Written by

Eric

Share this article

.svg)

Subscribe to updates

When I first started looking into the mortgage industry, I was completely overwhelmed. Like many of you, I found myself staring at job boards, wondering: what actually is the difference between a mortgage underwriter and a loan officer? Which one makes more money? Which one has a better work-life balance? If you are stuck trying to figure out which path suits your personality, you are in the right place.

In this guide, I will break down both careers comprehensively so you can decide which role aligns perfectly with your skills and financial goals.

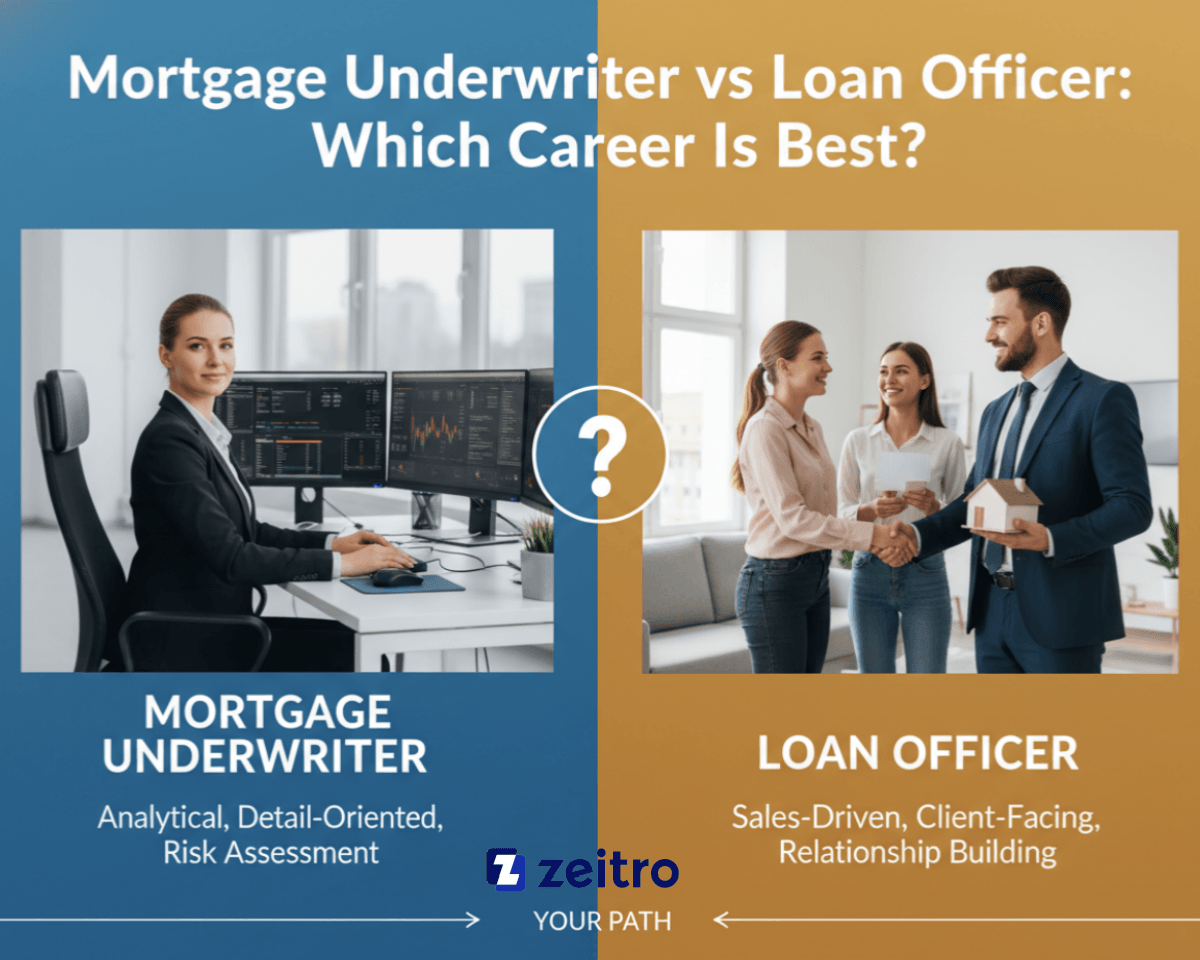

What is a Mortgage Underwriter?

Think of a mortgage underwriter as the ultimate gatekeeper of the lending world. From my experience, they are the analytical minds working tirelessly in the back office. Their primary job is to evaluate a borrower's financial risk—scrutinizing credit histories, assets, and debt-to-income (DTI) ratios—to decide if the bank should actually fund the loan.

While automation has slowed the overall job growth slightly, skilled underwriters who can navigate complex financial scenarios are still highly valued. If you love crunching numbers and prefer a quiet, analytical-driven environment, this is your zone.

Also Read:

- [NO Experience] How to Become a Mortgage Underwriter?

- What is Mortgage Underwriting? A Complete Guide & FAQs

- Best Mortgage Underwriter Software: AI & Guideline Verification

- 11 Best Loan Officer Schools for Newbies: Online & Local

- [Guide] What is a Loan Officer License? How to Get It?

- Loan Officer vs Real Estate Agent: Key Differences to Learn

- Realtor vs Loan Officer: What's the Difference?

What is a Loan Officer? (MLO)

On the flip side, a Mortgage Loan Officer (MLO) is the frontline guide for homebuyers. They are the face of the company, actively hunting for leads, networking with real estate agents, and helping clients pick the right mortgage products. MLOs gather the initial paperwork to get the ball rolling.

According to the Bureau of Labor Statistics, employment of loan officers is projected to grow 2% from 2024 to 2034, which is slower than the average for all occupations. It is an intensely client-facing, sales-driven role. If you thrive on building relationships and closing deals, this career fits like a glove.

Also Read:

- Detailed Guide: How to Become a Loan Officer with No Experience?

- Best CRM for Loan Officers: Which One Suits You Most?

- Best Mortgage Loan Officer Training: Which to Pick?

- Best Mortgage Companies for New Loan Officers

Quick Look at the Comparison Between Loan Officer vs Underwriter

Before we dive into the nitty-gritty details, let me save you some time. Here is a quick snapshot I put together highlighting the core differences between these two mortgage professionals.

This table covers the basics, but choosing your life's work requires a deeper understanding of the daily grind.

What is the Difference Between Loan Officer vs Underwriter?

Beyond that quick comparison, let's unpack exactly how these roles contrast on a day-to-day basis. I've broken down their differences across seven vital dimensions to give you a crystal-clear picture of what to expect.

Responsibilities

A loan officer's main responsibility revolves around origination. I always tell people that MLOs are the hunters. They bring the business through the door. Their day consists of cold calling, meeting with prospective buyers, explaining loan options, like fixed-rate vs. ARM, and taking the initial application.

Conversely, the underwriter handles the approval or denial phase. They are the risk managers protecting the lender's money. Once the MLO submits the file, the underwriter verifies that the borrower actually makes what they claim and that the property appraises correctly. They don't sell. They verify. While the loan officer wants every deal to close, the underwriter's duty is to ensure only the safe, qualified deals make it to the finish line.

Education, Skills & Certifications

When it comes to formal requirements, the paths diverge significantly. To legally work as a Loan Officer in the US, you absolutely must obtain your NMLS (Nationwide Multistate Licensing System) license. This requires passing a rigorous national exam, completing 20 hours of pre-licensing education, and undergoing background checks. You don't necessarily need a college degree, but sales charisma is non-negotiable.

Underwriters, however, rarely need a sales license. Instead, lenders look for extreme analytical prowess. A bachelor's degree in finance or accounting is highly preferred. Furthermore, to stand out or handle government loans, underwriters often pursue specific certifications, such as becoming an FHA Direct Endorsement (DE) underwriter or securing VA LAPP approval. Having these specialized designations proves your expertise in complex federal guidelines.

Also Read:

- NMLS License Cost Breakdown: Know Your Every Penny

- Best NMLS Test Prep Course: Which to Choose from?

Salary

Let's talk money, because I know that is a huge deciding factor. Based on 2024 data from the Bureau of Labor Statistics, the median base salary for a loan officer sits around $74,180. However, MLOs are heavily commission-based. A top-producing loan officer in a busy real estate market can easily rake in well over $150,000 to $200,000 annually. The catch? If you don't close, you don't eat.

Mortgage underwriter average salaries range from about $65,000 to $95,000 annually, depending on experience, location, and source, often including bonuses but generally more stable than loan officers' commission-heavy structure.

Also Read:

- Mortgage Loan Officer Salary: How Much Do Loan Officers Make?

- Mortgage Underwriter Salary: How Much Does a Underwriter Make?

Workflow

Understanding where each professional sits on the loan timeline is crucial. The loan officer lives entirely on the front-end. They represent the very beginning of the borrower's journey. An MLO initiates the application, locks in the interest rate, and passes the baton to the processing team to gather documents.

The underwriter operates strictly in the mid-to-back-end of the workflow. They only enter the picture once the loan processor has organized the file. The underwriter reviews the neatly packaged documents, issues conditions (asking for a missing bank statement, for example), and eventually grants the coveted "Clear to Close." They are the final checkpoint before the funds are actually wired to the title company.

Interaction

If you are an extreme extrovert, pay attention here. A loan officer's calendar is packed with social networking. I've seen successful MLOs spend their weekends hosting open houses with real estate agents, grabbing coffee with financial planners, and constantly texting anxious homebuyers. Your success depends directly on your external relationships.

An underwriter's social battery is drained very differently. They primarily engage in internal communication. Underwriters rarely, if ever, speak directly to the borrower. Their daily interactions are limited to emails and phone calls with loan officers and processors to clarify file discrepancies. It is a highly insulated, quiet role perfect for those who prefer analyzing spreadsheets over shaking hands.

Authority

Who really holds the power? I can answer that definitively: the underwriter has the final say. No matter how much a loan officer promises a client they will get approved, the MLO cannot override the underwriter.

Underwriters possess the ultimate authority to approve, suspend, or flat-out deny a mortgage. They are bound by strict investor guidelines, such as those set by Fannie Mae, Freddie Mac, or the FHA. If a borrower's file doesn't fit the matrix, the underwriter must reject it. While the loan officer can argue the case, escalate the issue to management, or provide compensating factors, they simply do not hold the pen that signs off on the company's millions of dollars.

Career Path

Both roles offer excellent upward mobility, just in different directions. An ambitious loan officer usually moves up the sales ladder. You might start as a junior MLO, become a top producer, and eventually transition into a Branch Manager or Regional VP of Sales. Some even open their own independent mortgage brokerages.

For an underwriter, the trajectory is firmly rooted in risk and operations. You typically start as a Junior Underwriter, advancing to a Senior Underwriter once you gain your government designations. From there, the path leads to Underwriting Manager, VP of Credit Operations, or even a Credit Risk Director. Both paths can lead to the executive suite, but one relies on sales volume while the other relies on technical expertise.

Suggestions on Picking Your Career

Still on the fence? Based on my time observing the mortgage industry, I've found that success comes down to matching your natural disposition with the job requirements. Here are a few practical suggestions to help you decide:

- Choose the Loan Officer route if you are naturally outgoing, resilient, and thrive in social networking settings.

- Opt for Underwriting if you are an introverted thinker who loves digging into data and scrutinizing details.

- Pick Loan Officer if you want unlimited earning potential and don't mind the stress of fluctuating, commission-based income.

- Go with Underwriting if a predictable 9-to-5 schedule, work-life balance, and a stable paycheck are your top priorities.

- Choose Loan Officer if you possess a knack for persuasion and have a true sales mentality.

- Select Underwriting if you have a strong sense of risk aversion and enjoy navigating complex regulatory frameworks.

FAQs About Mortgage Underwriter vs Loan Officer

Q1. Is a loan officer the same as an underwriter?

No, they are completely different roles. A loan officer is a sales professional who helps clients apply for a mortgage and selects the right loan product. An underwriter is a financial analyst who reviews the borrower's documents to assess risk and makes the final approval decision.

Q2. Who makes more, an underwriter or a loan officer?

It depends on performance. A top-tier loan officer earns significantly more due to uncapped commissions, sometimes exceeding $200,000 annually. However, an underwriter typically enjoys a much higher and more stable guaranteed base salary compared to an entry-level loan officer.

Q3. Will MLO be replaced by AI?

No. While AI and automated software are speeding up the initial processing and document sorting, buying a home is a massive, emotional financial decision. Borrowers will always need human loan officers for nuanced advice, empathy, and personalized problem-solving that AI simply cannot provide.

Q4. Can a loan officer override an underwriter?

No, a loan officer cannot override an underwriter's decision. The underwriter has the absolute final say on loan approval. However, if a loan is denied, the loan officer can submit an appeal or provide additional compensating factors to request a secondary review.

Q5. Is MLO in high demand?

Demand varies heavily with the economy. When interest rates drop, the demand for MLOs skyrockets due to a refinancing boom. While the overall long-term job growth is steady, the industry will always need skilled originators as long as people continue buying real estate.

Conclusion

Wrapping things up, deciding between these two paths really boils down to one fundamental question: do you want to drive the sales, or do you want to manage the risk? Loan officers are the extroverted engines of the mortgage industry, while underwriters are the meticulous brakes ensuring everything runs safely.

There is no absolute winner here. Choosing between a loan officer and mortgage underwriter career simply depends on your own personality traits, risk tolerance, and long-term financial goals. Take a moment to assess what makes you tick. If you found this breakdown helpful in clarifying your future career in real estate finance, please share it with others who might be weighing the exact same decision!