Written by

Eric

Share this article

.svg)

Subscribe to updates

If you've spent any time working as a loan officer or underwriter, you know the drill. A borrower wants to finance a vacation property, and suddenly, you're buried in PDF matrices trying to figure out if their scenario fits the latest second home mortgage guidelines. Sifting through varying lender requirements for LTVs, reserves, and distance rules is a massive time-sink.

I used to lose hours cross-referencing these details across different portals. Now, I rely on Zeitro's Scenario AI. This chat-based assistant instantly verifies guidelines across multiple lenders, giving you accurate, source-backed answers in seconds. Let's break down the core requirements and see how this tool changes the game for our pipelines.

What Are the Second Home Mortgage Guidelines?

Second home mortgage guidelines are the specific underwriting rules lenders use to qualify a borrower purchasing a property they intend to occupy for a portion of the year. As mortgage professionals, we know that pricing and risk profiles for these loans sit squarely between primary homes and investment properties.

The core difference comes down to intent and occupancy. A primary residence is where the borrower lives the majority of the year, while an investment property is purchased strictly for rental income. A second home, often a vacation house, must be occupied by the borrower for some part of the year. Crucially, you cannot use projected rental income to qualify the borrower. Furthermore, the property must be suitable for year-round occupancy per Fannie Mae guidelines. Understanding these boundaries is critical before moving a file to processing.

Key Requirements for Second Home Mortgage Guidelines

Qualifying a borrower for a vacation property isn't as straightforward as a primary residence purchase. While Conventional (QM) standards like Fannie Mae provide a baseline, Non-QM lenders have their own overlays. Here are the core metrics you must verify:

- Down Payment (LTV limits): Expect a minimum 10% down payment for conventional loans. However, to secure better pricing or when utilizing Non-QM products (like Bank Statement loans), 15% to 20% is frequently required.

- Credit Score: The absolute floor is generally 620 for agency loans, but realistically, many lenders look for a 680+ FICO to offer competitive pricing on secondary properties.

- Debt-to-Income (DTI) Ratio: Most underwriters will cap the DTI at 45%, factoring in the PITI of both the primary residence and the new second home.

- Reserves: This is where many deals fall apart. Lenders typically demand 2 to 6 months of PITI reserves.

Keep in mind, these requirements fluctuate drastically depending on the specific lender.

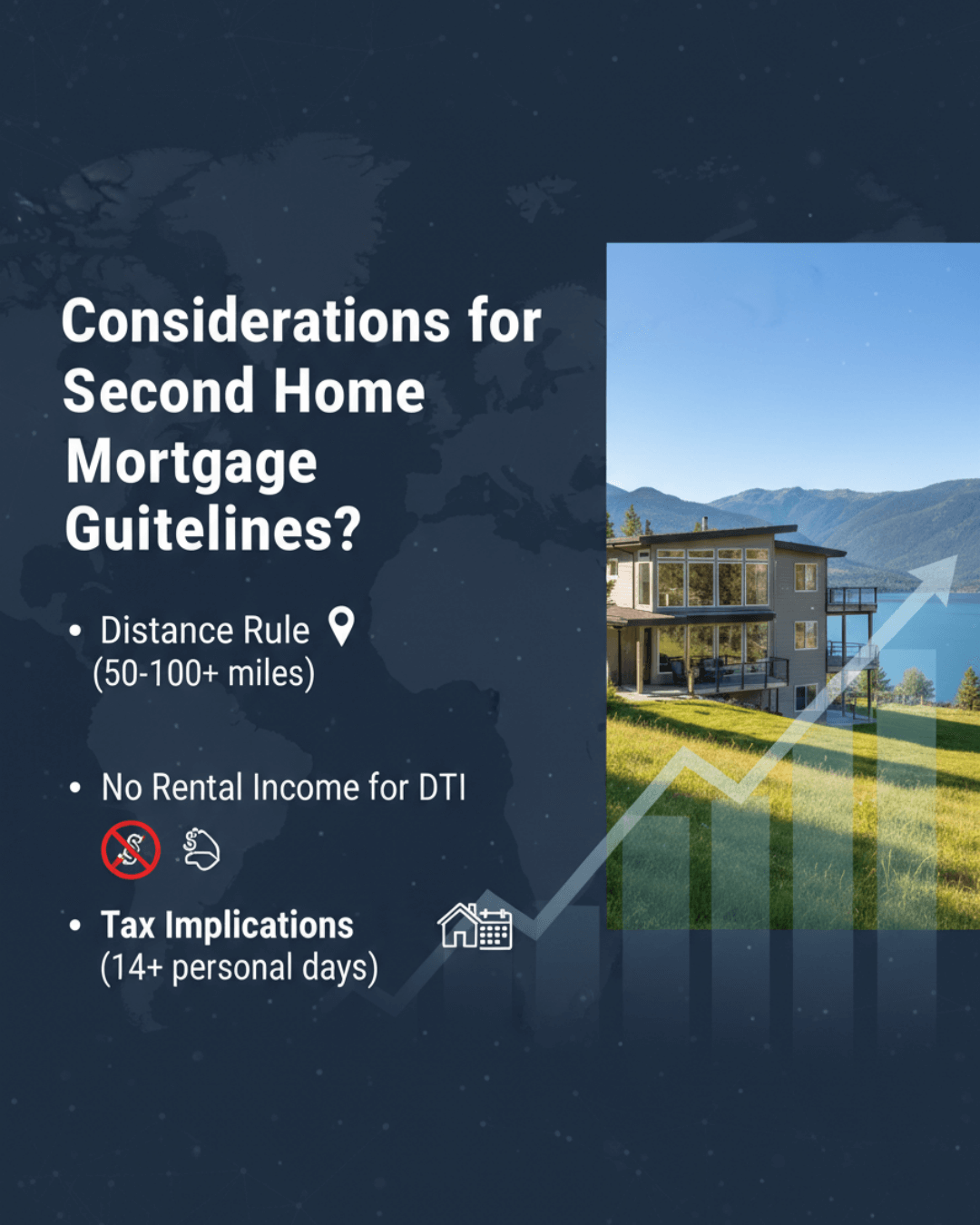

Considerations for Second Home Mortgages

Beyond the basic financial metrics, underwriters look closely at the "story" of the loan. If the scenario doesn't make logical sense, the file will get kicked back. Here are the critical underwriting hurdles to watch out for:

- The Distance Rule: Lenders often apply overlays requiring a minimum distance of 50 to 100 miles from the primary residence, though this is flexible for properties in resort or waterfront areas and focuses on logical personal use rather than a strict agency rule.

- No Rental Income for Qualifying: Unlike DSCR or investment loans, you cannot use potential short-term rental (Airbnb/VRBO) income to offset the DTI. The borrower must qualify carrying both housing expenses entirely on their standard income.

- Tax Implications: Borrowers often ask about tax deductions. While we aren't CPAs, it's worth noting that using the home for more than 14 days (or 10% of the days it's rented) affects its IRS classification.

Why You Should Check Second Home Mortgage Guidelines First?

Nothing kills your referral relationships faster than issuing a pre-approval, only to have the underwriter deny the file two weeks later because of a hidden reserve overlay or a distance rule violation. I always verify the exact second home mortgage guidelines before taking the application fee.

By checking the specific lender matrices upfront, you prevent late-stage denials, save your processor a massive headache, and deliver a smooth experience for your borrower. However, doing this manually is practically impossible today. With dozens of wholesale lenders constantly updating their policies, searching through clunky PDFs is soul-crushing. You need a smarter way to instantly query these rules.

How to Quickly Check Second Home Mortgage Guidelines?

This is exactly why I integrated Zeitro's Scenario AI into my daily workflow. It is an AI-powered mortgage guideline assistant designed specifically for loan officers, account executives, and underwriters. Currently covering nearly 300 guidelines from over top-tier lenders, it's built to handle both QM and the notoriously complex Non-QM landscape, including 8 dedicated second home matrices.

Instead of hitting Ctrl+F in a 200-page document, you simply ask the AI.

Here is why it has become an indispensable tool:

- High Accuracy with Citations: Scenario AI doesn't just guess. It pulls exact data and provides direct citations, allowing you to trace the answer back to the source document. No AI hallucinations, just hard facts.

- Unmatched Speed & Flexibility: Whether you have a vague eligibility question or a highly specific prequalify scenario, it instantly searches the vast guideline database and delivers precise answers in seconds.

- Advanced "Explain" Function: If a specific reserve requirement seems confusing, the "Explain" feature allows you to run a secondary deep-dive query on that specific scope for immediate clarification.

- Boost Efficiency & ROI: By integrating seamlessly with your LOS, it drastically reduces manual labor, speeds up your loan cycle, and ultimately boosts your bottom line.

- Cost-Effective: You can test it out with 3 free queries every single day, and the premium plans start at an incredibly low $8/month.

FAQs About Second Home Mortgage Guidelines

Can I use rental income to qualify for a second home mortgage?

Typically, no. This is the primary distinction between a second home and an investment property. The borrower must qualify for the loan using their own standard income streams, without relying on projected short-term or long-term rental income.

What is the distance requirement for a second home?

Historically, lenders looked for a 50 to 100-mile distance from the primary residence. Today, it's more about "logical sense." If it's a waterfront property or in a resort town, the distance rule can sometimes be waived, but it remains a key underwriting focus.

Are Non-QM loans available for second homes?

Absolutely. Many borrowers use Non-QM products like Bank Statement loans or Asset Utilization to finance vacation homes. Tools like Scenario AI can instantly show you which wholesale lenders offer the best terms for secondary properties.

How accurate is AI when checking mortgage guidelines?

Extremely accurate, provided you use an industry-specific tool. Scenario AI, for instance, provides direct citations and source links for every answer, ensuring your pre-approvals are based on verifiable, up-to-date lender data.

Can I try Scenario AI for free?

Yes. Zeitro offers 3 free queries per day, allowing loan officers and processors to test its accuracy on real loan scenarios before committing to the entry-level $8/month subscription.

Final Word

Structuring a second home mortgage requires absolute precision. Between the strict LTVs, reserve mandates, and occupancy logic, there is zero room for guesswork. A single missed overlay can derail a closing, costing you both commission and client trust.

As mortgage professionals, our time is best spent building relationships and originating loans, not acting as librarians for hundreds of ever-changing lender PDFs. Stop wasting hours doing manual research. I highly recommend heading over to Zeitro to register for your free account. Take advantage of your 3 free daily queries with Scenario AI today, and experience firsthand how fast and reliable guideline verification can actually be. Your pipeline will thank you.

People Also Read

- Mortgage Guidelines 2026: What Are They? How to Verify?

- Conventional Mortgage Guidelines: What and How to Check Quickly?

- Jumbo Mortgage Guidelines: Check Eligibility Quickly and Accurately

- VA Mortgage Guidelines: What Are They and How to Check Them Quickly?

- What Are FHA Mortgage Guidelines? How to Verify FHA & Overlays Quickly?