Written by

Eric

Share this article

.svg)

Subscribe to updates

Every loan officer dreads that moment: you are analyzing a self-employed borrower's tax returns and realize their income took a hit last year. Your stomach sinks because you know conventional guidelines are incredibly strict on downward trends. Instead of panicking or giving up, I have learned that navigating this scenario requires a highly tactical approach to satisfy picky underwriters and keep the deal alive.

Key Takeaways

- Determine the Cause: Know if the dip is temporary or structural.

- Provide Hard Proof: Support the file with a strong LOE and YTD financials.

- Adjust Calculations: Use only the lower, most recent year's income.

- Have a Backup: Pivot to Non-QM or restructuring if needed.

- Improve Efficiency: Use Zeitro Strata AI to automatically verify and calculate income.

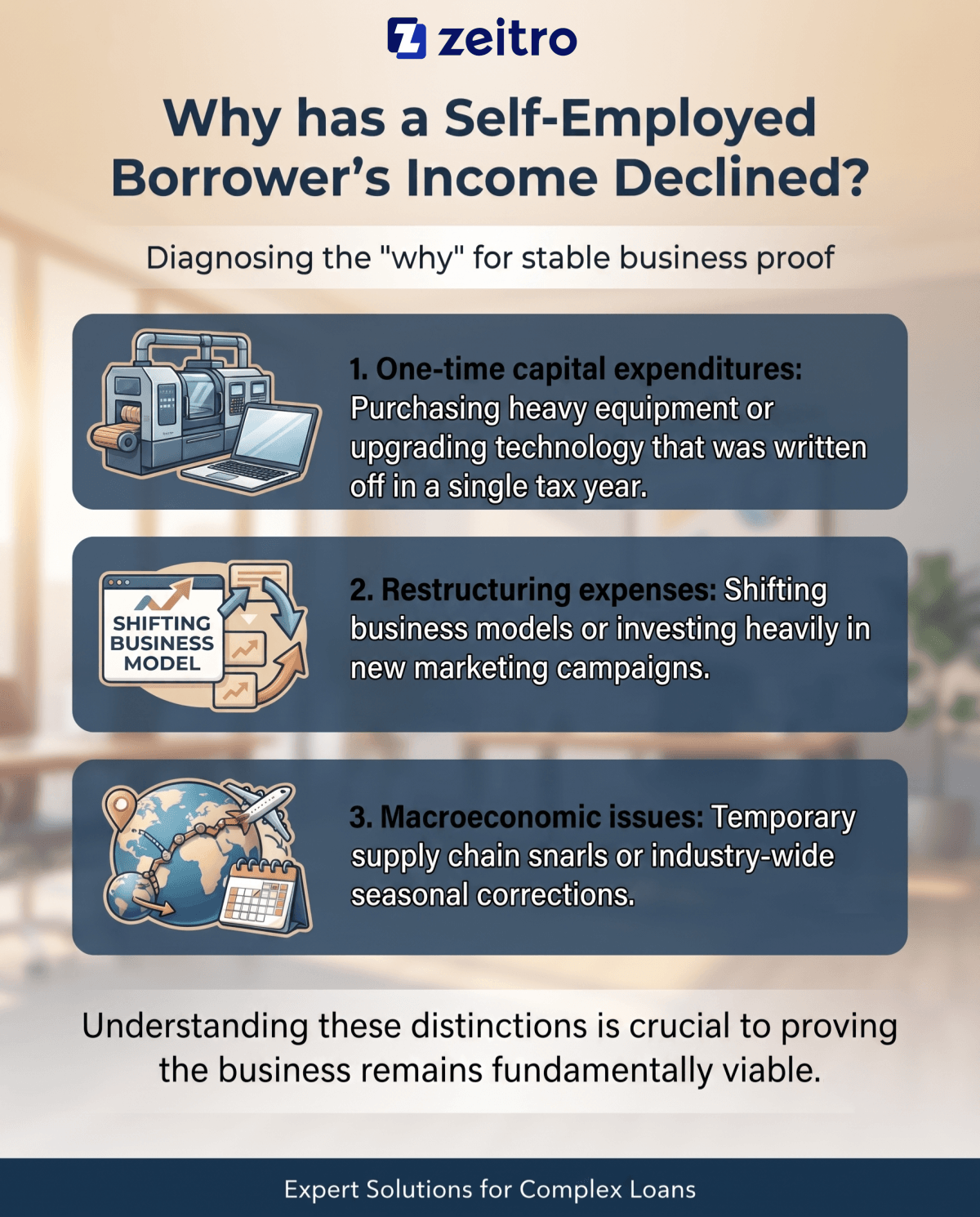

Why has a Self-Employed Borrower's Income Declined?

When I analyze a tax return with declining numbers, my first step is to act like an underwriter and diagnose the "why." A drop in net profit does not mean the file is dead, but we must prove the business is still stable. Over the years, I have seen several common reasons for these income fluctuations:

- One-time capital expenditures: Purchasing heavy equipment or upgrading technology that was written off in a single tax year.

- Restructuring expenses: Shifting business models or investing heavily in new marketing campaigns.

- Macroeconomic issues: Temporary supply chain snarls or industry-wide seasonal corrections.

Understanding these distinctions is crucial to proving the business remains fundamentally viable.

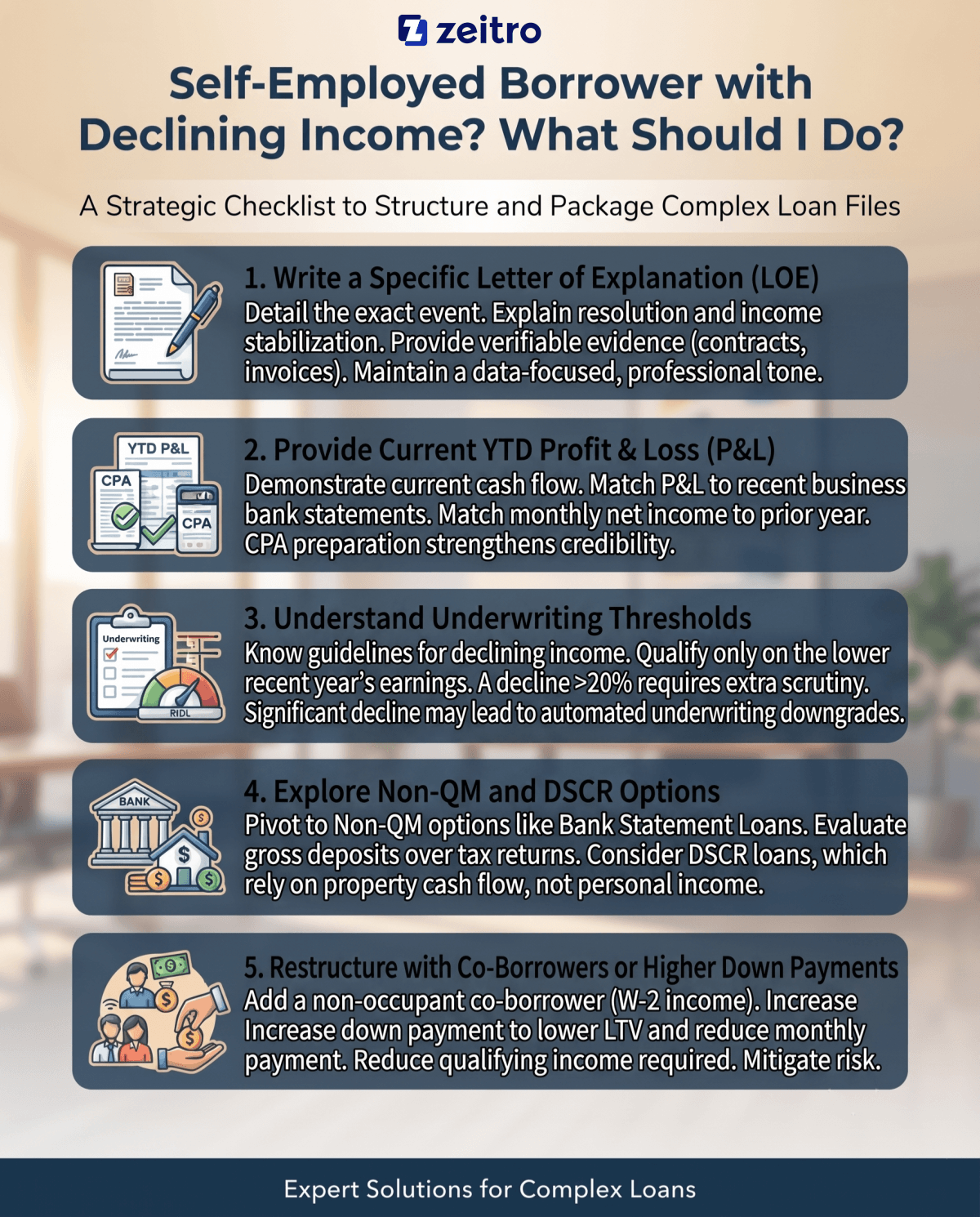

Self-Employed Borrower with Declining Income? What Should I Do?

Once you understand the cause of the decline, it is time to build a strong defense. Here is the exact checklist I use to structure and package these complex loan files for approval.

Write a Letter of Explanation

A generic "my business had a bad year" will not satisfy an underwriter. I always work closely with my borrowers to draft a highly specific, factual Letter of Explanation. The letter must clearly explain the exact event that caused the dip, detail why this event is now resolved, and prove that income has stabilized.

For instance, if a consultant lost a major client but replaced them with two new accounts, we list the names, contract dates, and values. I always ensure we back up our claims with verifiable evidence, like signed business agreements or paid invoices.

Underwriters look for data, not emotions, so keeping the tone professional and logical is key to showing that the downward trend was merely a temporary hump rather than a terminal business decline.

Provide YTD Profit & Loss (P&L) Statements

Tax returns show where a business was, but a Year-to-Date Profit and Loss statement proves where it is right now. To demonstrate that the income drop has stopped, I typically request a current YTD P&L, preferably prepared or reviewed by a licensed CPA to strengthen credibility, although borrower-prepared statements are often acceptable depending on the loan program.

To make this P&L bulletproof, I match it with the borrower's most recent three months of business bank statements. This allows us to prove that the current monthly gross deposits reasonably align with the revenue reported on the P&L. Showing that the monthly net income average over the last six months matches or exceeds the prior year's lower level gives underwriters the peace of mind they need. It shows them that the business has officially stabilized, which is the ultimate goal in saving these files.

Be Aware of Underwriting Thresholds

To protect your deal, you must know the technical underwriting boundaries. Under conventional Fannie Mae and Freddie Mac guidelines, if self-employment income declines year-over-year, you are generally not allowed to average the two years of income when there is a declining trend, unless the borrower can clearly demonstrate that the income has stabilized or recovered.

Instead, you must qualify the borrower using only the lower, most recent year's earnings. If the decline is severe, typically more than 20%, conventional and FHA guidelines require extra scrutiny. For FHA loans, a significant decline in income (often around or above 20%) may increase the likelihood of an automated underwriting downgrade, depending on the overall risk profile of the file.

In my experience, if the income has dropped by more than 30% without strong compensating factors, underwriters may view the income as unstable and scrutinize the file more heavily, potentially leading to a denial. Calculating the debt-to-income ratio based on the absolute worst-case scenario early on prevents disastrous last-minute loan denials.

Explore Alternative Mortgage Options

When conforming agency guidelines reject the file due to the decline, I immediately pivot to Non-QM options. The most popular choice for my self-employed clients is a Bank Statement Loan. Instead of looking at tax returns where heavy business write-offs and declining net profits hurt qualification, these programs evaluate 12 or 24 months of gross bank deposits. This often yields a much higher qualifying income.

If the property is an investment, I look at DSCR loans, which primarily rely on the property's rental income rather than the borrower's personal income and focus solely on whether the property's rental cash flow covers the monthly mortgage payment. While these alternative programs usually require a slightly higher down payment and interest rate, they provide a highly reliable path to closing when traditional tax-transcript-based loans are out of the question.

Consider Co-Signers or Higher Down Payments

If we must stay within conventional guidelines but the qualifying income is too low because we are using the lower year's numbers, we have to restructure the loan. One effective strategy I use is adding a non-occupant co-borrower, such as a family member with stable, predictable W-2 income, to offset the higher debt-to-income ratio.

Alternatively, I ask the borrower if they can increase their down payment. Putting more money down serves two purposes: it lowers the loan-to-value ratio, which reduces the underwriter's overall risk profile, and it directly shrinks the monthly mortgage payment, lowering the required qualifying income. Restructuring the loan in this manner shows the underwriter that we are actively mitigating the risk of the declining business income, making the file far more palatable to the risk department.

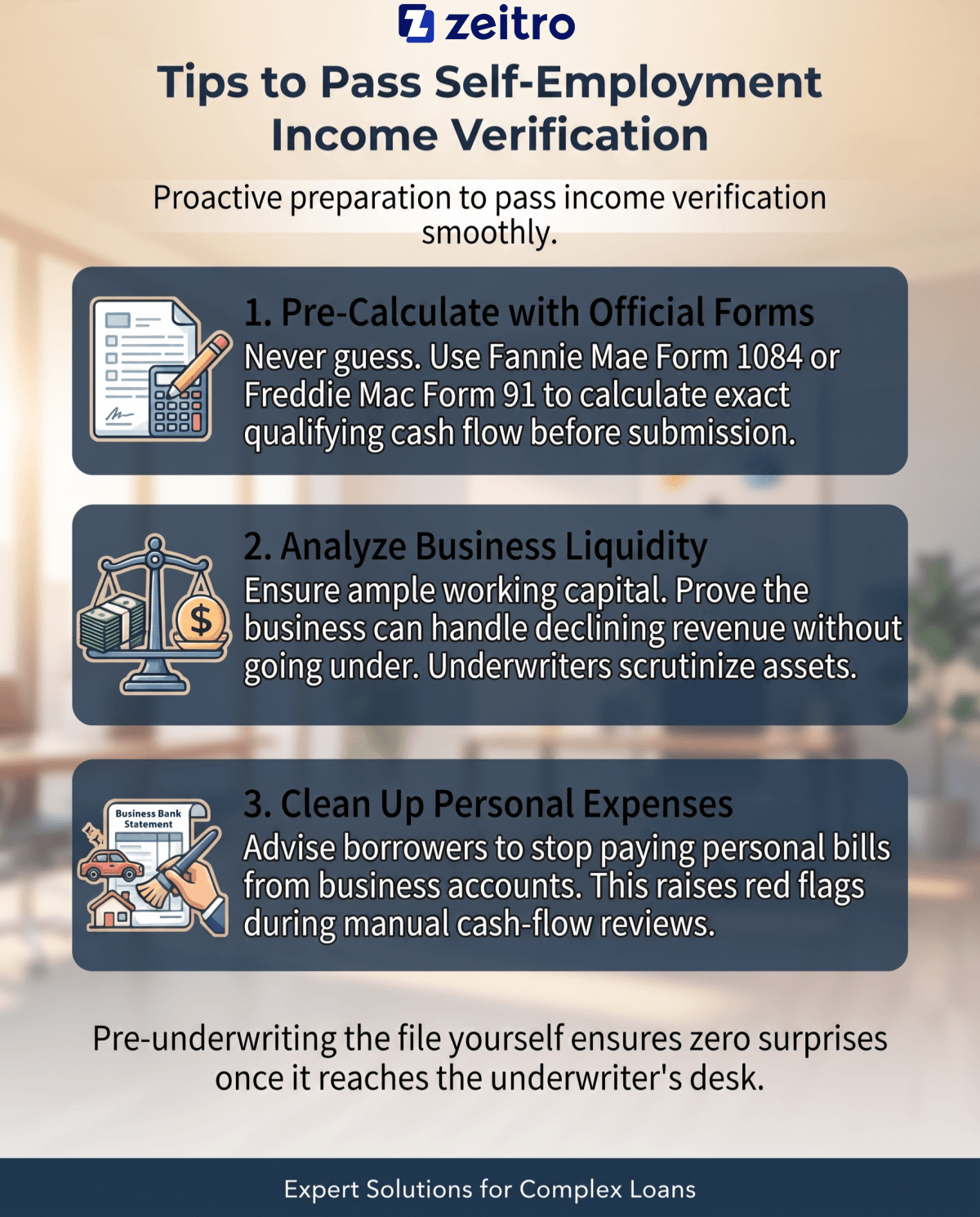

Tips to Pass Self-Employment Income Verification

Getting a self-employed borrower with declining income approved requires proactive preparation. Here are my top tips to help you pass income verification smoothly:

- Pre-Calculate with Official Forms: Never guess the income. I always use Fannie Mae Form 1084 or Freddie Mac Form 91 to calculate the exact qualifying cash flow before submitting the file.

- Analyze Business Liquidity: Underwriters look closely at business assets. Ensure the business has ample working capital to prove it can easily handle declining revenue without going under.

- Clean Up Personal Expenses: Advise your borrowers to stop paying personal bills out of business accounts, as this raises immediate red flags during a manual cash-flow review.

Pre-underwriting the file yourself ensures there are zero surprises once it lands on the underwriter's desk.

FAQs About Self-Employed with Declining Income

Q1: Can I qualify for a conventional loan if my self-employment income declined last year?

Yes, you can still qualify, but the underwriting process changes significantly. When conventional underwriters see a decline in year-over-year income, they will not allow you to average the two years. Instead, they will use the lower, most recent year's income to calculate your debt-to-income ratio.

Additionally, you must prove that the downward trend has stopped. I always package these files with a current Year-to-Date Profit and Loss statement and recent business bank statements to show the underwriter that the business income has stabilized and is highly likely to continue.

Q2: Does a drop in gross business revenue automatically disqualify me?

No, a drop in gross revenue is not an automatic deal-killer. Underwriters look at net qualifying income, not just gross receipts. For instance, if your business revenues fell but your operating expenses decreased even more, your net profit might actually be stable or higher than the previous year.

I recently had a client who scaled down their operations to focus only on high-margin clients. Although their gross revenue dropped by 15%, their net income increased. By highlighting this strategy, we secured a quick, hassle-free approval.

Q3: What level of income decline triggers a manual downgrade under FHA guidelines?

Under FHA guidelines, if a self-employed borrower's income declines by more than 20% over the analyzed tax years, the automated underwriting system will likely downgrade the file. This means the loan must be manually underwritten by a human underwriter. Manual underwriting requires much stricter standards, including verifying three to six months of mortgage payment reserves.

To pass a manual underwrite with a steep decline, you must provide extensive documentation of extenuating circumstances, showing that the decline was temporary and that the business has demonstrated a stable or improving trend with sufficient recent documentation.

Q4: Will a letter from my CPA help mitigate an underwriter's concerns?

A CPA letter is highly valuable, but it is not a magic wand. Underwriters appreciate a professional letter confirming your business ownership percentage, verifying that business expenses do not negatively impact your personal cash flow, or explaining the tax treatment of one-time write-offs. However, a letter simply stating "the business is doing great" carries no weight. The letter must be factual, objective, and backed up by hard financial numbers, such as an audited YTD Profit and Loss statement, to truly influence an underwriter's decision.

Q5: What is the best alternative loan if Fannie Mae or Freddie Mac guidelines decline my file?

If traditional conventional guidelines decline your file due to declining income, the best alternative is a Non-QM Bank Statement Loan. These programs completely ignore tax returns and net tax losses. Instead, lenders verify your ability to pay by calculating your actual monthly cash flow using 12 or 24 months of business bank deposits. If you are buying an investment property, a DSCR loan is another excellent alternative. It requires no personal income documentation at all, qualifying the loan solely on whether the property's projected rental income covers the mortgage payment.

Final Word

Handling a self-employed borrower with declining income is undoubtedly challenging, but it is far from impossible. In my years of originating loans, I have found that early detection, thorough documentation, and a deep understanding of guidelines are what separate closed deals from denied files.

By taking a proactive approach, preparing detailed explanation letters, and being ready to pivot to flexible Non-QM alternatives when necessary, you can successfully navigate these tough scenarios. Remember, a decline on paper is just a puzzle waiting for the right mortgage strategy to solve it.

People Also Read

- How Much Business Income Can Be Used for Mortgage Qualification?

- How Do Underwriters Calculate Schedule C Income?

- How Should I Calculate Income If the Borrower Owns an LLC?

![[Ultimate Guide] How Do I Analyze Self-Employed Tax Returns?](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/6a48809aea04f502e012dac9_analyze-self-employed-tax-returns-banner.png)