Written by

Eric

Share this article

.svg)

Subscribe to updates

If you are anything like me, your desk or your desktop is often a battlefield. I remember the panic of staring at a stack of 1003s, realizing I'd forgotten to call a hot lead back because I was too busy digging through a 500-page FHA guideline PDF for a different client.

It's a sinking feeling. In this industry, organization isn't just about being tidy. It's about survival. You cannot scale a loan business in 2026 using sticky notes and Excel spreadsheets. I've tested the s, felt the frustrations, and found the solutions. Here is how to find the digital partner that will actually help you close more some of the best CRM for loan officers, felt the frustrations, and found the solutions. Here is how to find the digital partner that will actually help you close more deals.

People Also Read

- [Tips] Where to Buy Mortgage Leads? Warm Leads for LOs

- 6 Best Loan Origination Software for LOs/Brokers in 2026

- 8 Best Mortgage Lead Generation Companies in 2026: Don't Miss

- [Proven] How to Generate Mortgage Leads for Free? 6 Methods

- 11 Best Loan Officer Schools for Newbies: Online & Local

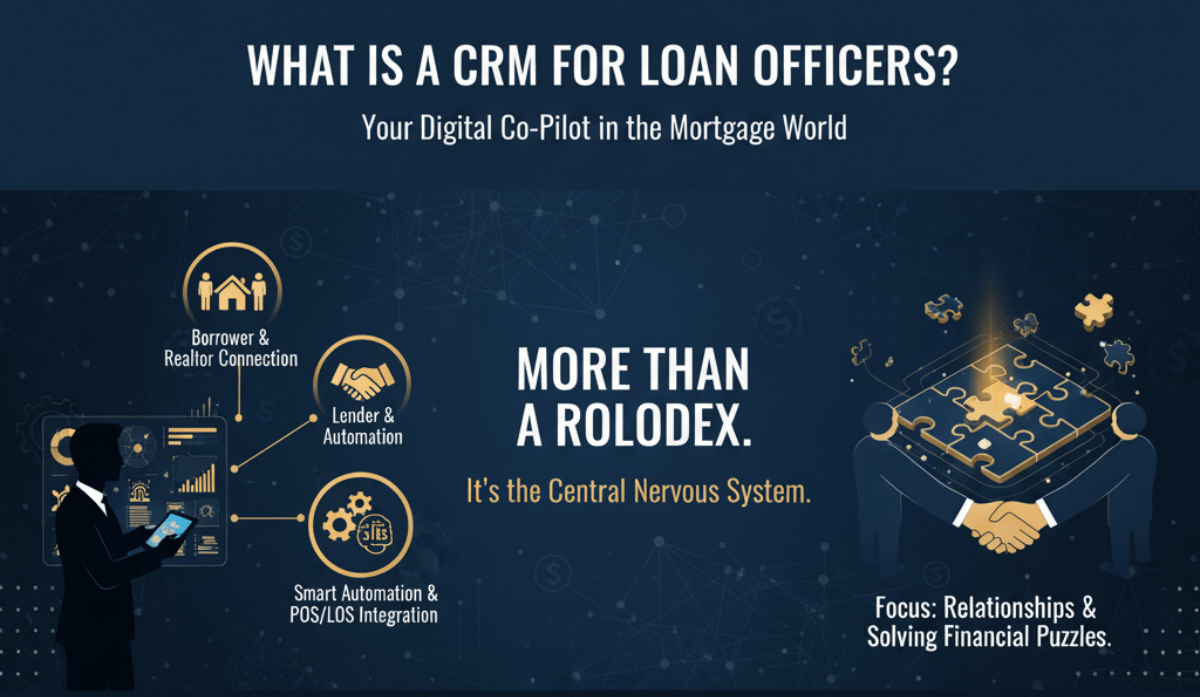

What is a CRM for Loan Officers?

In the mortgage world, "CRM" (Customer Relationship Management) has evolved. It is no longer just a digital Rolodex to store names and phone numbers. Today, the best platforms act as your digital co-pilot. They blur the lines between a CRM, a Point-of-Sale (POS), and a Loan Origination System (LOS).

For us Loan Officers, whether you are an independent broker or part of a large retail bank, these tools are the central nervous system of your business. They connect the borrower, the realtor, and the lender, automating the "busy work" so you can focus on what actually pays the bills: building relationships and solving complex financial puzzles.

Benefits of Using the Best CRM for Loan Officers

Why should you invest your hard-earned commission into sophisticated software? Simply put, manual processes are the enemy of growth. Here is why upgrading your tech stack is non-negotiable this year:

- Automated Lead Nurturing: You stop losing leads to the cracks. Automated drip campaigns keep you top-of-mind without you lifting a finger.

- Faster Loan Processing: By streamlining data collection, you can significantly shorten the "application-to-clear-to-close" timeline.

- AI-Powered Efficiency: This is the big one for 2026. Tools like Zeitro allow you to calculate income and check guidelines instantly, removing human error.

- Enhanced Compliance: With regulations like TCPA and RESPA constantly looming, a good system automatically logs communications and ensures you stay compliant.

- Better Borrower Experience: Clients expect a seamless, Amazon-like digital experience. A modern CRM/POS delivers that, boosting your referral rates.

- Centralized Data: Stop chasing emails. All documents and conversations live in one secure place.

8 Best CRM for Loan Officers in 2026

The market is flooded with software, but only a few are truly worth your time. Let's dive into the best mortgage CRM that are reshaping the mortgage industry this year.

#1 Zeitro

Best for: AI-Powered Workflow & Complex Scenarios

Zeitro is not just a CRM. It is arguably the smartest AI SaaS platform specifically engineered for US Loan Officers and Brokers. While most CRMs focus on managing contacts, Zeitro focuses on doing the work. I've found that the biggest bottleneck in our day is often researching guidelines and calculating income. Zeitro tackles this head-on.

Highlights:

- Scenario AI & DeepSearch: This is a game-changer. You can ask complex lending questions (FHA, VA, Non-QM) in plain English. The "DeepSearch" mode cuts through thousands of guideline pages to give you instant, source-backed answers, eliminating hours of manual research.

- Massive Time Savings: Data shows it can save professionals 7+ hours per loan file. Imagine what you could do with an extra 7 hours per deal.

- Speed to Lead: It is designed to deliver 2.5x faster pre-qualifications, which is critical when a borrower is making an offer in a competitive market.

- AI Tools Suite: It achieves 85%+ accuracy in AI-powered income calculation and automates document review and condition collection.

- Pricing Engine: A built-in engine covers all loan types (Conventional, Jumbo, DSCR, Hard Money), allowing you to quote fast.

- Conversion Boost: By reducing friction, users see a 90%+ application completion rate and close 30% more loans.

#2 Floify

Best for: A Superior Point-of-Sale (POS) Experience

If your main pain point is chasing borrowers for documents or dealing with clunky applications, Floify is the industry standard for a reason. It is a digital mortgage automation solution that makes you look incredibly professional to your clients.

Highlights:

- Streamlined 1003: They utilize an "interview-style" application that guides borrowers through the 1003 form painlessly, reducing incomplete apps.

- Dual AUS Integration: You can run Fannie Mae's Desktop Originator® (DO®) and Freddie Mac's Loan Product Advisor® (LPA℠) side-by-side to compare findings instantly.

- Dynamic Apps: You can customize the loan application flow based on the specific loan scenario, so borrowers aren't asked irrelevant questions.

- Automated Document Needs: The system automatically requests, collects, and organizes documents, sending reminders so you don't have to be the "bad guy."

- Massive Integrations: It connects seamlessly with over 50 platforms, including major credit reporting agencies, pricing engines, and other LOS.

#3 Jungo

Best for: Salesforce Power Users

If you believe in the power of Salesforce but hate the headache of customizing it, Jungo is your answer. It is a mortgage-specific layer built on top of the Salesforce ecosystem.

Highlights:

- The Salesforce Engine: You get the enterprise-grade security and data management of Salesforce, pre-configured for mortgage workflows.

- Reffinity (Referral Management): This feature is brilliant for keeping your Realtors happy. It tracks referrals and automates pipeline reports sent back to your partners.

- Concierge Program: It automates post-closing gifts and cards. This "set it and forget it" feature is amazing for long-term client retention.

- PrintPub Marketing: You can create co-branded flyers and postcards directly within the CRM, which is a huge value-add for your real estate agents.

- Multi-Channel Reach: It integrates SMS and video messaging (like BombBomb) directly into the contact record for higher engagement.

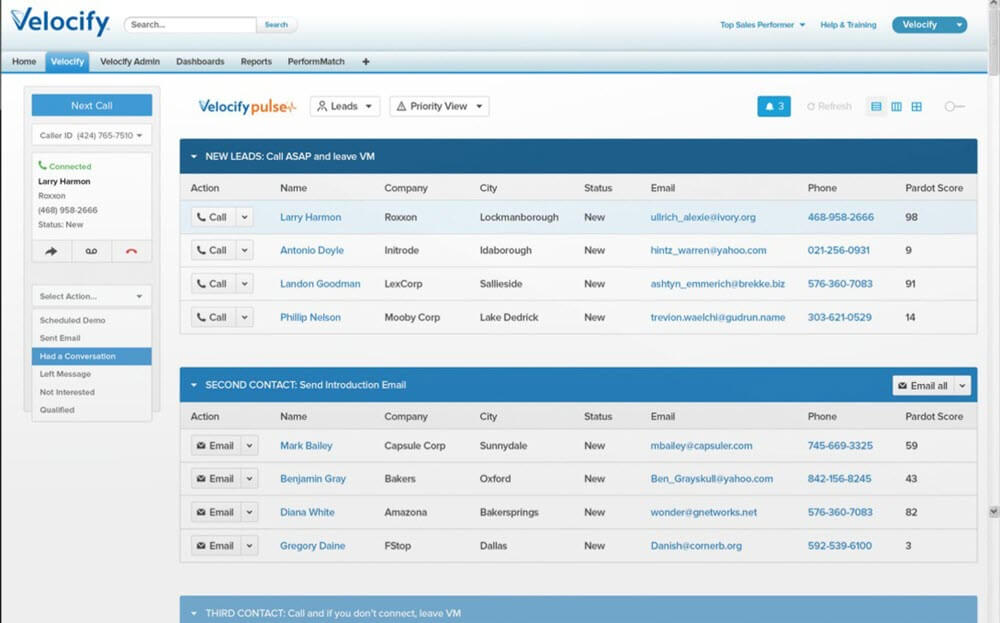

#4 Velocify

Best for: High-Volume Lead Management

Now part of ICE Mortgage Technology, Velocify is all about speed and volume. If you are running a shop that buys internet leads or handles a massive inflow of inquiries, this is the tool to enforce discipline.

Highlights:

- Sales Process Enforcement: It ensures every LO follows the exact same contact strategy, so no lead is ever "cherry-picked" or ignored.

- Dial-IQ: This integrated dialer helps LOs power through call lists, aimed at driving actionable conversations rather than just voicemails.

- High Conversion: Their methodology claims to increase lead conversion rates by up to 400% by optimizing exactly when and how you follow up.

- Encompass Integration: Since it is owned by ICE, the data flow into the Encompass LOS is tighter than almost any other third-party CRM.

- Lead Distribution: It automatically routes leads to the most available or qualified LO instantly, ensuring "speed to lead."

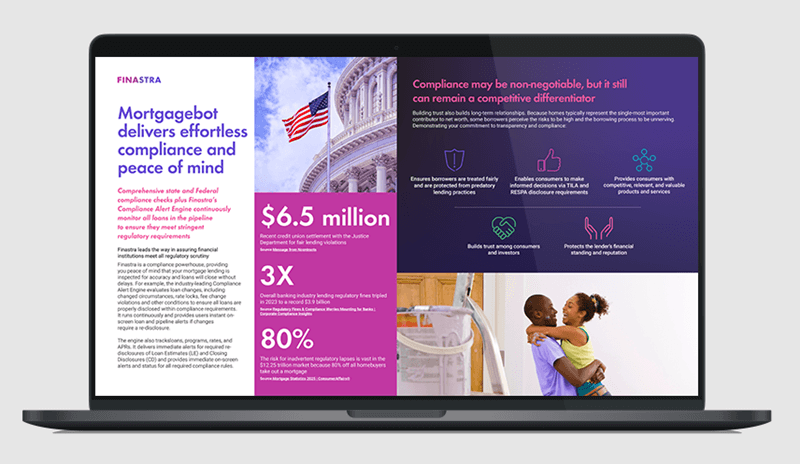

#5 MortgageBot

Best for: End-to-End Origination

Finastra's MortgageBot is a powerhouse for those who want an all-in-one solution. It combines the consumer-facing application with the back-office processing in a unified cloud environment.

Highlights:

- Cloud-Native Platform: Being fully web-based means you can access the entire origination system from anywhere, without clunky VPNs.

- Direct Integration: Because the POS (Originate) and LOS are one system, there is zero data loss or syncing delay between the borrower and the back office.

- Efficiency Gains: Users report up to a 40% faster application process compared to manual methods.

- Compliance Tools: It has robust, built-in compliance checks for State and Federal regulations, which provides significant peace of mind.

- Broad Support: It handles Retail, Wholesale, and Correspondent lending equally well, making it versatile for different business models.

#6 LendingDox

Best for: Secure Document Management

Often integrated with Shape Software, LendingDox focuses heavily on the document handling aspect of the business. If your current system is a mess of Google Drive folders and email attachments, look here.

Highlights:

- Centralized Storage: It provides a single, secure location for originating, managing, and storing all loan documents.

- Top-Tier Security: Built with SOC 2 compliance and GDPR standards, it ensures your sensitive borrower data is locked down tight.

- Real-Time Tracking: You can monitor the status of every document in real-time, receiving notifications the moment a client uploads a paystub.

- Shape Integration: It works hand-in-glove with Shape CRM, creating a seamless flow from lead intake to document collection.

- Cost-Effective: Their pricing model (often per user/month with no installation fees) is transparent and friendly for growing teams.

#7 LendingPad

Best for: Cloud-Based Flexibility & Brokers

LendingPad has gained a cult following among brokers and independent mortgage banks. It is lightweight, fast, and completely modern.

Highlights:

- Anywhere Access: It is a true cloud-native LOS. You can run your pipeline from a tablet in a coffee shop just as easily as from your office.

- Broker Edition: They have a version specifically tailored for brokers that simplifies the interface and workflow, stripping away unnecessary bank-level complexity.

- Fast Implementation: Unlike legacy systems that take months to set up, LendingPad gets teams up and running very quickly.

- Wholesale Integration: It has direct integrations with major wholesalers, making the submission process incredibly smooth.

- Collaboration: It supports multi-user editing, meaning a processor and an LO can work on the same file simultaneously without locking each other out.

#8 Backbase

Best for: Engagement Banking & Customer Journey

Backbase takes a different approach. They focus on "Engagement Banking." They are less about just processing a loan and more about the entire digital lifecycle of the customer.

Highlights:

- Frictionless Journey: They excel at allowing a borrower to start an application on a phone, pause, and finish it on a laptop without missing a beat.

- Unified Platform: It consolidates retail, SME, and commercial lending onto one platform, which is great for institutions offering diverse products.

- Customer-Centric: The system leverages data to offer personalized experiences, much like modern apps such as Uber or Netflix.

- Composable Banking: Their modular architecture allows you to "plug and play" new features without overhauling your entire legacy system.

- Employee Efficiency: It gives your back-office team a unified view of the customer, empowering them to provide faster, better support.

How to Choose Your Loan Officer CRM?

With so many options, how do you pick? In my experience, there is no "perfect" CRM, but there is one that fits your business model.

- First, define your Business Model. If you are a Broker, flexibility and speed (like LendingPad or Zeitro) are key. If you are a large lender with a sales floor, you need the discipline of Velocify.

- Second, consider your Tech Stack. Do you already use Encompass? Or are you a Salesforce shop? If the latter, Jungo is the logical choice.

- Third, assess your AI Needs. Do you spend hours fighting with guidelines? If yes, Zeitro is currently unmatched in this specific area.

- Finally, look at Ease of Use. You don't want a tool that requires a PhD to operate. Ask for a demo and see if the interface feels intuitive to you.

Conclusion

The mortgage industry in 2026 is unforgiving to those who refuse to adapt. Technology is your only leverage against margin compression and time constraints. While Salesforce-based tools like Jungo offer immense power for customization, and Floify dominates the borrower POS experience, the landscape is shifting towards AI.

If you want to truly future-proof your workflow, I highly recommend looking at Zeitro. The ability to save 7+ hours per loan and use AI to navigate complex guidelines is not just a "nice to have", it is a competitive advantage. It's like hiring a genius processor who works 24/7 for a fraction of the cost.

Don't just take my word for it. Most of these platforms offer trials. I suggest starting with Zeitro's Explorer Free plan to see the "Scenario AI" in action. Your future self (and your weekends) will thank you.