Written by

Eric

Share this article

.svg)

Subscribe to updates

Every tax season, I help real estate investors maximize write-offs to lower their tax bills. But when those same clients apply for a new mortgage, they panic when they see a rental loss on paper. From my experience as a loan officer, I can tell you that underwriters generally factor a net rental loss into your debt-to-income ratio by reducing qualifying income or, in some cases, treating the shortfall as a liability, depending on the loan program and documentation. Here is exactly how they handle it.

Key Takeaways

- Rental losses are treated as monthly liabilities, increasing your debt-to-income (DTI) ratio.

- Underwriters use Schedule E but will add back non-cash depreciation to offset the loss.

- Newer landlords face stricter rules regarding lease agreements and management history.

How Do Underwriters Treat Rental Losses?

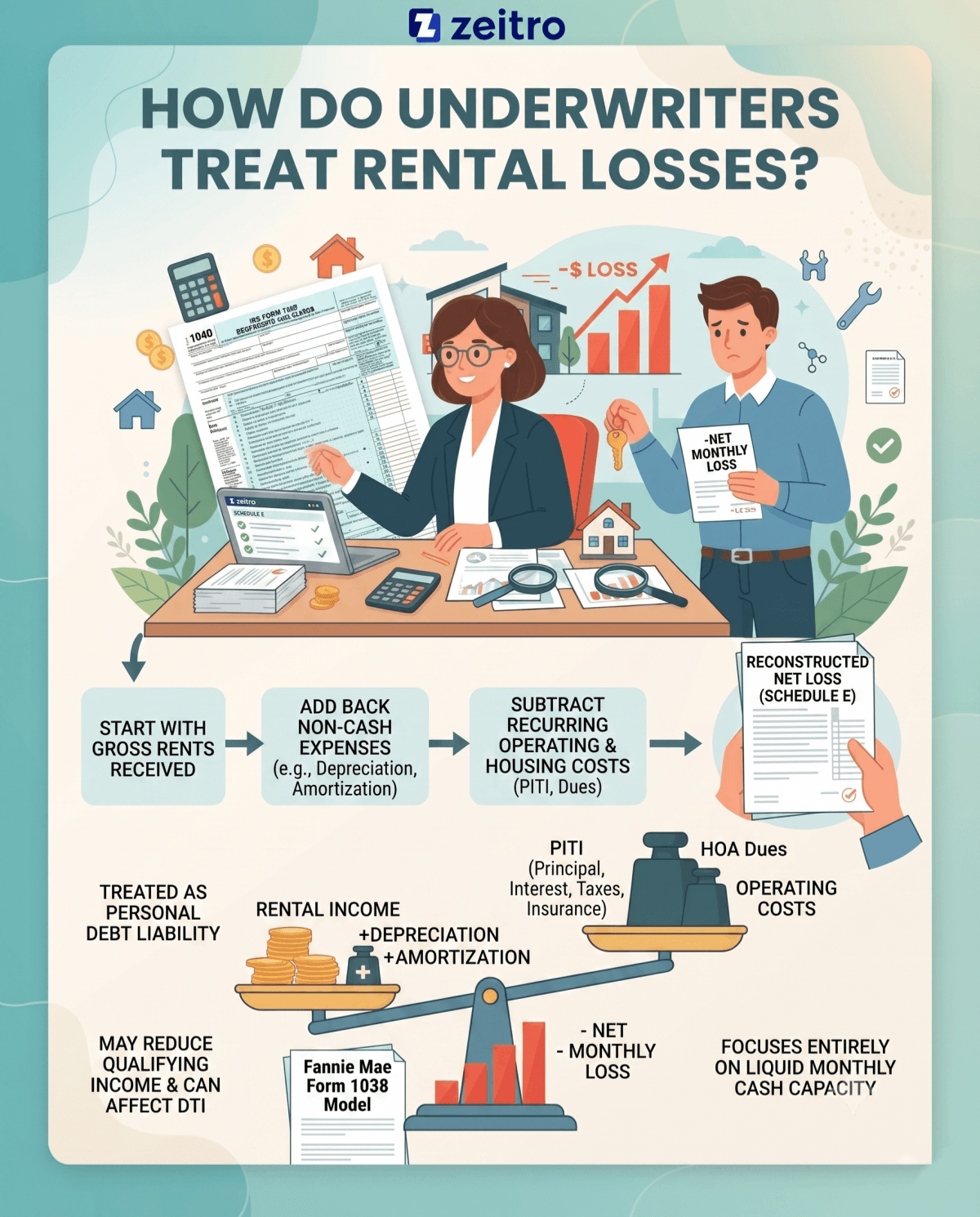

When you apply for a home loan, underwriters do not just look at your W-2 or business profits. They dissect IRS Form 1040 Schedule E to evaluate your real estate cash flow. If your properties operate in the red, that net monthly loss is treated as a personal debt liability.

To determine this, I use a standardized calculation modeled after Fannie Mae Form 1038:

I start with gross rents received, add back non-cash expenses such as depreciation, and then subtract the property's recurring operating and housing costs, including principal, interest, taxes, insurance, and association dues, as applicable.

If the final result is negative, the shortfall may reduce your qualifying income and can affect your DTI, depending on the lender's underwriting rules. This calculation differs significantly from IRS net income because it focuses entirely on your liquid monthly cash capacity to repay a new loan.

What Will Be Affected by Rental Losses on a Mortgage?

Having a rental loss on your application triggers several critical adjustments during the underwriting process.

- First, your Debt-to-Income (DTI) ratio increases. Because the net loss acts as a recurring monthly debt, it directly eats into your borrowing capacity, meaning you qualify for a much smaller loan on your next purchase.

- Second, it impacts your liquid reserve requirements. When I review files with rental losses, reserve requirements vary by loan program and borrower profile, and lenders may require additional reserves for borrowers with rental losses.

- Finally, severe losses can push you into a higher-risk tier in automated underwriting systems, which may require a larger down payment or a higher credit score to secure approval.

Exceptions, Special Rules, and Portfolio Rules to Know

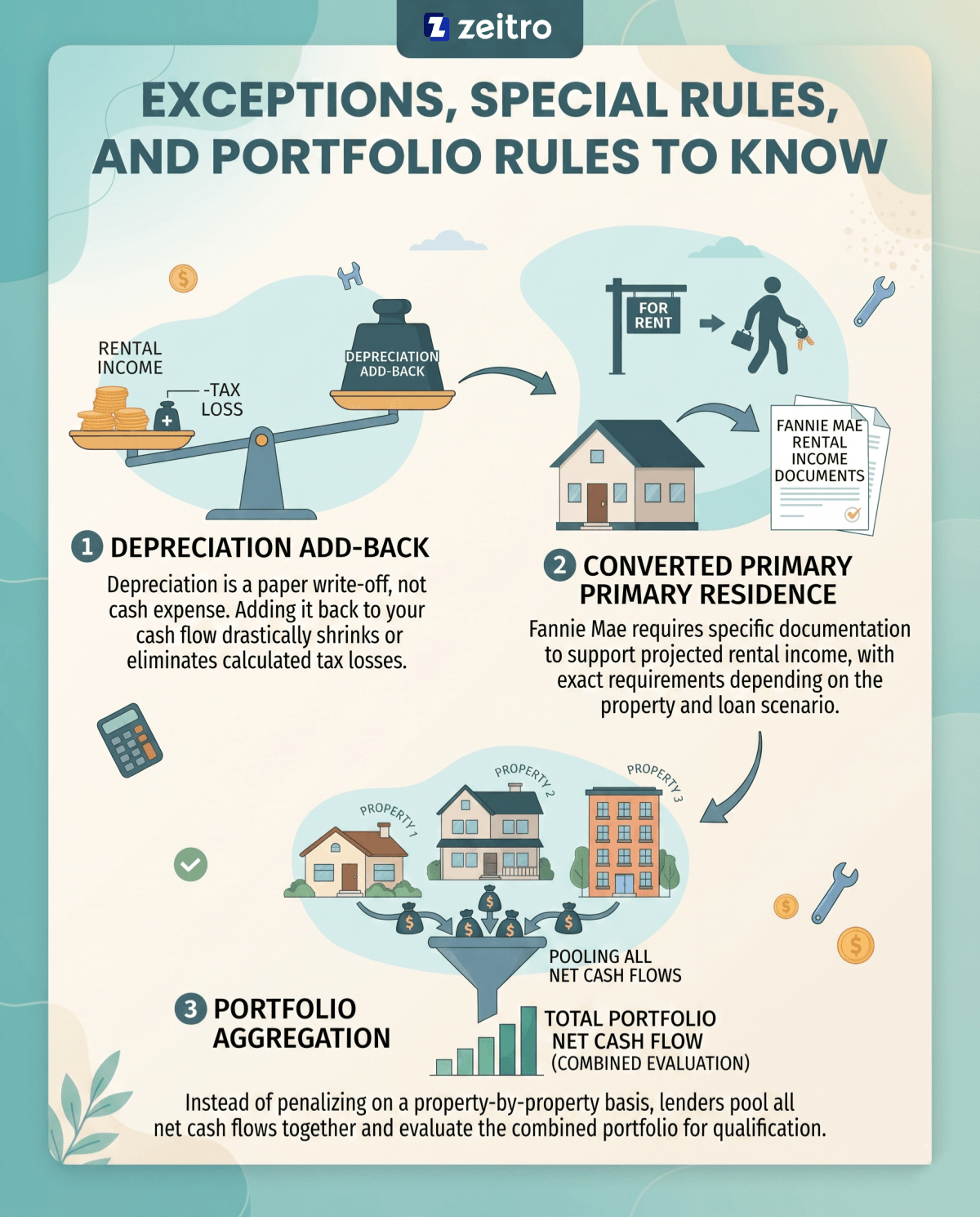

Underwriting is not entirely rigid. Several guidelines help offset tax-declared losses. First, the depreciation add-back is your best friend. Because depreciation is a paper write-off, not a cash expense, I always add it back to your cash flow, which drastically shrinks or eliminates the calculated loss.

For a primary residence converted to a rental, Fannie Mae requires specific documentation to support projected rental income, and the exact requirements depend on the property and the loan scenario.

Finally, under portfolio aggregation rules, we do not just penalize you property-by-property. If you own multiple properties, we pool the net cash flows together. When a borrower owns multiple rental properties, lenders typically evaluate the combined net cash flow across the portfolio rather than isolating each property in the same way.

How Underwriters Handle "Other" Housing Obligations (Avoiding Double Counting)

A common point of confusion for my clients is how we handle the monthly PITIA of a losing rental. When I calculate your net rental cash flow on Schedule E, the property's mortgage interest, taxes, and insurance are already factored into the calculation.

The property's housing payment is usually reflected in the rental cash flow analysis so it is not counted twice, rather than being ignored entirely. This prevents double-counting. However, the mortgage payment on your primary residence will always stand alone as your primary housing liability.

FAQs About Rental Losses

Q1. How do underwriters verify rental income?

We rely heavily on tax documentation. Specifically, I look at your most recent year's IRS Schedule E. If the property was recently acquired and does not appear on your last tax return, we will require a fully executed lease agreement paired with Form 1007 or 1025 appraisal rent schedules to verify current market rates.

Q2. What are the common red flags for underwriters?

The biggest red flags are sudden drops in rental income from one year to the next without a clear explanation, large unitemized "other expenses" on Schedule E, and properties that show 100% vacancy. These issues suggest structural problems, poor management, or undocumented rental losses that require deeper investigation.

Q3. What should you not do during underwriting?

Do not file amended tax returns to artificially boost your income without consulting your loan officer first. Also, do not let existing lease agreements expire or go month-to-month right before closing, as we need active, documented agreements to prove stable ongoing tenant occupancy.

Q4. Can a current lease agreement override a rental loss shown on tax returns?

Generally, underwriters must stick to tax returns. However, under Fannie Mae rules, if you acquired the property after your last tax filing, or if the property was out of service for renovations, we can use a current lease. In my experience, you must also provide proof of the lease taking effect, such as consecutive bank statements showing rent deposits or copies of the security deposit check.

Q5. Does a rental loss on taxes mean my mortgage application will be denied?

Absolutely not. Many of my most successful real estate investor clients show paper losses due to high depreciation. As long as your W-2 or primary self-employment income can comfortably support your total DTI, even with the rental liability factored in, your application can still easily be approved.

Conclusion

Navigating rental losses during a mortgage application can feel overwhelming, but understanding how underwriters calculate your DTI is the key to preparation. By leveraging depreciation add-backs and portfolio aggregation, many paper losses can be minimized.

I always advise reviewing your Schedule E with a knowledgeable mortgage professional before submitting your application. Please note that underwriting guidelines frequently update, so work closely with a licensed loan officer and your CPA to analyze your specific scenario for your next investment purchase.

People Also Read

- How Do Loan Officers Calculate Rental Income from Schedule E?

- Can Rental Income Offset a Mortgage? Lender Rules & Requirements

- How Much Rental Income Can Be Used for Qualification?

- Zeitro DSCR & Rental Income Calculator for Mortgage