Written by

Eric

Share this article

.svg)

Subscribe to updates

If you are reading this, you are likely a mortgage executive or brokerage owner facing a massive decision. You feel the pressure, the Fear Of Missing Out (FOMO), gnawing at you. You see competitors leveraging automation, and your instinct says, "We need to own this technology. We need to build our own AI".

I have sat in those boardrooms. I understand the allure of owning your intellectual property. But before you sign off on a multimillion-dollar R&D budget, we need to have a brutally honest conversation. For 99% of lenders and brokers, attempting to build a proprietary AI engine in-house is not just a headache. It is a strategic trap that leads to wasted capital and "zombie" projects.

The State of Mortgage AI in 2026: Efficiency & Speed

To understand why building is so risky, you first need to understand the standard that has already been set by specialized SaaS providers. In 2026, AI isn't just a chatbot on your website. It is the engine room of the loan origination process.

Take Zeitro as a prime example of the current market benchmark. This isn't a theoretical tool. It is a specialized AI SaaS platform built specifically for US Loan Officers (LOs) and brokers. The efficiency metrics they are delivering right now are staggering:

- 2.5x faster pre-qualifications.

- Elimination of 100% of manual guideline lookup work.

- Saving 7+ hours per loan file.

- Increasing loan closes by 30%.

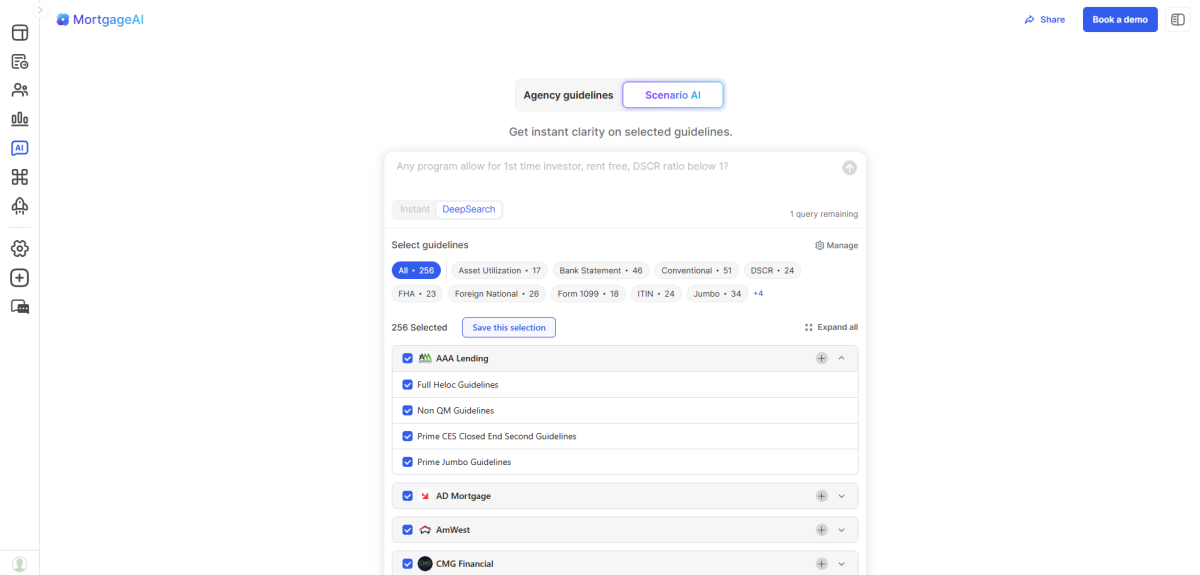

Their flagship feature, Scenario AI, essentially functions as a super-underwriter. It supports both QM and Non-QM loans, allowing LOs to ask vague or complex questions and get instant, citation-backed answers from Fannie Mae, Freddie Mac, VA, and niche lender guidelines.

Here is the reality check: Building a tool like Scenario AI took a dedicated team of experts over six months of rigorous development, data cleaning, and testing. It involved ingesting thousands of PDF pages and fine-tuning models to avoid hallucinations. Do you truly have the time to pause your business operations for half a year to replicate what already exists?

6 Strategic Risks of Building In-House Mortgage AI

If you are still tempted to hire a dev team and build your own "Proprietary Underwriting Bot," you need to consider the six major hurdles that kill most internal AI projects before they ever process a single loan.

- Insufficient AI Expertise and Production Readiness

There is a massive difference between building a prototype that works on a laptop and a scalable system that works for your entire branch network. Most lenders are experts in risk assessment, not MLOps (Machine Learning Operations).

The biggest silent killer of these projects is data quality. As a lender, you have data, but it is likely "messy", such as unstructured PDFs, email threads, and siloed CRM notes. According to recent industry observations and echoed by Gartner, a lack of "AI-ready data" is the primary reason AI projects fail. Without a team of data engineers to clean and structure this information 24/7, your expensive AI model will simply output garbage. You risk building a tool that gives your LOs wrong guideline advice—a compliance nightmare.

- High AI Talent Costs and Hiring Barriers

Let's talk numbers. You cannot build a competitive AI tool with just one "IT guy". To build something comparable to Zeitro, you would need a full squad: 2–5 Machine Learning Engineers, 1–3 Data Scientists, plus Backend Developers and a Product Manager.

In the US market, this talent is incredibly expensive. Data from platforms like Glassdoor and Levels.fyi shows that ML Engineers command salaries significantly higher than traditional software developers, often exceeding $600k per year per person. When you factor in benefits and overhead, a "Minimum Viable Product" (MVP) team could easily cost $1 million to $2 million annually. Compare that to the cost of a SaaS subscription, and the math starts to look terrifying.

- Weak ROI from Limited Scale and Ongoing Maintenance

This is a lesson in unit economics. A SaaS company like Zeitro spreads its development costs across thousands of users. If they spend $5 million on R&D, it costs you pennies. If you build in-house, 100% of that cost sits on your P&L.

Furthermore, AI is not a "set it and forget it" asset. Models suffer from "drift". They degrade over time as the world changes. You need a permanent team to monitor performance, retrain models, and fix bugs. This creates "Technical Debt". As noted in AWS MLOps frameworks, the initial code is just the tip of the iceberg. The massive bulk of the work is ongoing maintenance. For a mid-sized lender, the ROI simply isn't there because you don't have the user volume to justify the perpetual expense.

- High Talent Churn in a Competitive AI Market

Even if you have the budget to hire a genius AI Lead, can you keep them? In 2026, you aren't just competing with other lenders for talent. You are competing with Google, Meta, and high-frequency trading firms.

Reports from financial news outlets like FNLondon have highlighted that hedge funds and tech giants are offering astronomical packages to poach top AI engineers. If your lead engineer leaves six months into the project for a double-salary offer, your project dies. You are left with "zombie code" that no one at your company understands how to fix or update. This continuity risk is a danger most mortgage CEOs underestimate.

- Rapid AI Innovation and Model Obsolescence Risk

The speed of AI evolution is blinding. New Large Language Models (LLMs) and architectures are released every few months. Dedicated AI companies pivot instantly to integrate these advancements.

If you build in-house, your team will likely spend a year building on "last year's technology". By the time you launch, your tool is already obsolete compared to what's available on the open market. According to Gartner surveys on GenAI deployment, organizations that "buy" or partner are finding value much faster than those trying to build foundational models themselves. You don't want to be the company holding the bag on a legacy system that can't keep up with the latest Non-QM guideline updates.

- High Failure Rates from Pilot to Production

Finally, we must look at the statistics. The failure rate for taking AI projects from "Pilot" (testing) to "Production" (real-world use) is notoriously high. It takes an average time of 8.6 months to develop from prototype to production, but only 53% succeeds in mature organizations.

Many in-house tools get stuck in "Pilot Purgatory". They work great in a controlled demo, but when real LOs try to use them for complex, messy loan scenarios, the tool breaks or hallucinates. For a SaaS provider, a failed feature is a bad quarter. For a lender, a failed $2M internal project is a disaster that can cost executives their jobs.

When Does Building In-House Actually Make Sense?

To be fair, there is a 1% exception. Building in-house might be justified if you meet a very strict set of criteria:

- Massive Scale: You are a top 5 national lender processing volumes that justify a permanent, multi-million dollar R&D department.

- Proprietary Data Advantage: You possess unique, proprietary data that no competitor has, which gives you an edge beyond standard agency guidelines.

- Mature Governance: You already have a mature Data Governance and MLOps structure in place.

If you cannot check all three of these boxes, the building is vanity, not strategy.

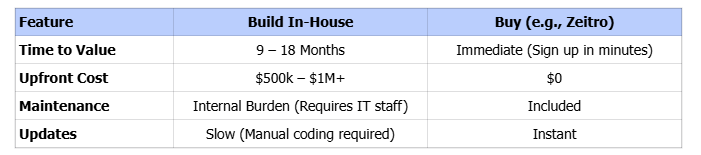

Build vs. Buy: The Mortgage AI Cost-Benefit Analysis

Let's look at the direct comparison.

Conclusion

In the mortgage business, your competitive advantage comes from your relationships, your service speed, and your ability to close tough deals. It does not come from being a mediocre software development shop.

The risks of building in-house, like runaway costs, talent churn, and technical obsolescence, are simply too high. Instead of distracting your leadership team with software engineering problems, leverage specialized partners like Zeitro. They have absorbed the R&D risk, so you don't have to.

Smart lenders aren't the ones building the AI. They are the ones adopting it fastest. Save your capital, protect your margins, and let the experts handle the code while you handle the loans.

People Also Read

- 6 Best Mortgage CRM for Brokers, Lenders, MLOs

- Best Mortgage Companies for New Loan Officers

- Best NMLS Test Prep Course: Which to Choose from?

- What Are FHA Mortgage Guidelines? How to Verify FHA & Overlays Quickly?

- Guide: What is NMLS? Definitions, FAQs, More