.webp)

As mortgage loan officers, my team and I frequently encounter buyers asking if they can use their higher, current-year income instead of the lower numbers on their past tax returns. It is a common dilemma, especially after a promotion or a strong business year. The short answer is yes, but the path depends heavily on whether you are a W-2 employee or self-employed.

Key Takeaways

If you are short on time, here is what we look for when evaluating your current-year earnings:

- W-2 Employees: For many W-2 borrowers, lenders primarily verify current income with recent pay stubs, W-2s, and employment verification, though additional documents such as tax returns may still be required depending on the loan program and the income structure.

- Self-Employed Borrowers: Self-employed borrowers are often underwritten using an average of two years of tax returns, although some programs offer limited exceptions or alternative documentation, such as bank statement-based non-QM loans.

How Lenders Evaluate Current Year Income vs. Tax Returns

Understanding how underwriters view current income is the key to a smooth closing. This verification process is split into two distinct paths, depending entirely on how you earn your living.

If You Are a W-2 Employee

For salaried or hourly W-2 employees, utilizing current-year income is generally straightforward. In our day-to-day experience processing conventional loans, we rarely request personal tax returns for standard W-2 applicants.

Instead, underwriters prioritize your current earnings. We typically verify this using:

- Your most recent 30 days of paystubs.

- Your year-to-date (YTD) earnings shown on those paystubs.

- W-2 forms from the past two years.

- A standard Verification of Employment (VOE) with your employer.

However, if your income relies heavily on fluctuating commissions, bonuses, or overtime, we must look at a two-year average to ensure stability. If your base salary recently increased, we can usually use that higher, current rate immediately, provided the position is stable.

If You Are Self-Employed

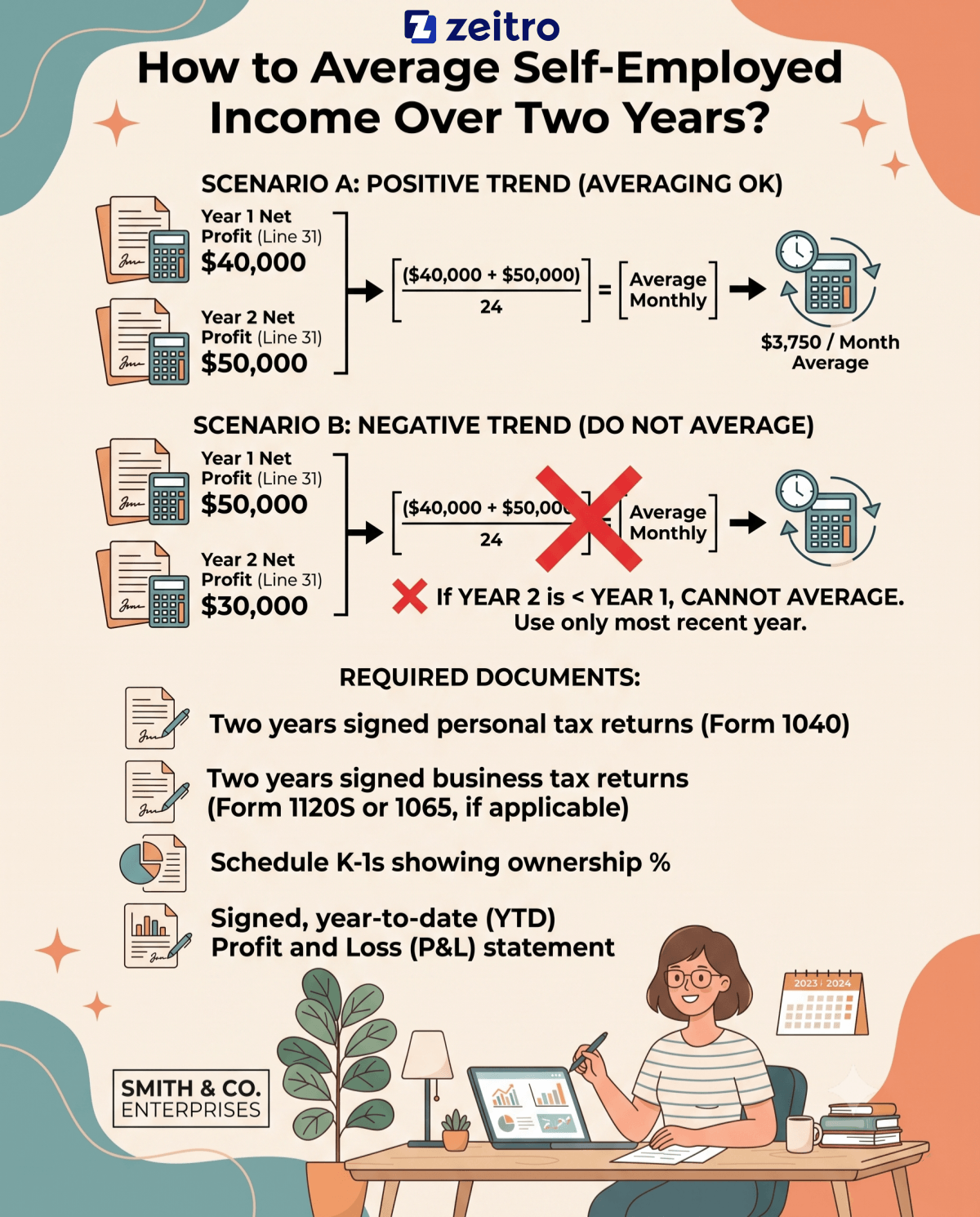

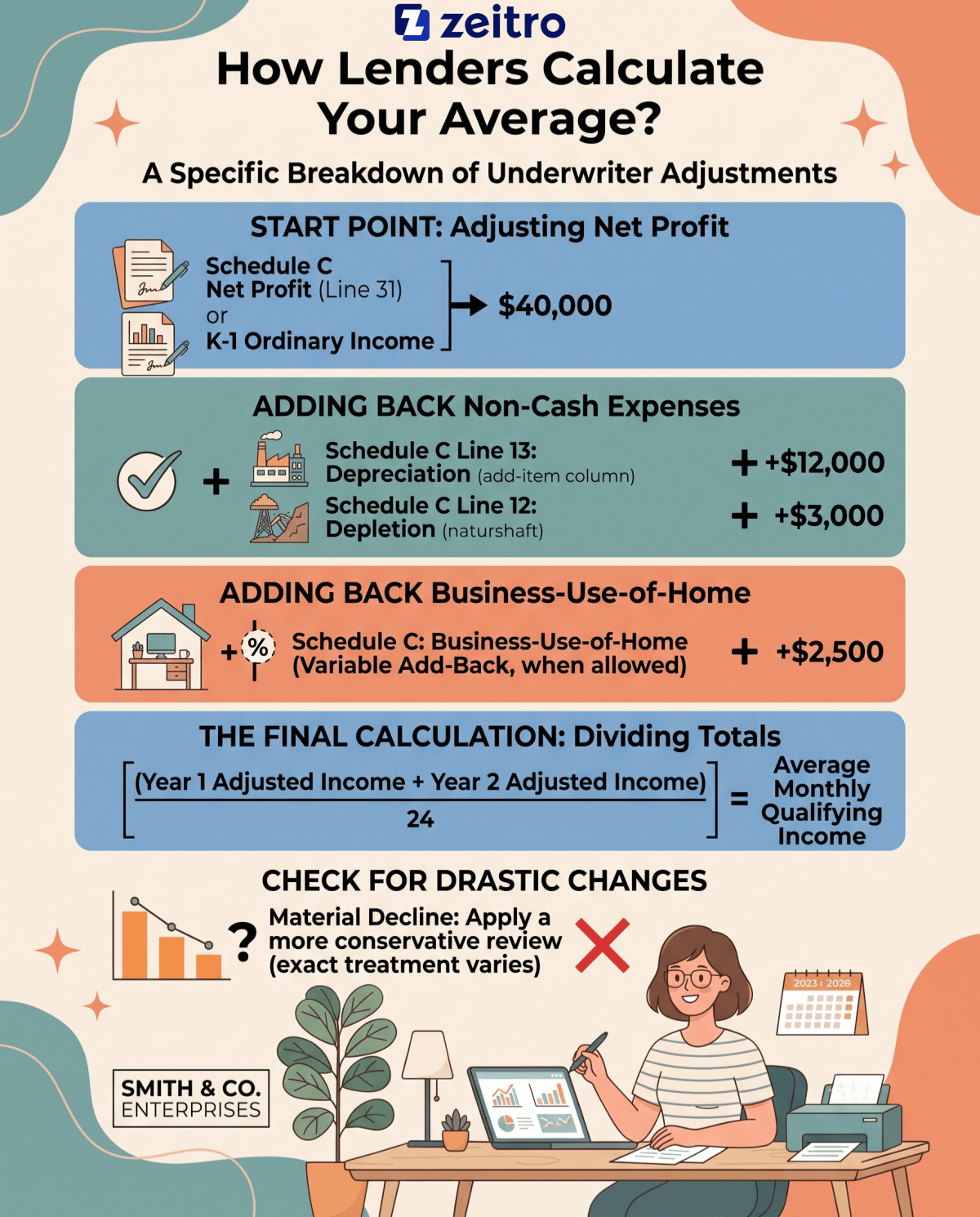

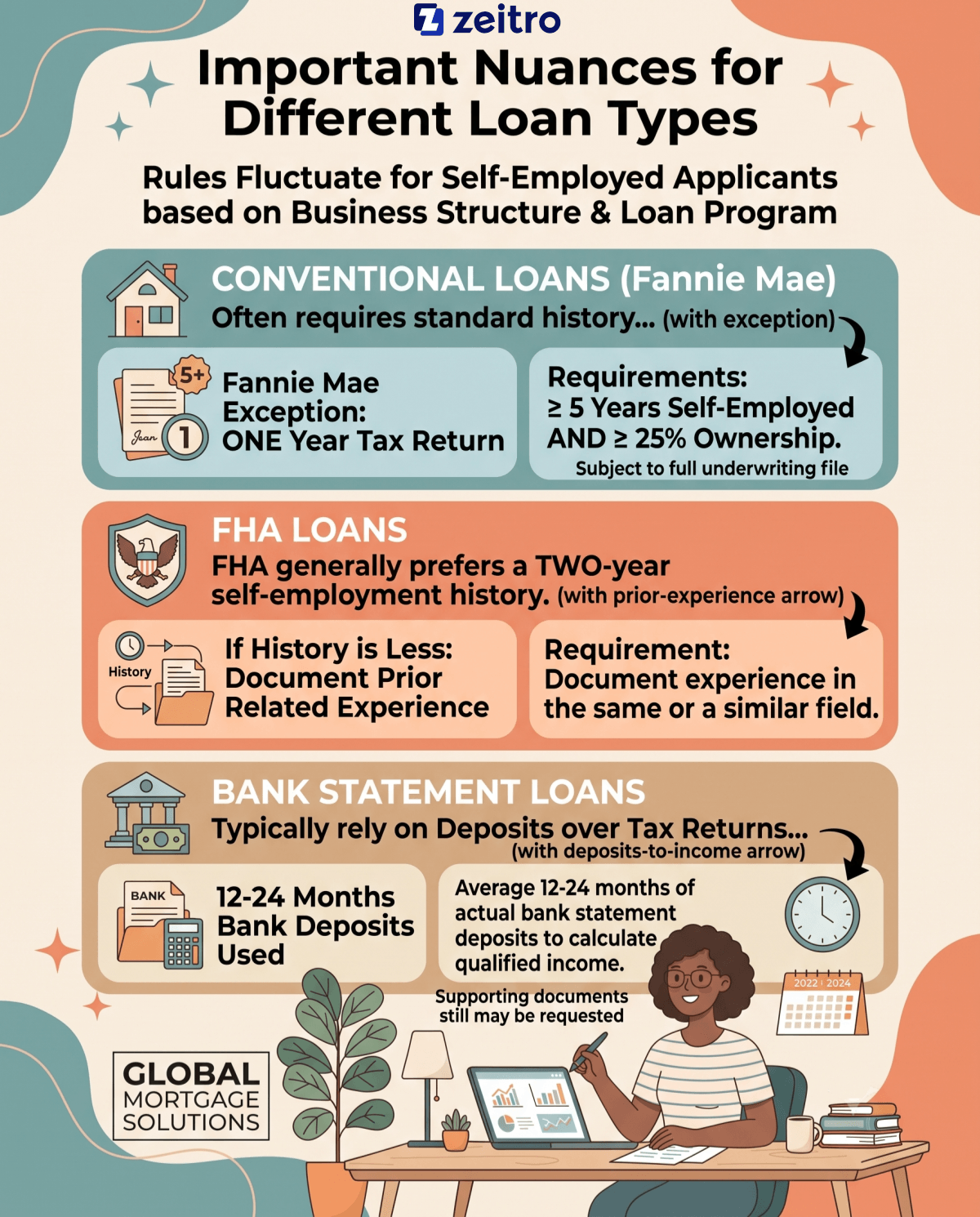

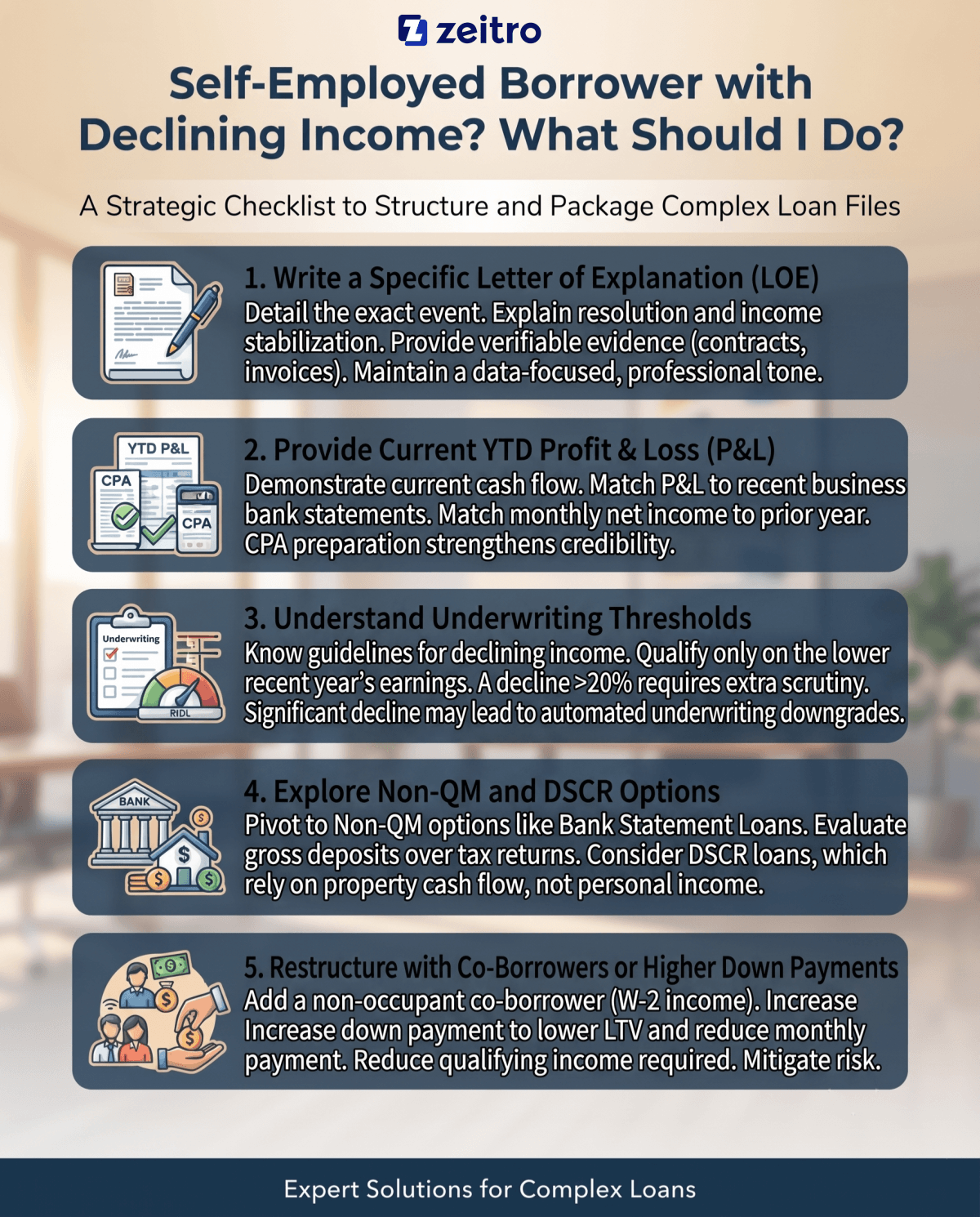

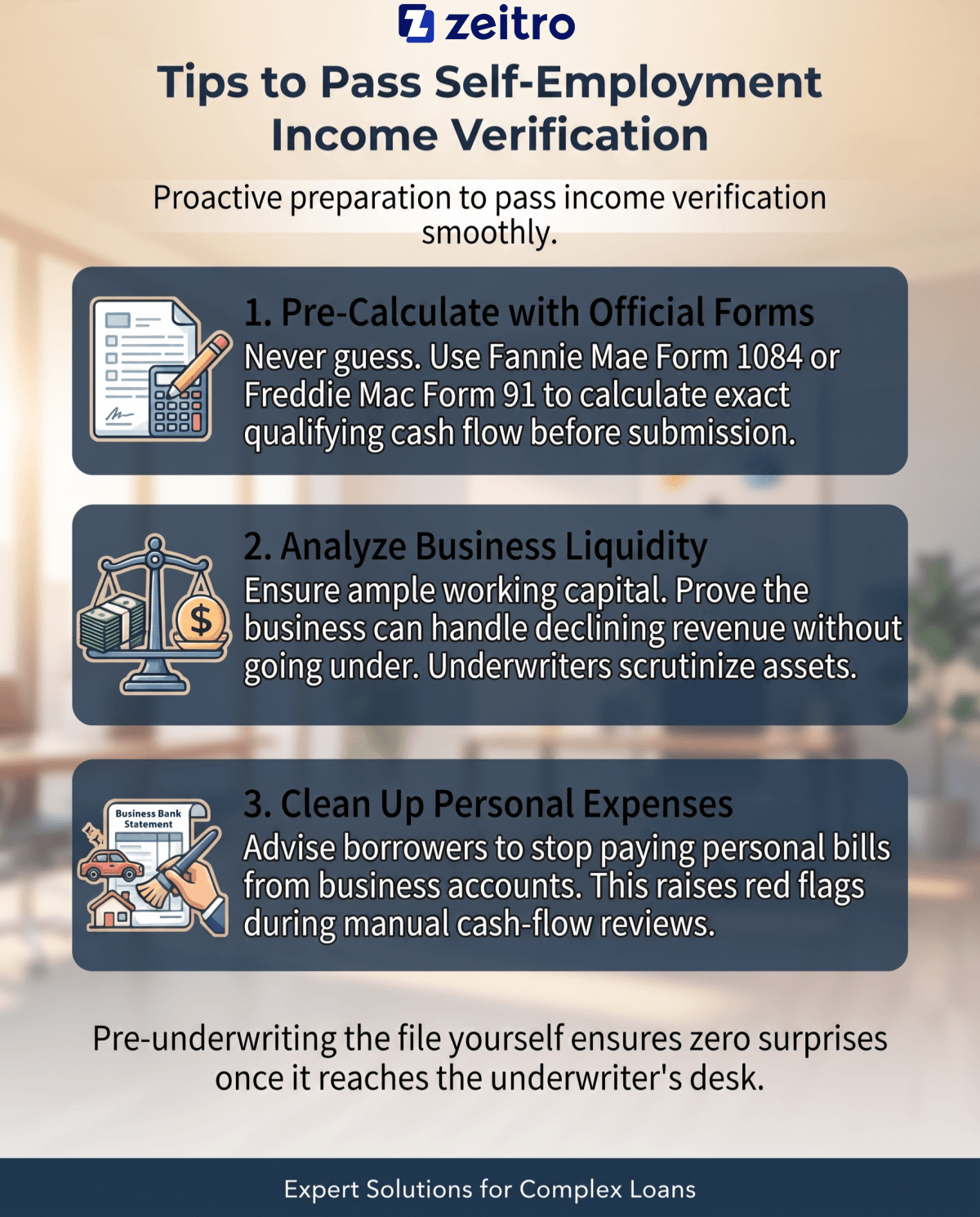

For self-employed borrowers, using only current-year income is more challenging. Traditionally, agency guidelines require a two-year average of your net self-employment income from your tax returns. However, we do have viable alternatives for growing businesses.

First, in some cases, borrowers with a business history of five or more years may be eligible for a one-year tax return exception, but approval depends on additional underwriting conditions such as ownership history, related work experience, and income stability.

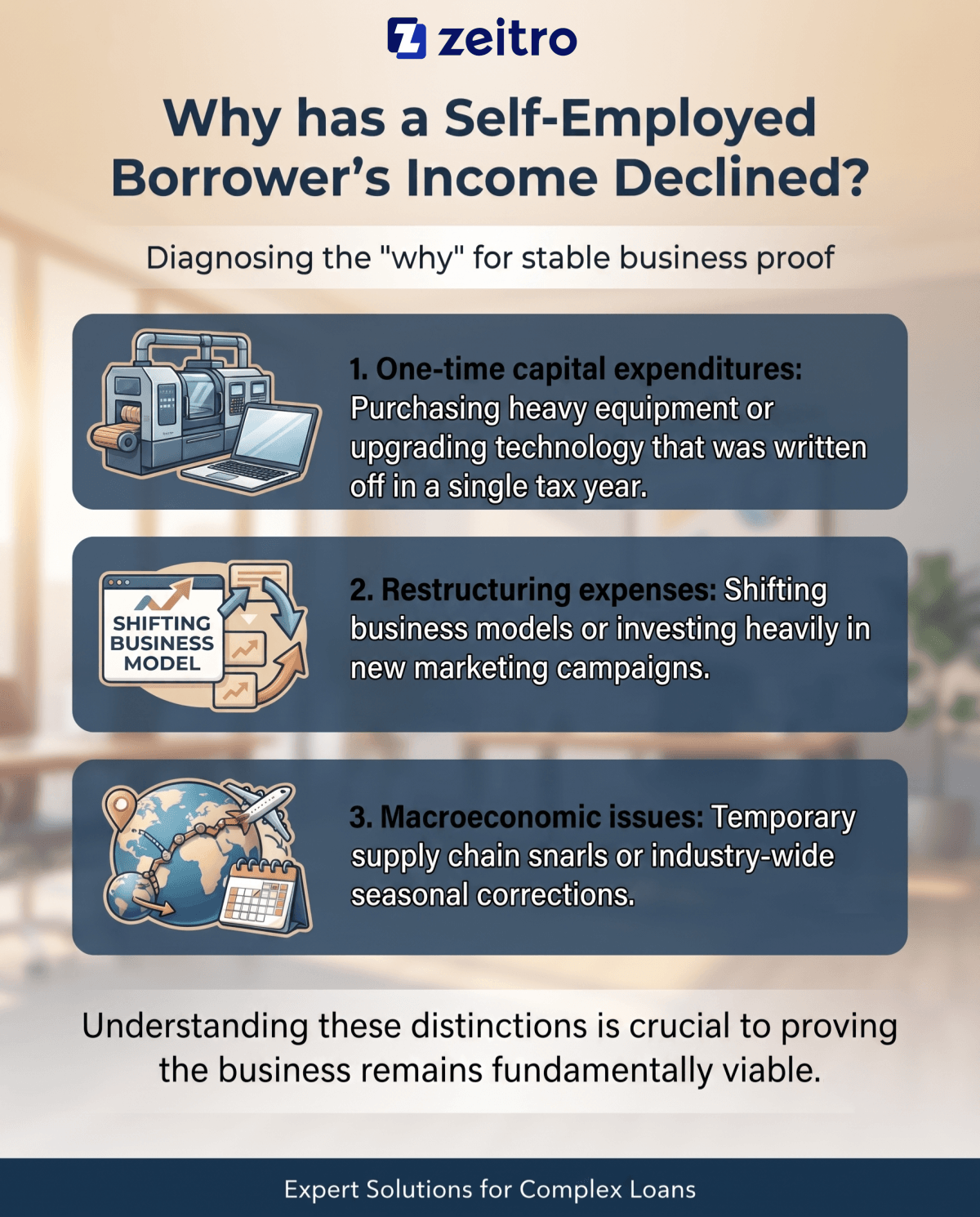

Second, if your business is booming this year but past tax returns show heavy write-offs, you can opt for a Bank Statement Loan. Bank statement loans may use 12 to 24 months of bank deposits or statements instead of traditional tax-return income analysis, although lenders can still require supporting documents. These alternative paths ensure that your hard work and recent growth are fairly represented during the approval process.

More FAQs to Explore

Q1. Can I use a tax return instead of W-2 for a mortgage?

Generally, a tax return is not a direct substitute for a W-2. Lenders may still request tax returns in some cases, but they do not replace the W-2 itself. If you are a standard employee, lenders require the W-2 because it breaks down your specific payroll taxes and withholding. If you have lost your W-2, we cannot accept a tax return as a direct substitute. Instead, we will work with you to obtain a duplicate from your employer or request a Wage and Income Transcript directly from the IRS. This ensures the underwriting file meets compliance standards.

Q2. Can I use my tax return as proof of income to buy a house?

Yes, but its necessity depends on your income type. For self-employed individuals, independent contractors, or those relying on rental income and investment dividends, tax returns are the primary proof of income we use. However, if you are a salaried W-2 employee, tax returns are usually unnecessary. We rely on your current paystubs and W-2s instead, as tax returns can sometimes complicate the approval process by revealing unrelated business write-offs or real estate losses.

Q3. Is it possible to get a mortgage without tax returns?

In some cases, a mortgage can be obtained without tax returns, but feasibility depends on the loan program, borrower profile, and documentation available. If you are a W-2 wage earner, you naturally bypass this requirement on most standard residential loans. For self-employed borrowers, we often guide clients toward Non-QM (Non-Qualified Mortgage) products.

These programs include Bank Statement Loans, which analyze business deposits, and Asset Depletion loans, which calculate monthly income based on your liquid wealth. Additionally, for real estate investors, DSCR loans bypass personal tax returns altogether, qualifying the buyer based solely on the projected rental income of the property itself. These options require slightly higher down payments but offer immense flexibility.

Q4. What is the 2 2 2 rule for mortgages?

In our industry, the "2-2-2 rule" has a couple of different meanings depending on the context. The term '2-2-2 rule' is not a standardized mortgage guideline and may be used informally in different ways by different lenders. Lenders like to see at least two active credit accounts (tradelines) that have been open for at least two years, each with a credit limit of at least $2,000.

Alternatively, some loan officers use it as a document checklist shorthand, reminding buyers to gather two years of W-2s, two months of bank statements, and two recent paystubs. Both interpretations serve as excellent benchmarks for preparing your finances.

Q5. What is the $100,000 loophole for family loans?

When helping family members buy a home, many parents offer below-market rate loans. Under IRS Section 7872, the government usually taxes the lender on "imputed interest" as if they charged market rates. However, the $100,000 loophole offers a tax-saving exception.

For certain family loans under IRC Section 7872, special rules may limit or eliminate imputed interest when the loan balance is small and the borrower's net investment income is low, but the exception is more specific than a simple $100,000 threshold.

Better yet, if the borrower's annual net investment income is $1,000 or less, the imputed interest drops to zero. Please note that this exception does not apply if the loan's primary purpose is tax avoidance, and we always advise consulting a certified public accountant to navigate these structures safely.

Q6. Can you refinance a mortgage without tax returns?

Yes, refinancing without tax returns is common. W-2 employees rarely need them for conventional rate-and-term refinances. If you have a government-backed loan, you can take advantage of streamline programs like the FHA Streamline Refinance or VA Interest Rate Reduction Refinance Loan (IRRRL). These streamline programs generally do not require full income verification or tax returns, but they still have eligibility rules and lender-specific documentation requirements. For self-employed borrowers, Non-QM refinance options also offer similar tax-return-free paths.

Conclusion

Navigating mortgage guidelines can feel overwhelming, but utilizing your current-year income is often more achievable than it seems. Whether you are a W-2 employee with a recent raise or a self-employed business owner experiencing a record year, there are tailored programs designed to fit your scenario.

To find the clearest path forward, we recommend speaking with a licensed loan officer who can run your scenario through an automated underwriting system, giving you an accurate picture of your borrowing power.

People Also Read

- How to Calculate Employment Income for a Mortgage?

- How to Calculate Self-Employed Income for a Mortgage?

- Mortgage Income Requirements: Learn Before You Apply

- Income Verification Documents: A Complete Guide for Employees and Self-Employed