Written by

Eric

Share this article

.svg)

Subscribe to updates

As a loan officer in today's competitive mortgage landscape, securing quality leads remains your top business priority. Buying leads is one option, but the smarter play is to find warm, qualified prospects. Borrowers who are actively searching or already trusting a resource. This guide tells you where to find mortgage leads in 2026, how much they typically cost, which vendors to consider, and which channels deliver the best ROI. Let's dive in.

People Also Read:

- Detailed Guide: How to Become a Loan Officer with No Experience?

- 8 Best Mortgage Lead Management Software: Efficiency Matters

- Mortgage Pipeline Management: Ultimate Guide & Best Practices

Learn Mortgage Lead Generation Statistics 2026

Before you spend a dollar, understand the marketplace and how different lead sources perform. Below, we cover: the overall market outlook for 2026, typical conversion rates by channel, and comparative ROI so you can judge which channels to prioritize for your production goals.

Mortgage Market Potential in 2026

Industry forecasts show origination volume recovering in 2026. The Mortgage Bankers Association (MBA) projects total single-family mortgage originations will increase in 2026 vs. 2025, with both purchase originations and refinance activity rebounding as rates stabilize. This recovery means a larger addressable market for originators who are ready to capture demand.

Conversion Rate of Mortgage Leads

Conversion varies widely by source and by how quickly you follow up:

- Referral / agent-sourced leads typically convert highest, which is often reported in the high teens to 30%+ range) because of pre-existing trust.

- Organic search (SEO) leads: Borrowers who find you via search or content. frequently outperform paid aggregator leads. The conservative industry ranges places organic lead conversion roughly in the 5–15% band, depending on local authority and funnel quality.

- Aggregator / shared purchased leads: commonly convert lower. often in the 1–5% range. because these prospects are shopped around and receive multiple inbound calls.

Speed-to-lead matters enormously: multiple studies show that contacting inbound mortgage/financial leads within minutes rather than hours multiplies qualification and conversion rates. Historic research and industry replications put the uplift at many times higher for first responders by HBR. Prioritize automation and immediate acknowledgement to protect conversion.

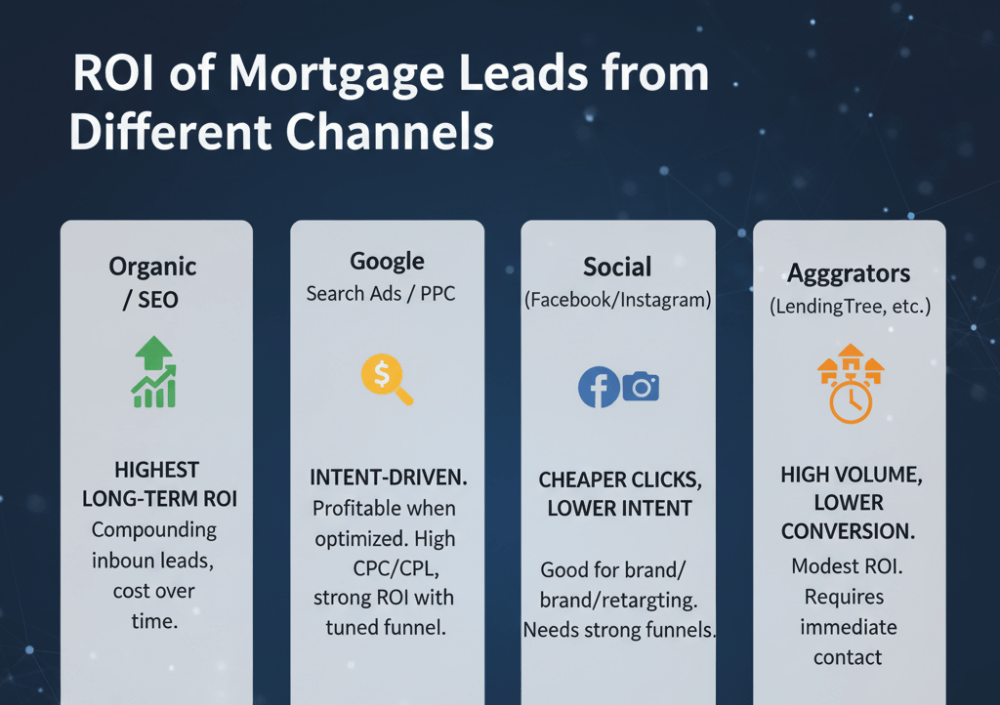

ROI of Mortgage Leads from Different Channels

ROI depends on your loan size, team efficiency, and conversion rates, but these patterns recur:

- Organic / SEO: highest long-term ROI. Upfront time and content investment pay off with compounding inbound leads and lower per-lead marginal cost over time.

- Google Search Ads / PPC: intent-driven. It can be profitable when optimized. Industry benchmarks show search CPCs and CPLs for mortgage keywords are relatively high, but optimized campaigns often return multiple dollars for every ad dollar when funnel and conversion are tuned.

- Social (Facebook / Instagram): cheaper clicks but lower intent. It can work well for brand-building, retargeting, and first-time buyer audiences when combined with strong funnel flows.

- Aggregators (LendingTree, Bankrate, Lendgo, etc.): high volume, but lower conversion and more competition. ROI can be modest if your contact processes aren't immediate and relentless.

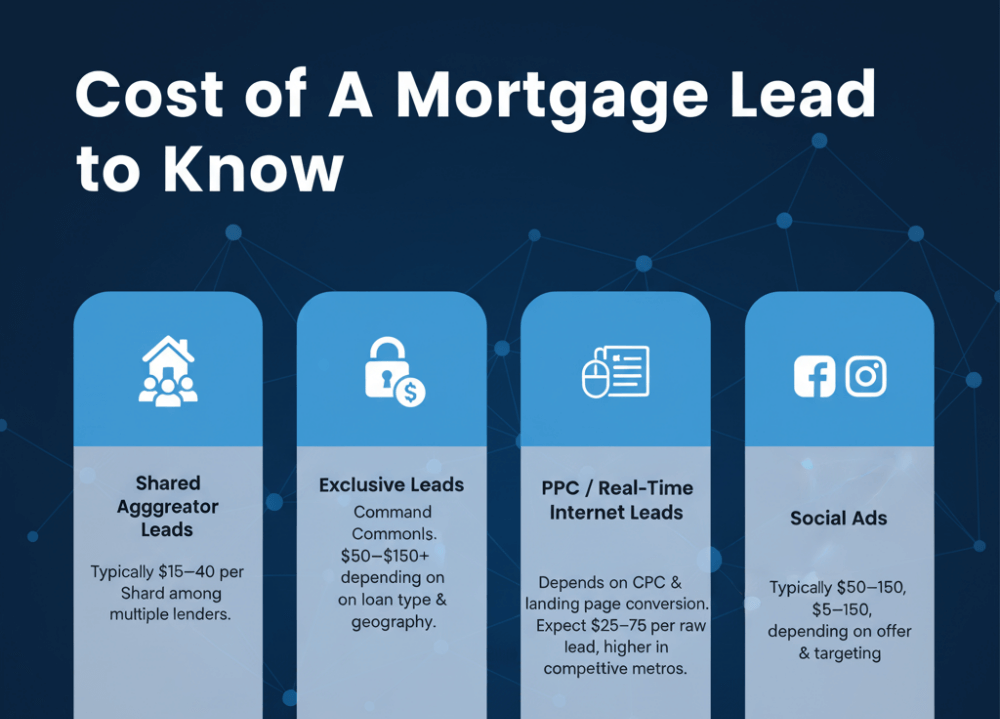

Cost of a Mortgage Lead to Know

Lead prices vary widely by exclusivity, intent, and channel:

- Shared aggregator leads: typically $15–40 per lead in many markets and shared among multiple lenders.

- Exclusive leads: command premiums. commonly $50–$150+, depending on loan type and geography.

- PPC / real-time internet leads (landing page → form): costs depend on CPC and landing page conversion. expect $25–$75 per raw internet lead in many markets, with higher CPLs in competitive metro areas.

- Social ads: typical CPLs range broadly from $50–$150, depending on offer and targeting.

How to evaluate price: calculate your acceptable Cost-Per-Funded-Loan:Max CPL = (Average Commission per Funded Loan) × (Targeted % of revenue you'll reinvest in acquisition) × (1 / Expected lead→fund conversion). If a lead source pushes your CPL below that threshold and the leads are real, scale up.

Best Mortgage Lead Generation Companies

Your first thought must be buying mortgage leads from generation companies. Here are five ones for you to consider.

#1 Zeitro

Zeitro is an industry-focused AI SaaS that helps loan officers create SEO-optimized personal microsites and speed up borrower qualification with AI tools. Zeitro's Growth Hub lets loan officers publish a branded microsite for free, embed rate quote tools and calculators, and surface content that attracts organic search traffic. Turning searchers into warm inbound leads. Zeitro also markets product features that streamline guideline lookups and borrower intake.

Key Features:

- Personal branded microsite with SEO optimization for organic lead capture

- Real-time rate quote engine covering conventional, Non-QM, and private lending

- Affordability calculator that keeps prospects engaged on your site

- GuidelineGPT for instant, accurate answers across multiple loan programs

- AI-powered income calculation with 85%+ accuracy

- Digital 1003 application with 90%+ completion rates in 5 minutes

- Integration with leading lenders and wholesalers for comprehensive pricing

- Open House Finder connecting you with real estate professionals

#2 LendingTree

LendingTree runs one of the largest online lending marketplaces in the U.S., matching borrowers to multiple lenders via a comparison funnel. Lenders buy those consumer requests as leads. Because multiple lenders often receive the same lead, speed and follow-up quality determine conversion success. LendingTree is strong for loan officers who can respond instantly and compete on pricing and service.

Key Features:

- High-volume lead flow from established consumer brand

- Pre-qualified borrowers who have expressed mortgage intent

- Multiple loan types including purchase, refinance, and home equity

- Detailed borrower information including credit score ranges and loan amount

- Real-time lead delivery for immediate follow-up opportunity

- Geographic and loan type filtering options

- Mobile-optimized lead management interface

- Integration capabilities with CRM systems

#3 LendingPad

LendingPad is primarily a modern cloud LOS that also offers borrower-facing point-of-sale tools and co-branded borrower portals. For LO teams that want an end-to-end digital loan flow (POS → LOS), LendingPad helps capture and convert borrowers coming from your own marketing or referral sources, effectively turning origination technology into a lead-capture channel.

Key Features:

- Borrower-facing digital application portal for lead capture

- Seamless online document upload and loan tracking functionality

- Co-branding options to maintain your professional identity

- Integration with wholesale lenders for expanded product offerings

- Real-time collaboration tools for team-based lead management

- Automated compliance and reporting to ensure regulatory adherence

- Mobile accessibility for on-the-go lead response

- API connectivity with marketing and CRM platforms

#4 Lendgo

Lendgo is a consumer mortgage marketplace that matches borrowers with lenders after they complete a request form. Lendgo emphasizes comparison shopping and matching borrower profiles with participating lenders, which can produce higher intent leads when borrowers are actively comparing offers.

Key Features:

- Borrower matching based on loan type and qualification criteria

- Real-time lead delivery notifications for fast response

- Detailed borrower financial profiles including income and assets

- Competitive marketplace with transparent pricing expectations

- Lead quality filters to reduce unqualified prospect volume

- Dashboard for tracking lead status and conversion metrics

- Multi-channel lead sources including web, mobile, and partner sites

- Flexible purchasing options including shared and exclusive leads

#5 Bankrate

Bankrate is a high-traffic personal finance publisher that generates leads via rate tables, calculators, and editorial content. Leads from Bankrate often come from shoppers who have researched extensively. That can mean better lead quality, although these leads are commonly sold to multiple lenders. Bankrate also offers advertising/rate table placements for lenders.

Key Features:

- Access to highly trafficked financial comparison site

- Educated borrowers who have researched options before submitting

- Comprehensive borrower data including loan purpose and timeline

- National coverage with geographic targeting capabilities

- Multiple loan product types including conventional and government programs

- Real-time rate integration for competitive positioning

- Brand credibility that provides third-party validation

- Performance analytics and lead source tracking tools

Best Ways to Buy Mortgage Leads Online

Below, I compare the main online channels and what you should expect.

Organic Traffic

Organic search. owned content, local SEO, and SEO-optimized microsites. produces the most consistent warm inbound leads over time. The advantage: compounding returns and usually higher conversion rates because searchers actively seek mortgage help. Zeitro's Growth Hub is an example of how a loan officer can build organic visibility without ongoing per-lead purchase costs. Invest in localized content (city + loan type), calculators, and clear CTAs for best results.

Google Search Ads

Google Search Ads target active searchers and therefore, can drive high-intent traffic quickly. Benchmarks (industry PPC reporting) show mortgage keywords are competitive. CPCs can be high, and CPLs depend heavily on landing page performance. With disciplined funnel optimization and good landing pages, Google Ads often deliver strong ROI. Use geo-targeting, tight keyword match types, and conversion-focused landing pages to control CPL.

Facebook/Instagram

Social advertising is powerful for reach, audience building, and retargeting. Costs per click are generally lower than search, but intent is lower too. expect lower raw conversion rates unless the campaign uses strong retargeting and educational content to warm prospects before asking for contact details. Video and webinar sign-ups perform particularly well for first-time buyer audiences.

LinkedIn is more expensive per click but useful when you target high-income prospects (jumbos, physician loans, executive relocation) or when your product needs professional targeting. Expect higher CPLs but potentially larger loan sizes and LTVs that justify the spend in specialized niches. Recent benchmarks put LinkedIn CPCs higher than social platforms, but with higher lead quality for B2B/professional audiences.

Get Mortgage Leads Through Local Workshops and Webinars

Running local seminars and webinars is an often-underused channel that builds trust and captures warm leads. First-time homebuyer workshops typically attract 15–30 attendees. conversion from attendee → qualified lead can be high (industry estimates often show double-digit conversion rates for education attendees).

Costs are modest (local venue, refreshments, promotion), and webinars are even cheaper. Combine these events with a robust follow-up sequence and a dedicated post-event landing page to convert attendees into applicants. Recent industry pieces show strong ROI for educational events when events are co-hosted with agents or local partners.

Conclusion

Buying mortgage leads can speed pipeline growth, but the smartest originators balance purchased volume with owned channels. Organic search (SEO + personal microsites) and referral partnerships deliver the warmest leads and the best long-term ROI, while paid channels (search, social, aggregators) are powerful for targeted, short-term volume if you measure CPL and speed-to-lead closely.

Why Zeitro matters in this mix: Zeitro provides tools that help LOs build owned organic channels like branded microsites, calculators, and AI intake, so you rely less on expensive, shared leads and more on warm prospects you control. If you're buying leads now, pair that spend with an investment in a personal organic funnel. That's how most high-performing originators reduce acquisition costs over time.

![[Solved] How to Calculate Commission Income for Mortgage?](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/6a3ce1b02009d0aba39b3174_how-to-calculate-commission-income-banner.png)