Written by

Eric

Share this article

.svg)

Subscribe to updates

When I first started as a loan officer, opening a client's tax return and staring at Schedule E felt incredibly overwhelming. Trying to manually calculate the qualifying cash flow without making mistakes is a common hurdle for beginners. Fortunately, you do not have to guess. I routinely use the Zeitro Rental Income Calculator to quickly analyze these figures and verify calculations before submitting files to underwriting.

Key Takeaways

- Underwriting cash flow differs from IRS taxable income because non-cash expenses are added back.

- Fannie Mae uses Forms 1037 and 1038 for certain rental income calculations, while Freddie Mac follows its own rental income worksheet and documentation requirements.

- Calculating 'Months in Service' should be based on the number of months the property was actually rented during the year, using the Schedule E days-rented information as supporting data.

- Automated tools help eliminate manual calculation errors.

What is Schedule E on a Mortgage?

IRS Form 1040 Schedule E is the tax document where real estate investors report their rental income, expenses, and depreciation. For tax purposes, CPA firms aggressively write off expenses to lower the borrower's taxable income.

However, mortgage underwriters do not just look at the bottom line. Our job is to evaluate the property's actual cash flow. We analyze Schedule E to identify stable historical income. By adding back non-cash expenses, like depreciation, and certain items already counted in the debt-to-income ratio, we reconstruct a realistic monthly income.

This process ensures the borrower can safely qualify for a new mortgage without jeopardizing their financial stability.

Rental Income Guidelines to Learn

To analyze rental income correctly, you must align with agency guidelines. Fannie Mae Selling Guide B3-3.1-08 relies on Forms 1037 and 1038 to document individual rental cash flow. Meanwhile, Freddie Mac Selling Guide Section 5306.1 utilizes Form 92. These standards require checking the property's history, identifying whether it is the subject property or a non-subject investment, and assessing the borrower's property management experience.

If a borrower lacks a one-year history of managing rental properties, guidelines limit how much positive cash flow we can use to qualify them. Knowing these nuances is what separates a knowledgeable loan officer from someone who constantly gets files kicked back by underwriting.

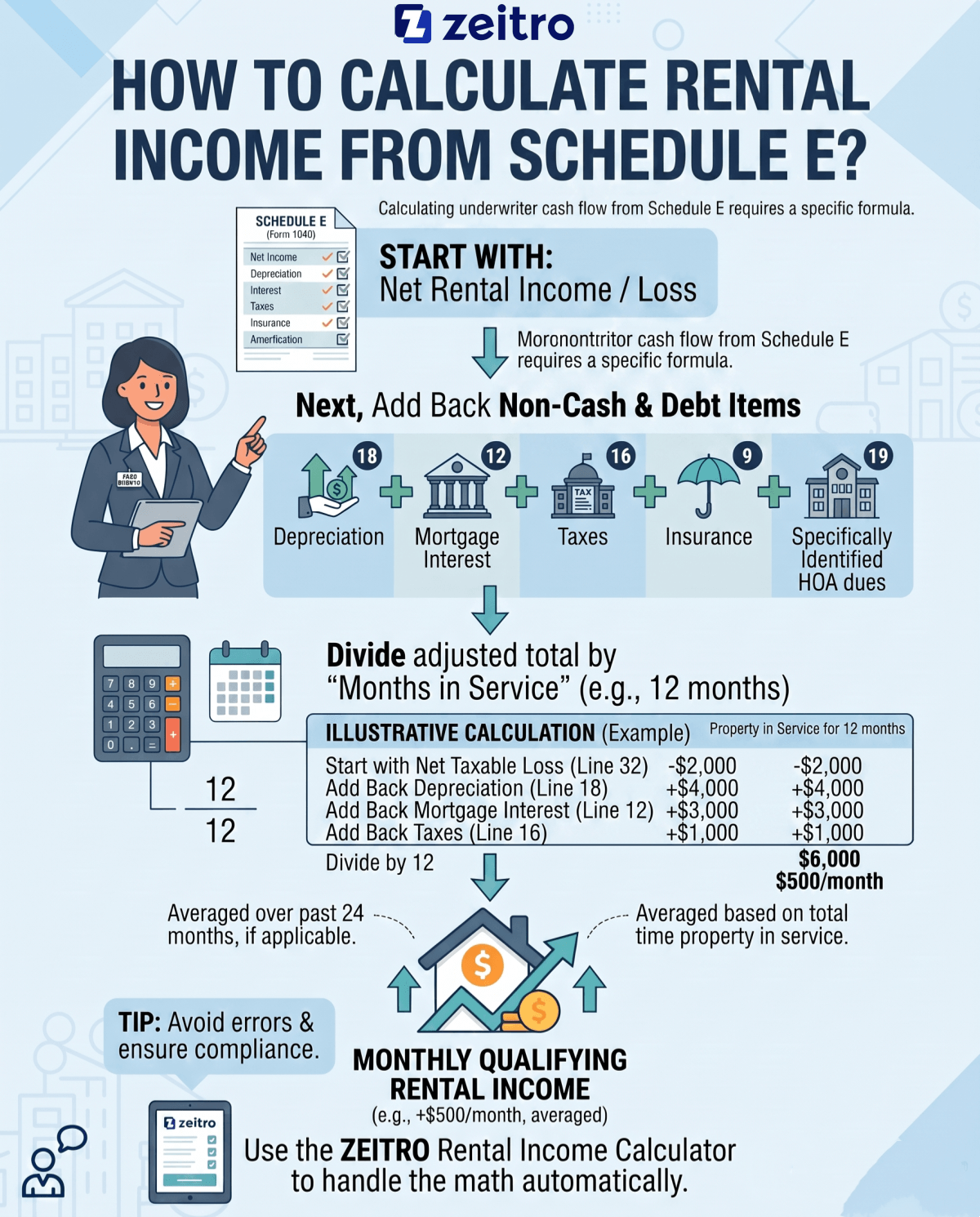

How to Calculate Rental Income from Schedule E?

Calculating underwriter cash flow from Schedule E requires a specific formula.

- Start with the net rental income or loss reported on Schedule E for the relevant tax year, using the final total lines on that year's form.

- Next, add back non-cash and debt-related expenses. These include Depreciation (Line 18), Mortgage Interest (Line 12), Taxes (Line 16), Insurance (Line 9), and specifically identified HOA dues (Line 19).

- Divide this adjusted total by the "Months in Service."

For example, if a property shows a net taxable loss of -$2,000 but has $4,000 in depreciation, $3,000 in mortgage interest, and $1,000 in taxes over 12 months, your adjusted annual cash flow is $6,000. Dividing this by 12 gives you $500 of monthly qualifying rental income before subtracting the monthly PITIA.

Tip: To avoid manual errors and ensure compliance, use the Zeitro Rental Income Calculator to handle the math automatically.

FAQs About Schedule E Calculation

Q1. Can I use a lease agreement instead of Schedule E to qualify?

In some cases, a signed lease may be used when tax-return rental history is unavailable, such as for a recently acquired or converted property, but eligibility depends on the specific loan program and supporting documentation requirements. You must also document the security deposit or first month's rent check.

Q2. What expenses on Schedule E can be added back by underwriters?

Underwriters add back non-cash expenses like depreciation and depletion. We also add back mortgage interest, property taxes, homeowner's insurance, and HOA dues if they are already included in the monthly housing liabilities used for the borrower's debt-to-income ratio, avoiding double-counting.

Q3. How do "Months in Service" affect the qualifying income calculation?

You must divide the adjusted income by the actual months the property was active. Locate the "Fair Rental Days" on Schedule E and divide by 30. If a property was active for only 6 months, dividing by 12 would artificially cut the borrower's qualifying income in half.

Q4. Does a passive loss limitation on tax returns lower my borrower's qualifying income?

Passive loss limitations are tax rules, but they can still affect the figures shown on the tax return. Underwriters then apply agency guidelines to determine what rental income, if any, can be counted for qualification.

Q5. What is the difference between Fannie Mae and Freddie Mac rental income worksheets?

Fannie Mae and Freddie Mac both provide their own rental income worksheets and documentation rules, and the exact form or worksheet depends on the transaction and property type. While the math is similar, their specific documentation rules and treatment of management history can vary slightly.

Final Word

Learning to calculate rental income from Schedule E is a rite of passage for every loan officer. It requires balancing strict agency guidelines with the unique realities of a borrower's tax returns.

While you should understand the underlying formulas and add-back logic, manual math leaves room for mistakes that can stall a loan in underwriting. Utilizing the Zeitro Rental Income Calculator streamlines your workflow, ensures policy compliance, and keeps your focus where it belongs—helping your clients close on their homes.

People Also Read

- How to Calculate Rental Income? Loan Officer's Guide

- How to Calculate Qualifying Income as a Loan Officer?

- How Do Underwriters Calculate Schedule C Income?

- How Do I Calculate Income from an S Corp?

- Can I Use Current Year Income Instead of Tax Return Income?