Written by

Eric

Share this article

.svg)

Subscribe to updates

Getting a mortgage when you own an S Corp can feel like navigating a maze. Unlike regular W-2 employees with simple payslips, our tax returns as business owners require a much closer look. I have spent years helping self-employed clients qualify for home loans. Today, I will show you how underwriters combine your personal and business income to calculate your true qualifying monthly cash flow.

Key Takeaways

- Self-employed threshold: In most conventional mortgage programs, owning 25% or more of an S Corp generally causes lenders to treat you as self-employed and apply self-employed underwriting guidelines, although individual lenders may have slightly different thresholds.

- The formula: Lenders combine your W-2 wages with your adjusted share of S Corp net income.

- Paperwork needed: Prepare two years of personal and business federal tax returns, including Schedule K-1.

- Depreciation add-back: Underwriters add back non-cash business deductions to boost your qualifying cash flow.

What is an S Corporation?

An S Corporation is a unique business structure that passes corporate income, losses, and deductions directly to its owners' personal tax returns. Unlike a standard C Corporation, which faces double taxation at both the corporate and individual levels, an S Corp avoids this. Meanwhile, a standard LLC provides similar liability protection but defaults to simpler partnership or sole proprietorship taxation.

In my experience, what sets the S Corp apart is how it splits your compensation. You must pay yourself a "reasonable" W-2 salary, and any remaining profit flows through to your Schedule K-1. This distinction is exactly what makes calculating mortgage income so unique.

What is S Corp Income for a Mortgage?

When you apply for a home loan, S Corp income isn't just your total business revenue. Lenders look at it differently than normal personal income. They want to know how much cash you can actually pull from your company without hurting its daily operations.

Because of this, underwriters don't just look at your gross earnings. They evaluate a mix of your personal W-2 wage and your share of the business's net cash flow. They adjust this net income by adding back non-cash expenses like depreciation. This gives them a clear picture of your actual qualifying cash flow, ensuring you can comfortably afford your monthly mortgage payments.

Can My S Corp Pay My Mortgage?

Directly paying your personal home loan from an S Corp business account is highly discouraged. Doing so creates a serious tax and legal problem known as commingling funds, which can weaken your corporate liability protection and greatly increase your risk of IRS scrutiny or audit.

Instead, I always advise clients to pay themselves first through an official W-2 payroll or a formal shareholder distribution. Once those funds land safely in your personal bank account, you can pay your mortgage from there.

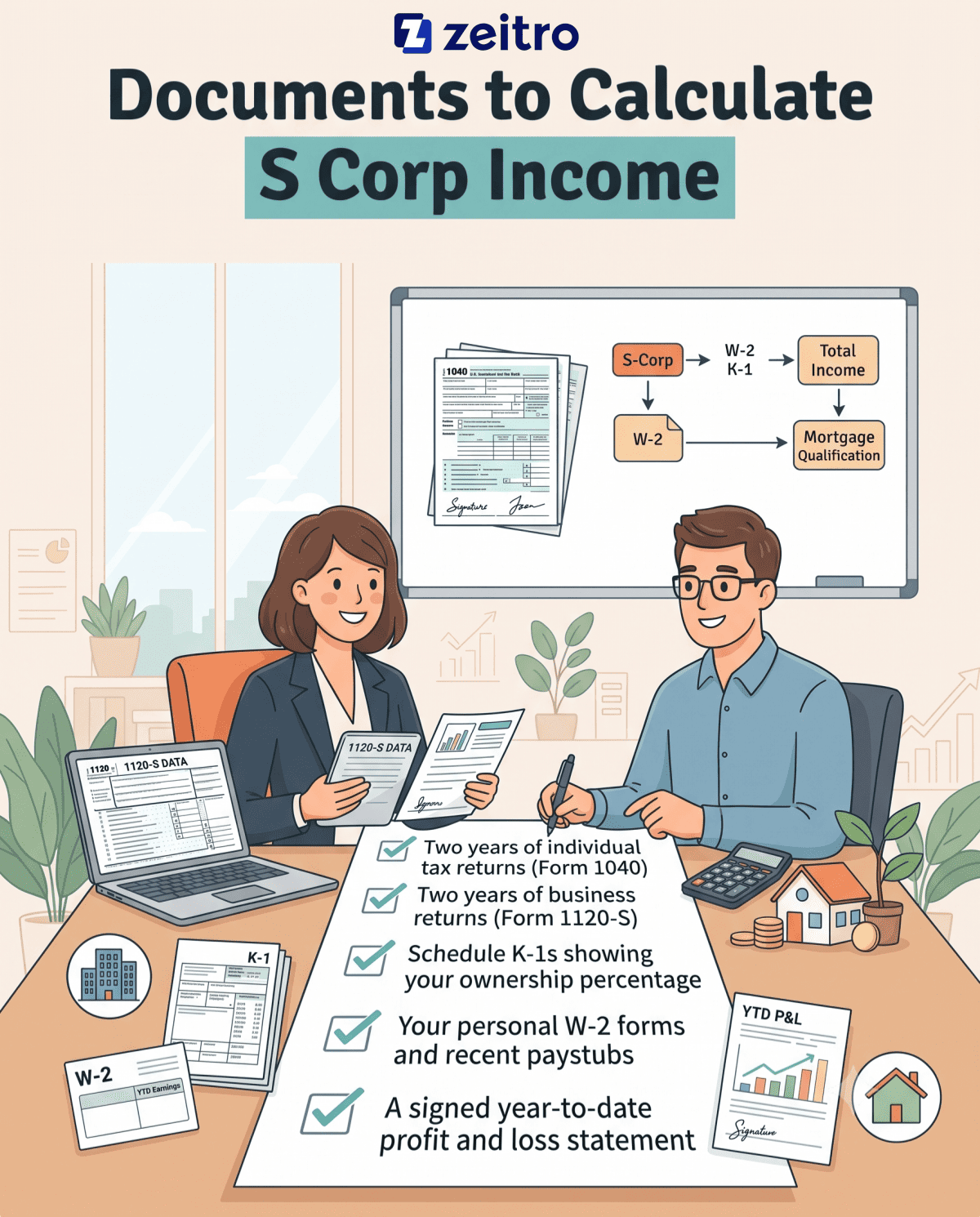

Documents to Calculate S Corp Income

Before I can calculate your borrowing power, we need to gather specific IRS documents. Mortgage underwriters require these papers to verify that your S Corp is stable and your cash flow is completely real. I always tell my clients that preparation here prevents major underwriting delays later.

Typically, most lenders will ask for:

- Two years of individual tax returns (Form 1040)

- Two years of business returns (Form 1120-S)

- Schedule K-1s showing your ownership percentage

- Your personal W-2 forms and recent paystubs

- A signed year-to-date profit and loss statement to show current revenue trends

How to Calculate Income from an S Corp?

To find your monthly qualifying income, lenders typically review your S Corp earnings over the past 24 months and average them, following Fannie Mae's self-employed income guidelines. A common simplified approach looks like this:

Qualifying Monthly Income = [W-2 Wages] + [(Adjusted Net Business Income × Ownership %) / 12]

However, underwriters may adjust this calculation based on factors such as declining income, one-time gains or losses, and program-specific rules.

- First, locate your ownership percentage on your Schedule K-1. Next, determine the "Adjusted Net Business Income" from Form 1120-S by taking your ordinary business income and adding back non-cash expenses like depreciation and depletion.

- Then, subtract any short-term business debts due in less than one year.

- Multiply this adjusted number by your ownership share, add your personal W-2 salary, and divide the sum by 24.

For example, say you own 50% of an S Corp. Your annual W-2 wage is $60,000.

Your business reports $100,000 in ordinary income, has $10,000 in depreciation, and $10,000 in short-term debts due within one year. In this simple example, adding back depreciation and subtracting short-term debts offset each other, so the adjusted net business income remains $100,000.

Your 50% share of this is $50,000. Adding your $60,000 W-2 gives $110,000 annually, which averages out to a qualifying income of $4,583 per month.

FAQs About S Corp Income Calculation

Q1. Can I use Schedule K-1 income if I own less than 25% of the S Corp?

Yes, you can, but the rules are different. If your ownership share is below 25%, mortgage lenders do not classify you as self-employed. They treat you as a typical W-2 employee. To count your K-1 ordinary income, I have to prove to the underwriters that you have a two-year history of actually receiving those corporate distributions and show that the business is highly stable.

Q2. Why do mortgage lenders add back depreciation to S Corp income?

Depreciation is a non-cash paper expense used to lower your taxable business income. While it saves you money on taxes, it does not actually involve cash leaving your business bank account. Because underwriters want to evaluate your true cash flow rather than just your taxable income, they add this figure back. This standard practice significantly increases your qualifying income and buying power.

Q3. What happens if my S Corp shows a net loss?

A business net loss will negatively impact your mortgage application. When your S Corp shows a net loss, underwriters generally subtract your share of that loss from your overall qualifying income. In practice, this often feels like your W-2 wages are being reduced by the loss amount, which lowers the income the lender can use to qualify you.

For example, if you earned $70,000 in W-2 wages but your corporate share of the loss was $20,000, your qualifying income drops to $50,000. If the losses are massive or show a downward trend, lenders might refuse the loan entirely.

Q4. Will I need a Year-to-Date (YTD) Profit and Loss (P&L) statement?

Yes, you almost certainly will. Because your latest tax returns only show historical data, lenders need to verify that your S Corp is still healthy today. A signed YTD Profit and Loss statement, along with a balance sheet, proves that your current business revenues are consistent with your previous tax filings. Keeping these documents updated keeps your mortgage application on the fast track.

Q5. How do lenders treat declining S Corp income over the last two years?

If your business income is declining, many lenders will be reluctant to simply average your last two years. Instead, they generally focus on the most recent, lower year when determining your qualifying income. When the year-over-year drop exceeds roughly 20%, it often raises a red flag and may require additional explanations or supporting documentation. In my practice, I have seen underwriters reject loans for declining revenues unless we can prove the drop was a one-time event.

Final Word

Navigating S Corp cash flows requires a careful approach. While tax advisors focus on reducing your liability, mortgage underwriters focus strictly on your borrowing safety. Preparing your files six to twelve months before applying makes a massive difference. If you are planning a home purchase, I highly recommend sitting down with a mortgage professional who specializes in self-employed underwriting to ensure your math aligns with today's lending guidelines.

People Also Read

- Can I Use Current Year Income Instead of Tax Return Income?

- How to Average Self-Employed Income Over Two Years?

- How Much Business Income Can Be Used for Mortgage Qualification?

- [Ultimate Guide] How Do I Analyze Self-Employed Tax Returns?