Written by

Eric

Share this article

.svg)

Subscribe to updates

In my early days as a loan officer, I quickly learned that qualifying borrower income is rarely straightforward. With changing economic conditions and a surge in gig-economy and self-employed applicants, calculating qualifying income can feel like hitting a moving target. Every file that lands on my desk has its own story, whether it is a straightforward W-2 wage earner or an investor juggling multiple rental properties.

A single calculation error can stall a file in underwriting or, worse, trigger a costly loan buyback. In this ultimate guide, I will share the exact methods and frameworks I use to dissect borrower income. We will cover the core calculation logic for various income types, essential documentation checklists, and how leveraging modern automated tools has completely transformed my daily pipeline speed. Let us dive in.

Key Takeaways

- Accuracy is Key: Precision in income calculation directly impacts your pull-through rate and borrower trust.

- Context Matters: W-2, variable, self-employed, and rental income all follow entirely different underwriting rules.

- Documentation is Critical: Collecting the right paperwork upfront prevents stressful last-minute loan conditions.

- Tech Simplifies Work: Using AI-powered tools helps cross-reference lender guidelines in seconds, keeping your pipeline moving.

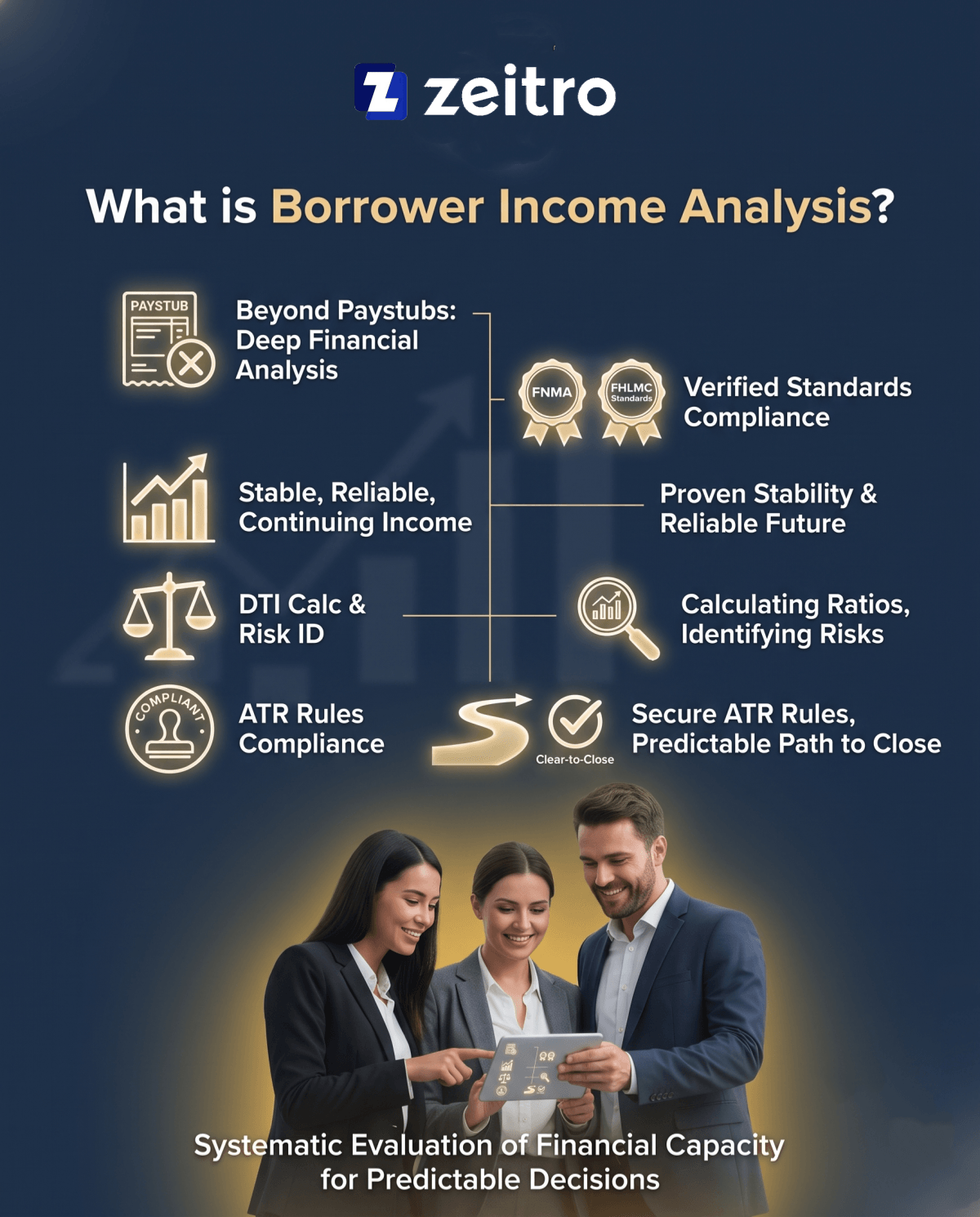

What is Borrower Income Analysis?

Basically, borrower income analysis is the systematic process we use to evaluate a borrower's financial capacity to repay a mortgage. It goes far beyond simply looking at a paystub. Under Fannie Mae and Freddie Mac standards, the primary goal is to establish that qualifying income is stable, reliable, and expected to continue. If the income source has a defined expiration date or depends on limited assets, lenders must document that it is likely to continue for at least three years.

In my day-to-day work, this involves calculating the monthly qualifying income, analyzing debt-to-income (DTI) ratios, and identifying any potential financial risks. Doing this thoroughly upfront ensures that we meet federal Ability-to-Repay (ATR) rules and secure a smooth, predictable path to a clear-to-close.

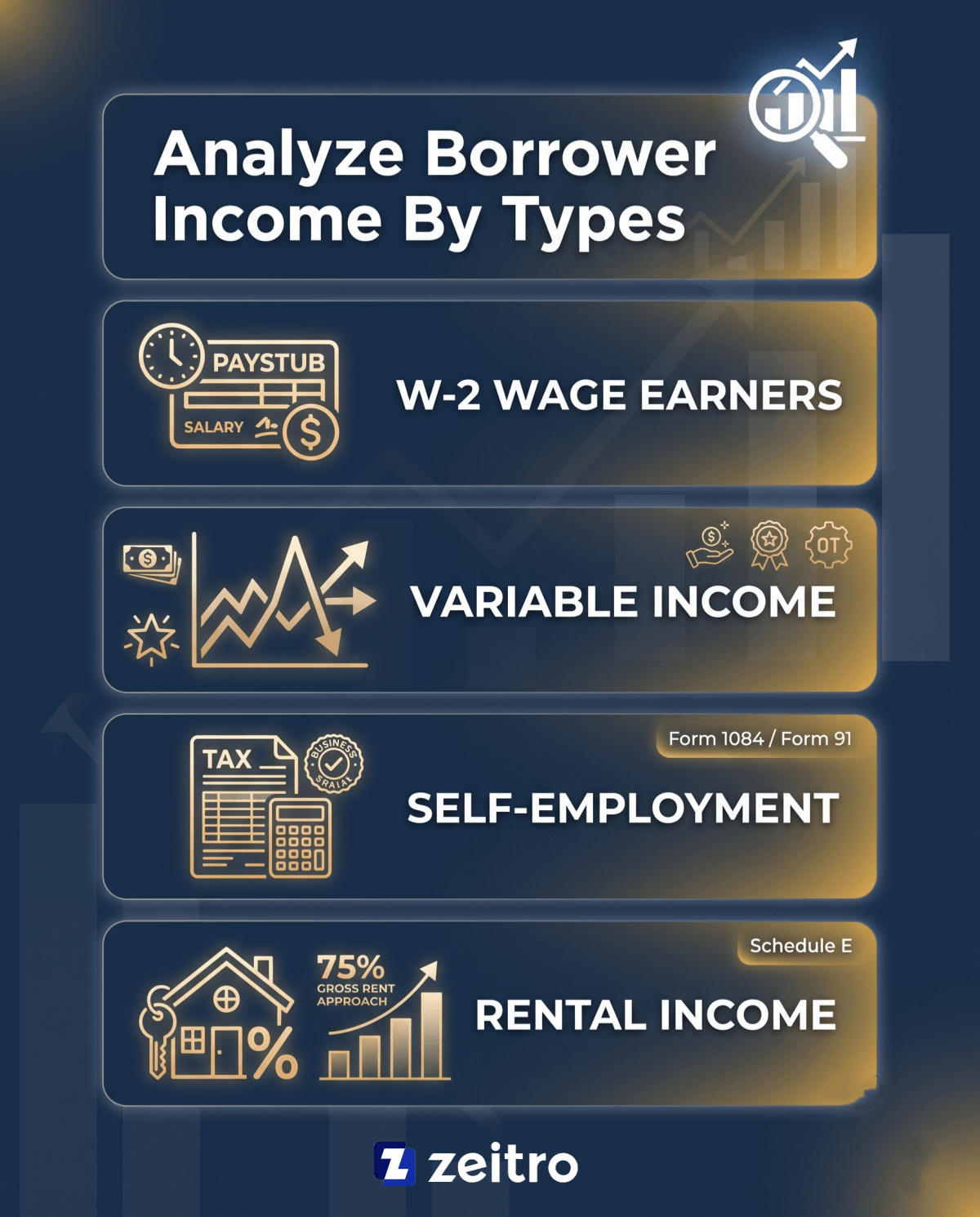

Analyze Borrower Income By Types

Not all income is treated equally in the mortgage world. In my experience, understanding the nuances of each income category is what separates average loan officers from top producers. Here is how I break down the four main types:

- W-2 Wage Earners: This is the most straightforward category. I calculate qualifying income using the base hourly rate or salary. However, I always cross-reference the year-to-date paystubs to ensure no sudden drops in hours.Variable Income: This includes commission, bonuses, and overtime. Variable income such as commission, bonuses, and overtime is often evaluated using a two-year history, but 12 to 24 months may still be acceptable when offset by strong positive factors. Lenders also review the income trend and may need to use the current lower amount if the trend is declining.

- Self-Employment: This is where things get tricky. I use Fannie Mae Form 1084 or Freddie Mac Form 91 to analyze cash flow, starting with tax-return net profit and adjusting for applicable non-cash expenses and other guideline-driven add-backs such as depreciation.

- Rental Income: For rental properties, lenders commonly use Schedule E, tax returns, or a current lease agreement to evaluate rental income, and many programs use a 75% of gross rent approach to account for vacancy and expenses, depending on the loan product and guidelines.

Also Read:

- How to Calculate Self-Employed Income for a Mortgage?

- How to Calculate Employment Income for a Mortgage?

- How to Calculate Rental Income? Loan Officer's Guide

- How to Calculate Commission Income for Mortgage?

- How to Calculate Overtime Income for a Mortgage?

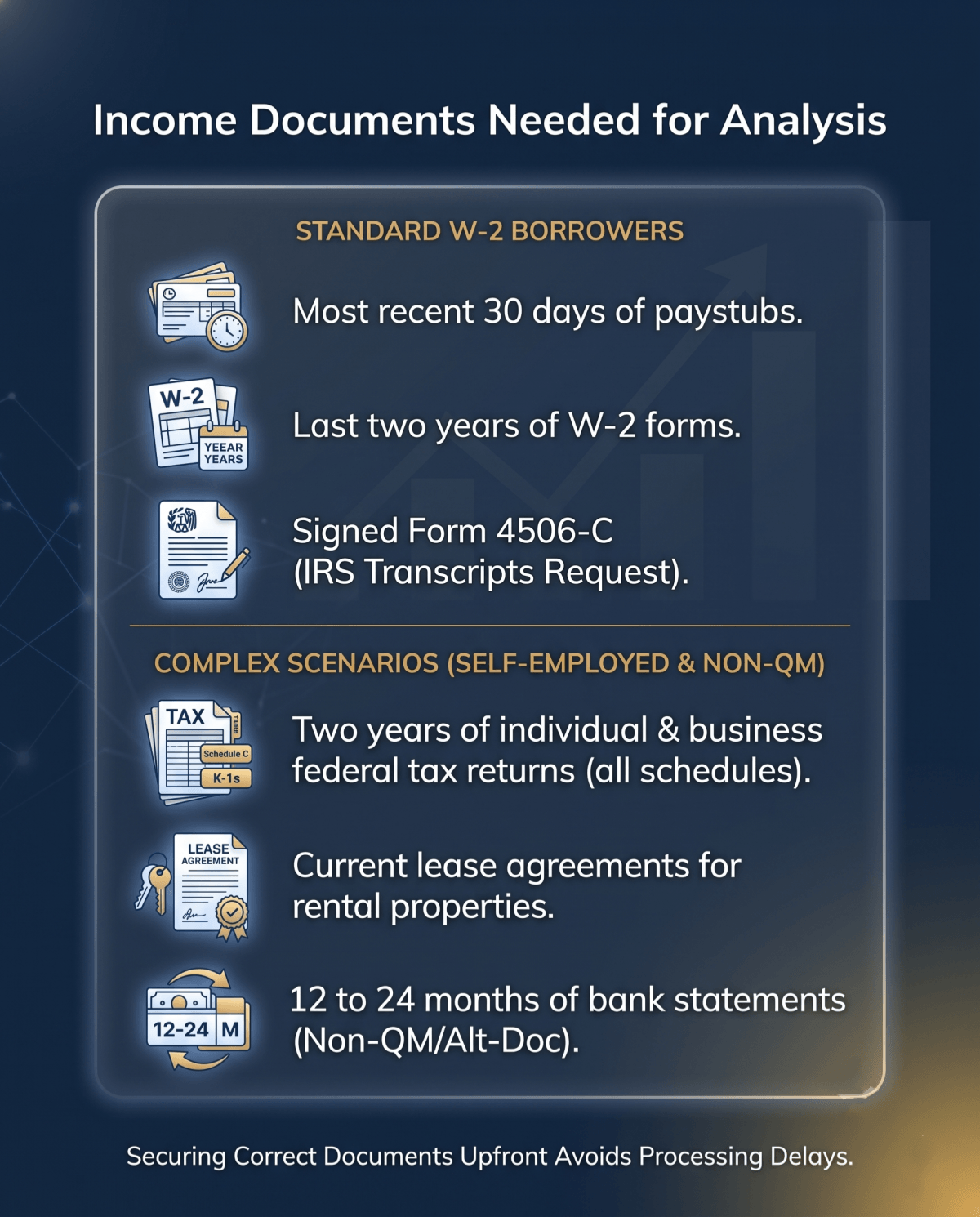

Income Documents Needed for Analysis

Securing the correct documents upfront is essential to avoid processing delays. Over the years, I have built a go-to checklist that covers both standard files and complex scenarios.

For standard W-2 borrowers, I always collect the most recent 30 days of paystubs and the last two years of W-2 forms. I also require a signed Form 4506-C so the lender can request tax transcripts from the IRS.

When dealing with self-employed borrowers or real estate investors, the paperwork gets heavier. I ask for two years of individual and business federal tax returns, including all pages and schedules like Schedule C and K-1s. For rental properties, current lease agreements are necessary. If we are working on a Non-QM or alternative document loan, I pivot to collecting 12 to 24 months of personal or business bank statements to reconstruct their actual monthly cash flow accurately.

Zeitro Strata AI - Borrower Income Analysis Tool Recommended

Manual income analysis and guideline research can easily consume hours of your day. To streamline this bottleneck, I highly recommend using Zeitro Strata AI. It is an AI-powered mortgage guideline assistant that has redefined how I manage my pipeline.

What makes this platform stand out is its ability to let you upload financial documents directly for automated, highly secure income calculations. Because it is SOC 2 Type II certified, the platform has undergone an independent examination of its controls over a period of time, which can provide added confidence in its security and privacy practices.

Whether you are working on a conventional self-employed loan or a complex Non-QM deal, Zeitro Strata AI helps you cross-reference guidelines across more than mainstream wholesale lenders in seconds. Key features include:

- DeepSearch Capabilities: Easily run queries across 300+ guidelines, including bank statements, DSCR, and FHA programs.

- Zero Hallucinations: Every answer comes with clear, hyperlinked citations to the original lender guidelines, giving you complete confidence.

- Integrated Tools: It features a built-in pricing engine, digital 1003 POS, and support for multilngual queries, with 10 free daily queries to get started.

Also Try:

- Zeitro Mortgage Employment Income Calculator for Loan Pros

- Zeitro Mortgage Affordability Calculator Free and Online

- Zeitro DSCR & Rental Income Calculator for Mortgage

FAQs About Borrower Income Analysis

Q1. How do you handle a self-employed borrower with declining year-over-year income?

If a self-employed borrower's income has declined, lenders generally may not average the declining period. If the lower level has stabilized, the current lower amount is typically used, and additional documentation may be needed to confirm stability.

Q2. Can I use rental income from a departing primary residence to qualify?

Yes. You can offset the existing mortgage payment using a signed lease agreement and proof of a security deposit. Most guidelines require applying a 25% vacancy factor to the gross rent.

Q3. What is the minimum history required to count commission income?

Generally, a 12 to 24-month history of receiving commission income with the same employer is required. If it is less than 24 months, you will need a strong letter of explanation showing industry consistency.

Q4. Why is SOC 2 Type II certification important for mortgage AI tools?

This certification indicates that the software's controls have been independently examined against SOC 2 trust services criteria. It ensures that sensitive borrower documents, like tax returns and bank statements, are handled with enterprise-grade security.

Q5. Can 1099 income be qualified without a full tax return?

Yes, through Non-QM programs. Many lenders offer specific 1099 loan options where we can qualify borrowers using just their 1099 forms and a year-to-date profit and loss statement, bypassing complex tax write-offs.

Final Word

Mastering borrower income analysis is the ultimate way to close more loans and build a stellar reputation in the mortgage industry. While manual calculations and guideline research used to take up half of my day, adopting smart automation has changed everything.

By integrating tools like Zeitro Strata AI into your workflow, you can accurately calculate complex incomes, search vast investor guidelines, and protect borrower data through SOC 2 Type II compliance. I highly recommend giving their free daily queries a try to experience the time savings firsthand.