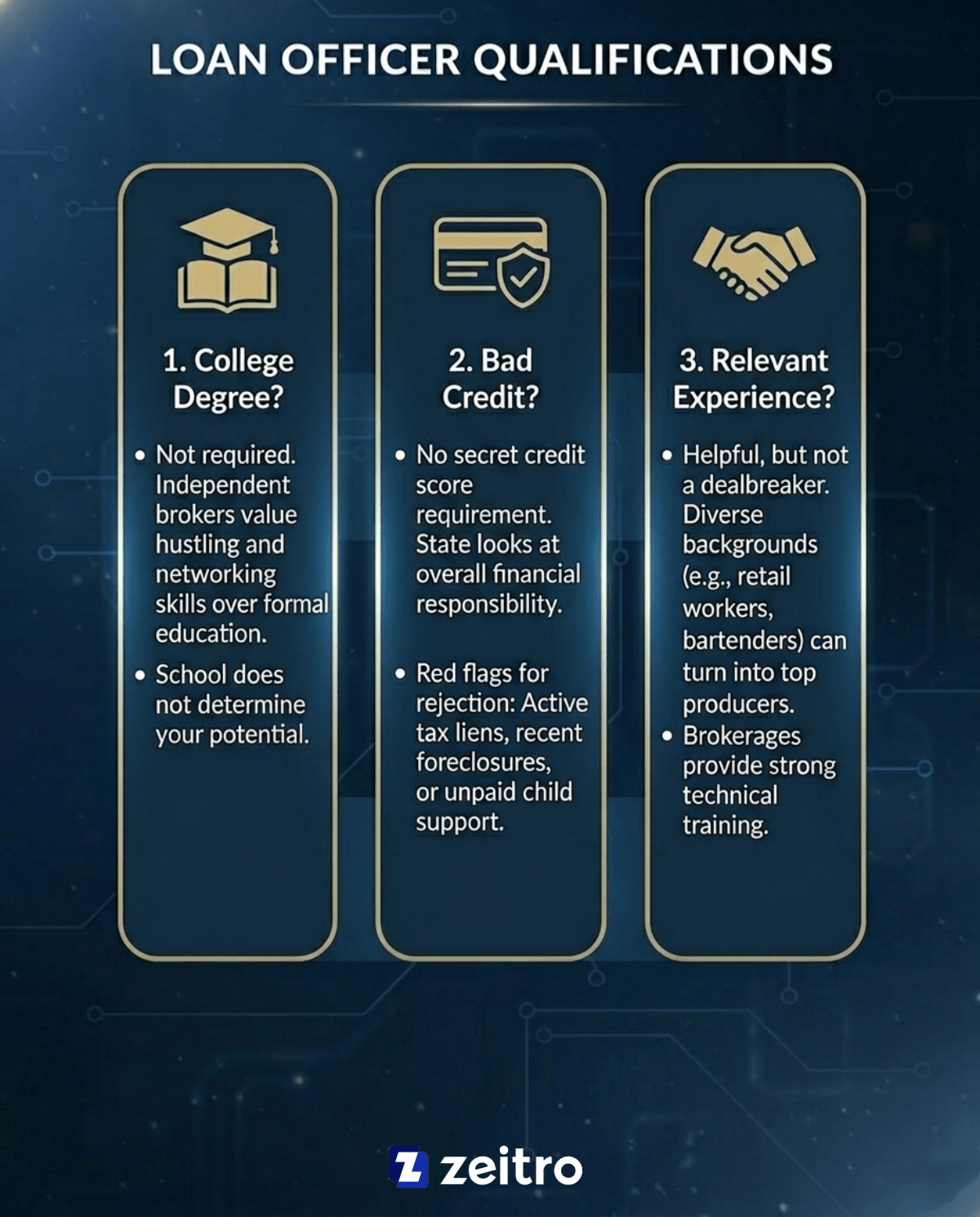

Loan Officer Qualifications

Let's tackle the questions I hear most from prospective LOs trying to see if they fit the bill.

- First, do you need a college degree? No. Most independent shops care about your hustle and networking skills, not where you went to school.

- Second, what if you have bad credit? There isn't a secret credit score you have to hit. The state looks at your overall financial responsibility. If you have active tax liens, a recent foreclosure, or unpaid child support, that's what triggers a rejection.

- Third, do you need sales or real estate experience? Honestly, it helps, but it's not a dealbreaker. I've seen bartenders, teachers, and retail workers turn into top-producing loan officers. Most brokerages offer strong training programs to teach you the technical stuff. If you genuinely like talking to people, are highly organized, and can handle a fast-paced environment, you've got the basic qualifications to make it in this industry.

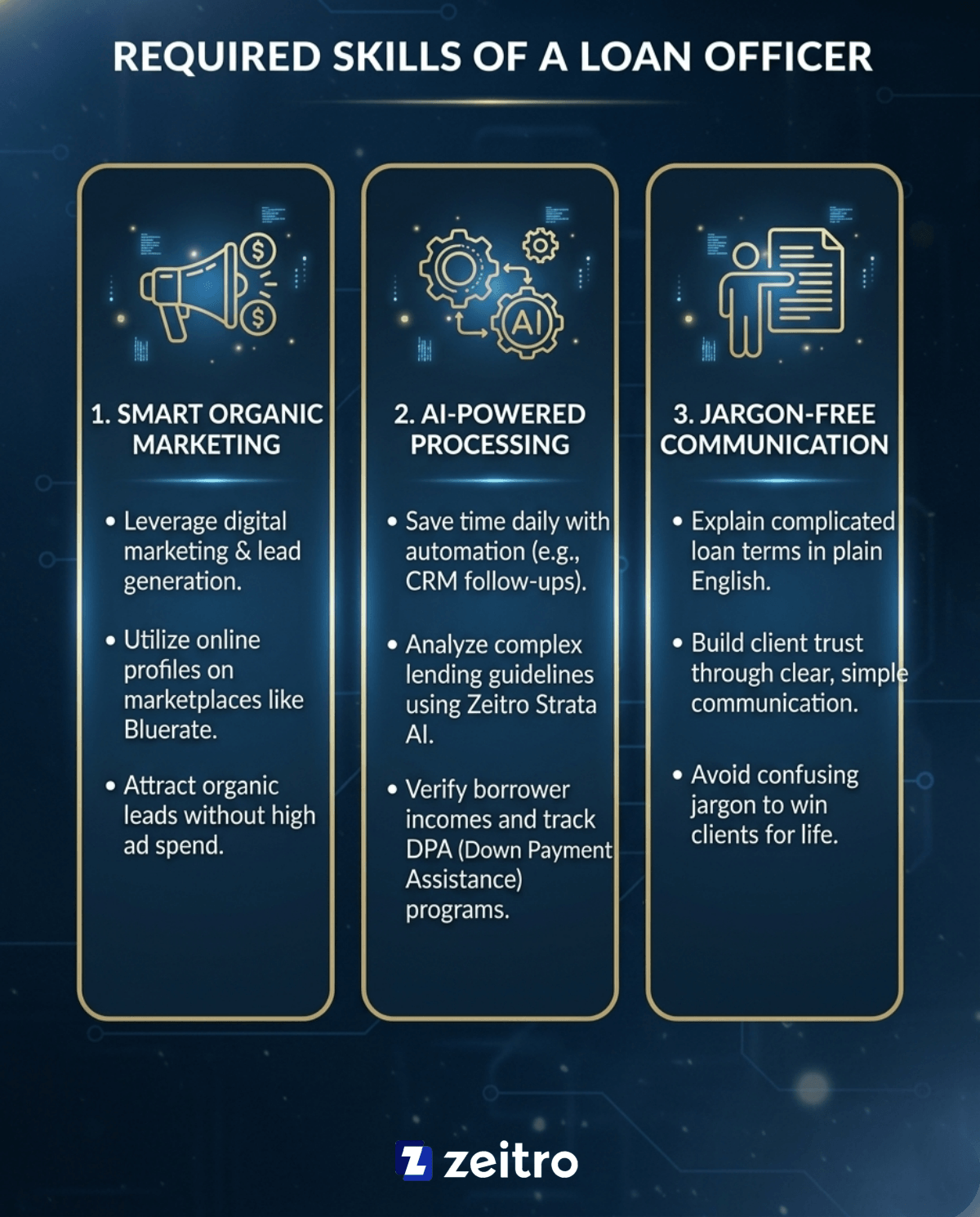

Required Skills of a Loan Officer

The classic skills, like crunching numbers and calculating debt-to-income ratios, are still vital. But today's market requires you to work smarter, not harder. Here are the tools and skills I rely on daily:

- Smart Organic Marketing: While cold calling is less effective than it once was, many loan officers still use it alongside digital marketing strategies. I suggest setting up a free profile on Bluerate, a modern mortgage marketplace. It lets you display your live rates on a custom page, drawing in organic homebuyer leads without spending a fortune on ads.

- AI-Powered Processing: I save hours every week using Zeitro. It handles everything from automating my CRM follow-ups to analyzing complex guidelines via Zeitro Strata AI, verifying borrower incomes, and tracking down payment assistance (DPA) programs instantly.

- Clear, Jargon-Free Communication: If you can explain complicated loan terms in plain English, you'll win clients for life.

FAQs About Requirements to Be a Loan Officer

Q1. Is it hard to make it as a loan officer?

Getting the license is actually the easy part. The real test is surviving your first twelve months. Since this is a commission-heavy business, you don't get paid unless you close loans. Finding clients is tough, and many rookies throw in the towel because they run out of money before their pipeline fills up. But if you're willing to put in the hours, network with local realtors, and embrace modern digital lead tools, the payoff is incredibly worth it.

Q2. What disqualifies you from being a loan officer?

Certain issues on your record will trigger an automatic 'no' from state regulators. Any felony involving money laundering, check fraud, tax evasion, or embezzlement means a permanent lifetime ban. Non-financial felonies will disqualify you if they happened within the last seven years. Additionally, severe financial red flags, like unresolved tax liens, unpaid child support, or active foreclosures, will cause regulators to deny your license because they show a lack of financial responsibility and character.

Q3. Do I need to be licensed to work as a bank loan officer?

No, you don't. If you get hired by a federally insured bank like Chase or a local credit union, you only have to register with the NMLS. You get to skip the 20 hours of pre-licensing classes and the SAFE exam entirely. However, if you want the freedom of working as an independent mortgage broker or for a non-bank lender, you absolutely must go through the full state licensing process.

Q4. How much does it cost to get an MLO license?

Expect to spend roughly $400 to $1,000+, depending on your state and education provider. Your biggest upfront cost will be the 20-hour pre-licensing education, which usually runs between $150 and $400. The national SAFE exam costs $110 per attempt. You'll also pay about $36 for fingerprinting, $15 for your credit report check, and varying state-specific application fees. It's a small investment considering the career's earning potential, but you should budget for it.

Also Read: NMLS License Cost Breakdown: Know Your Every Penny

Q5. Can you work as a part-time loan officer?

It's legally possible, but I rarely see part-timers succeed. Real estate moves incredibly fast. Homebuyers want pre-approval letters on Saturday afternoons, and listing agents will call you on Tuesday morning with urgent questions. If you can only return calls after your day job ends at 5 PM, clients and realtors will quickly take their business to a full-time professional who is always available. It's best to treat this as a full-time commitment.

Wrap Up

Starting a career as a loan officer takes some real work, but the freedom and income potential make the journey incredibly rewarding. Focus first on getting your education out of the way, passing the SAFE exam, and finding a supportive company to sponsor your license.

Once you're in, don't just rely on old-school tactics. Setting up a free profile on Bluerate to capture organic leads and using Zeitro to handle your daily paperwork will give you a massive head start over traditional loan officers. If you've got the work ethic, the right tools are waiting to help you build a highly successful business.

People Also Read

- Best NMLS Test Prep Course: Which to Choose from?

- Best Mortgage Loan Officer Training: Which to Pick?

- Is There a Loan Officer University for Newcomers?

- 11 Best Loan Officer Schools for Newbies: Online & Local

- Mortgage Underwriter vs Loan Officer: Which Career Is Best?

- Realtor vs Loan Officer: What's the Difference?