Written by

Eric

Share this article

.svg)

Subscribe to updates

As an experienced loan officer navigating the US housing market, I often see self-employed homebuyers feel overwhelmed by the lending process. If you run your own business, getting a home loan absolutely involves more scrutiny than a standard W-2 employee faces.

Why? Because lenders must ensure the long-term stability of your earnings. We aren't just looking at what you made last month. We need to verify your business has the ongoing ability to generate enough cash flow to cover a monthly mortgage payment safely. In this guide, I will break down exactly how underwriters calculate your qualifying income, the specific documents you need, and why understanding this process is your secret weapon.

Key Takeaways

- Ownership threshold: Having a 25% or greater ownership interest in a business officially classifies you as self-employed in the mortgage world.

- History matters: Lenders generally require a two-year earnings history, though certain exceptions allow for just one year.

- Cash flow is king: We use cash flow analysis (often via Fannie Mae's Form 1084) to determine qualifying income, which includes "adding back" non-cash deductions like depreciation to boost your borrowing power.

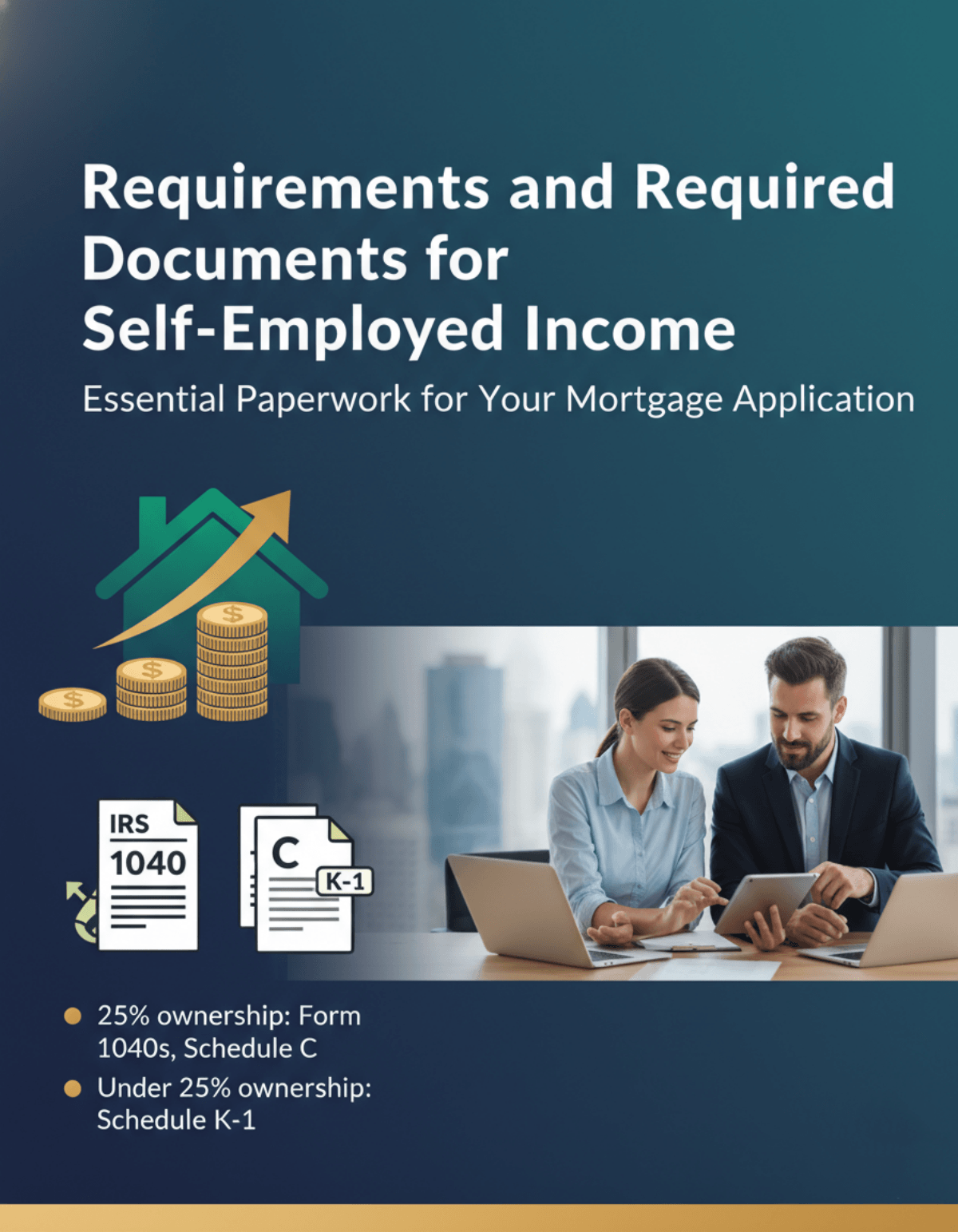

Requirements and Required Documents for Self-Employed Income

To get started, we first need to define your exact employment status. In mortgage underwriting, an individual is considered self-employed if they hold a 25% or greater ownership interest in a company. Because we must establish a track record showing your earnings will likely continue, a standard two-year history of prior income is generally required. The exact paperwork you provide depends entirely on your ownership percentage:

- For 25% ownership or more (Self-Employed): You must provide your personal IRS Form 1040s and Schedule C (for sole proprietorships) or applicable corporate returns.

- For under 25% ownership: If you are a partner or part of an S Corporation or LLC, you may not be subject to the full-scale self-employment business analysis required for majority owners. However, because you hold an ownership stake, your income from the business, often reported on a Schedule K-1, is still subject to specific verification regarding your proportionate share of earnings and their accessibility.

How Does Self-Employed Income Affect Your Mortgage Loan?

You might wonder why underwriters dig so deep into your financials. When reviewing a self-employed file, we analyze several critical factors: the historical stability of your earnings, the location and nature of your company, the market demand for your products or services, and the overall financial strength of the business.

All of this directly impacts your Debt-to-Income (DTI) ratio. The final "qualifying income" we calculate dictates your maximum approved loan amount. If your tax write-offs are aggressively high, your paper income drops, which could potentially lower your purchasing power. Don't worry. This standard procedure isn't meant to penalize you. It's simply the bank's way to ensure you aren't taking on more debt than your actual business cash flow can comfortably handle.

How to Calculate Self-Employment Income in Mortgage?

Also Try: Zeitro Mortgage Income Calculator

This is where the magic happens. As a loan officer, I don't just look at the bottom line of your tax return. We use a cash flow analysis method, utilizing tools like Fannie Mae's Form 1084 or an internal income calculator.

- For 25% or Greater Ownership (Self-Employment): We evaluate your gross income, business expenses, and taxable income. The best part? We apply Add-backs. We add back nonrecurring losses, depreciation, and depletion to your bottom line, as these are "paper losses" that don't affect your real cash flow. We will subtract out-of-pocket costs like travel and meals. We must also analyze business liquidity and viability.

Exception: We can actually waive business tax returns if you use personal funds to close, have been operating for 5+ years, and show increasing earnings. Otherwise, expect to provide 2 years of personal and business returns (or 1 year if in business 5+ years).

- For Under 25% Ownership (Schedule K-1): We look at your proportionate share of earnings reported on the K-1. We must verify that this money was either distributed to you or that the company has adequate liquidity to support your withdrawal.

Exception: Normally, this requires 2 years of personal returns plus the K-1s. However, 1 year is allowed if only rental income is reported on your K-1.

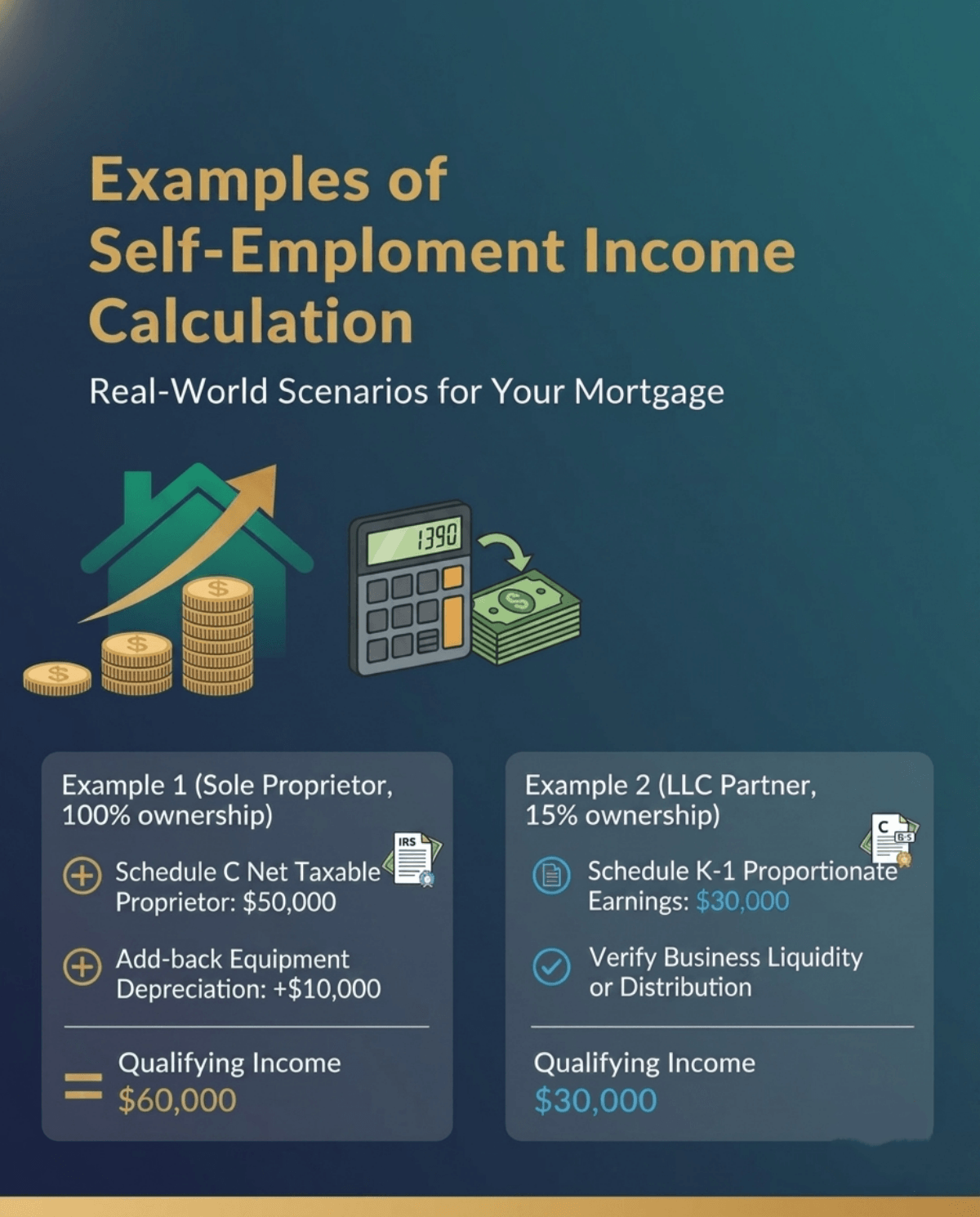

Examples of Self-Employment Income Calculation

Let's look at two realistic scenarios to show how paper income differs from mortgage qualifying income.

- Example 1 (Sole Proprietor, 100% ownership):Imagine your Schedule C shows a net taxable income of $50,000. However, you claimed $10,000 in equipment depreciation. Because depreciation is a non-cash expense, I get to use an "add-back." Your actual qualifying income for the mortgage is $50,000 + $10,000 = $60,000.

- Example 2 (LLC Partner, 15% ownership):You hold a 15% stake in an LLC. Your Schedule K-1 shows your proportionate share of earnings is $30,000. As long as we can verify the business has adequate liquidity or that the $30,000 was actually distributed into your personal accounts, we can add that full amount to your qualifying income.

FAQs About Self-Employed Income Calculation

Q1. Can I get a mortgage with only 1 year of self-employment history?

Yes, it is possible. If you own 25% or more of the business, you usually need to prove the company has been operating for at least five years. For Schedule K-1 borrowers, a one-year history is permitted if the K-1 only reports rental income.

Q2. What are "add-backs" in a self-employed mortgage calculation?

Add-backs are a buyer's best friend. They are non-cash expenses, like depreciation or depletion, that reduce your taxable income on paper but don't negatively impact your actual cash on hand. Lenders add these figures back into your qualifying income, helping you secure a higher loan amount.

Q3. What is the difference between Schedule C and Schedule K-1 for mortgages?

Schedule C is used for sole proprietors or independent contractors who typically own 100% of their business (or at least 25%). A Schedule K-1 is used for borrowers who are partners in an S-Corp, LLC, or partnership, usually indicating an ownership stake of less than 25%.

Q4. What mortgage loans can the self-employed apply for?

You have access to all standard options, including Conventional, FHA, and VA loans. However, if your tax write-offs are too high, you can explore Non-QM products like Bank Statement Loans, which qualify you based on actual banking deposits rather than tax returns.

Q5. What is considered a 1099 self-employed borrower?

A 1099 borrower is an independent contractor, freelancer, or gig worker. Because taxes aren't automatically withheld from your paychecks by an employer, the mortgage industry views you as a self-employed sole proprietor. You will need to provide a Schedule C to calculate your qualifying income.

Conclusion

Being your own boss shouldn't stop you from achieving the American dream of homeownership. While the paperwork might seem daunting at first glance, understanding the 25% ownership threshold, gathering your two years of tax returns or K-1s, and knowing how add-backs work can completely change your perspective. As lenders, our goal isn't to reject your application. It is to accurately measure your true cash flow to set you up for long-term success.

Calculating self-employed income can be tricky, and every business structure is unique. Don't let tax write-offs discourage you from applying. Consult with an experienced loan officer today to find out your true qualifying income. You might be surprised by how much house you can actually afford!

People Also Ask

- How to Calculate PMI? Do the Math On Your Own

- [Solved] What Percentage of Income Should Go to Mortgage?

- Mortgage Income Requirements 2026: Learn Before You Apply

- Ultimate Guide: How to Calculate Net Income for a Mortgage?

- 2026 Guide: How to Calculate Gross Income for a Mortgage?

- Income Needed for Mortgage: Methods, Examples & Requirements

- Mortgage Income Verification Guide for Loan Officers

- How to Calculate Rental Income? Loan Officer's Guide

- How Should I Calculate Income If the Borrower Owns an LLC?

- [Ultimate Guide] How Do I Analyze Self-Employed Tax Returns?