![[NO Experience] How to Become a Mortgage Underwriter?](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/69b3d224fd31186886db51ce_how-to-become-a-mortgage-underwriter-banner.png)

Written by

Eric

Share this article

.svg)

Subscribe to updates

Last checked and updated on July, 2026

A few years back, I was stuck. I wanted a stable, well-paying career but had zero finance background, and the title "mortgage underwriter" sounded like something reserved for Wall Street types. If you're trying to figure out how to become a mortgage underwriter with no experience, I know exactly how intimidating that feels. Here's the truth: it's doable, and you don't need a finance degree to break into an entry-level underwriting career. This guide walks through the exact roadmap I used to land my first role.

Quick answers before you dive in:

- You do not need a four-year degree or a state license to become a mortgage underwriter — most lenders care more about your accuracy and judgment than your diploma.

- Realistic entry point: a processor or underwriting assistant role, not "underwriter" on day one.

- Entry-level pay typically lands between $58,000 and $75,000, with experienced underwriters averaging closer to $80,000–$95,000 nationally.

- A NAMU certification (roughly $795 for the core credential) can shorten your job search, but it's not the only way in.

Who is a Mortgage Underwriter?

A mortgage underwriter is the person who decides whether a lender should take on the risk of a home loan. My daily routine involves digging into credit histories, tearing apart W-2s and tax returns to verify income, and calculating debt-to-income (DTI) and loan-to-value (LTV) ratios against the lender's guidelines, which are usually tied to Fannie Mae and Freddie Mac rules. Automated underwriting systems like Desktop Underwriter now flag a lot of this upfront, but a human still has to resolve anything the software can't clear, which is where the real skill lives.

What underwriters typically check on every file:

- Credit history and payment patterns

- Income and employment stability

- DTI and LTV ratios against investor guidelines

- Asset sourcing (down payment, reserves, gift funds)

- Property value and title issues flagged by the appraisal

Do Mortgage Underwriters Need a License?

This trips up a lot of newcomers, so let's clear it up. Unlike loan officers, who must hold an NMLS license in every state they work in, mortgage underwriters generally do not need a personal state license to do the job. What you do need is to follow your employer's and its investors' underwriting standards, and eventually you may pursue authorizations like FHA Direct Endorsement, which are earned through demonstrated experience rather than a licensing exam. So if you're wondering how to become a mortgage underwriter in Texas, Florida, or any other state, the good news is there's no separate state exam standing between you and the job.

Also Read:

- Mortgage Underwriter Salary: How Much Does a Home Loan Underwriter Make?

- Mortgage Underwriter vs Loan Officer: Which Career Is Best?

- 30 Mortgage Underwriter Interview Questions to Prepare First

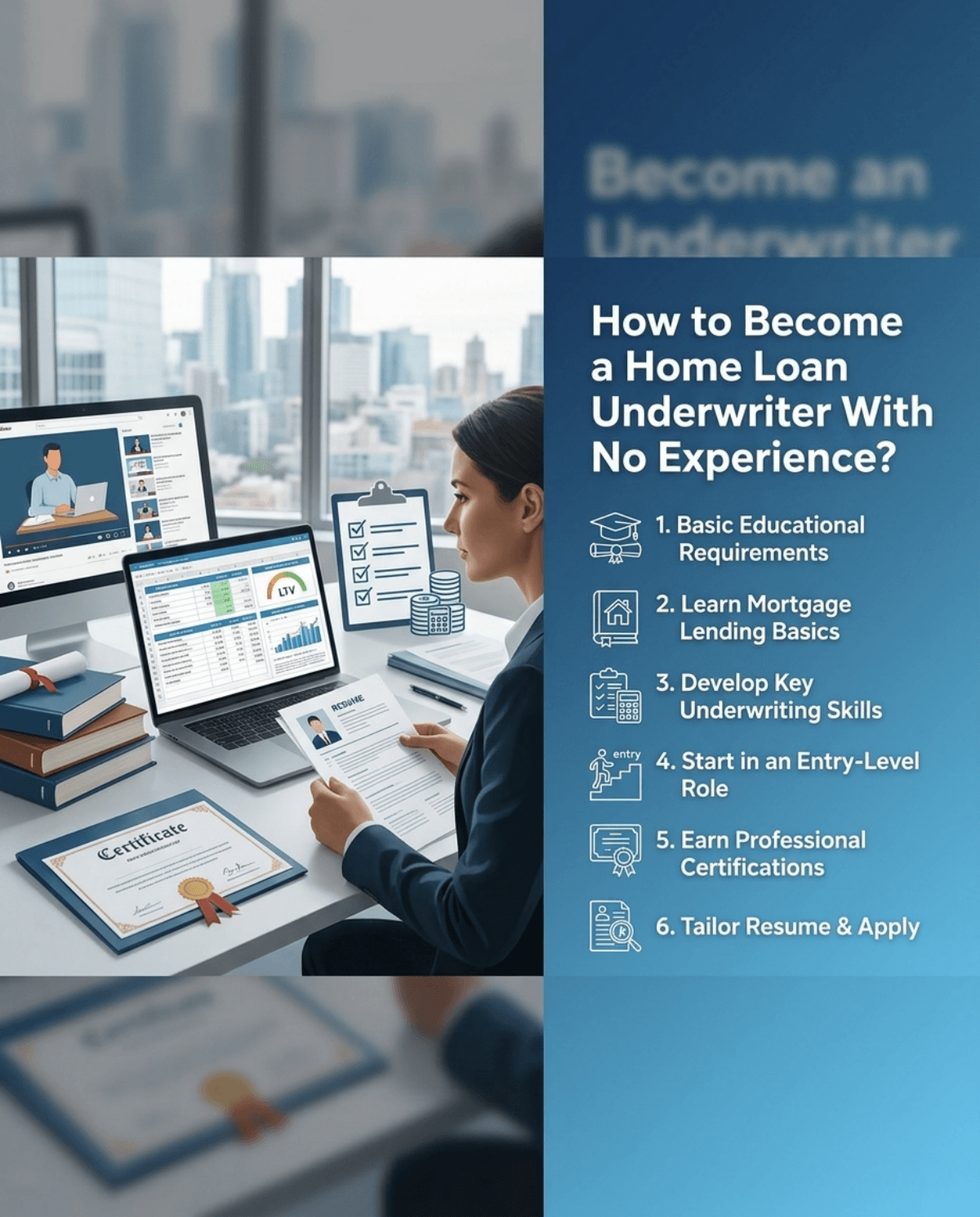

How to Become a Home Loan Underwriter With No Experience?

Looking at a blank resume is scary, but underwriting is remarkably open to newcomers if you take the right approach. Here's the roadmap.

Also Read:

- Best Mortgage Underwriter Training Online: Improve Your Expertise

- Best Mortgage Underwriter Certifications: Everything to Know Here

STEP 1. Meet the Basic Educational Requirements

When I started job hunting, I assumed my lack of a finance degree would get my resume tossed. That's a myth. A bachelor's degree in business or accounting helps, and many lenders prefer one for full underwriter roles, but some will hire candidates with just a high school diploma or associate's degree into processor or assistant positions first. What hiring managers actually want is comfort with numbers and the ability to spot inconsistencies. If you don't have a four-year degree, don't let it stop you. Strong math skills and stubborn attention to detail carry real weight here.

STEP 2. Learn Mortgage Lending Basics

Since you don't have a track record yet, self-study is your best differentiator. Learn the difference between conventional loans and government-backed products like FHA, VA, and USDA mortgages. You'll also want a working grasp of Fannie Mae and Freddie Mac, since their guidelines shape most U.S. housing loans. You don't need to memorize the entire rulebook — nobody does — but knowing the terminology shows interviewers you're serious. Free resources like the Fannie Mae Selling Guide, HUD's Handbook 4000.1, and YouTube channels built for loan processors are a solid starting point. Also, when necessary, I use Zeitro Strata to verify mortgage eligibility as a double-check.

STEP 3. Develop Key Underwriting Skills

This role demands a specific mix of technical and personal skills. Eventually you'll read tax transcripts, decode financial statements, and run underwriting software, but the soft skills matter just as much early on. The most important trait is borderline-obsessive attention to detail, missing one decimal on a bank statement can sink a loan. You also need a thick skin for month-end pressure, when agents are chasing closing dates. Start practicing by catching typos and math errors in your own paperwork; it's the same muscle you'll use on the job.

STEP 4. Start in a "Stepping Stone" Role (Entry-Level)

No one hands you an underwriter title on day one. Ocertainly didn't get one. Look for stepping-stone jobs like Loan Processor, Loan Officer Assistant, or Underwriting Trainee. I'd point you toward processing first: a processor collects the W-2s and pay stubs before a file ever reaches underwriting, so you get a front-row seat to what actually gets a loan approved or denied. Pay for processors typically runs in the $40,000 to $55,000 range depending on region and lender, and many of these roles are hybrid or fully remote now, since the job is largely file review and system work rather than in-person banking. Managers also love promoting their strongest processors into junior underwriting seats, since they already know the file flow.

STEP 5. Earn Professional Certifications

When your resume doesn't scream "finance expert," a certification does the talking for you. The most recognized option is the National Association of Mortgage Underwriters (NAMU), whose Certified Mortgage Underwriter (CMU) credential currently runs around $795 and covers loan origination basics, DTI calculation, appraisal review, and fraud red flags through a short proctored exam. More advanced tracks, like the Certified Master Mortgage Underwriter (CMMU), cost closer to $1,000 and go deeper into government and non-QM lending. A certification isn't the only path in — some lenders will still hire you into a processor role and train you from scratch — but it noticeably improved my callback rate when I added it to my resume.

STEP 6. Tailor Your Resume & Apply for Jobs

Now it's time to actually apply. Stop focusing on the experience you lack and start reframing what you already have. Did you handle cash, audit inventory, or manage frustrated customers? That's "analytical ability," "attention to detail," and "conflict resolution" on paper. Put any self-study courses or new certifications near the top of your resume. I also networked aggressively on LinkedIn, connecting with branch managers at credit unions and mid-sized lenders, and applied to postings labeled "Junior" or "Trainee" even when I only checked half the boxes. Search terms like "entry level underwriter jobs," "underwriting assistant jobs," and "remote underwriting jobs" are worth setting up as job alerts.

Mortgage Underwriter Career Path

Underwriting isn't a flat job title — it's a ladder, and knowing the rungs helps you set realistic expectations.

- Loan Processor / Underwriting Assistant – gathering and organizing borrower documents, roughly $40,000–$55,000

- Junior or Associate Underwriter – reviewing simpler files under supervision, roughly $75,000–$85,000

- Underwriter I/II – handling full files independently, roughly $80,000–$95,000

- Senior Underwriter – complex, jumbo, or exception files, roughly $95,000–$115,000

- Chief Underwriter / DE Underwriter – authorized to approve FHA or VA loans without agency review, often six figures in high-volume shops

Moving up this ladder usually takes one to two years of solid file experience per level, though a certification or a DE authorization can accelerate things.

Mortgage Underwriter Certification

A solid credential bridges the gap between being a total newbie and a viable candidate. Here are the ones that actually carry weight in the industry:

NAMU (National Association of Mortgage Underwriters): This is one respected organization in the U.S. mortgage industry. Earning a credential such as their Certified Mortgage Underwriter (CMU) or Certified Residential Underwriter (CRU) designation can show employers that you have studied formal underwriting guidelines, though it is not the only path to becoming a strong candidate.

FHA Direct Endorsement (DE)/VA SAR: These are advanced, specialized credentials for government‑backed loans. You won't be eligible right away, but pursuing them later in your career can help position you for higher‑level roles that often pay six‑figure salaries, depending on market, lender, and experience.

How Much Does It Cost to Become a Mortgage Underwriter?

Let's be completely transparent about the money. You will have to spend a little out of pocket to get started, but the return on investment is huge.

- Training Courses: Good online boot camps or self-paced classes usually run anywhere from $300 to $1,000.

- NAMU certification: Expect around $795 for the core CMU credential, more for advanced tracks.

- Background Checks: Sometimes you pay for this yourself initially. Plan for about $50 to $100.

All in, plan on roughly $1,000 to $2,000. Given that entry-level U.S. underwriters commonly start between $58,000 and $75,000 and averages across the profession run closer to $80,000–$95,000 once you account for experience and location, with metros like New York City paying noticeably above the national number. That's a small price for a career shift.

Tips for New Home Loan Underwriters

Once you finally get a desk, the real stress tests begin. Here are three things that saved me during my first year:

- Tip 1: Stay Updated on Guidelines: Fannie Mae changes their rules constantly. Make a habit of reading agency bulletins on Friday afternoons so you don't approve something using last month's rules.

- Tip 2: Ask Questions: If a self-employed borrower's tax return looks like a mess, swallow your pride and ask a senior underwriter. Guessing will get you fired.

- Tip 3: Embrace AI and Automation Technology: The industry isn't just paper anymore. I highly recommend familiarizing yourself with an AI-powered LOS (Loan Origination System) like Zeitro. Modern underwriters who use automated workflows to catch errors and speed up closing times are the ones who get promoted fastest.

Also Read: Best Mortgage Underwriter Software: AI & Guideline Verification

Mortgage Underwriter vs. Insurance Underwriter: What's the Difference?

If you've been searching around this topic, you've probably noticed "underwriter" also shows up in insurance job postings and it's a genuinely different career. An insurance underwriter evaluates the risk of insuring a person or property (health, life, auto, property) rather than the risk of repaying a home loan. According to the Bureau of Labor Statistics, insurance underwriters earned a median annual wage of $79,880 in May 2024, with roughly 8,200 openings projected each year through 2034 despite a slowly shrinking headcount as automation takes over routine approvals. If you're deciding between the two paths, mortgage underwriting tends to track more closely with the housing market's ups and downs, while insurance underwriting is spread across health, life, and property lines with steadier long-term demand.

FAQs About Becoming a Mortgage Underwriter

Q1. How hard is it to become a Mortgage Underwriter?

It isn't rocket science, but it demands extreme attention to detail and patience. Starting from scratch is tough, but if you take a transitional role like a loan processor first, the learning curve becomes much more manageable. You just have to be willing to study the guidelines.

Q2. How do I start a career as an underwriter?

The most realistic way in is to get hired as a Loan Processor or Underwriting Assistant. While working that job, study lending guidelines on your own time and earn a professional credential from NAMU to show managers you are ready to move up.

Q3. How long does it take to become a certified underwriter?

With consistent part‑time effort, many candidates can complete foundational training and pass their NAMU certification exams within roughly two to six months, though this will vary depending on prior background and study pace.

However, getting enough on-the-job experience to become an independent, fully authorized underwriter usually takes about one to two full years.

Q4. Do underwriters make a lot of money?

In many U.S. markets, entry‑level residential underwriters commonly start in roughly the $55,000 to $65,000 range, though this can be higher or lower depending on location and lender. With a few years of experience, total compensation often moves into the $70,000–90,000 band, and senior underwriters or those with advanced credentials (like FHA Direct Endorsement) can reach six‑figure salaries in stronger markets or high‑volume shops.

Q5. Is underwriting a hard career?

It can be highly stressful, especially when real estate volume spikes in the spring. You carry the burden of risk decisions and handle massive amounts of paperwork. But if you enjoy analyzing data and working in a structured, desk‑based environment, while also being comfortable with occasional high‑pressure deadlines and team coordination, it can be a very fulfilling career.

Q6. Do you need a license to become a mortgage underwriter?

No. Unlike loan officers, underwriters don't need a personal NMLS license in most cases — you'll follow your employer's compliance standards instead, and pursue authorizations like FHA DE later in your career if you want them.

Q7. Is mortgage underwriting the same as insurance underwriting?

No. Mortgage underwriters assess the risk of a home loan; insurance underwriters assess the risk of insuring a person or property. They share a job title but almost nothing else in daily responsibilities.

Conclusion

Looking back, stepping into the mortgage industry without a finance background was terrifying, but it was one of the best career decisions I've made. Becoming a mortgage underwriter with zero experience is realistic if you follow the roadmap: learn the guidelines, get a respected certification under your belt, and put in the time in an entry-level processor role first. Staying comfortable with modern tools, like an AI-powered loan origination system, will keep you competitive as the job keeps changing.

Don't wait until you feel "ready," because that day doesn't really come. Start with the basic loan types today, look into platforms like Zeitro, and take the first step.

People Also Read

- Best Mortgage Companies for New Loan Officers

- How to Become a Loan Officer with No Experience?

- Best Mortgage CRM for Brokers, Lenders, MLOs

- [Tips] Where to Buy Mortgage Leads? Warm Leads for LOs

- Beginner's Guide: How to Get Leads for Mortgage Loans?

- [Solved] How Long Does Mortgage Underwriting Take?