Written by

Eric

Share this article

.svg)

Subscribe to updates

We have all been there. You have a borrower who fits the FHA box on paper—580 credit score, steady job, ready to buy. But then you submit the file, and the underwriter kicks it back because of a specific "lender overlay" you missed in the fine print. It's frustrating, time-consuming, and frankly, it kills deals.

In 2026, the volume of guidelines we have to navigate is overwhelming. Between the massive HUD Handbook 4000.1 and the individual rulebooks of every wholesaler, manually verifying eligibility is becoming impossible. That is why I started using Zeitro's Scenario AI. It acts like a digital underwriting assistant, allowing me to verify FHA guidelines and specific lender overlays through a simple chat interface. It turns hours of PDF searching into seconds of verification.

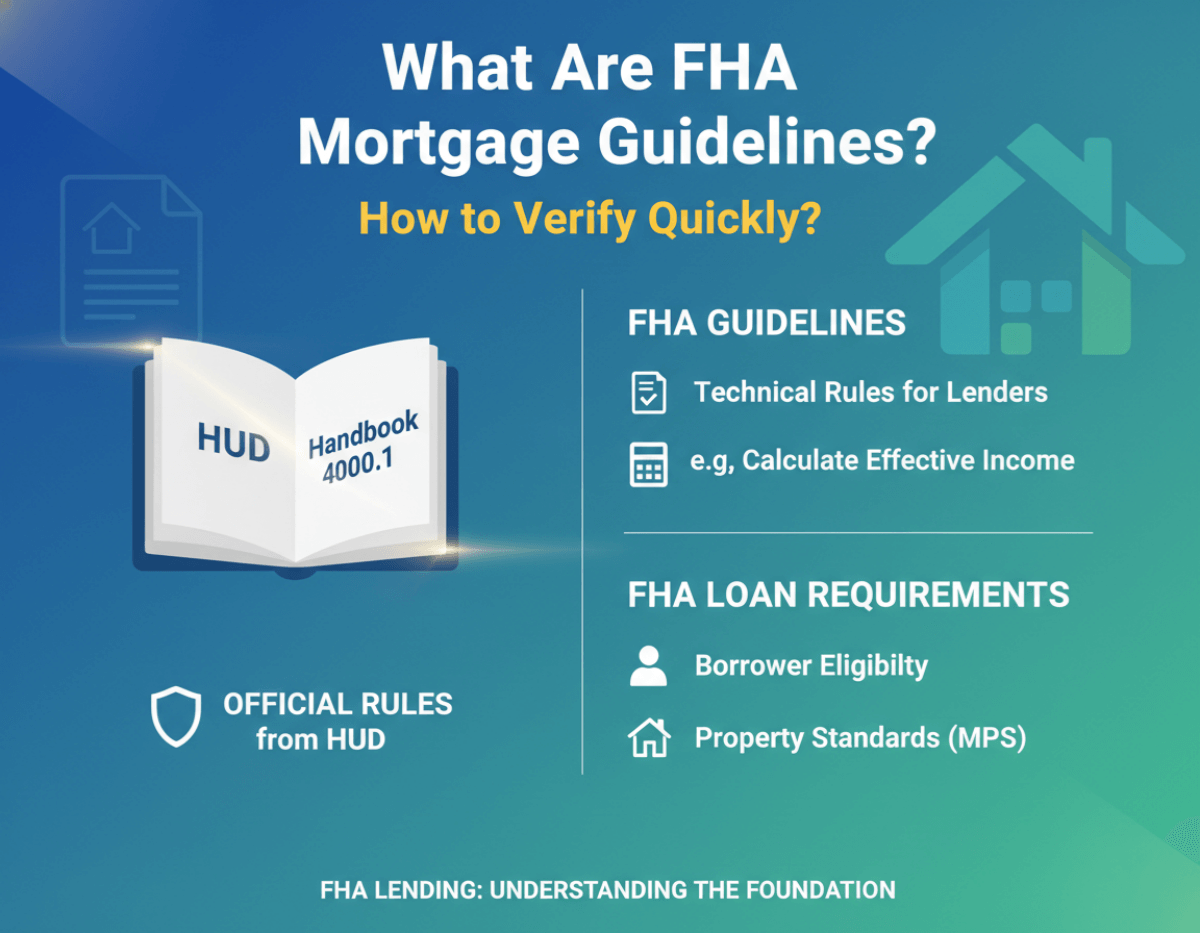

What Are FHA Mortgage Guidelines?

To navigate this landscape, we first need to respect the source. FHA Mortgage Guidelines are the official rules set forth by the Department of Housing and Urban Development (HUD). These are the "Constitution" of FHA lending, primarily housed in the HUD Handbook 4000.1 (Single Family Housing Policy Handbook).

These guidelines dictate the minimum standards for a loan to be insured by the federal government. They cover everything from borrower creditworthiness to property safety standards (Minimum Property Standards or MPS).

The Critical Distinction: It is vital for us as professionals to distinguish between "FHA Guidelines" and "FHA Loan Requirements."

- FHA Guidelines: The official, technical rules written by HUD for lenders (e.g., how to calculate effective income).

- FHA Loan Requirements: The tangible targets a borrower sees (e.g., "I need a 3.5% down payment").

While consumers focus on the requirements, our job as Loan Officers (LOs) and Processors is to master the guidelines that dictate how those requirements are met.

Who Do FHA Guidelines Apply To?

Many clients assume these rules are just for them, but we know the reality is much broader. The guidelines create a chain of liability that affects every professional touching the file:

- Lenders (Mortgagees): Specifically, Direct Endorsement (DE) lenders. They must ensure every file meets HUD standards to maintain their insurance endorsement. If they fail, they face indemnification requests.

- Underwriters: They are the gatekeepers. They must sign off that the borrower's income, assets, and credit history align strictly with Handbook 4000.1.

- Appraisers: They aren't just valuing the home. They are inspecting it for health and safety issues as defined by HUD.

- Mortgage Brokers: We are the front line. We must structure the deal correctly from day one so it survives the underwriting scrub.

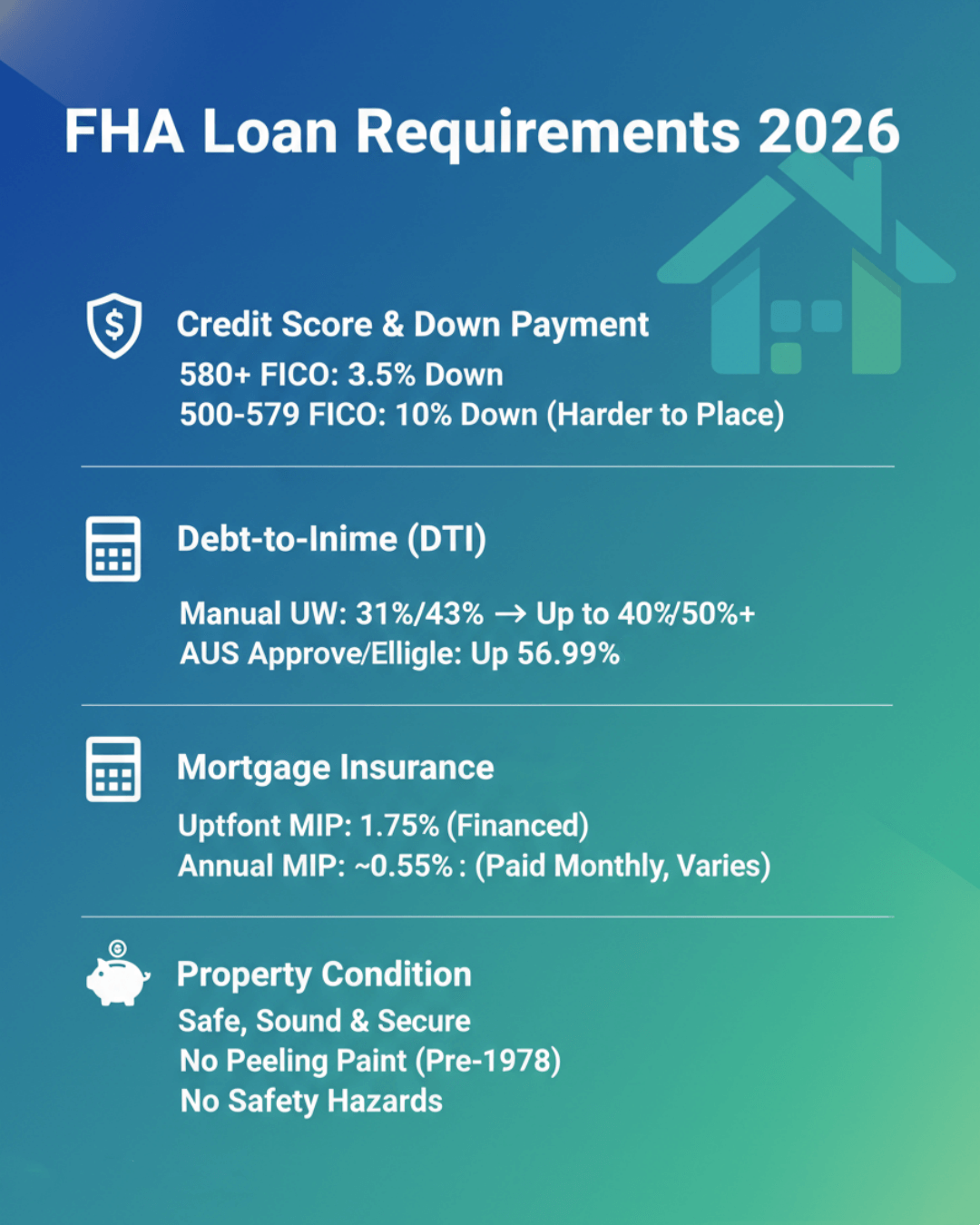

FHA Loan Requirements 2026

For 2026, the baseline requirements remain accessible, but we are seeing stricter scrutiny on income stability. Here is the current snapshot you need to know for your files:

Credit Score & Down Payment:

- 580+ FICO: Eligible for maximum financing (3.5% down payment).

- 500–579 FICO: Requires a 10% down payment (Harder to place due to overlays).

Debt-to-Income (DTI) Ratios: The standard manual underwriting benchmark is 31%/43% (front-end/back-end) with no compensating factors. Limits increase to 37%/47% (one factor) or 40%/50% (two+ factors). With AUS Approve/Eligible, total DTI can reach up to 56.99% even without manual comp factors.

Mortgage Insurance (MIP):

- Upfront MIP: 1.75% of the loan amount (can be financed).

- Annual MIP: Typically 0.55% for loans ≤ $726,200 with LTV >95% (>15-year term), but varies (e.g., 0.50% for 90.01-95% LTV, 0.15%-0.75% overall by LTV/term/amount), paid monthly.

Property Condition: The home must be safe, sound, and secure. Peeling paint (pre-1978) or safety hazards are deal-breakers until fixed.

Also Read: How to Check Mortgage Eligibility? Quick and Accurate with Sources

Why FHA Guidelines Are Often Confusing?

If the HUD Handbook is the "Constitution," then Lender Overlays are the local laws that confuse everyone. This is the single biggest pain point in our industry.

HUD might say a 580 credit score is acceptable. However, Lender A might require a 620, while Lender B demands a 640. These are "overlays"—additional rules imposed by lenders to minimize their risk.

This creates a chaotic environment where a borrower is "FHA Eligible" per the government, but "Ineligible" per the specific investor you are trying to sell the loan to. You aren't just memorizing one rulebook. You are juggling the invisible rules of dozens of different investors.

How Professionals Verify FHA Guidelines Efficiently?

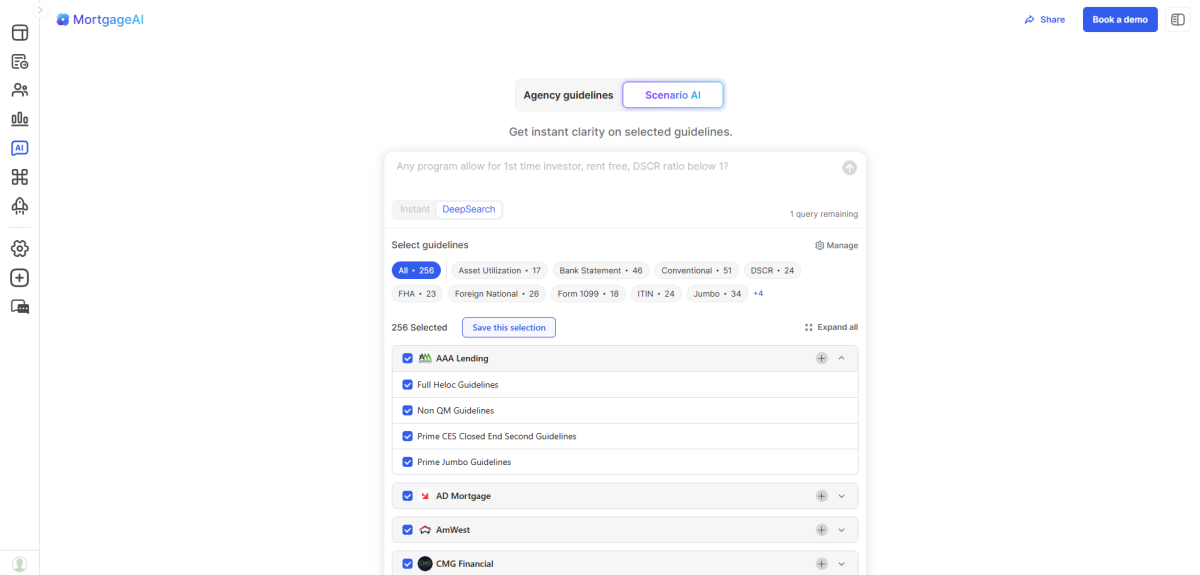

This is where technology has finally caught up to our needs. I used to spend hours Ctrl+F searching through PDFs to find which lender would accept a specific credit event. Now, I use Zeitro's Scenario AI.

Scenario AI is a specialized Mortgage Guideline Assistant built for LOs and Underwriters. It doesn't just search the web. It searches a curated database of nearly 300 guidelines (including 42 specific FHA guidelines and 256 total QM/Non-QM rulebooks).

Here is why it has become my daily driver:

- Deep Lender Coverage: It covers guidelines from over 15 mainstream lenders like Freedom Mortgage, AD Mortgage, and Nations Direct. If I have a tricky FHA file, I can verify it against multiple investors simultaneously.

- Accuracy with Citations: In our business, "I think so" isn't good enough. When I ask Scenario AI a question, it provides the answer and cites the specific source (e.g., "Page 42 of AD Mortgage FHA Matrix"). This gives me the confidence to quote guidelines to my processors.

- Complex Scenario Analysis: I can ask vague questions like, "Can I use 12 months bank statements for income on an FHA loan with a 580 score?" or specific ones about DTI caps. The AI parses the logic and gives a precise answer in seconds.

- The "Explain" Feature: Sometimes a guideline is technically "correct" but practically confusing. I use the Explain feature to get a secondary breakdown of the rule, ensuring I understand the why behind the no.

At roughly $8/month, the ROI is undeniable. It saves me at least 3-4 hours of research a week.

FAQs About FHA Mortgage Guidelines

Q1. Can FHA guidelines change year to year?

Yes. HUD issues Mortgagee Letters throughout the year that update or supersede sections of the 4000.1 Handbook. For example, recent updates in 2025/2026 adjusted how we calculate self-employment income add-backs.

Q2. Are FHA guidelines the same for every lender?

No. As mentioned, lenders apply overlays. While the core FHA insurance rules are universal, the credit score, DTI, and property standards can vary significantly from one lender to the next.

Q3. Can I qualify for FHA with past bankruptcy?

Yes. The standard waiting period is 2 years after a Chapter 7 discharge date (1 year with extenuating circumstances). For Chapter 13, 1 year of successful payout performance with court/trustee approval, or 2 years from discharge. However, you must have re-established good credit and have a clean payment history since the event.

Q4. What disqualifies you from an FHA?

The most common disqualifiers are CAIVRS hits (delinquency on federal debt like student loans), recent foreclosures (under 3 years), or property conditions that fail the safety/sanitary check.

Q5. Is it hard to get approved for FHA?

Generally, no. FHA is often more forgiving than Conventional loans regarding credit events and DTI. The "difficulty" usually comes from the stricter property appraisal and the documentation required for income.

Final Thoughts

FHA loans remain the bedrock of the American housing market, but for us as originators, the complexity of verifying guidelines across different lenders is a constant hurdle. The difference between a funded loan and a denial often comes down to knowing which investor allows that one specific exception.

We need to move away from manual research and embrace tools that offer speed and precision. Zeitro's Scenario AI has bridged that gap for me, handling everything from standard FHA questions to complex Non-QM scenarios. If you want to stop guessing and start verifying with confidence, I highly recommend giving it a try. You can even test it out with 3 free queries per day to see how much time it saves you.

Work smarter, not harder.

People Also Read

- 8 Best Mortgage Lead Generation Companies: Don't Miss

- [Tips] Where to Buy Mortgage Leads? Warm Leads for LOs

- Best CRM for Loan Officers: Which One Suits You Most?

- Beginner's Guide: How to Get Leads for Mortgage Loans?

- Best Mortgage Companies for New Loan Officers

- Mortgage Guidelines 2026: What Are They? How to Verify?