Written by

Eric

Share this article

.svg)

Subscribe to updates

Last checked and updated on July, 2026

Quick answer: if you're on a tight budget, 24hourEDU is hard to beat for value. If you want a deeper, more entertaining learning style, Knowledge Coop is my pick. Californians should look closely at Retrainersca for the state-specific quirks. And once you're licensed and want to actually sell, XINNIX or TLOPonline are where the real sales training happens.

When I first decided to dive into the mortgage industry, I was overwhelmed. It felt like I was staring at a mountain of acronyms, NMLS, SAFE, UST, DRE, without a climbing map. If you are standing in that same spot today, looking ahead at 2026, I have good news: the path is clearer than you think, provided you pick the right guide.

Becoming a Loan Officer is one of the most rewarding career pivots you can make, but the difference between "just passing the test" and "actually knowing how to close loans" lies entirely in your training. This isn't just about ticking compliance boxes. It's about building a foundation that survives a shifting market. In this guide, I'll walk you through exactly how to get licensed, which schools are actually worth your money in 2026, and the tools you'll need to survive your first year.

People Also Read:

- [Tips] Where to Buy Mortgage Leads? Warm Leads for LOs

- Are Mortgage Rates Expected to Go Down in 2026? Expert Forecasts

- Best CRM for Mortgage Brokers in 2026: Choose As Required

- Best Mortgage Underwriter Training Online: Improve Your Expertise

- Best Mortgage Underwriter Certifications: Everything to Know Here

- Best Mortgage Loan Processor Training for Beginners

- 11 Best Loan Officer Schools for Newbies: Online & Local

Key Training Components & Steps to Learn

Before we look at the schools, you need to understand the roadmap. The mortgage industry is federally regulated, meaning there is no "shortcut" to getting your license. However, understanding the flow can save you weeks of confusion.

Here is the standard path I recommend following:

- NMLS Registration: Your journey starts at the Nationwide Multistate Licensing System (NMLS). You need to create an account to receive your unique NMLS ID number. Think of this as your "social security number" for your mortgage career. It will follow you forever, regardless of which company you work for.

- Pre-Licensure Education (PE): This is the big hurdle. You must complete 20 hours of NMLS-approved coursework. This isn't random study. It's a strict breakdown: 3 hours of Federal Law, 3 hours of Ethics, 2 hours of Non-traditional Mortgage Lending, and 12 hours of Electives.Note: If you are in a state like California and licensing under the DFPI, you must complete state‑specific education (for example, a 2‑hour CA‑DFPI course), which is counted as part of the required 20 hours rather than added on top of it.

- SAFE Exam: You will need to pass the SAFE MLO Test with Uniform State Content. The exam has 125 multiple‑choice questions in total, of which a subset is scored and the rest are unscored experimental items, and you need a score of at least 75% on the scored portion to pass. It's not easy, the national first‑time pass rate is roughly in the mid‑50% range, which is why your choice of training school matters.

- Background & Credit Check: Trust is the currency of this business. You will need to get fingerprinted and authorize a credit report through the NMLS portal to prove your financial responsibility and lack of criminal history.

- Licensing & Sponsorship: Passing the exam doesn't mean you are "active." You must apply for your state license and, crucially, gain Sponsorship. This means an employer (a licensed mortgage broker or lender) must officially accept your license under their company umbrella. You cannot originate loans without this sponsorship.

- Employer-Provided Training: Once you are hired, the real learning begins. Your employer will train you on their specific Loan Origination System and CRM for loan officers. This is where you learn the art of prospecting and managing client relationships, which is very different from the legal theory you learned for the exam.

How Much Does It Cost to Get Licensed?

New candidates are usually surprised that the "$189 course" isn't the whole bill. Based on current NMLS fee schedules and state averages, here's roughly what to budget:

- 20-hour PE course: $150–$400

- SAFE exam fee: $110 per attempt

- NMLS processing fee: $30–$35

- Credit report: $15

- FBI background check (electronic): $36.25

- State license application fee: $100–$400 (varies widely by state)

- Rough total: $600–$1,000+

State fees are the biggest wildcard, so check your specific state regulator's page before you budget. Some employers reimburse part of this once you're hired, so it never hurts to ask during the interview.

Also Read: NMLS License Cost Breakdown: Know Your Every Penny

Annual Continuing Education: The Part Most Guides Skip

Getting licensed is only half the job. Every state-licensed MLO has to complete 8 hours of NMLS-approved continuing education (CE) each year to keep the license active. Those 8 hours break down into 3 hours of federal law, 2 hours of ethics, 2 hours of non-traditional mortgage lending, and 1 hour of elective coursework, which is sometimes state-specific.

A handful of states pile on extra hours. California, for example, requires an additional hour of DFPI-specific law within that annual requirement if you're licensed under the DFPI. Most states set the renewal deadline for December 31, so it pays to knock CE out well before the holiday rush rather than scrambling in the last week of the year. NMLS also enforces a "successive years" rule, meaning you can't retake the exact same CE course two years running.

Providers like 24hourEDU, Mortgage Educators and Compliance (MEC), and OnCourseLearning all offer approved CE packages alongside their pre-licensing courses, so it's worth sticking with a provider you already trust rather than shopping around every single year.

Where to Find the Best Mortgage Loan Officer Training?

Now that you know what to do, the question is where to do it. The market is flooded with course providers, but they are not all created equal. Based on my research and industry feedback for 2026, here are the top contenders.

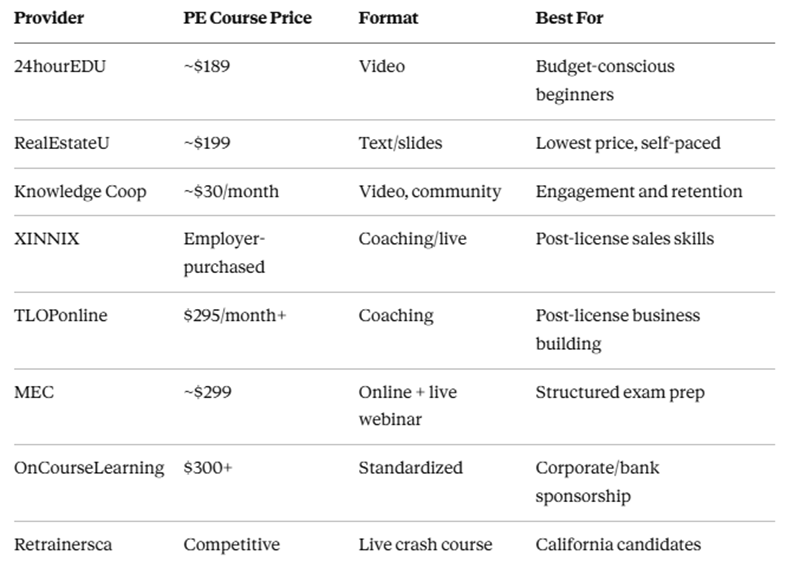

1. 24hourEDU

If you are looking for a balance between affordability and modern content delivery, 24hourEDU is often my top recommendation for beginners. They have carved out a niche by offering "budget-friendly" courses that don't feel cheap.

Their primary selling point is the video-based format. Unlike some old-school providers that make you read PDF slides for 20 hours, 24hourEDU uses video instruction which I find much easier to digest. For 2026, their packages are very competitive, typically around the $189 mark for the full 20‑hour SAFE course, and that price generally includes exam prep.

What I really like is the value-add: they usually include the Test Prep materials and the NMLS credit banking fee (which costs $30) in the price. Many other schools hide these fees until checkout. They also offer a "Pass Guarantee" on their exam prep, giving you peace of mind. If you want to get done quickly (they have a 14-day completion track) without breaking the bank, this is a solid pick.

2. RealEstateU

RealEstateU built its name in real estate licensing before expanding hard into mortgage education, and its whole pitch comes down to one word: cheap. Courses are often listed under $199, and discount codes pop up frequently.

The catch is format. Expect more reading and slide-based instruction rather than polished video. That's fine if you're someone who studies best at your own pace with a highlighter in hand. They also bundle real estate and MLO licensing together, which can save money if you're chasing both credentials at once.

3. Knowledge Coop

If you dread the idea of boring compliance lectures, Knowledge Coop is the antidote. Their CEO, Ken Perry, is a legend in the industry for making compliance actually... fun.

They use an "Edutainment" approach. The videos are high-quality, funny, and engaging, often feeling more like a YouTube series than a federal law class. For 2026, they have expanded their "Coop+" membership, which is a subscription model (often starting around $30/month or an annual fee).

This membership gives you access to your PE (Pre-Licensure), CE (Continuing Education), and a massive library of deeper mortgage training. They focus heavily on building a community, so you aren't just learning in isolation. If you are a visual learner who needs engagement to retain information, the extra cost here is absolutely worth it.

4. TLOPonline

I want to make a clear distinction here: TLOPonline is not where you go to get your NMLS license. It's where you go to learn how to make money after you get it.

Founded by Dustin Owen, this platform focuses on Sales and Practical Training. Most new Loan Officers quit within the first year not because they failed the exam, but because they didn't know how to get business. TLOP offers coaching programs like "Originator Launch" and "Bootcamps."

Pricing here is higher, often ranging from $295/month for community access to 2,000+ for intensive bootcamps. However, the ROI is substantial. You learn how to structure your day, how to talk to Realtors, and how to sell. If you have your license but feel lost on day one of the job, this is the training you need.

5. MortgageEducators (MEC)

Mortgage Educators and Compliance (MEC) is the reliable, "old faithful" of the industry. They have been around for years and have a sterling reputation for comprehensive education.

Their 20-hour course bundles usually start around $299, but they run frequent sales. The standout feature here is their Test Prep. Many students report that MEC's practice exams are the closest thing to the actual NMLS National Test.

I also appreciate their customer service. If you get stuck on a module or have a technical glitch, you can actually get a human on the phone. They offer both online self-study and "Live Webinar" formats. If you are nervous about the exam and want a structured, academic approach to ensure you pass on the first try, MEC is a very safe bet.

6. Retrainersca (Real Estate Trainers)

If you are located in California, pay close attention to this one. Retrainersca (Real Estate Trainers) is a specialist institution that focuses heavily on the specific needs of the California market.

California has a complex licensing structure (DFPI vs. DRE), and Retrainersca excels at clarifying this. They are famous for their Live Crash Courses (often held in Anaheim or via Zoom). For many people, sitting in a room (virtual or physical) for a weekend crash course is the only way to absorb the material.

Their pricing is competitive for live instruction. If you are transitioning from being a Real Estate Agent to a Loan Officer in CA, their instructors are experts at explaining the overlap and differences between the two licenses. It's a local favorite for a reason.

7. OnCourseLearning

OnCourseLearning is the corporate heavyweight. If you get hired by a large bank or a national lender, there is a high chance they will pay for you to take your training here.

Their catalog is massive. They don't just cover the 20-hour SAFE course. They have training for underwriters, processors, and compliance officers. The pricing is standard, typically in the $300+ range for the PE bundle.

The vibe here is very professional and standardized. You won't find the humor of Knowledge Coop, but you will find extremely accurate, vetted content that compliance departments love. If you plan to work in a corporate banking environment, having OnCourseLearning on your resume shows you were trained by the industry standard.

8. XINNIX

XINNIX isn't where you go to get your NMLS license, and that's an important distinction. It's a performance and sales training academy, best known for its ORIGINATOR program for brand-new loan officers and its coaching tracks for experienced ones.

Companies frequently purchase XINNIX training in bulk for entire teams rather than individuals paying out of pocket, so ask your employer if it's already part of your onboarding before signing up independently. The Ground School and Flight School structure focuses on turning book knowledge into actual client conversations and pipeline management, which is exactly the gap that trips up so many first-year originators.

Quick Comaprison

Pricing above was checked against provider sites in mid-2026 and can shift, so confirm current rates directly with the school before enrolling.

Other Providers Worth Knowing: A few other names come up often in loan officer forums and deserve an honest mention. AmeriTrain and CampusMortgage both offer instructor-led options that some candidates prefer over pure self-study. LoanOfficerSchool.com and smaller regional academies like Affinity Mortgage Training can be solid picks if you want a more personal, boutique feel. Whichever provider you're considering, confirm its NMLS Course ID is active before paying; that's the one detail that guarantees your hours will actually count.

Tips to Be a Professional Loan Officer

Getting your license is just the entry fee. To succeed in 2026, you need to operate like a professional from day one. Here are the pillars of success I've observed in top producers.

Master Local Specifics

You cannot be a generalist. You must be a local expert. Every state has unique quirks, but California is the prime example of why details matter.

In CA, you have two potential paths. If you are a pure mortgage professional, you will likely license under the DFPI (Department of Financial Protection and Innovation). This requires the standard 20 hours plus a specific 2-hour CA-DFPI course. However, if you are a Real Estate Agent adding mortgage services, you are licensed under the DRE (Department of Real Estate). Mixing these up can delay your career by months. Know your local regulations inside and out, clients rely on you to navigate this red tape.

Master Technology

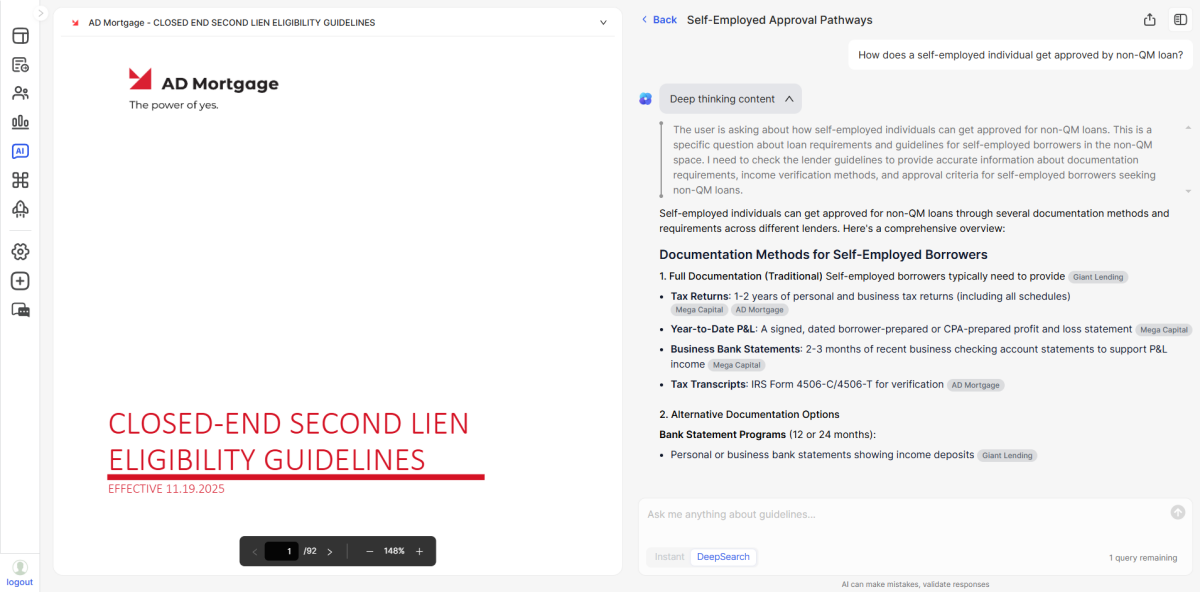

The days of manual calculations and flipping through PDF guidelines are over. The mortgage process is notoriously complex and labor-intensive, often leading to burnout. To survive, you must leverage AI.

While your company will provide a CRM, you need a personal "copilot" to handle the heavy lifting of loan scenarios. This is where I highly recommend looking into Zeitro.

Zeitro is an AI Mortgage Platform designed specifically to solve the biggest pain point for LOs: speed and accuracy. Instead of spending hours digging through Fannie Mae or Non-QM guidelines, you can use Zeitro's Scenario AI. You simply ask it a question, even a vague one, and it provides a precise, citation-backed answer in seconds.

Here is why I think it's essential for 2026:

- Efficiency: It can save you 7+ hours per loan file by automating the manual guideline checks.

- Speed: It delivers 2.5x faster pre-qualifications, meaning you can get back to your Realtors faster than the competition.

- Accuracy: It boasts 85%+ income calculation accuracy, reducing those embarrassing moments where you have to retract a pre-approval.

- Versatility: It handles everything from Conventional (Fannie/Freddie) to FHA, VA, and complex Non-QM or DSCR loans.

Best of all, it's incredibly accessible for new LOs. It operates on a freemium model and starts at just $8/month for the pro features. It's a small investment that can help you close 30% more loans by freeing up your time to sell rather than research.

Enhance Communication Skills

Mortgages are math, but sales are human. You need to translate "Debt-to-Income Ratio" into "Here is how much home you can afford for your family." Work on your empathy and clarity. If a client feels confused, they won't trust you. If they don't trust you, they won't close.

Continuous Learning

The market changes weekly. Rates shift, new loan products (like 2-1 buydowns) appear, and guidelines update. Subscribe to industry newsletters and make it a habit to read the news every morning. In 2026, being the "most informed" person in the room is a competitive advantage.

Network Strategically

Don't just ask Realtors for business. Build relationships with CPAs, divorce attorneys, and financial planners. These are "referral partners" who can send you high-quality clients. Remember, you are building a business, not just processing transactions.

Frequently Asked Questions

Q1. What is an MLO license?

An MLO license is a state-issued credential, tracked through the federal NMLS system, that legally allows someone to take residential mortgage loan applications and negotiate terms with borrowers.

Q2. What is the best course for becoming a loan officer?

It depends on your budget and learning style. 24hourEDU offers strong value for beginners, Knowledge Coop suits people who need engaging video content, and OnCourseLearning is common when a corporate employer is footing the bill.

Q3. How much does mortgage loan officer training cost?

Most candidates spend $600 to $1,000 total once you add the PE course, SAFE exam fee, background check, credit report, and state licensing fee, though state fees vary widely.

Q4. Do I need continuing education after I'm licensed?

Yes. Every state-licensed MLO must complete 8 hours of NMLS-approved continuing education annually, covering federal law, ethics, non-traditional lending, and an elective.

Q5. Is 24hourEDU a legitimate NMLS provider?

Yes. 24hourEDU is an NMLS-approved course provider offering both pre-licensing and continuing education, and it's widely used by new MLO candidates nationwide.

Conclusion

The road to becoming a top-tier Mortgage Loan Officer in 2026 starts with high-quality education, but it is paved with the tools and habits you adopt along the way. Whether you choose the engaging video style of Knowledge Coop, the budget-friendly 24hourEDU, or the live instruction of Retrainersca, the goal is the same: get licensed and get confident.

However, don't stop there. Once you have that license in hand, equip yourself with modern tools like Zeitro. While your training teaches you how to lend, tools like Zeitro give you the speed and guideline accuracy to actually win deals in a fast-paced market. Pick your school, commit to the study hours, and get ready to launch a lucrative career. Also, it's recommended to showcase your expertise for free with a personal site on Bluerate.