Written by

Eric

Share this article

.svg)

Subscribe to updates

Analyzing self-employed tax returns presents a notorious bottleneck for underwriters, who must painstakingly calculate cash flow while adhering to rigid agency guidelines. Understanding how underwriters calculate Schedule C income is essential for processing these complex loans.

To simplify this process and eliminate manual math errors, you can use the Zeitro Mortgage Income Calculator to upload documents and generate fast, secure, and fully compliant income calculations.

Key Takeaways

- Standardized Adjustments: Underwriters use IRS Schedule C to evaluate the cash flow of sole proprietors, beginning with net profit (Line 31) and adjusting for non-cash expenses.

- Essential Add-Backs: Non-cash items such as depreciation, depletion, and business use of home are added back to boost the borrower's qualifying income.

- Necessary Deductions: Actual cash expenses like non-deductible meals and one-time non-recurring income are subtracted to reveal true operational cash flow.

- Historical Trend Analysis: Lenders generally analyze two years of Schedule C income, but a declining trend may require additional trend analysis and a more conservative qualifying income approach, depending on the file and guideline requirements.

- Automated Acceleration: Implementing automated systems like Zeitro helps mortgage professionals bypass tedious manual calculations and ensure strict guideline compliance.

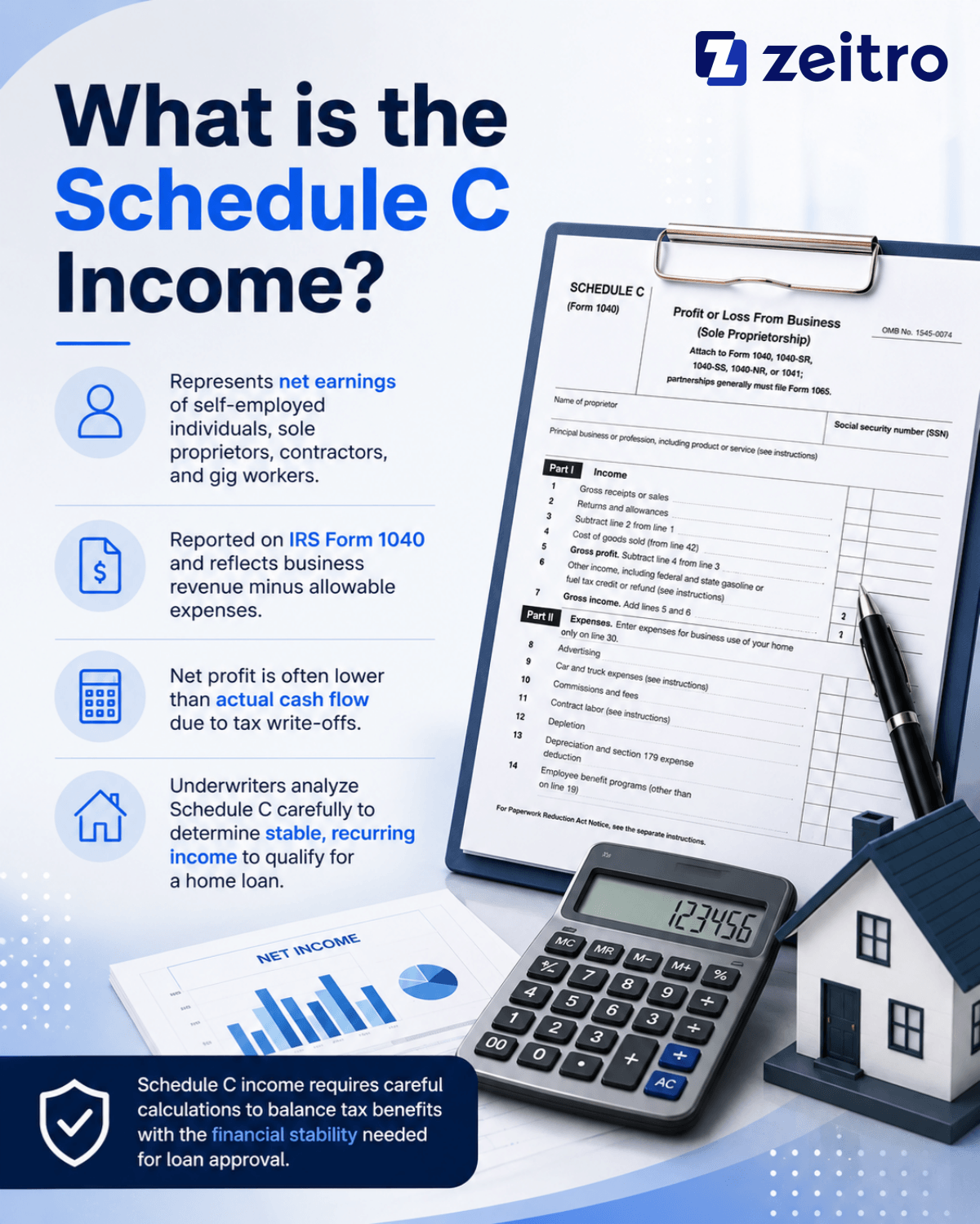

What is the Schedule C Income?

In real estate financing, Schedule C income represents the net earnings of self-employed individuals, sole proprietors, independent contractors, and gig workers. Unlike regular W-2 salaried employees who receive steady, predictable biweekly paychecks, Schedule C borrowers report business revenues and expenses on IRS Form 1040. Because their income is subjected to tax write-offs, the net profit reported to the IRS is often lower than their actual cash flow.

This makes underwriting more complex. Mortgage underwriters cannot simply use a borrower's gross revenue; they must analyze the Schedule C to determine the stable, recurring income available to repay a home loan. Qualifying these borrowers requires careful calculations to balance the tax benefits they claim with the financial stability needed for loan approval.

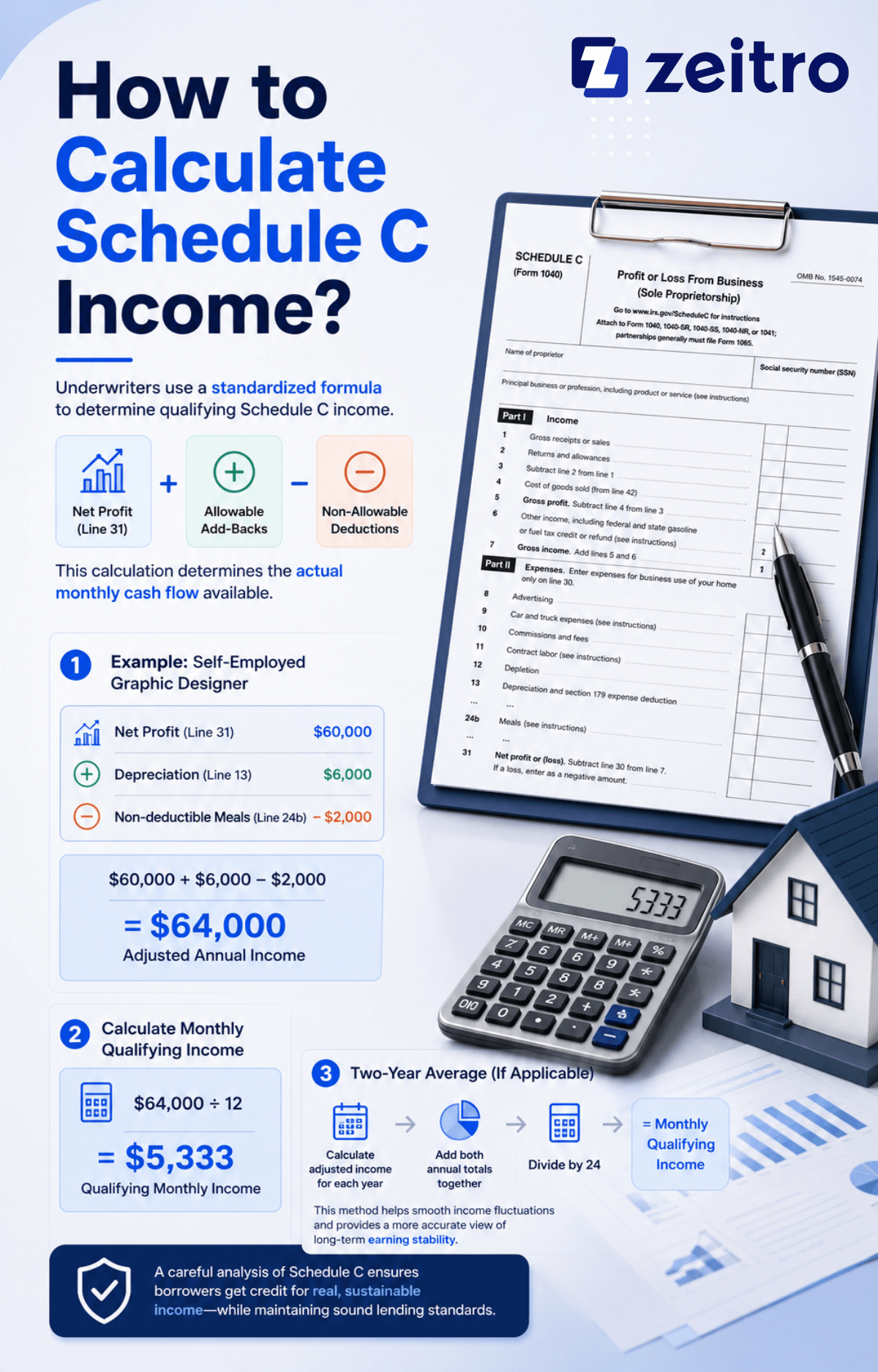

How to Calculate Schedule C Income?

To calculate qualifying Schedule C income, underwriters use a standardized formula: Net Profit (Line 31) + Allowable Add-Backs - Non-Allowable Deductions. This calculation determines the actual monthly cash flow available.

For example, let's look at a self-employed graphic designer's tax return. If their Schedule C reports a Net Profit of $60,000 on Line 31, but also lists $6,000 in Depreciation (Line 13) and $2,000 in Non-deductible Meals (Line 24b), the underwriting adjustment works as follows:

$60,000 (Net Profit) + $6,000 (Depreciation Add-Back) - $2,000 (Non-deductible Meals) = $64,000 Adjusted Annual Income.

To find the qualifying monthly income, underwriters typically divide this adjusted annual total by 12, resulting in $5,333 per month. If analyzing a two-year period, underwriters typically calculate each year’s adjusted income separately and then average the two annual totals by dividing the combined amount by 24 to arrive at the monthly qualifying income

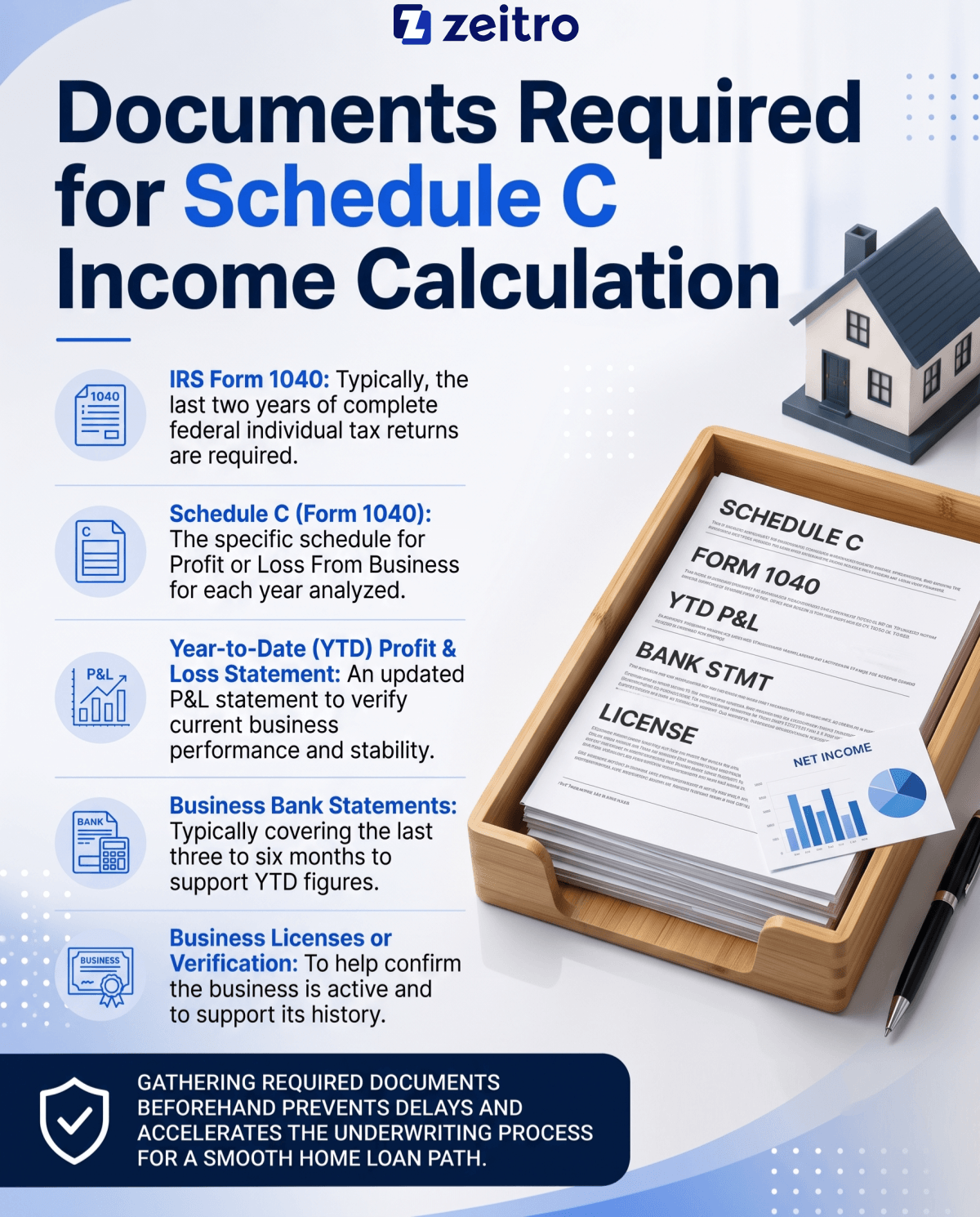

Documents Required for Schedule C Income Calculation

To evaluate a sole proprietor’s cash flow accurately, lenders require a comprehensive set of financial and tax documents. Gathering these items beforehand prevents delays in the underwriting process:

- IRS Form 1040: Typically, the last two years of complete federal individual tax returns are required.

- Schedule C (Form 1040): The specific schedule for Profit or Loss From Business for each year analyzed.

- Year-to-Date (YTD) Profit & Loss Statement: An updated P&L statement to verify the business's current performance and stability.

- Business Bank Statements: Typically covering the last three to six months to support the YTD figures.

- Business Licenses or Verification: Business licenses or other verification may be used to help confirm that the business is active and to support its history, but a full two-year business existence is not always required; in some cases, less than two years may be acceptable if the guideline conditions are met.

What are Common Add-Backs?

Underwriters add certain non-cash paper losses back to the net profit because these write-offs reduce taxable income without requiring an actual, physical cash outflow from the business. Common add-backs include:

- Depreciation: Depreciation (Line 13) is a common add-back, representing a non-cash expense that may be added back in qualifying income analysis.

- Depletion: Non-cash tax deductions (Line 12) allowed for businesses that extract natural resources.

- Amortization/Casualty Losses: Intangible asset write-offs or sudden, non-recurring losses that do not impact daily cash operations.

- Business Use of Home: Business use of home expenses (Line 30) are often added back in underwriting worksheets when allowed by the applicable guideline, because they are treated as a business expense adjustment in the cash-flow analysis.

What are Common Deductions?

Just as some non-cash expenses are added back, certain financial items must be deducted from the reported net profit to accurately capture the borrower's actual, ongoing cash flow. Common deductions include:

- Non-Deductible Meals: the non-deductible portion of meals expense reported on Line 24b may be adjusted in underwriting to reflect actual cash flow.

- Non-Recurring Income: Any one-time revenues, unexpected insurance payouts, or extraordinary business gains must be subtracted, as they do not represent steady, predictable future cash flow.

- Business Mileage Adjustments: Business mileage adjustments may be treated as a separate underwriting adjustment, with mileage depreciation calculated and included according to the applicable worksheet and guideline.

FAQs About Calculating Schedule C Income

Q1. How do underwriters handle declining Schedule C income?

If tax returns show a year-over-year decline in net income, underwriters generally do not average the two years. Instead, they will use the most recent, lower-earning year as the qualifying income, or they may deny the loan if the decline is substantial and threatens the viability of the business.

Q2. Why does my qualifying income differ so much from my actual bank deposits?

Qualifying income is heavily adjusted for tax write-offs, non-deductible items, and non-cash expenses to reflect stable long-term cash flow rather than just gross cash flowing in. Underwriters must align your earnings with agency guidelines, which differs from simply looking at your gross bank deposits.

Q3. Can I qualify for a mortgage with only one year of Schedule C tax returns?

While two years of tax returns are standard, some automated underwriting systems (such as Fannie Mae's DU or Freddie Mac's LP) may permit a one-year requirement if the borrower has been in the same line of work for several years and the business exhibits high stability.

Q4. What is the role of a Year-to-Date (YTD) Profit and Loss (P&L) statement?

Underwriters use a YTD P&L statement (often supported by recent bank statements) to verify that your business's income has remained stable since your last filed tax return, ensuring there are no sudden financial downturns that would jeopardize your mortgage application.

Q5. Are home office deductions added back to Schedule C income?

Yes, in many cases, standard guidelines allow underwriters to add back the "Business Use of Home" deduction (Line 30) because those housing expenses are already accounted for in your primary housing payments.

Final Word

Calculating Schedule C income involves careful analysis of tax write-offs, non-cash expenses, and historical income trends. Underwriters must navigate these adjustments carefully to ensure accurate cash flow calculations that meet strict agency standards. To minimize the administrative burden and reduce processing times, utilizing automated tools is highly beneficial.

The Zeitro Mortgage Income Calculator offers a reliable solution, allowing you to upload documents securely and calculate qualifying income according to guidelines. By simplifying complex calculations, it helps both originators and underwriters evaluate self-employed files with greater confidence and efficiency. You can access the tool today to streamline your underwriting workflow.

People Also Read

- How to Calculate Self-Employed Income for a Mortgage?

- Income Verification Documents: A Complete Guide for Employees and Self-Employed

- How Should I Calculate Income If the Borrower Owns an LLC?

- Borrower Income Analysis: Ultimate Guide for Loan Officers

- Solved] Can I Use K-1 Income to Qualify a Borrower?

![[Solved] Can I Use K-1 Income to Qualify a Borrower?](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/6a44cb55129383ad19f46080_can-i-use-k-1-income-to-qualify-a-borrower-banner.png)