Written by

Eric

Share this article

.svg)

Subscribe to updates

If you are like most renters I talk to, saving for a down payment feels like trying to catch a moving train. You have the monthly income to handle a mortgage, but watching home prices climb makes saving that initial lump sum feel almost impossible.

That is where Down Payment Assistance (DPA) comes in. Over the years, I have seen these programs turn renting families into proud homeowners overnight. Let us look at how they work.

Key Takeaways

- Lowers Cash Barriers: These programs slash the upfront cash needed for down payments and closing costs.

- Not Just for Beginners: Many DPA programs are not limited to first-time buyers, and some also allow repeat buyers depending on program rules.

- Varied Structures: Assistance comes as interest-free grants, forgivable loans, or low-interest seconds.

- Local Requirements: Qualification hinges on your location, household income, and completing a homebuyer class.

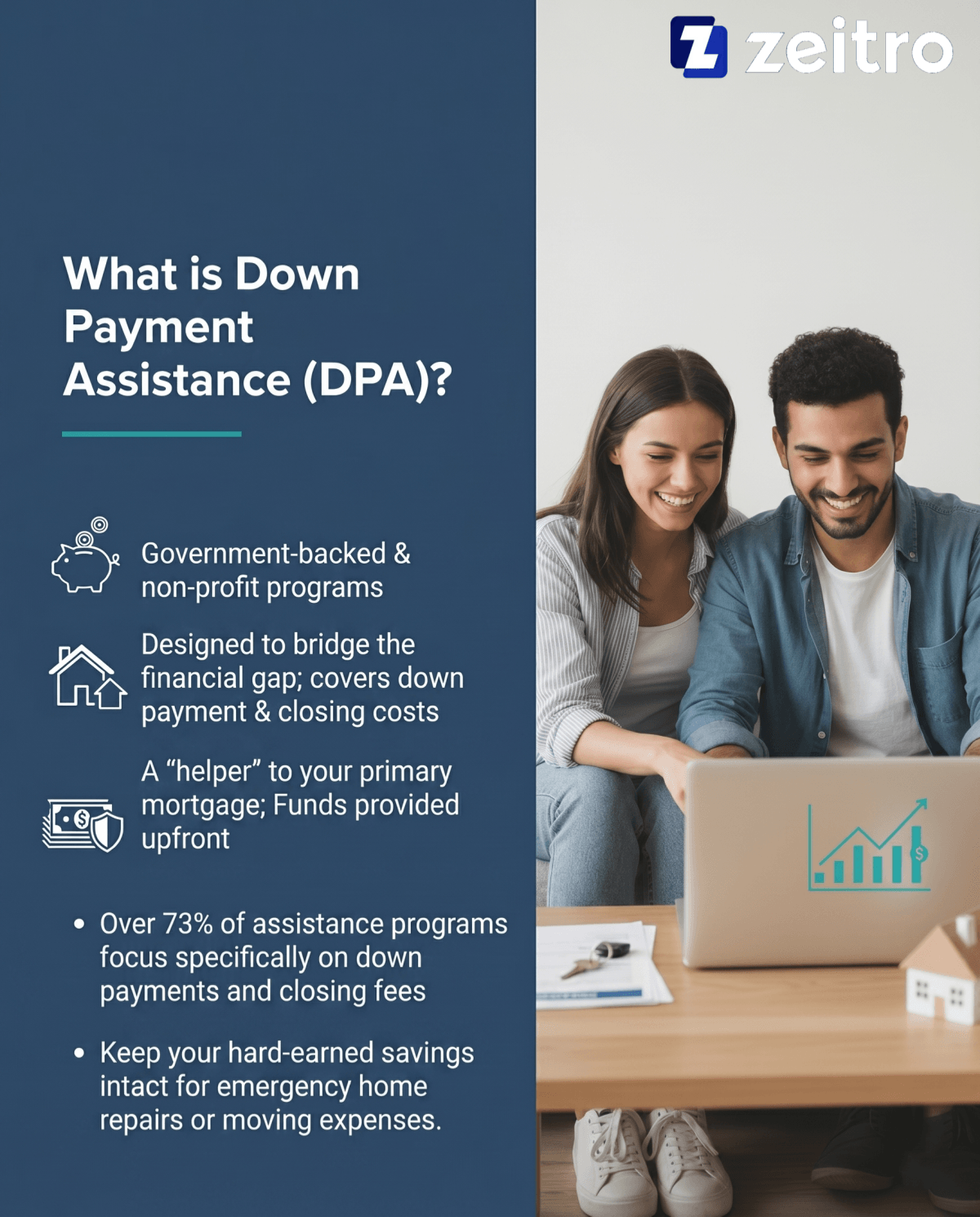

What is Down Payment Assistance (DPA)?

When you purchase a home, lenders typically expect you to put some skin in the game. Down Payment Assistance (DPA) consists of government-backed and non-profit programs designed to bridge this financial gap. During my time in the industry, I have seen these programs provide anywhere from a few thousand dollars to tens of thousands of dollars, depending on the program and location, to cover your down payment or closing costs.

Essentially, DPA acts as a helper to your primary mortgage. Instead of waiting years to save tens of thousands of dollars, a DPA program provides those funds upfront. Over 73% of these assistance programs in the U.S. focus specifically on down payments and closing fees. By utilizing them, you can keep your hard-earned savings intact for emergency home repairs or moving expenses.

Also Try: Zeitro Down Payment Assistance Program Finder

Also Read:

- Best First-Time Home Buyer Programs: Get the Right Choice

- 10 First-Time Home Buyer Tips: What to Know in 2026

- Zeitro Mortgage Employment Income Calculator for Loan Pros

- Zeitro Mortgage Affordability Calculator Free and Online

- Zeitro Mortgage Payment Calculator with Interest & Taxes

- California Down Payment Assistance: All Programs & Application

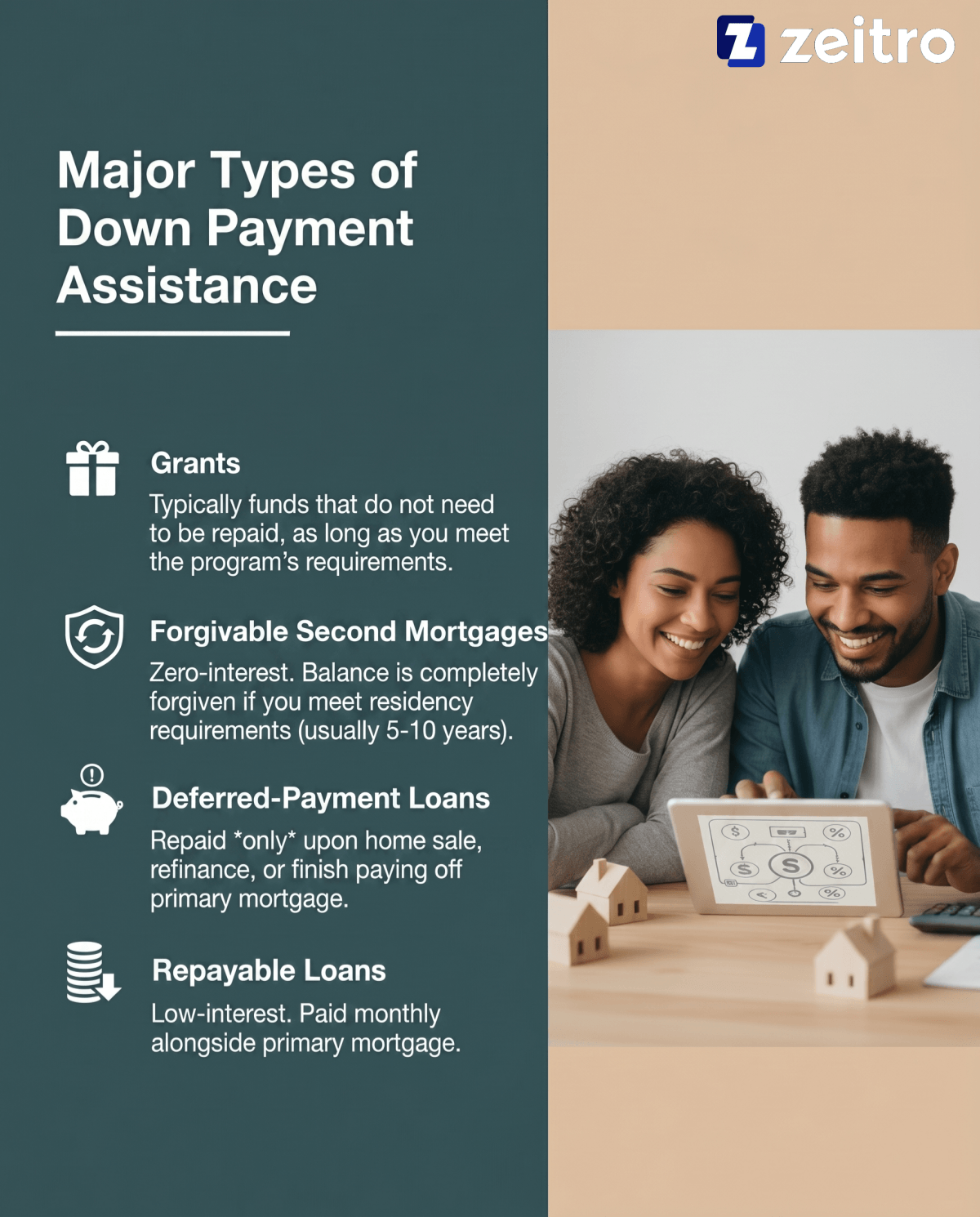

Major Types of Down Payment Assistance

From my experience, buyers often think DPA is always a "gift." In reality, these programs are structured in a few distinct ways, and understanding the differences is crucial for your long-term budget:

- Grants: These are typically funds that do not need to be repaid, as long as you meet the program's requirements.

- Forgivable Second Mortgages: These are often low- or zero-interest second loans that may be forgiven over time if you meet residency requirements. If you stay in the home for a specific period, usually five to ten years, the debt is completely wiped out. If you sell or refinance early, you pay back a pro-rated portion.

- Deferred-Payment Loans: You do not make monthly payments on this second mortgage. Instead, the balance is repaid only when you sell the home, refinance, or finish paying off your main mortgage.

- Repayable Loans: These are low-interest second loans that you pay back alongside your primary mortgage each month.

Eligibility Requirements for Down Payment Assistance

Every state and city handles DPA differently, but most programs look at a few common baseline factors.

- First is your buyer status. While many programs target first-time buyers, the legal definition of "first-time" is surprisingly generous: it simply means you have not owned a primary residence in the past three years.

- Second is income limits. Most programs require your gross household income to fall below a certain threshold, like 80% to 120% of your Area Median Income (AMI) in CA, as defined by HUD.

- Lastly, expect a homebuyer education requirement. You will need to complete a quick, HUD-approved course. In my view, this is actually a massive benefit. It teaches you how to budget for home repairs, understand mortgage terms, and avoid costly mistakes. You also need to meet your main lender's minimum credit score requirements, which vary by loan type but are often around 580 or higher for FHA loans and higher for conventional loans.

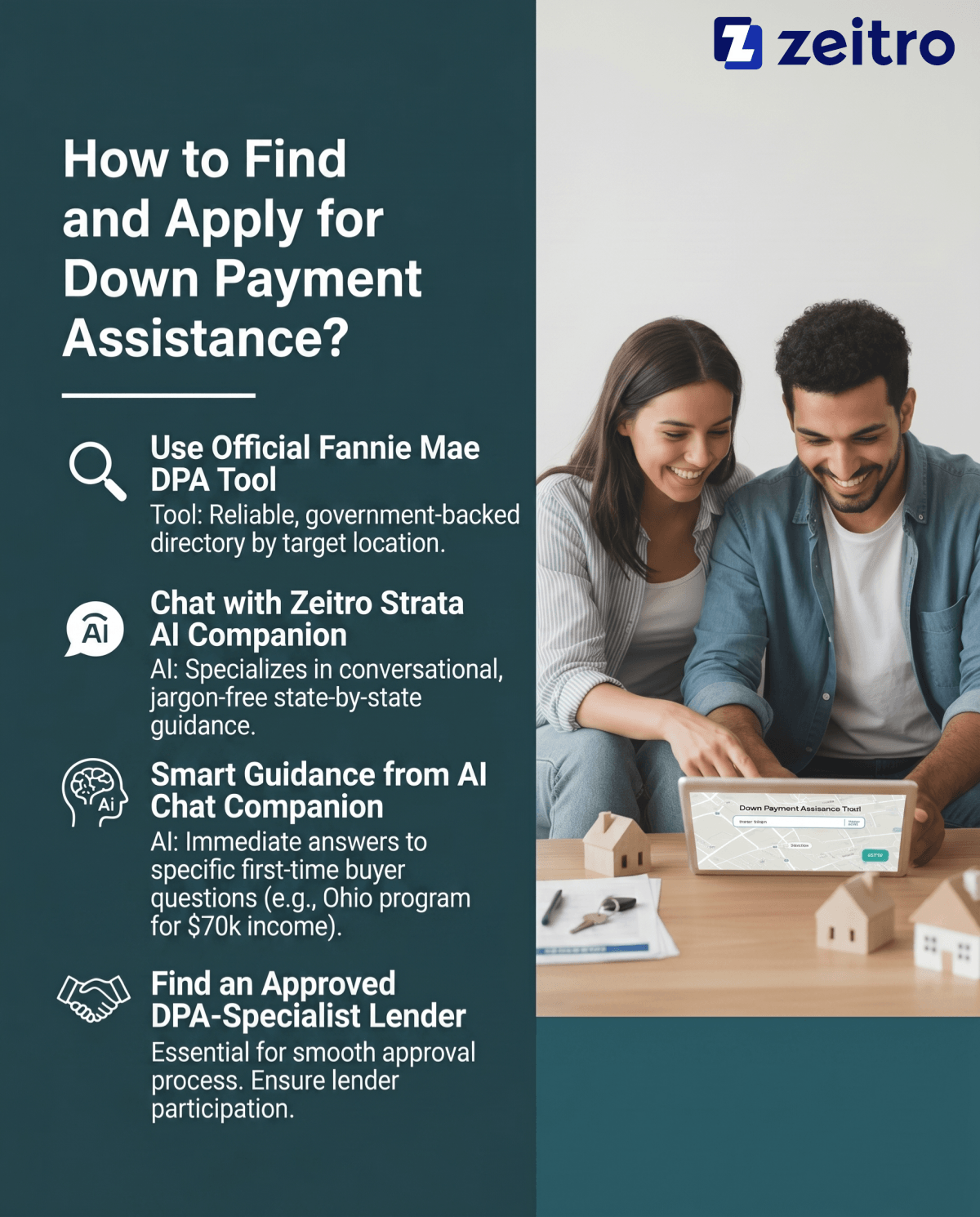

How to Find and Apply for Down Payment Assistance?

Finding these programs can feel overwhelming because they are highly localized. When my clients ask where to start, I point them toward two highly effective tools.

- First, use the official Fannie Mae Down Payment Assistance Tool. This is a reliable, government-backed directory where you can type in your target neighborhood to see exact, current programs available in your county.

- Second, to cut through the jargon, try chatting with Zeitro Strata AI. This smart AI chat companion specializes in state-by-state mortgage assistance. You can literally ask, "What DPA programs are available for a first-time buyer in Ohio making $70,000?" and get immediate, conversational guidance.

- Once you identify a program, your next move is to find a mortgage lender approved to work with that specific DPA. Not every bank participates, so working with a DPA-specialist loan officer is essential to getting your application approved smoothly.

FAQs About Down Payment Assistance

Q1. What does down payment assistance help with?

DPA programs primarily cover your upfront down payment and closing costs, which include lender fees, escrow, and title insurance. Some advanced local programs even allow you to use these funds to buy down your mortgage interest rate, lowering your monthly payments.

Q2. What are the risks of down payment assistance?

The biggest trade-off I caution buyers about is that DPA programs can sometimes come with a slightly higher interest rate on your primary mortgage. Additionally, if you have a forgivable loan and need to move or sell the home unexpectedly before your residency term ends, you may have to pay that money back immediately.

Q3. Do you have to pay back down payment assistance?

It completely depends on the DPA structure. True grants never have to be repaid. Forgivable loans are wiped clean after you live in the home for a set number of years. However, repayable and deferred second mortgages must be paid back eventually, usually when you sell or refinance.

Q4. Can you use DPA with conventional loans or FHA loans?

Yes, absolutely. Most state housing agencies build their DPA programs to "stack" seamlessly with conventional, FHA, VA, or USDA loans. Your loan officer will help you choose the primary mortgage that pairs best with your local DPA.

Q5. How long does the DPA approval process take?

In my experience, DPA can extend the mortgage timeline, sometimes by several weeks, depending on the program and processing requirements. Because local housing authorities must manually verify your income and tax records, I always advise my clients to write a 45-to-60-day closing period into their initial home purchase contract.

Conclusion

Buying a home is one of the most rewarding financial milestones you will ever achieve, but saving the upfront cash should not keep you locked in a cycle of renting. Down payment assistance exists to make homeownership a reality today, not a decade from now.

Whether you qualify for a non-repayable grant or a forgivable loan, taking the time to explore your local options is incredibly worthwhile. I encourage you to use the Fannie Mae tool and chat with Zeitro Strata AI to start mapping out your path. You might be much closer to those keys than you think.

People Also Read

- Guide: Loan Origination Points Explained in Mortgage

- Ultimate Guide: How to Get a 1099 Form Online?

- Fixed vs Adjustable Rate Mortgage: Full Differences to Compare

- Must-Read Tips for Paying Off Mortgage Early