Written by

Eric

Share this article

.svg)

Subscribe to updates

I've lost count of how many times a deal has stalled because of a minor guideline nuance I missed during pre-approval. In our industry, speed is currency, but accuracy is survival. As Loan Officers and processors, we juggle massive PDF guides from Fannie Mae and Freddie Mac, not to mention the specific overlays from every wholesaler we work with.

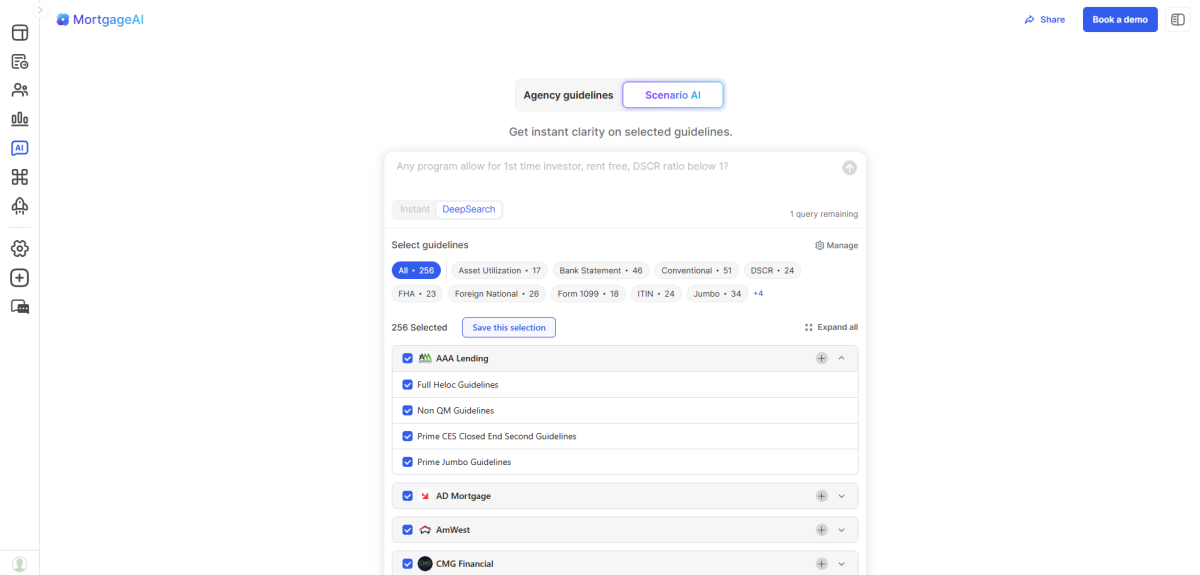

Scanning through thousands of pages to verify a DTI exception or a self-employment calculation is no longer efficient. This is where technology shifts the landscape. I've recently started utilizing Zeitro's Scenario AI, a specialized assistant that allows me to verify complex Conventional Mortgage Loan Guidelines via a simple chat interface. It streamlines the research process, ensuring I have the right answers before I even submit the file to underwriting.

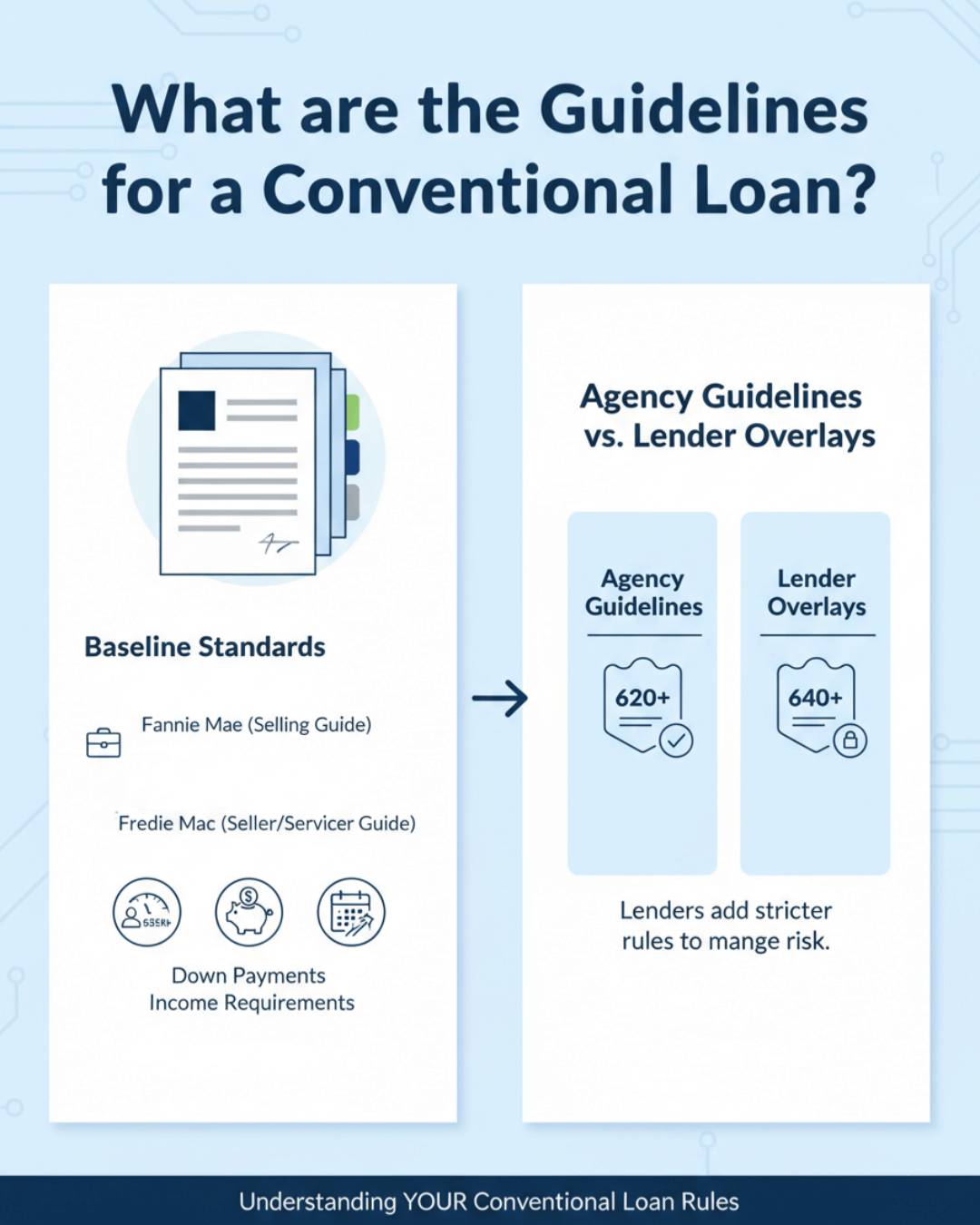

What are the Guidelines for a Conventional Loan?

A "conventional loan" is simply any mortgage that is not insured or guaranteed by the federal government (unlike FHA, VA, or USDA loans). However, just because the government doesn't back them doesn't mean they lack rules.

The baseline standards are established by the two Government-Sponsored Enterprises (GSEs):

- Fannie Mae (governed by its Selling Guide)

- Freddie Mac (governed by its Seller/Servicer Guide)

These agencies set the floor for credit scores, down payments, and income requirements. However, here is where many newer LOs get tripped up: The Agency Guidelines vs. Lender Overlays.

While Fannie Mae might accept a 620 credit score, a specific lender might require a 640 to buy that loan. This is called an "overlay." Understanding conventional guidelines means understanding both the agency rulebook and the stricter rules your specific lender might impose to manage their risk.

Who Do Conventional Mortgage Loan Guidelines Apply To?

These guidelines act as the rulebook for two distinct groups in the mortgage ecosystem.

The Borrowers

The rules shift dramatically based on occupancy and intent.

- Primary Residence: Offers the most lenient terms (lowest down payment, best rates).

- Second Home: Stricter reserves and down payment requirements.

- Investment Property: The most scrutiny. Guidelines here demand higher credit scores and significant equity (often 15-25% down).

Lenders and Underwriters

For my colleagues in underwriting, following these guidelines isn't optional, it's mandatory for the loan's salability. If an underwriter approves a loan that deviates from agency rules without a proper waiver, that loan becomes "unsalable" on the secondary market. This creates "repurchase risk," where the lender is forced to buy the bad loan back. This is exactly why lenders apply overlays, to create a safety buffer above the minimum agency requirements.

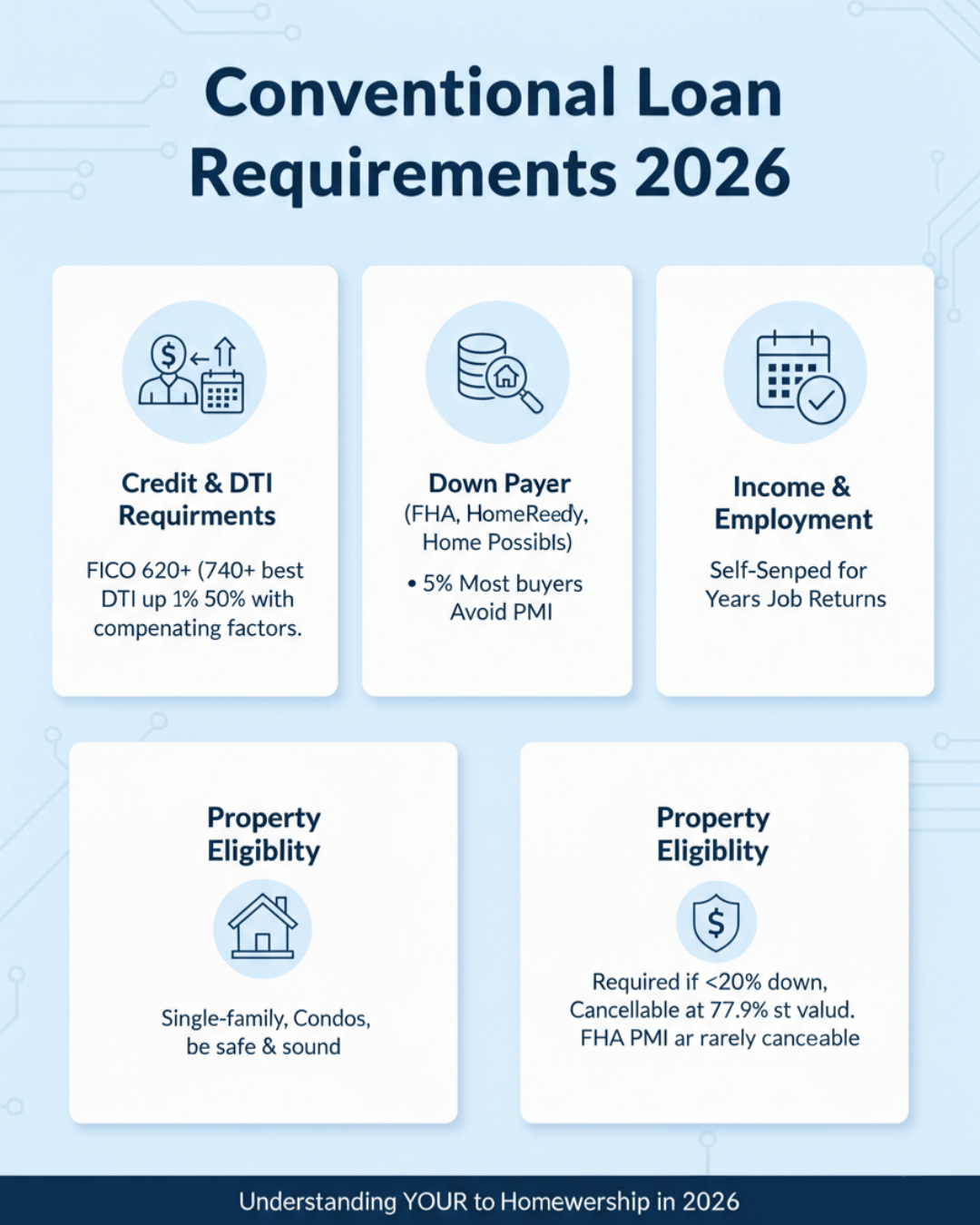

Conventional Loan Requirements 2026

As we navigate the market in 2026, the fundamentals of conventional lending remain anchored in risk assessment, though we are seeing slight adjustments in loan limits and automated verifications.

Credit Score Requirements

The minimum FICO score for most conventional loans is 620 (e.g., via DU Approve/Eligible for fixed-rate purchases), though manual underwriting and some products require 660+. However, purely hitting 620 doesn't guarantee a favorable approval.

Your borrower's credit score directly impacts the Loan-Level Price Adjustments (LLPAs), which determine the interest rate and the cost of Private Mortgage Insurance (PMI). While I have seen Desktop Underwriter (DU) approve scores slightly below 620 in rare cases with massive compensating factors, most lenders will not touch them due to overlays. For the best pricing and ease of underwriting, a score of 740+ is still the "gold standard" in 2026.

Debt-to-Income (DTI) Guidelines

The standard manual underwriting benchmark is 36% for housing ratios and 45% for total debt. However, in the real world, we rely heavily on the Automated Underwriting System (AUS).

If the rest of the file is strong, DU or LPA often return an "Approve/Eligible" finding with a DTI as high as 50%. To stretch to this upper limit, you usually need compensating factors. These are positive attributes that offset the risk of high debt, such as significant cash reserves (6+ months of payments), a long job history, or a large down payment. Without these, capping at 45% is the safe bet.

Down Payment Rules

One of the biggest myths I still bust daily is the "20% down" requirement. In 2026, the guidelines are quite flexible:

- 3% Down: Available for first-time homebuyers or those qualifying for programs like HomeReady or Home Possible.

- 5% Down: The standard minimum for most repeat buyers on primary residences.

- 20% Down: Not required for approval, but required to avoid Private Mortgage Insurance (PMI).

For multi-unit properties (2-4 units), the minimum down payment jumps significantly (often 15-25%), so always double-check the specific matrix for those scenarios.

Income and Employment Verification

Consistency is king. Underwriters are looking for a two-year history of stable income.

- W-2 Employees: Generally straightforward, requiring recent pay stubs and W-2s.

- Self-Employed: This is where deals often die. Both agencies require two years of personal and business tax returns. One year is rarely accepted, even via LPA, without exceptional compensating factors.

The logic here is stability. If a borrower has a history of gaps in employment or declining income year-over-year, the guidelines require a deeper explanation or disqualification, regardless of how much money they made last month.

Property Eligibility Guidelines

Not every roof and four walls qualifies for a conventional mortgage.

- Eligible: Single-family homes, PUDs, warrantable condos, and 2-4 unit properties.

- Ineligible: Timeshares, houseboats, condo-hotels, or properties with major health and safety violations (e.g., mold, structural damage).

I always remind clients that the appraisal isn't just about value. It's about the property's condition. If a home is deemed "unsafe or unsound," conventional guidelines mandate that repairs be completed before closing.

Mortgage Insurance (PMI) Guidelines

If your borrower puts down less than 20%, they must carry Private Mortgage Insurance (PMI). This protects the lender, not the borrower.

The crucial advantage of Conventional loans over FHA is that PMI is temporary. Once the loan-to-value (LTV) ratio drops to 77.9% (automatically) or 80% (by borrower request with appraisal), PMI can be removed. In contrast, FHA MIP is cancelable after 11 years for most loans with LTV ≤90%, though upfront and annual premiums apply. This exit strategy makes conventional loans far more attractive for borrowers with good credit.

How to Verify Conventional Mortgage Guidelines Quickly?

In a perfect world, we would all have the Fannie Mae Selling Guide memorized. In reality, guidelines change, and referencing them manually is a massive time sink.

This is why I've integrated Zeitro's Scenario AI into my workflow. It is an AI-powered mortgage guideline assistant specifically designed for QM and Non-QM verifications. Rather than digging through PDF overlays from 15 different investors, I can simply ask the chat interface a specific question.

Why I find it indispensable:

- Handling Complexity: I can ask vague questions like "Can I use rental income from a departing residence?" or specific ones about LTV limits.

- Citations & Trust: As pros, we can't just trust a robot. Zeitro provides citations for its answers. It links back to the source material so I can verify the data myself. This is critical for E-E-A-T and compliance.

- Coverage: It covers nearly 300 guidelines, including 57 Conventional guides and major lenders like Freedom Mortgage and AD Mortgage.

- Speed: It scans these documents in seconds.

If an answer is unclear, the Explain feature lets me dig deeper without starting over. For roughly $8 a month, it saves me hours of "ctrl+f" searching and reduces the human error of missing a recent overlay update.

FAQs About Conventional Mortgage Guidelines

Q1. What does a conventional mortgage mean?

It means the loan is funded by a private lender and sold to Fannie Mae or Freddie Mac, without government insurance (like FHA or VA).

Q2. Do all conventional mortgages require 20% down?

No. First-time buyers can put down as little as 3%, and repeat buyers can put down 5%. 20% is only required to avoid PMI.

Q3. What are the qualifications for a conventional mortgage?

Generally, you need a credit score of at least 620, a verifiable two-year income history, and a Debt-to-Income (DTI) ratio under 45% (sometimes up to 50% with AUS approval).

Q4. What disqualifies a home from a conventional loan?

Properties with significant structural issues, safety hazards, or "non-warrantable" condo features (like operating as a hotel) will be disqualified.

Q5. Are conventional mortgage guidelines the same for all lenders?

No. While the base rules are the same, lenders add "overlays." One lender might accept a 620 score, while another requires 640 for the same loan program.

Q6. Can conventional guidelines change year to year?

Yes. Loan limits (the maximum amount you can borrow) usually increase annually, and underwriting rules regarding credit or income calculation can change based on economic conditions.

Q7. How do lender overlays affect conventional loan approval?

Overlays make approval harder. Even if you meet Fannie Mae's minimums, you must also meet the stricter specific rules of the bank lending you the money.

Q8. What is the difference between FHA and conventional guidelines?

FHA is more lenient on credit scores (down to 580) and high DTI, but requires permanent mortgage insurance. Conventional requires better credit but offers lower costs and cancelable PMI.

Conclusion

Navigating conventional mortgage guidelines is not about memorizing every rule. It's about knowing where to find the right information fast. Remember, Guidelines ≠ Guaranteed Approval. A borrower might look good on paper but fail due to a specific lender overlay or a property issue.

To reduce the trial-and-error and prevent awkward denials days before closing, you need to verify rules upfront. I highly recommend trying Zeitro's Scenario AI. It allows you to check specific scenarios against hundreds of lender guidelines instantly. With free daily queries and a low entry cost, it's a high-ROI tool for any serious Loan Officer. Don't guess—verify.

People Also Read

- What Are FHA Mortgage Guidelines? How to Verify FHA & Overlays Quickly?

- Jumbo Mortgage Guidelines: Check Eligibility Quickly and Accurately

- Best Mortgage Loan Officer Training in 2026: Which to Pick?

- 6 Best Mortgage CRM for Brokers, Lenders, MLOs

- Best NMLS Test Prep Course 2026: Which to Choose from?

- Should Mortgage Lender and Broker Build In-House AI Tools?

- Mortgage Guidelines 2026: What Are They? How to Verify?