Written by

Eric

Share this article

.svg)

Subscribe to updates

If you've been in the mortgage industry as long as I have, over 15 years now, you know that keeping up with lending rules is a full-time job. In 2026, the mortgage market is shifting faster than ever. Between the new conforming loan limit hitting $832,750 and the explosive growth of Non-QM products, manually digging through hundreds of PDF matrices is a surefire way to kill a deal.

Today, top-producing Loan Officers are ditching the old way. Instead, they are turning to tools like Zeitro's Scenario AI. By simply using a chat interface, you can instantly verify guidelines across different lenders, saving hours of research and rescuing dying deals.

What are Mortgage Guidelines?

Think of mortgage guidelines as the absolute "rulebook" or the DNA of a loan approval. In simple terms, these are the strict criteria established by government-sponsored enterprises (like Fannie Mae and Freddie Mac), government agencies (such as the FHA), and private investors in the secondary market.

These rules dictate the minimum standards a borrower must meet for a loan to be approved and ultimately funded. They cover everything from acceptable credit profiles and income verification methods to property types and reserve requirements.

When I train new Loan Processors, I always tell them: Guidelines aren't suggestions. They are boundaries. If a file doesn't fit the box perfectly, you need a documented exception, or the deal simply won't close. As the market evolves into 2026, understanding this foundational rulebook is the only way to determine whether you can actually get your client to the closing table.

Types of Mortgage Guidelines (QM vs. Non-QM & More)

The mortgage landscape isn't one-size-fits-all. Because we serve vastly different borrower profiles, the guidelines are broken down into specific categories. Generally, they are split between Qualified Mortgage (QM) and Non-Qualified Mortgage (Non-QM) loans. With Non-QM expected to capture a massive share of originations in 2026, it is vital to understand these diverse niches.

Here are the most common types of guidelines you'll encounter today:

- Conventional: The gold standard backed by Fannie Mae and Freddie Mac. Great for W-2 borrowers with strong credit.

- FHA (Federal Housing Administration): Perfect for first-time buyers or those with lower credit scores, offering low down payments.

- VA (Veterans Affairs): Designed for eligible military members, focusing heavily on residual income rather than strict debt ratios.

- Jumbo: For loan amounts exceeding the 2026 baseline limit of $832,750. These carry strict investor-specific rules.

- Bank Statement (Non-QM): A lifesaver for self-employed borrowers, qualifying them based on 12 to 24 months of business deposits rather than tax returns.

- DSCR (Debt Service Coverage Ratio): Specifically for real estate investors. Qualification is based on the property's rental cash flow rather than personal income.

- Asset Utilization (Non-QM): Allows high-net-worth individuals to use their liquid assets to calculate a monthly income equivalent.

- Foreign National (Non-QM): Tailored for non-U.S. citizens buying property here, requiring alternative credit verification.

- ITIN (Non-QM): Designed for tax-paying immigrants without a standard Social Security Number.

- WVOE (Written Verification of Employment): A niche option relying solely on an employer's written verification rather than traditional pay stubs.

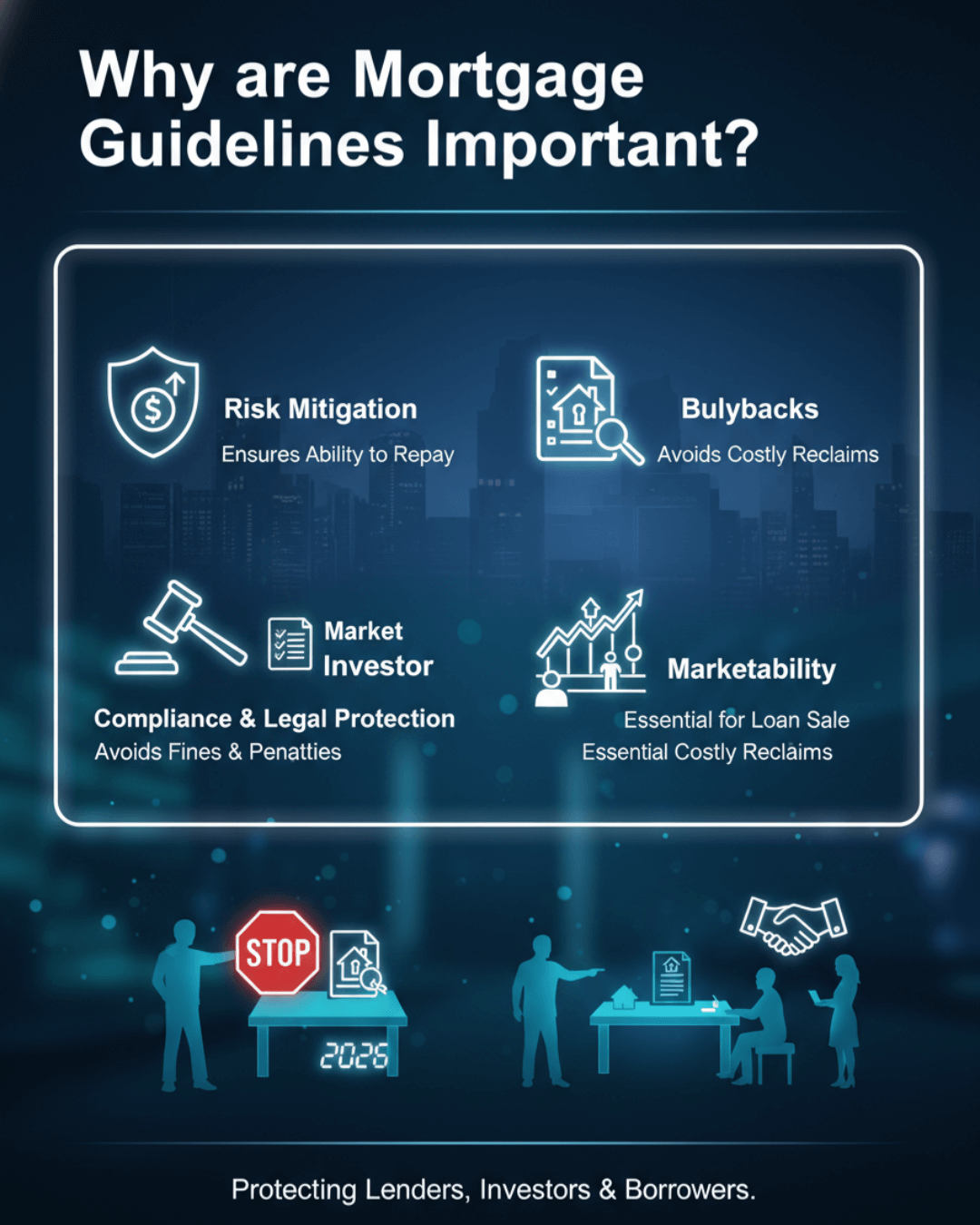

Why are Mortgage Guidelines Important?

You might wonder why lenders are so obsessed with these rules. From a Loan Officer or Broker's perspective, strict adherence to guidelines is about protecting your pipeline and your paycheck. Here is why they matter:

- Risk Mitigation: Guidelines ensure that the borrower actually has the ability to repay the loan, drastically lowering the risk of default.

- Compliance & Legal Protection: Following the rules keeps originators compliant with federal regulations, avoiding hefty fines.

- Marketability: Most lenders don't hold loans. They sell them. If a loan doesn't meet the investor's guidelines, it cannot be legally sold in the secondary market.

- Preventing Buybacks: This is every lender's worst nightmare. If you close a loan that violates a guideline, the investor can force your company to buy the unsalable loan back.

Key Mortgage Qualification Guidelines

No matter which loan type you are structuring, Underwriters will always scrutinize a few core qualification metrics. I like to call these the "Big Five."

- Credit Score (FICO): The ultimate indicator of creditworthiness. While FHA might accept a 580, a Jumbo investor might demand a 700+.

- LTV (Loan-to-Value Ratio): This measures how much equity is in the deal. Higher LTVs equal higher risk.

- DTI (Debt-to-Income Ratio): Your borrower's monthly debt compared to their gross income. Conventional loans usually cap around 45-50%, while Non-QM loans might offer more flexibility.

- Reserves: The liquid cash a borrower has left after closing. Essential for investment properties and Jumbo loans to cover months of mortgage payments if things go south.

- Employment & Income History: Standard rules require a two-year history, but how it's calculated varies wildly between W-2 and self-employed files.

The tricky part? These baseline metrics look completely different depending on the specific lender and loan program.

How to Quickly Check & Verify Mortgage Guidelines in 2026?

Back in the day, when I had a tricky file, I would spend hours hitting "Control-F" on massive PDF matrices or waiting a full day for an Account Executive (AE) to reply to my email. With nearly 100 lenders updating their policies daily, that traditional method is completely dead in 2026.

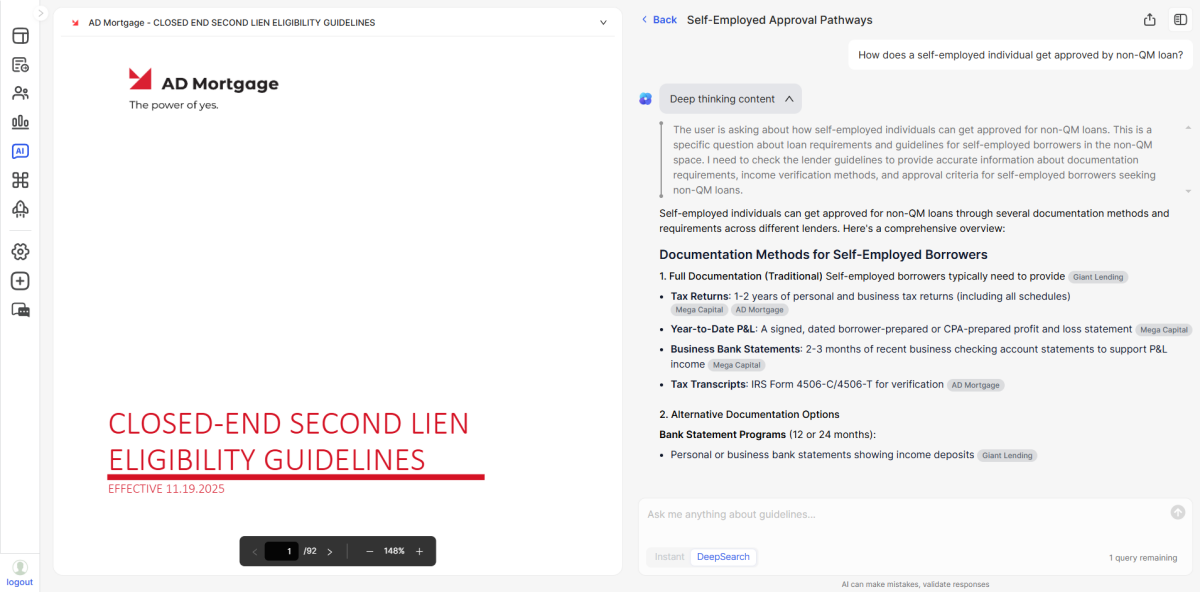

To stay competitive, I now rely on Zeitro's Scenario AI, what I consider the ultimate AI-powered mortgage guideline assistant. It is built specifically for our industry and is an absolute game-changer, especially when navigating complex Non-QM scenarios.

Here is why top-producing originators are making the switch:

- Comprehensive & Constantly Updated Coverage: It covers over 300 unique guidelines across major wholesale lenders, including powerhouses like AD Mortgage, Freedom Mortgage, and CMG Financial. Whether it's QM or Non-QM, the database is always current.

- Instant Answers with Citations: You can ask vague questions like "What is DSCR?" or highly specific ones like "Eligibility for ITIN with 10% down." Within seconds, it delivers precise answers. Better yet, it provides direct citations linking back to the source document, giving you 100% confidence to quote your borrower.

- Customizable DeepSearch & 'Explain' Feature: You can narrow your search to specific lenders. If you don't fully understand an underwriting caveat, you can use the "Explain" function to have the AI break down the jargon into plain English based on your selected parameters.

- Cost-Effective Efficiency Booster: It drastically reduces the manual labor for Loan Officers and Processors. By accelerating the loan structuring process and minimizing human error, it directly boosts your ROI.

- Unmatched Market Value: It integrates smoothly with LOS (Loan Origination Systems), supports multiple languages (you can type in English or Chinese), and operates at lightning speed. And the cost? It starts at a ridiculously low $8 per month.

FAQs About Mortgage Guidelines

Q1: How often do mortgage guidelines change?

Guidelines change frequently, often driven by macroeconomic factors, interest rate fluctuations, and investor risk appetite. Fannie Mae and Freddie Mac release updates regularly, while private Non-QM investors might tweak their matrices weekly. Using an automated tool is essential to track these silent updates.

Q2: What is an underwriting exception?

An exception occurs when a borrower falls slightly short of a specific guideline (like being 1% over the DTI limit) but has strong "compensating factors," such as massive cash reserves. Understanding the underlying rules helps you successfully argue for an exception with your Underwriter.

Q3: Can AI accurately verify non-QM guidelines?

Yes. While early generic AI suffered from "hallucinations," purpose-built tools like Scenario AI pull directly from the lenders' primary source documents. Because they provide exact citations to the original matrices, the accuracy is exceptionally high, making them safe for real-world loan structuring.

Also Read: Non-QM Loan Guidelines: How to Check and Verify with AI Accuracy

Conclusion

In the highly competitive 2026 mortgage market, speed and accuracy are everything. The originators who can instantly digest and apply complex guidelines are the ones closing the most deals and earning the trust of their referral partners. You simply cannot afford to lose a borrower to a competitor just because you were stuck reading a 100-page PDF or waiting for an AE to call you back.

It's time to modernize your workflow. I highly recommend trying out Zeitro's Scenario AI today. You can experience the platform absolutely risk-free since they offer 3 free queries every single day. Test it on your hardest Non-QM file and watch it instantly pull the exact answer with a citation. Do yourself, and your processing team, a favor: share the link or send them an email about this tool. Embrace the AI advantage, protect your margins, and let's close more loans this year.

People Also Read

- What Are FHA Mortgage Guidelines? How to Verify FHA & Overlays Quickly?

- Conventional Mortgage Guidelines: What and How to Check Quickly?

- VA Mortgage Guidelines: What Are They and How to Check Them Quickly?

- Jumbo Mortgage Guidelines: Check Eligibility Quickly and Accurately

- Foreign National Mortgage Guidelines: Verify Eligibility Fast

- How to Check Mortgage Eligibility? Quick and Accurate with Sources

- Max DTI for Mortgage: Requirements By Loan Types