![[Proven] How to Generate Mortgage Leads for Free? 6 Methods](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/69329d01f2ad175a87d0d88b_how-to-generate-mortgage-for-free.png)

Written by

Eric

Share this article

.svg)

Subscribe to updates

Are you tired of burning through your marketing budget on paid ads or buying mortgage leads that just don't convert? You are not alone. Whether you are a loan officer, mortgage broker, wholesaler, or part of a small lending team, the pressure to find quality borrowers without spending a fortune is real. We've all been there, staring at a pipeline that needs filling while trying to keep costs low.

The good news? Some of the highest-converting mortgage leads won't cost you a dime, but just your time and expertise.

In this guide, I'm sharing 6 proven, free methods to generate mortgage leads. These aren't theoretical concepts. They are actionable steps you can start today. By the end of this article, you will have a clear roadmap to build a sustainable flow of clients, from leveraging AI platforms to mastering local networking.

Let's dive into how you can stop chasing leads and start attracting them.

People Also Read:

- 8 Best Mortgage Lead Generation Companies: Don't Miss

- 6 Best Loan Origination Software for LOs/Broker

- 6 Best Mortgage CRM for Brokers, Lenders, MLOs

- Detailed Guide: How to Become a Loan Officer with No Experience?

- 8 Best Mortgage Lead Management Software: Efficiency Matters

Method 1. A Website to Showcase Yourself

In the digital age, if you aren't online, you don't exist. However, I've seen too many loan officers get stuck in the trap of building a custom website. Honestly, it's a headache. It requires expensive hosting, endless maintenance, and worst of all, you have to fight tooth and nail for SEO just to get a single visitor.

There is a smarter, zero-cost alternative.

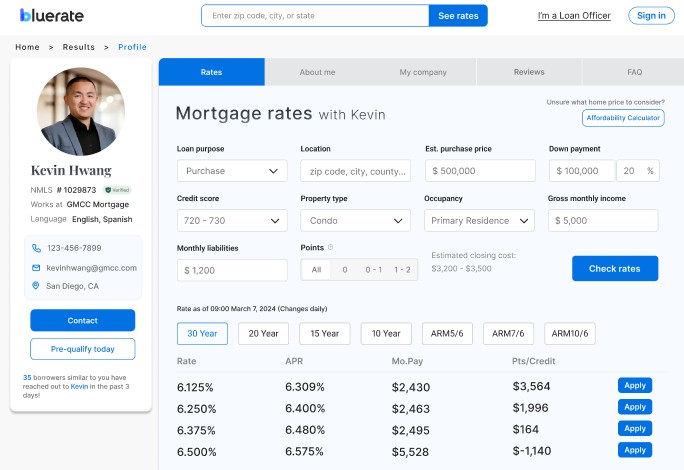

Instead of building a lonely island on the web, I highly recommend creating a free profile on an AI Mortgage Marketplace like Bluerate. Think of this as your professional storefront that comes pre-loaded with traffic. By joining a platform where borrowers are already searching for rates and lenders, you leverage their SEO and marketing efforts for your own benefit.

But Bluerate is more than just a digital business card. It's a powerhouse that integrates directly with the bets Loan Origination System (LOS). Here is why this is a game-changer for your workflow:

- Total Transparency: From the initial Rate Quote to the final Close, everything is tracked in real-time.

- AI Efficiency: The platform utilizes tools like GuidelineGPT and Scenario AI, which can reduce manual guideline research by 100%.

- Speed Wins: With AI empowerment, professionals using Bluerate save 7+ hours per loan and see 20% faster loan closing speeds.

When you streamline the process, borrowers notice. In fact, the platform boasts a 90%+ application completion rate. You aren't just getting a lead. You're getting a borrower who experiences a seamless, transparent journey. That level of service helps you close 30% more loans naturally. Why pay for a website when you can join an ecosystem that actually helps you work?

Method 2. High-Quality Content Marketing

You might be thinking, "I'm a lender, not a writer." But here is the truth: content is the only asset that works for you while you sleep. High-quality content builds trust before you ever pick up the phone.

The secret isn't to write generic updates, and it's to solve specific problems. Focus on educational content that answers the exact questions your clients ask. You can write blog posts like "How to get pre-approved in [Your City]" or "FHA vs. Conventional: What's best for first-time buyers?" Share a monthly local market snapshot. Use data from authoritative sources (like the Fed or local realtor boards) to show trends in your specific county.

Don't let them read and leave. Always include a "Lead Magnet." For example, offer a free eBook like "The Ultimate Closing Cost Guide" in exchange for their email. Place a sticky contact widget on your page so they can book a call instantly.

By consistently posting, say, one solid article every two weeks, you build a library of answers. Over time, this organic traffic becomes your most reliable source of free leads.

Method 3. Leverage the Power of Social Media

Social media is often misunderstood in our industry. It's not about broadcasting your daily rates to an empty room. It's about community and education. Each platform has a specific role in your lead generation strategy.

- LinkedIn: This is your B2B powerhouse. Use it to connect with real estate agents and financial planners. Share case studies of tough deals you saved or professional insights on market shifts.

- Facebook: Focus on hyper-local community groups. Don't spam, and be the helpful expert. When someone asks about housing in a local group, answer their question genuinely without a hard sell.

- Instagram/TikTok YouTube: Video is king here. Create short, captioned videos explaining complex terms (e.g., "What is refinance?"). These "micro-lessons" build massive trust.

Consistency beats virality. Create a simple schedule: FAQs on Tuesday, Client Success Stories on Thursday, and Market Updates on Friday. Always include a clear Call to Action (CTA), such as "Link in bio to book a consultation."Show the human side. Share a photo of a closing day (with client permission) or a "behind-the-scenes" look at your underwriting process. This transparency proves you are a real person helping real families, not just a faceless bank.

Method 4. Word of Mouth with a Great Reputation

A referral is the "Holy Grail" of mortgage leads, because it's free, high-intent, and closes fast. But hoping for referrals isn't a strategy. You need a system to generate them.

Reputation management starts with the client experience. If you use tools like Bluerate mentioned above to speed up closing, your clients are already happier. Capitalize on that joy. Don't know how to get reviews? Check out the ideas below:

- Timing is Key: Ask for the review right when the loan funds. That is the moment of peak happiness.

- Make it Easy: Send a text or email with a direct link to your Google Business Profile. Don't make them search for you.

- The "Referral Tree": Create a simple program. Send handwritten thank-you cards or host small community appreciation events.

Note that you should always check your local regulations and RESPA guidelines regarding referral rewards to ensure you remain compliant. When future prospects search your name and see 50 five-star reviews mentioning your transparency and speed, the sale is already half-made.

Method 5. Network with Local Real Estate Agents

This is the bread and butter for most top producers. Real estate agents control the buyer relationship, and they are desperate for a lender who won't kill their deal.

Don't just email them asking for coffee. You need to offer value first. Target high-volume local realtors and buy-side agents. Here are some partnership ideas:

- Co-Marketing: Offer to create co-branded open house flyers using your marketing templates.

- Education: Host a "Lunch & Learn" specifically on new loan products that help them sell hard-to-move properties like renovation loans or buydowns.

- Open House Support: Offer to sit at their open house to pre-qualify buyers on the spot.

Show them you have a system. "I use an AI-driven process that ensures I never miss a closing date, and I update you every Tuesday on file status." When you prove you can make their life easier and protect their commission, the referrals will flow naturally.

Method 6. Connect with Other Professionals

While everyone chases realtors, many overlook the "Other Professionals" who advise clients on major life financial decisions. These relationships can yield incredibly high-quality borrowers. Here are some professionals you can target:

- CPAs: They know exactly who is buying a home for tax benefits or who has a self-employed income structure that needs a skilled lender.

- Financial Planners: They handle clients looking to refinance for investment purposes or wealth management.

- Divorce Attorneys: A niche, but these clients often need to refinance a spouse off a title or buy a new home quickly.

You can try to send a professional, personalized email. Focus on how you protect your client's interests. For example: "I specialize in helping self-employed clients navigate mortgage approvals without triggering audits. I'd love to be a resource for your tax clients."

Treat these partners with extreme professionalism. A referral from a CPA comes with a high level of trust transferred to you, and don't break it.

Conclusion

Generating free mortgage leads isn't about finding a "magic button". It's about building a presence where trust and value meet. Whether you are leveraging the AI power of Bluerate, creating educational content, or shaking hands with local realtors, the core principle is the same: Give value first.Don't try to do all six methods at once. First of all, you can create your free profile on Bluerate to handle your digital presence and streamline your workflow. Then, pick one distribution channel like Instagram or local Realtor networking, and commit to it for 90 days.

The leads are out there, and they are looking for a professional like you. Start building your pipeline today.