Written by

Eric

Share this article

.svg)

Subscribe to updates

Last checked and updated on July, 2026

Quick answer: Loan officers earn a median wage of $74,180 a year, according to the Bureau of Labor Statistics' most recent full-year figures. But that number blends bank tellers writing car loans with commissioned mortgage originators, so it undersells what a busy MLO actually takes home. Once you factor in commission, mortgage-specific loan officers typically land somewhere between $88,000 and $135,000, and top producers regularly clear $200,000 or more. Location, lender type, and how many loans you close each month all swing that range hard.

I've been in the industry long enough to know that when someone asks, "How much does a loan officer make?", the only honest answer is: it depends.

Are you looking at those flashy recruitment ads promising $200k in your first year? Or are you scrolling through Reddit threads where people vent about market cycles? I've seen both sides. The reality is that mortgage loan officer salaries have a massive variance. You aren't just getting a paycheck. You're hunting for one. Your income is directly tied to your hustle, your network, and honestly, how efficiently you can close deals without drowning in paperwork.

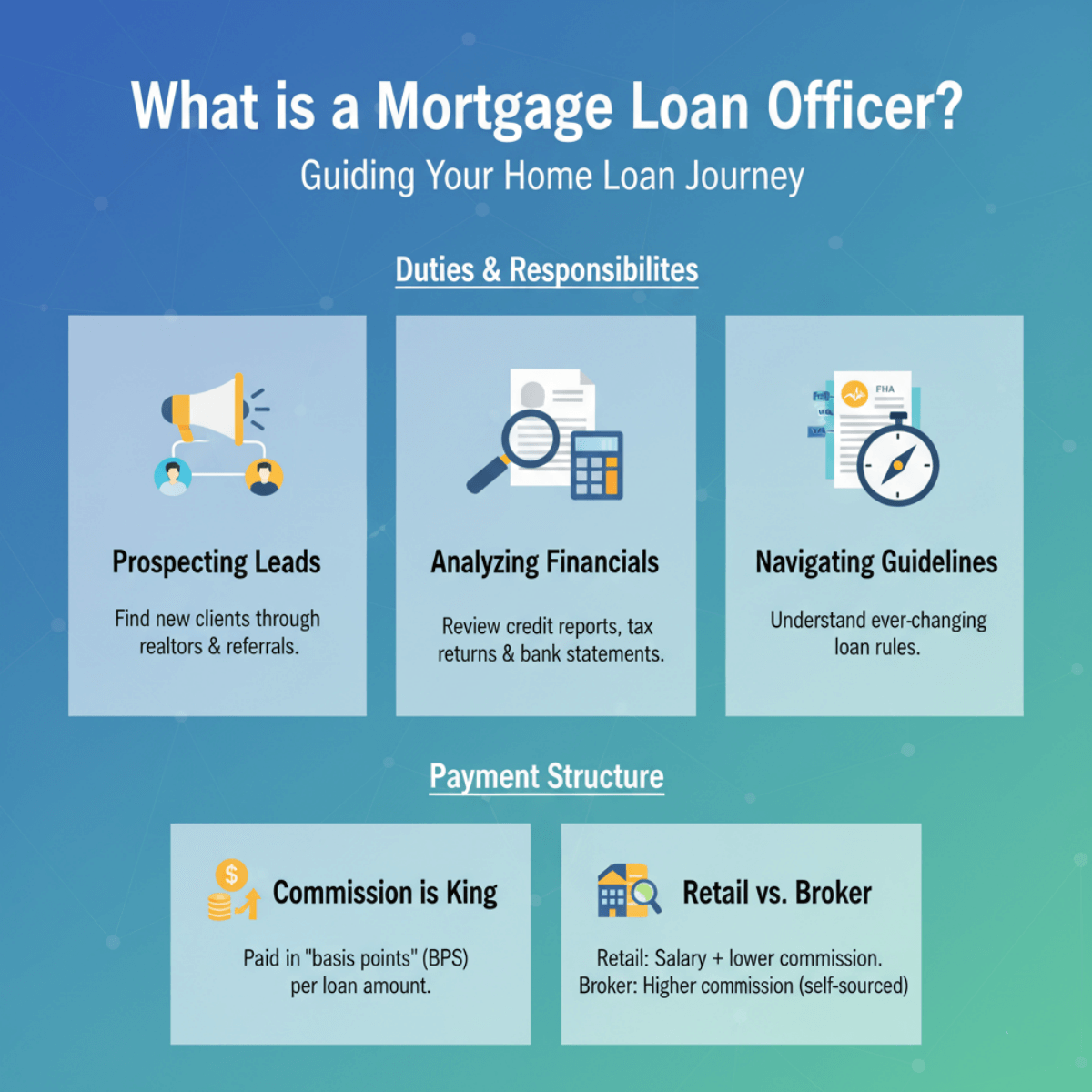

What is a Mortgage Loan Officer?

Simply put, we are the bridge between a borrower's dream home and the bank's money. A Mortgage Loan Officer (MLO) guides applicants through the complex approval process, ensuring they get the right loan product while protecting the lender's interest. It's equal parts sales, financial counseling, and problem-solving.

Also Read: Mortgage Underwriter vs Loan Officer: Which Career Is Best?

Duties and Responsibilities

If you think this job is just shaking hands and quoting rates, think again. Here is what the daily grind actually looks like:

- Prospecting Leads: This is the lifeblood of the job. You need to constantly find new clients through realtors, builders, and past referrals.

- Analyzing Financials: You'll spend hours digging through credit reports, tax returns, and bank statements to determine eligibility.

- Navigating Guidelines: This is the tricky part. You must understand the ever-changing rules for Fannie Mae, FHA, VA, and Non-QM loans to structure deals that actually close.

- Ensuring Compliance: One mistake here can kill a deal or cost you your license. You manage the file from the application to the closing table.

Payment Structure

Forget the idea of a flat paycheck — most originators live and die by commission.

- Commission is King: We are typically paid in "basis points" (BPS). For example, if your commission is 100 bps on a $500,000 loan, you make $5,000.

- Retail vs. Broker: Retail lenders often offer a small base salary plus lower commission (e.g., 50-80 bps) and provide some leads. Mortgage brokers usually offer zero base salary but much higher commission (e.g., 100-200+ bps) because you hunt your own food.

- The "Draw": Some companies offer a "draw against commission," meaning they advance you a monthly paycheck, but you have to pay it back from your future commissions.

How Much Does a Loan Officer Make Per Loan?

Here's the simplest way to picture it: multiply your commission rate by the loan amount. A 75-bps plan on a $350,000 loan pays $2,625. Bump that to 150 bps on a $600,000 loan and you're looking at $9,000 for one file. Volume and average loan size, not hours worked, are what actually move the needle on annual income.

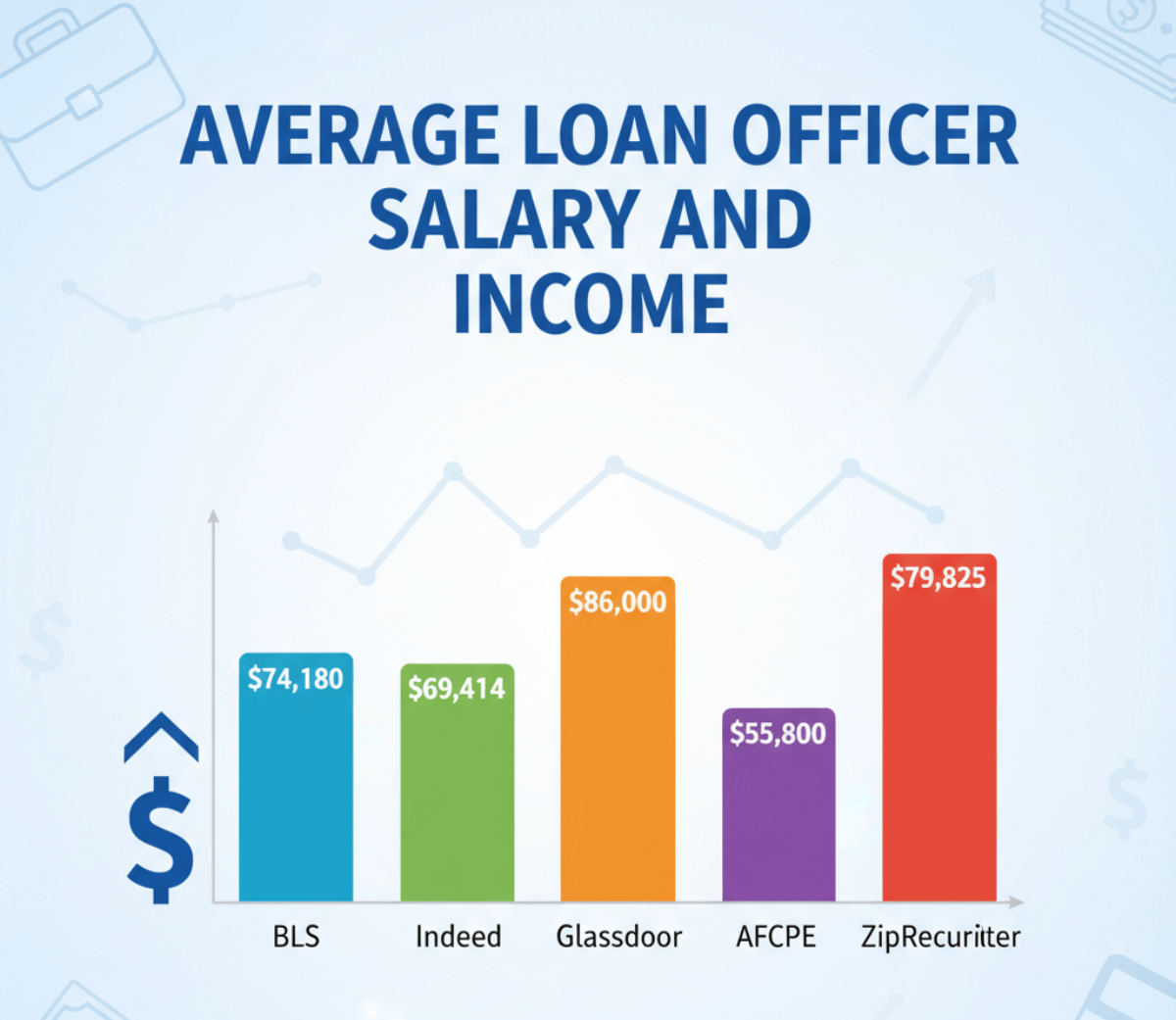

Average Loan Officer Salary and Income

Every platform gives you a different number because they average out the top producers with the part-timers. Context is everything. Geography also plays a massive role. Higher home prices mean bigger loan amounts and fatter commission checks.

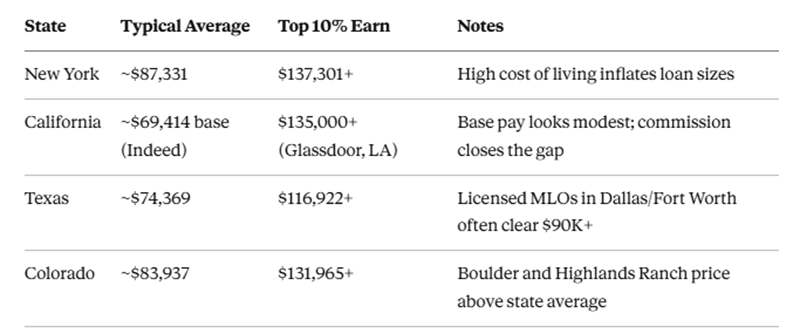

According to recent data, the top 5 highest-paying states for loan officers in 2024-2025 often include high-cost areas like New York, California, Massachusetts, Washington, and Colorado.

U.S. Bureau of Labor Statistics

The BLS figure is worth a closer look because it's the most conservative number out there, and also the most misunderstood. Their $74,180 median lumps mortgage specialists in with general loan officers, including people processing auto loans at a bank branch nine-to-five. A more recent BLS wage release, covering a later survey period, already shows the mean climbing to $87,790 nationally — a signal that the 2026 rate environment is putting more money back into originators' pockets. Commission-heavy MLOs working full pipelines routinely beat both figures.

Indeed's postings for "Licensed MLO" or "Top Producer" roles often show realistic earning potential between $88,000 and well over $120,000 a year once commission is added back in, especially in high-volume metros.

The BLS tends to be the most conservative source. For May 2024, they reported a median annual wage of $74,180 for loan officers.

However, keep in mind that the BLS lumps "Mortgage Loan Officers" in with general "Loan Officers" who might work 9-to-5 at a local bank branch, handling auto loans. That drags the average down. Specialized MLOs who hustle often see numbers significantly higher than this median.

Indeed

Indeed's data is often more reflective of current job postings. For late 2025 in a high-volume market like California, the average base salary is reported to be around $69,414, but this is misleading without commission.

When you factor in commission-heavy roles, Indeed listings for "Top Loan Officers" or "Licensed MLOs" often show earning potential ranging from $88,000 to well over $120,000 annually, depending on volume.

Glassdoor

Glassdoor gives us a better look at "Total Pay." For a major metro area like Los Angeles, reports in late 2025 suggest an average total compensation of around $86,000, with a very wide range.

The "Additional Pay" (commission/bonuses) component is huge here. Glassdoor data indicates that while the base might be modest, the top earners (90th percentile) in these hubs are clearing $135,000+, proving that experience and a strong pipeline make all the difference.

AFCPE

The Association for Financial Counseling & Planning Education (AFCPE) provides a broader view of financial professionals. Their data for December 2025 suggests a national average for Mortgage Loan Officers around $55,800, with top earner scrossing $104,000.

Interestingly, they highlight a massive disparity by state. For example, their data shows Texas MLOs averaging higher than the national mean, while other regions lag, reinforcing that your zip code dictates your paycheck.

ZipRecruiter

ZipRecruiter is great for seeing the spread between "Entry Level" and "Pro." As of December 2025, they see a national average of roughly $79,825.

But look at the percentile spread: the 25th percentile (newbies) is around $52,000, while the 75th percentile is nearly $100,000. If you are in the top 10% of earners, you are looking at $125,500+. This gap proves that in this industry, you eat what you kill.

Salary by State: Location Changes Everything

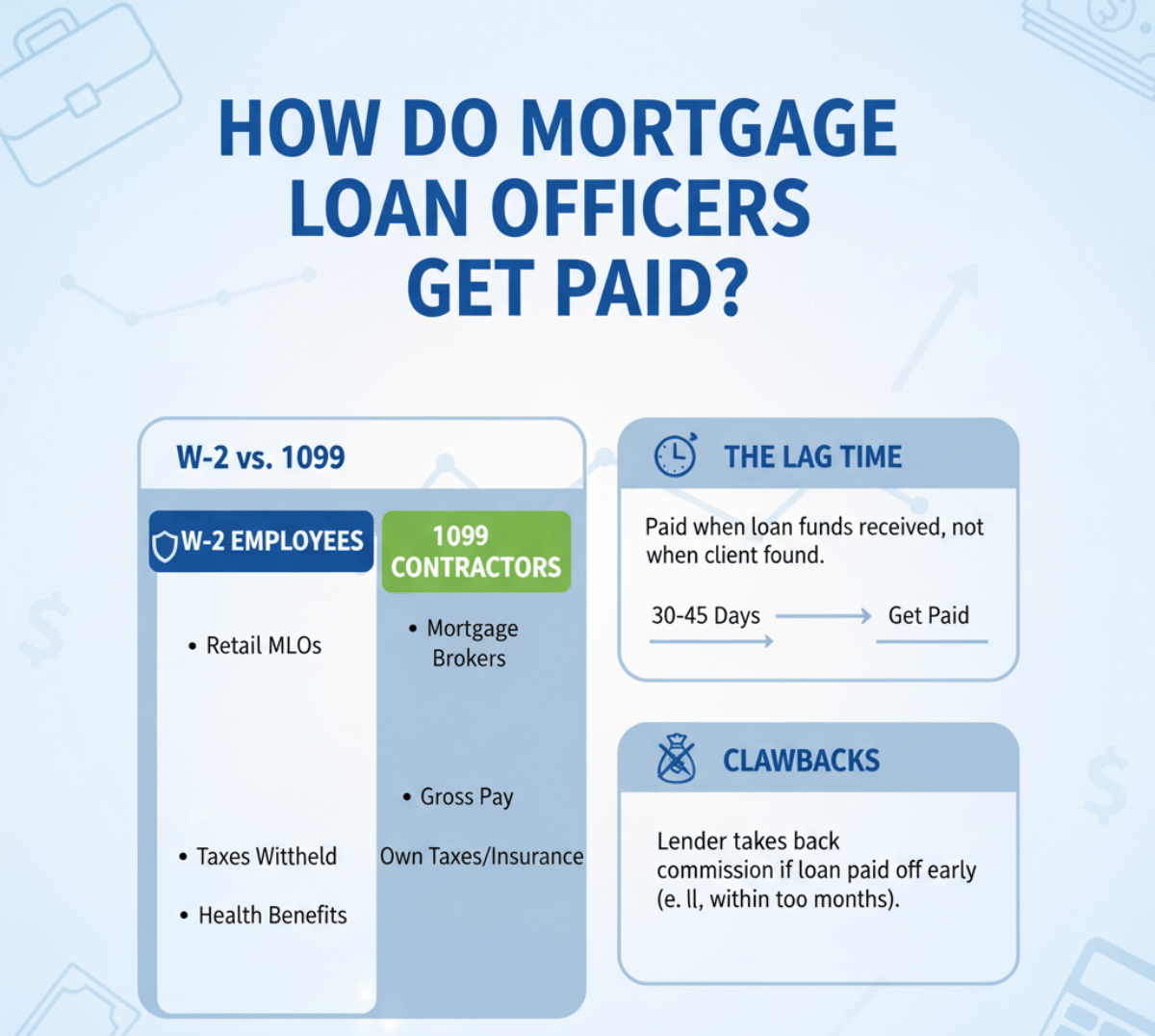

How Do Mortgage Loan Officers Get Paid?

Understanding how the money hits your account is as important as how much.

- W-2 vs. 1099: Most retail MLOs are W-2 employees, meaning taxes are withheld, and you might get benefits like health insurance. Mortgage Brokers are often 1099 independent contractors. You get the gross check, but you pay your own taxes and health insurance.

- The Lag Time: You don't get paid when you find a client. You get paid when the loan funds are received. This means you might work for 30-45 days on a deal before seeing a dime.

- Clawbacks: If a borrower pays off their loan too early (usually within 6 months), the lender might take back your commission. It's painful, but it happens.

The W-2 vs. 1099 Split (And Why It Matters for Your Take-Home Pay)

Most retail loan officers are W-2 employees — taxes get withheld, and benefits like health insurance are usually part of the package. Independent brokers are frequently 1099 contractors instead: you collect the full commission check but cover your own taxes and insurance out of pocket.

There's also a lag most new originators don't expect. You get paid when the loan funds, not when the client signs an application — meaning a single file can take 30 to 45 days to turn into an actual deposit. And if a borrower refinances or pays off the loan within roughly six months, some lenders will claw back part or all of your commission on that file.

Also Read:

- 1099 Form vs W2: What's the Difference? Details Here

- 1099 Form Explained: What Is It? What Is Used for?

How to Become a Mortgage Loan Officer?

Getting into the industry is straightforward, but staying in is the hard part. Here's how to become a mortgage loan officer.

- Meet the Criteria: You generally need to be 18+ and pass a background check (credit issues can be a blocker).

- Pre-Licensure Education (PE): You must complete 20 hours of NMLS-approved education.

- Pass the SAFE Exam: This is the big hurdle. It covers federal law, ethics, and non-traditional mortgage lending.

- Find a Sponsor: You can't just hold a license. A lender or broker must employ (sponsor) you to activate it.

Is it hard to make it as a loan officer? Yes. The washout rate is high. Many new LOs quit in the first year because they underestimate the difficulty of building a referral network from scratch while surviving months without a commission check.

Is Being a Mortgage Loan Officer a Good Career in 2026?

For the right kind of person, yes — but it's not for everyone. This job is highly cyclical: when interest rates soften, business picks up fast; when rates climb, pipelines can dry up just as quickly.

If you're a self-starter who genuinely likes solving financial puzzles and helping people buy homes, though, there's no real income ceiling. Plenty of experienced MLOs out-earn doctors without carrying medical-school debt, and the flexibility to essentially run your own small business inside a larger company is hard to match elsewhere.

Tip: How to Improve Your Income As a Loan Officer?

Here is the secret top producers know: Income = Volume × Efficiency.

You can't manufacture more hours in the day. To break through the income ceiling, you have to stop doing manual grunt work and start using tools that multiply your effort. This is where leveraging platforms like Zeitro and Bluerate changed the game for me.

- Stop "Pdf-Diving": I used to waste hours manually searching through Fannie Mae or Freddie Mac guidelines to see if a weird borrower scenario would fly. Now, I use Zeitro's Scenario AI. It lets me ask complex questions (even for Non-QM) and get instant, cited answers. This saves me 5+ hours a week that I can spend selling.

- Speed Kills: In this market, speed is your differentiator. Zeitro's platform helps deliver 2.5x faster pre-qualifications. When a realtor knows you can get a solid pre-qual letter out in minutes, not hours, they send you the leads, not your competitor.

- Accuracy is Cash: There is nothing worse than a loan dying in underwriting because you miscalculated income. Zeitro's AI Income Calculation tools increase accuracy to 85%+, helping you close 30% more loans.

- Get More Leads Automatically: Finding borrowers is the hardest part. Bluerate is a marketplace designed to fix this. You can create a free personal profile that showcases your expertise. Unlike buying cold leads, Bluerate uses SEO to put you in front of borrowers actively searching for rates in your area.

- Build Trust with Transparency: Borrowers today are skeptical. Bluerate allows you to offer real-time, personalized rate quotes (not fake teaser rates) and use an Affordability Calculator. This transparency builds trust before you even pick up the phone.

- Focus on High-Value Work: By letting AI handle the document review and guideline checking (Zeitro) and letting the marketplace bring you warm leads (Bluerate), you focus 100% on closing. That is how you double your income.

Conclusion

So, how much do loan officers make? The answer is largely up to you. You can be the median earner making $70k, or you can be the top producer clearing $200k+.

The difference isn't usually talent. It's tenacity and technology. The market in 2026 rewards those who are efficient. If you are ready to embrace the grind and equip yourself with the right tools like Zeitro to streamline your workflow, this career can be life-changing. Don't just work hard, work smart.

People Also Read

- [Tips] Where to Buy Mortgage Leads? Warm Leads for LOs

- Beginner's Guide: How to Get Leads for Mortgage Loans?

- Best CRM for Loan Officers: Which One Suits You Most?

- Best Mortgage Loan Officer Training: Which to Pick?