Written by

Eric

Share this article

.svg)

Subscribe to updates

If you've ever found yourself staring at a stack of 1003 forms at 8 PM, wondering why you're doing data entry instead of selling, you know the struggle. I've been there, like chasing missing stips, cross-referencing PDF guidelines until my eyes blurred, and losing clients because my process was just too slow.

The mortgage industry is brutal. Speed isn't just a "nice to have". It is the only way to survive. In 2026, the difference between a top producer and someone struggling to make quota often comes down to one thing: the tech stack. We are moving past the era of clunky, server-based software into a time where AI doesn't just "help"—it does the heavy lifting.

After testing nearly everything on the market, I've realized that the right Loan Origination System (LOS) is your best employee. It doesn't sleep, it doesn't make calculation errors, and it can turn a chaotic pipeline into a well-oiled machine. Let's look at the tools that are actually changing the game.

People Also Read:

- [Tips] Where to Buy Mortgage Leads? Warm Leads for LOs

- Detailed Guide: How to Become a Loan Officer with No Experience?

Introduction: What is a Loan Origination System?

A Loan Origination System (LOS) is the central nervous system of any lending operation. It manages the entire loan lifecycle—from the moment a borrower submits an application to the final funding and closing.

Think of it as the engine under the hood. While your CRM handles the relationships and marketing, the LOS handles the actual manufacturing of the loan. It collects documents, runs credit checks, integrates with pricing engines, and ensures you aren't breaking any compliance rules.

Who is this for?

- Loan Officers: To track files and speed up approvals.

- Mortgage Brokers: To shop rates and package loans for lenders.

- Banks & Credit Unions: To manage risk and process high volumes of applications.

- Private Lenders: To automate decision-making on non-standard deals.

In short, if you are lending money or helping others lend money, the LOS is where your business lives.

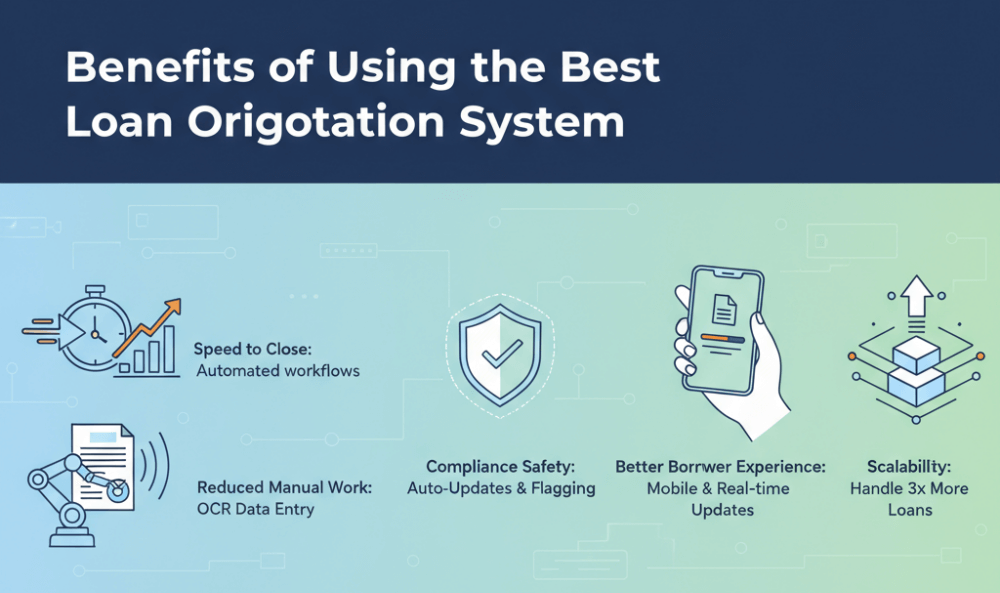

Benefits of Using the Best Loan Origination System

Why should you care about upgrading your LOS in 2026? Because the "old way" is costing you money. Modern loan origination software offers benefits that go far beyond just digital storage:

- Speed to Close: The biggest benefit. Automated workflows can cut weeks off your closing time.

- Reduced Manual Work: Modern LOS platforms use OCR (Optical Character Recognition) to read tax returns and pay stubs, so you don't have to type in data manually.

- Compliance Safety: Rules change constantly. A good LOS updates automatically, flagging files that might trigger an audit or buyback.

- Better Borrower Experience: Borrowers expect a "Amazon-like" experience. They want to upload docs from their phone and see real-time status updates, not wait for an email.

- Scalability: With the right system, you can handle 30 loans a month with the same effort it used to take to handle 10.

6 Top Loan Origination Systems for You

I've dug through the features, pricing, and user feedback to bring you the systems that are actually worth your time this year.

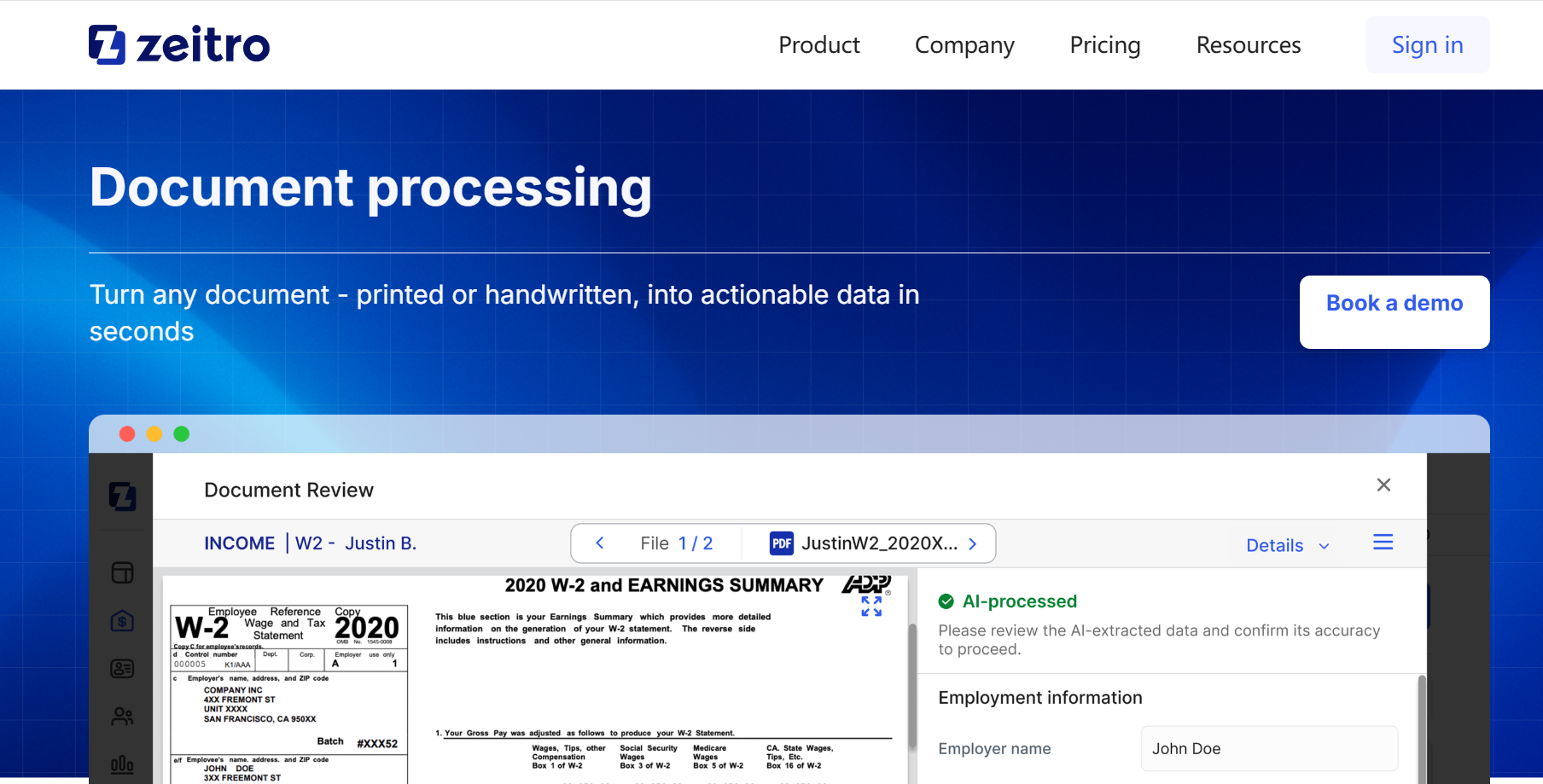

Zeitro - Best Loan Origination System for Anyone

Zeitro is, frankly, the tool I wish I had when I started. While most legacy systems are clunky and expensive "enterpriseware," Zeitro feels like it was built by people who actually understand the daily grind of a Loan Officer. It positions itself as an AI Mortgage Platform, and it lives up to the hype.

The standout feature here is GuidelineGPT. We all know the pain of digging through 1,000-page PDF guidelines to find one specific rule about self-employment income. With Zeitro, you just ask the AI, and it gives you the answer. This alone saves massive amounts of time.

It can help deliver 2.5x faster pre-qualifications and save 7+ hours per loan file. From my experience seeing how it automates the 1003 generation and document review, these numbers are realistic. It's designed to handle everything: Fannie Mae, Freddie Mac, FHA, VA, and even complex Non-QM or Hard Money loans.

Key Highlights:

- AI Efficiency: Reduces 100% of manual guideline research work.

- Speed: Increases loan closes by 30% and closes them up to 20% faster.

- Accuracy: Reach 85%+ income calculation accuracy powered by AI.

- Borrower Experience: Achieve 90%+ application completion rates, letting borrowers finish in just 5 minutes.

- Pricing: This is a huge disruptor. They have a "Freemium" mode, which is great for testing. Paid plans start at just $8/mo per user and $35/mo per company. Compared to the thousands you spend on other tech, this is a steal.

2. LendingPad - Best Loan Origination System for Teamwork

If your team is scattered across different locations or you just hate the "check-in/check-out" file conflicts of older desktop software, LendingPad is your answer. It is a cloud-native LOS, meaning it was built for the web from day one, not ported over from an old server system.

The "Network Effect" inside LendingPad is excellent. It allows Loan Officers, processors, and underwriters to work in the same file at the same time without overwriting each other's work. It connects seamlessly with wholesale lenders, which makes it a favorite for independent mortgage brokers.

Key Highlights:

- Cross-Department Collaboration: Real-time updates mean everyone is always on the same page.

- Anywhere Access: Since it's purely cloud-based, you can originate a loan from your iPad while on vacation though I hope you don't have to!.

- Vendor Marketplace: Huge network of integrated partners for credit, appraisal, and title.

- Fast Implementation: You can get up and running in days, not months.

3. Backbase - Best Loan Origination System for Banks

Backbase is a powerhouse for traditional financial institutions that need to modernize without tearing down their entire infrastructure. If you are a bank, your biggest problem is usually "siloed" data. Your mortgage system doesn't talk to your checking account system. Backbase solves this with what they call "Engagement Banking."

They focus heavily on the customer journey. Their goal is to make a legacy bank app feel as smooth as a fintech app. For loan origination, this means a frictionless application process where customers can start on their phone, stop, and finish on their laptop without losing data.

Key Highlights:

- Unified Platform: Connects retail, SME, and corporate lending into one visual dashboard.

- Customer Experience: Focuses on "frictionless" journeys to reduce drop-off rates.

- Reuse Capabilities: You can reuse data across different loan products, speeding up cross-selling.

- Legacy Integration: specialized in sitting on top of old core banking systems to make them look and feel modern.

4. Turnkey Lender - Best Loan Origination System for Automation

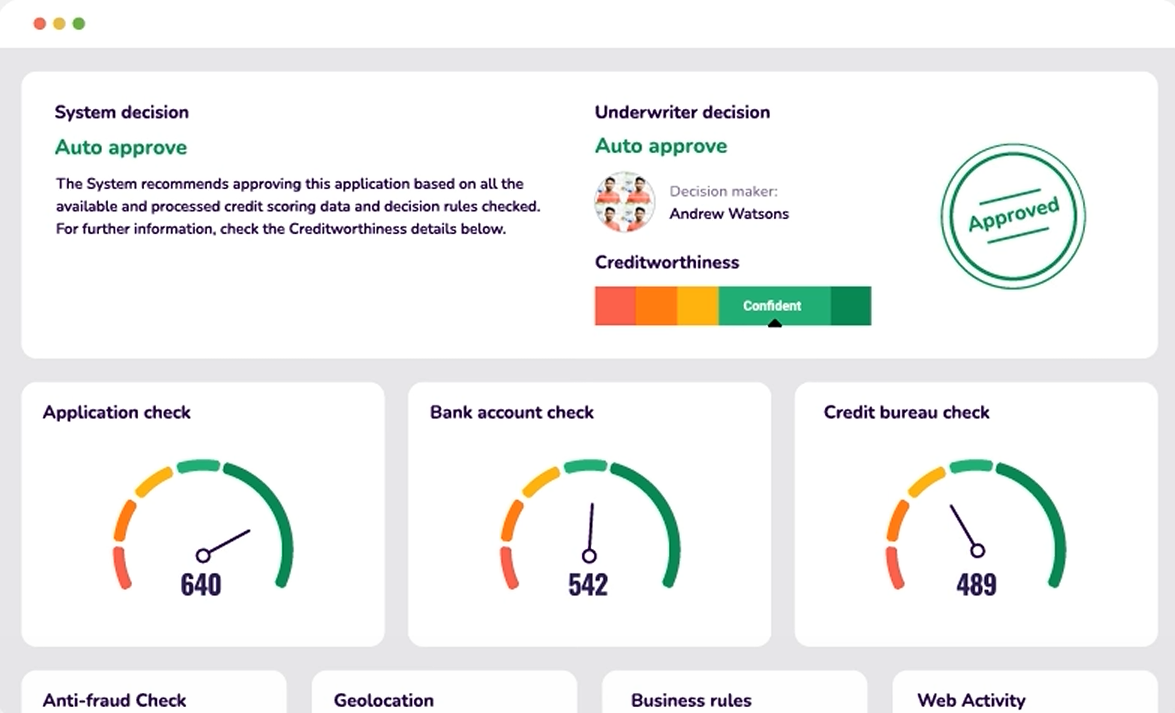

Turnkey Lender is exactly what it sounds like—a complete, ready-to-go solution, but its superpower is automation. This system is heavily focused on using AI for decision-making. If you are a lender who wants to automate the "Yes/No" decision on loans based on credit criteria, this is a strong contender.

They claim to automate over 90% of the loan origination process. This is particularly useful for consumer lenders or alternative lenders who deal with high volumes of smaller loans where manual underwriting just doesn't make financial sense.

Key Highlights:

- AI Decisioning: Proprietary AI credit scoring for instant decisions.

- End-to-End: Handles everything from origination and underwriting to servicing and debt collection.

- Speed: Can process loan applications in under 1 second for auto-approvals.

- Configurability: You can adjust the scorecard and decision rules without needing to code.

5. Trade Ledger - Best Loan Origination System for Real-time Insights

Trade Ledger is a bit different. It shines in the business and commercial lending space. Business loans are notoriously messy because analyzing a company's financials is harder than analyzing a person's pay stub.

Trade Ledger uses a "Unified Data Model" to ingest real-time data from a business's accounting software, bank accounts, and supply chain data. This gives lenders a real-time view of a borrower's risk, rather than looking at a tax return from 12 months ago.

Key Highlights:

- Data-Driven: connects directly to business data sources for real-time risk assessment.

- Business Logic: Specifically designed for complex products like invoice finance and supply chain finance.

- Efficiency: Eliminates the repetitive data entry that plagues commercial lending teams.

- Clarity: Provides a "single source of truth" for complex business borrower profiles.

6. NetOxygen LOS - Best Loan Origination System for Consulting

NetOxygen is a product by Wipro Gallagher Solutions. If you know Wipro, you know they are giants in consulting and enterprise services. NetOxygen is not typically for the solo broker. it is for lenders who need a heavy-duty, enterprise-grade machine.

This system is highly customizable. If you have a unique lending model or need to integrate with proprietary internal systems that no off-the-shelf software can handle, NetOxygen is likely the route you take. It supports multiple channels (retail, wholesale, correspondent) seamlessly.

Key Highlights:

- Enterprise Scale: Built to handle massive volumes and complex organizational structures.

- Customization: If you can dream up a workflow, they can probably build it (with the right consulting support).

- Digital Extensions: Includes tools like "Launchpad" for a better borrower portal experience.

- Compliance: Deep focus on staying compliant across different lending channels and state regulations.

Tip: How to Choose the Best LOS?

Choosing the best mortgage CRM is like a marriage. It's expensive to get into and painful to get out of. Here is how I recommend you approach the decision:

- Assess Your Needs and Define Goals: Are you a solo broker needing speed, or a bank needing compliance? If you are an individual LO, a massive enterprise system like NetOxygen might drown you. If you are a bank, a lightweight tool might not have the security you need.

- Prioritize Essential Features: Make a list of "Must-Haves" vs. "Nice-to-Haves." For me, AI Guideline Search is a must-have in 2026 because of the time it saves. For others, it might be a specific integration with a CRM like Salesforce.

- Evaluate Vendors and Request Demos: Don't trust the screenshots. Get a demo. Ask them to show you a live loan file. See how many clicks it takes to send a pre-approval letter. The fewer clicks, the better.

- Consider Total Cost of Ownership (TCO): Look beyond the monthly fee. Is there an implementation fee? Training costs? usage fees per loan? Zeitro's flat monthly model is transparent, whereas some enterprise tools have complex per-seat or per-closed-loan pricing that eats into your margin.

Conclusion

The lending landscape in 2026 demands efficiency. You simply cannot afford to spend hours manually entering data or digging through guidelines while your competitors are using AI to close deals in half the time.

While all the systems listed above have their strengths, Zeitro stands out as the most forward-thinking option for the majority of loan officers and brokers. The combination of Scenario AI, accurate AI income calculation, and an incredibly accessible price point (starting at Free or $8/mo) makes it a no-brainer to at least try out. It solves the immediate pain points of time and manual labor better than almost anything else I've seen.