Written by

Eric

Share this article

.svg)

Subscribe to updates

Let's be brutally honest for a minute. If you have spent any time scrolling through the r/loanoriginators subreddit lately, you know exactly what the atmosphere is like. You see the posts from exhausted newcomers: "I've made 500 calls this week and got zero apps," or "Is this industry even viable anymore?" The anxiety is palpable. As a new Loan Officer (LO), you are likely feeling the weight of the "feast or famine" cycle that defines our industry. You might be staring at a silent phone, wondering if you should max out your credit card on expensive leads that may never convert.

I have been exactly where you are. I know the feeling of needing a deal just to keep the lights on. But here is the good news: the "meat grinder" phase doesn't last forever if you build the right foundation. The top producers in 2026 aren't just working harder. They are working smarter by blending old-school relationship building with new-school technology. This guide isn't just theory. It's a breakdown of how to survive your first year and build a pipeline that feeds you for the next ten.

People Also Read:

- [Proven] How to Generate Mortgage Leads for Free? 6 Methods

- Best Mortgage Loan Officer Training: Which to Pick?

- 8 Best Non-QM Mortgage Lenders : Which to Choose?

- Are Mortgage Rates Expected to Go Down in 2026? Expert Forecasts

- Best CRM for Mortgage Brokers: Choose As Required

- 8 Best Mortgage Lead Management Software: Efficiency Matters

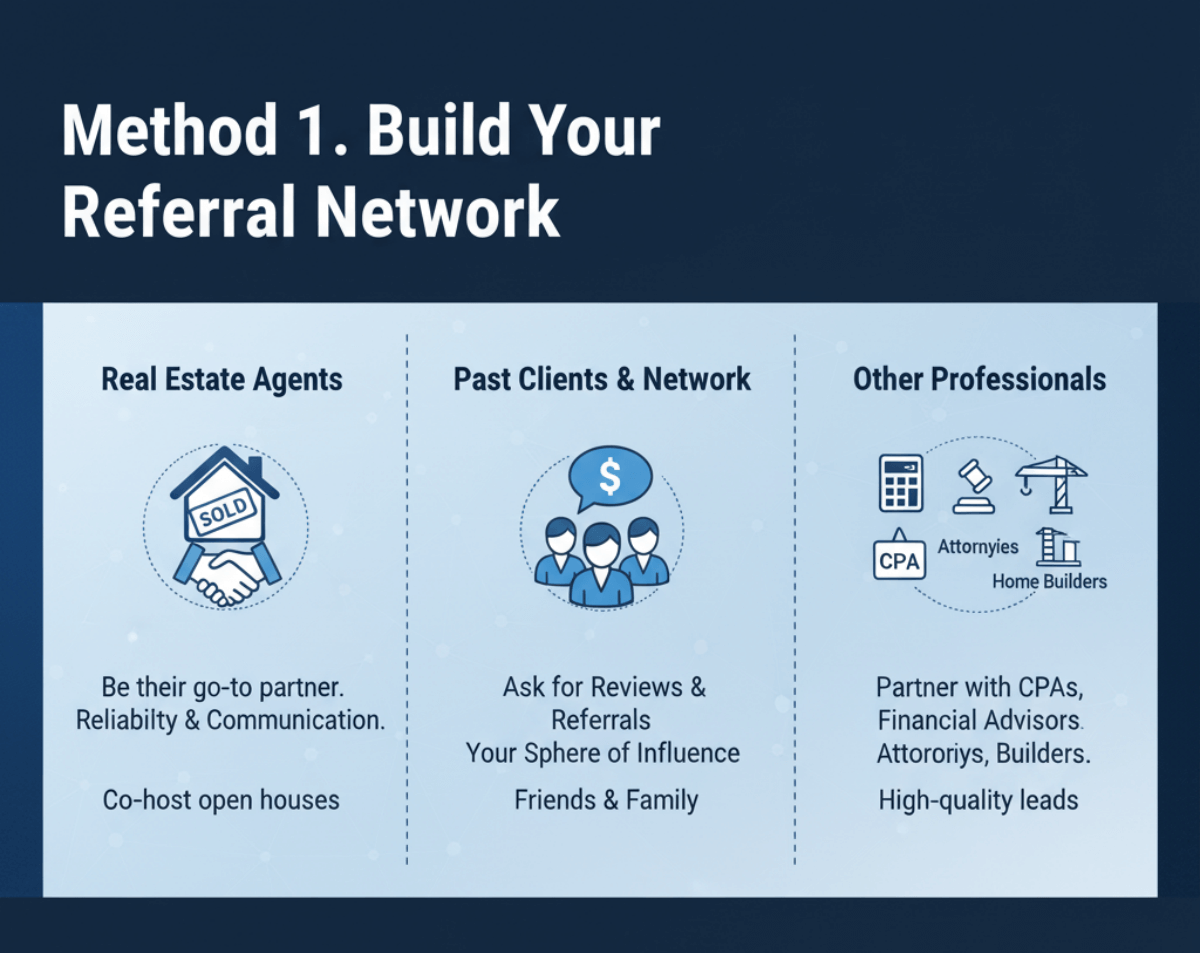

Method 1. Build Your Referral Network

Despite the rise of AI and automation, the mortgage industry remains deeply human. People don't just want a loan. They want to trust the person handling the biggest debt of their lives. Building a referral network is about planting seeds. It takes longer than buying a lead, but the fruit is much sweeter and costs you nothing but time and effort.

Real Estate Agents

Real estate agents are the traditional gatekeepers of purchase business. However, most new LOs approach this completely wrong. They call agents and essentially beg for business: "Do you have any buyers I can pre-qualify?" That is a fast track to being ignored. Agents already have a lender. You need to give them a reason to switch to you.

To become their go-to partner, you must offer value before you ask for a single lead. Value means reliability. Agents are terrified of one thing: a deal falling apart at the closing table. Be the LO who guarantees a "Pre-Approval" is solid, not just a guess. Communicate proactively, update the agent every Tuesday on the status of the file so they never have to chase you. Furthermore, help them grow. Offer to co-host open houses or help design co-branded marketing flyers. Focus on building deep, reciprocal relationships with 5 to 10 producing agents who trust you implicitly, rather than spamming 100 agents who don't know your name.

Past Clients & Network

Your "Sphere of Influence" (SOI) and past clients are your lowest-hanging fruit, yet they are often the most neglected. It is easy to close a loan, shake hands, and never speak to that borrower again. This is a massive mistake. Your past clients have already trusted you with their finances. If you did a good job, they are your best evangelists. But here is the catch: they will not refer you if you don't ask.

You need a systematic approach. I use a specific script during the "Congratulations, you are clear to close!" call, which is when the client is happiest. I say: "It has been an honor helping you get this home. My business relies entirely on people like you. If you have a friend or family member looking to buy, would you feel comfortable introducing us?" Additionally, don't forget your personal network, your dentist, your kid's soccer coach, and your barista. If the people you see every week don't know you are a mortgage expert, you are leaving money on the table.

Other Professionals

While everyone chases realtors, smart LOs diversify. Partnering with professionals like CPAs and Financial Advisors can yield some of the highest-quality leads you will ever get. Why? Because when a financial advisor refers a client, that client usually has their financial house in order, good credit, documented assets, and a clear budget. These are "slam dunk" files compared to the messy leads you might get from the internet.

Don't overlook divorce attorneys or family law practitioners. It sounds grim, but divorce often necessitates a refinance (to buy out a spouse) or a new home purchase. Being the empathetic, efficient expert in those situations can secure you a steady stream of business. Similarly, local home builders need preferred lenders to qualify buyers for their new developments. If you can prove you understand new construction nuances, you can lock in an entire subdivision of loans.

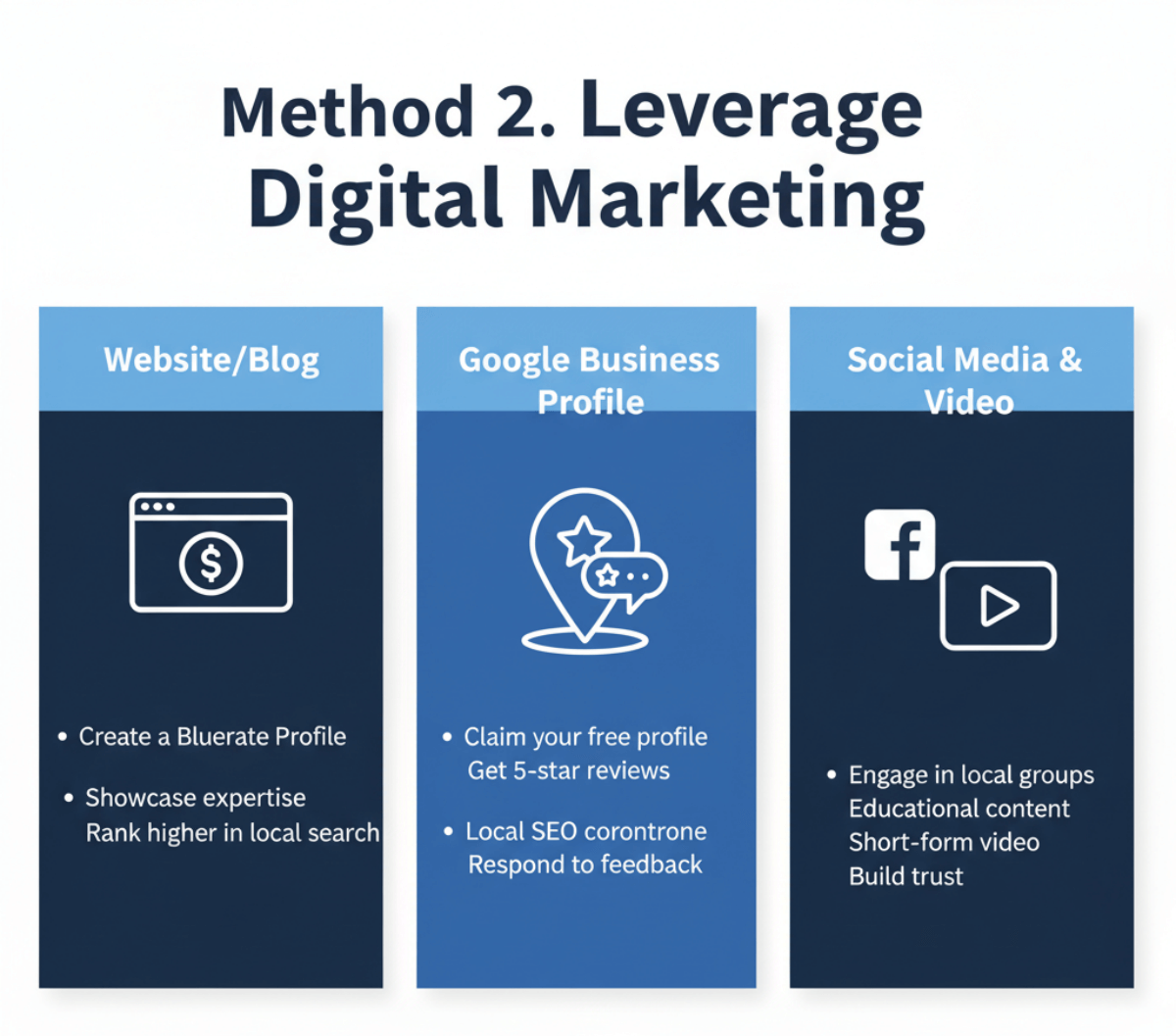

Method 2. Leverage Digital Marketing

In 2026, if you are not visible online, you do not exist. Referrals are great, but they are hard t, if you are not visible online, you do not exist. Referrals are great, but they are hard to scale. To truly grow, you need to capture the attention of the 90% of homebuyers who start their journey on the internet.

Website/Blog

Building a personal brand starts with a website, but let's be real: building a custom website is expensive, time-consuming, and incredibly hard to rank on Google. You could spend thousands on a WordPress site that no one ever sees. This is where I strongly recommend using Bluerate.

Bluerate is a marketplace designed specifically for connecting borrowers with Loan Officers. Instead of fighting an uphill battle with web design, you can create a free personal profile page on Bluerate. This isn't just a static biography. it's a functional microsite. It allows you to showcase your expertise, your photo, and your bio without needing to know a single line of code. More importantly, Bluerate invests heavily in SEO, meaning your profile has a much better chance of ranking in local searches (like "Loan Officer in [Your City]") than a personal site would. The platform drives warm leads to you, borrowers who are actively searching for rates and help, so you can focus on closing rather than coding.

Google Business Profile

If a borrower hears your name, the first thing they will do is Google you. If they see no profile, or worse, a profile with zero reviews, trust is lost instantly. You must claim your Google Business Profile. It is free and is the cornerstone of local SEO.

Fill out every section: your address, phone number, hours, and photos of yourself (not just stock photos of houses). But the real currency here is reviews. Social proof is powerful. A profile with fifteen 5-star reviews will consistently beat a veteran with 30 years of experience who has no digital footprint. Make it part of your process to send a direct link to your happy clients, asking for a review. Respond to every review, good or bad, to show that you are active and care about client feedback.

Social Media

You don't need to be an influencer with a million followers, but you do need to be present. LinkedIn is fantastic for B2B networking, connecting with realtors, CPAs, and recruiters. Share industry news, rate updates, and professional insights.

For reaching borrowers, Facebook and Instagram are key. Join local community groups (e.g., "Moms of Chicago," "First Time Buyers of Florida"). Do not spam these groups with "Call me for low rates!" Instead, watch for people asking questions. When someone posts, "Does anyone know a good lender?", reply with a helpful, non-salesy comment first, then DM them. Share content that educates: "3 Mistakes First Time Buyers Make" or "How to Buy a Home with Student Debt." Be the helpful neighbor, not the pushy salesperson.

Video Marketing

Video bridges the trust gap faster than any other medium. When a potential borrower sees your face and hears your voice, they feel like they already know you. You don't need a professional studio. Your smartphone is enough.

Focus on short-form content for TikTok and Reels. Answer the questions you get asked every day: "Rent vs. Buy," "What is DTI?", "How to improve your credit score." Explain complex topics in simple terms. This positions you as an authority. If you are camera shy, start by recording your screen and narrating over charts or rate sheets. The goal is to provide value. When people learn from you, they will eventually buy from you.

Email Marketing

Most of the leads you generate won't be ready to buy today. They might be 6 to 12 months away. If you don't stay in touch, they will forget you and use whoever is in front of them when they are ready. This is where email marketing shines.

Avoid generic, canned newsletters that just list interest rates. Send content that matters to their life stage. Send home maintenance tips, local market trends, or neighborhood news. Segment your list: renters need different emails than past clients who might want to refinance. Consistent, valuable communication keeps you "top of mind" so that when the trigger moment happens, you are the only LO they call.

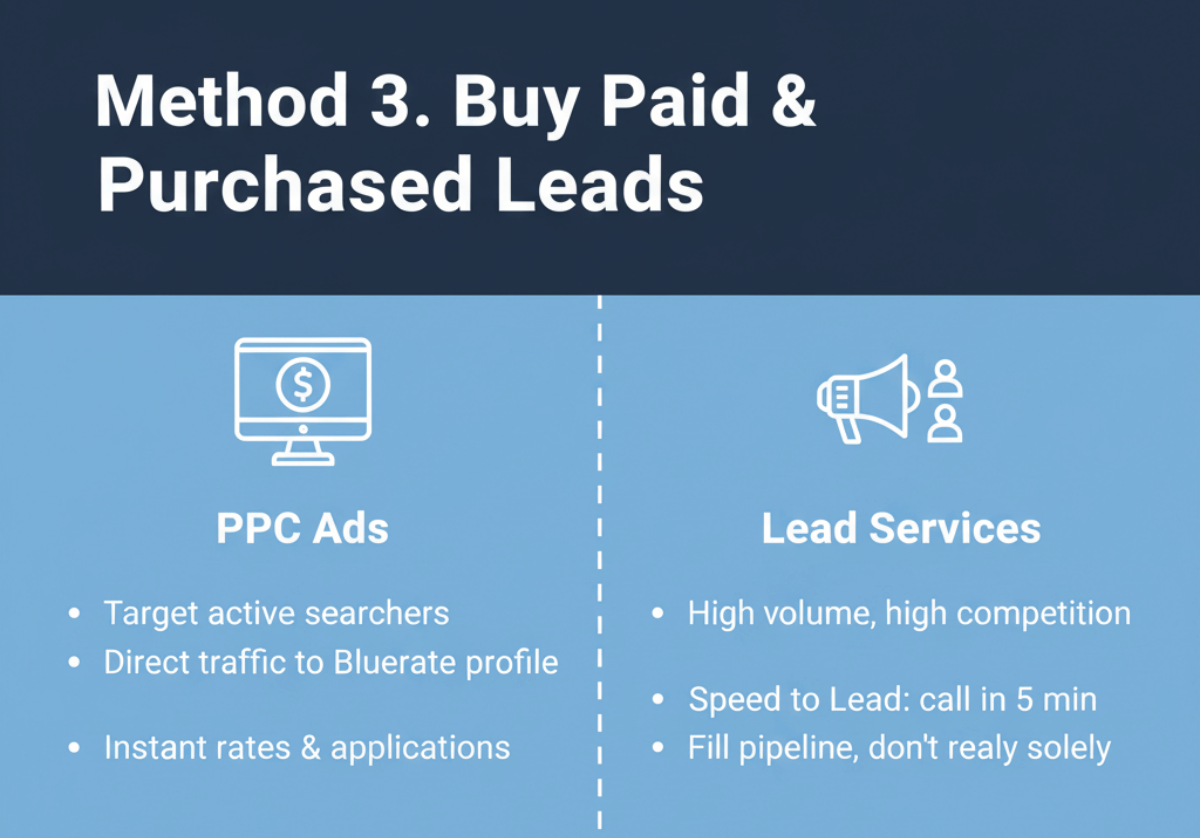

Method 3. Buy Paid & Purchased Leads

This is often called the "fast lane" to leads, but be warned: it has potholes. If you have the budget, paid strategies can bring immediate volume, but they require a rigorous follow-up system to be profitable.

PPC Ads

Pay-Per-Click (PPC) ads allow you to target people who are actively searching for mortgages right now. However, dumping ad traffic onto a generic homepage is a waste of money. Borrowers want immediate answers.

This is another area where your Bluerate profile is a massive asset. When you run Facebook or Google ads, direct that traffic to your Bluerate personal page. Why? Because Bluerate features built-in tools like "Personalized Rates" and "Digital 1003" applications. When a user clicks your ad, they can instantly see real-time rates tailored to their scenario or start an application online. This interactivity significantly increases conversion rates compared to a static contact form. You own the lead, and the user gets a seamless, tech-forward experience.

Lead Services

Best Mortgage Lead Generation Companies like Zillow or LendingTree can provide a high volume of leads instantly. The problem is quality and competition. These leads are often sold to multiple lenders simultaneously.

Success here depends entirely on "Speed to Lead." If you do not call within the first 5 minutes, your chances of conversion drop by 400%. You also need a thick skin. Internet leads are colder and more price-sensitive. You might need to call 100 leads to get 2 or 3 closings. It is a numbers game. Use this method to fill the gaps in your pipeline, but do not rely on it as your only source of business, or you will be racing to the bottom on margins forever.

Strategies to Become a Successful Loan Professional

Getting the lead is only step one. Converting that lead into a closed loan, and doing it efficiently, is where the real money is made. Here are the strategies to master the craft.

Use CRM

You cannot manage a pipeline on sticky notes or Excel spreadsheets. You will lose leads, forget follow-ups, and drown in paperwork. You need a dedicated mortgage CRM. I highly recommend looking into Zeitro. Unlike generic CRMs, Zeitro is built specifically for the mortgage industry. It integrates document collection, organization, and communication. When a borrower sends you 50 disorganized PDF attachments, Zeitro's AI tools (Document Review) can automatically categorize and verify them. This keeps your pipeline organized and frees you up to sell, rather than acting as a glorified file clerk.

Community Involvement

To be a leader in your market, get offline and get involved. Host "First Time Home Buyer" seminars at your local library or community center. Sponsor a local Little League team. Volunteer at a food bank. When people see you giving back, they trust you. Being a familiar face in the community creates a "halo effect" around your business. You stop being just a salesperson and start being a neighbor who happens to do mortgages.

Be Responsive/Patient/Persistent

The mortgage process is stressful for borrowers. Your responsiveness is their emotional anchor. Reply to texts quickly, even if it's just to say, "I'm in a meeting, I'll call you in an hour." Be patient with their repetitive questions, this is likely the first time they are doing this. And be persistent with leads. A "no" today is often a "yes" in 6 months. Most LOs give up after one call. the money is made on the 5th, 6th, and 7th follow-up.

Be Client-Centric

Always put the borrower's financial health ahead of your commission check. If a refinance doesn't make sense for them because the break-even point is 10 years away, tell them. If they shouldn't stretch their budget for that bigger house, advise them against it. It might hurt to lose a deal today, but that level of honesty builds a reputation that is bulletproof. Clients can smell commission breath. They run to advisors who actually care.

Embrace Continuous Learning

The only constant in this industry is change. Guidelines, rates, and regulations shift weekly. You must be a student of the game. Join professional groups like the Association of Independent Mortgage Experts (AIME) or local broker associations. Seek mentorship from senior LOs who have survived previous market downturns. Attend webinars on new loan products. The more you know, the more scenarios you can save, and the more deals you will close.

Focus on Your Strengths

You don't have to be good at everything. If you are terrified of video but are a networking machine, double down on coffee meetings with realtors. If you are an introvert who loves data, focus on SEO and paid ads. Analyze where your best loans came from in the last 6 months and pour your energy into that channel. Don't try to copy someone else's blueprint if it doesn't fit your personality.

Provide Exceptional Value

Education is your greatest sales tool. A confused borrower doesn't sign papers. Take the time to explain the difference between FHA and Conventional, or why points might be worth paying. Use tools to create "Total Cost Analysis" comparisons. When you offer tailored advice rather than just pushing a product, you commoditize the competition. They might find a lower rate by 0.125%, but they will stick with you because you gave them clarity and peace of mind.

Master Your Craft

Here is the biggest hurdle for rookies: confidence. You get a complex lead, maybe a self-employed borrower with a 650 credit score, and you freeze. You don't know if they qualify, so you say, "I'll check and get back to you." That hesitation kills deals.

This is where Scenario AI is an absolute game-changer. It is an AI tool trained on thousands of guidelines (Fannie Mae, FHA, Non-QM, etc.). Instead of spending hours reading PDF handbooks or waiting for an Account Executive to call you back, you can ask Scenario AI complex questions like, "Can I use 12 months of bank statements for a borrower with a 650 score?" It gives you instant, citation-backed answers. This allows you to speak with expert authority instantly, saving you 20+ hours of research a month and preventing you from losing deals due to uncertainty.

Conclusion

Success in the mortgage industry is not a sprint. It is a marathon. There is no single "magic pill" that will fill your pipeline overnight. Instead, it requires a hybrid approach. You need the human element, building deep, trust-based relationships with partners and past clients. But you also need to embrace the digital shift. By building a strong personal brand on platforms like Bluerate to attract organic leads, and utilizing powerful AI tools like Zeitro and Scenario AI to handle the complexity of guidelines and processing, you can free up your time to focus on what matters most: the people. Stop chasing low-quality leads and start building a business that is professional, efficient, and built to last.