Written by

Eric

Share this article

.svg)

Subscribe to updates

I remember sitting across from my mortgage broker, ready to buy my first home, only to be hit with a question that stalled the whole process: "Are you a W-2 employee or a 1099 worker?" If you've ever applied for a loan, you know the panic. Your income classification dramatically impacts your financial life, especially approval odds for big purchases.

If you're navigating this maze, a quick chat with local loan officers for a free consultation can save you countless headaches. But before you make any career leaps, let's break down exactly what sets the 1099 Form vs W-2 apart and figure out which path actually benefits you most.

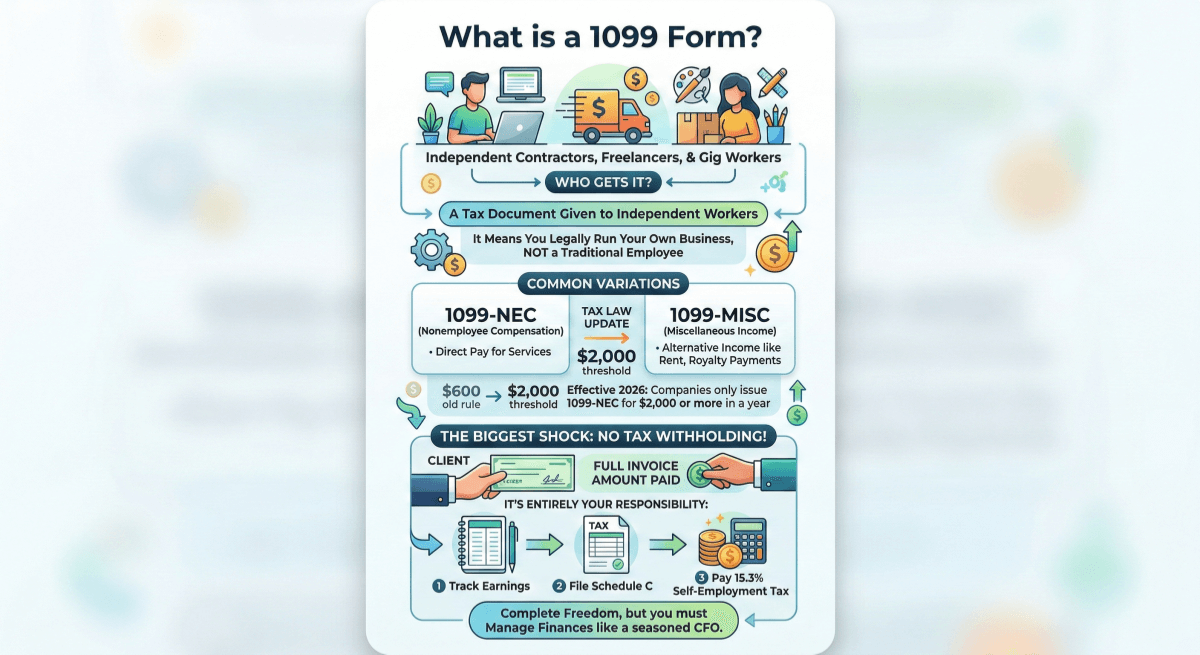

What is a 1099 Form?

First, what is a 1099 form? When I first started freelancing, receiving a 1099 felt like a badge of honor. As per IRS guidelines, a 1099 is the tax document given to Independent Contractors, freelancers, and gig workers. If you get this slip, you are legally running your own business. You are definitely not a traditional employee.

There are a few variations you might encounter. The most common is the 1099-NEC (Nonemployee Compensation), which tracks direct pay for your services. Interestingly, recent tax law changes updated the reporting threshold. Starting in 2026, companies only issue a 1099-NEC if they pay you $2,000 or more in a year, a huge jump from the old $600 rule. Meanwhile, the 1099-MISC handles alternate income like rent or royalty payments.

The biggest shock for newcomers? No tax withholding. Your clients write you a check for the full invoice amount, but they don't hold back a single penny for the government. It becomes entirely your responsibility to track your earnings, file a Schedule C, and pay the 15.3% self-employment tax out of your own pocket. You have complete freedom, but the IRS expects you to manage your finances like a seasoned CFO.

What is a W-2 Form?

On the flip side, getting a W-2 means you belong to the club of Traditional Employees. Employers must furnish W-2 forms to employees by January 31 or next business day if weekend. I spent over a decade working under this classification, and honestly, the sheer convenience is hard to beat.

The defining feature here is automatic Tax Withholding. Every time payday rolls around, your company's HR department automatically slices off your federal and state income taxes, along with your share of FICA taxes (Social Security and Medicare). You never have to worry about accidentally spending money that belongs to Uncle Sam. Even better, your employer is legally required to cover half of those FICA taxes for you.

Receiving a W-2 signifies a direct relationship of control and protection. The company dictates when you clock in, what tools you use, and how tasks are completed. In exchange for surrendering that autonomy, you gain a massive safety net. The organization absorbs the overhead costs, deals with the messy administrative compliance, and ensures your paycheck lands in your bank account consistently, week after week, without fail.

1099 vs W-2: Key Differences Explained

Choosing between these two paths isn't just about how you file taxes in April. It fundamentally changes your daily lifestyle, baseline income, and legal rights. From out-of-pocket expenses to workplace freedom, the daily realities are worlds apart. Let's dive into the core differences to see which option aligns better with your personal goals.

Taxes

As a traditional employee, your tax burden feels relatively light and hands-off. You only pay 7.65% for your half of the FICA taxes, while your employer kindly picks up the remaining 7.65% on your behalf. However, when you operate independently, you bear the full weight of the system. The IRS views you as both the worker and the business owner, meaning you must pay the entire 15.3% self-employment tax yourself. This substantial chunk comes right off the top of your net earnings, long before standard federal and state income taxes even enter the chat. It's a noticeably steep price tag for independence, requiring careful financial planning year-round.Winner for Tax Simplicity: W-2

Benefits

Corporate perks are often the golden handcuffs that keep people happily tied to a steady job. A W-2 status usually unlocks highly subsidized health insurance, employer-matched 401(k) retirement plans, paid time off (PTO), and maybe even vision or dental coverage. These “invisible” financial perks easily add tens of thousands of dollars in value to your total compensation package. Conversely, as a 1099 contractor, you are entirely on your own. If you want to take a week-long vacation, you simply don't generate income for those days. If you need comprehensive medical coverage, you must navigate the open healthcare marketplace and fund the steep monthly premiums entirely out of your own revenue stream.Winner for Comprehensive Benefits: W-2

Control

Nothing beats the feeling of setting your own alarm clock. Contractors operate with ultimate autonomy. You dictate your schedule, choose the specific projects you want to tackle, and decide whether you want to work from a local coffee shop or a beach in Bali. Clients pay for the final result, not your physical presence. Meanwhile, W-2 employees must adhere to the company rulebook. Your manager determines your working hours, your physical location, and exactly how you execute your daily tasks. If you crave creative freedom and despise micromanagement, the contractor route wins by a landslide.Winner for Flexibility and Control: 1099

Expenses

Here is where independent workers finally get to strike back against the tax code. Under current federal tax law (permanent after 2025 changes), W-2 employees cannot deduct unreimbursed business expenses such as laptops, home office, or commuting costs on their federal returns. Contractors, however, can leverage massive write-offs on their returns. You can legally deduct a percentage of your home office rent, internet bills, business mileage, marketing software subscriptions, and specialized equipment. Every legitimate business purchase directly lowers your taxable net income. If you play your cards right and track receipts diligently, these strategic deductions can dramatically offset the pain of that hefty self-employment tax.Winner for Tax Deductions: 1099

Tax Forms

Filing season as a standard employee takes about twenty minutes. You simply import your single wage document into your preferred software, opt for the standard deduction, and you're basically finished. It is remarkably stress-free and straightforward. Conversely, the self-employed face a literal mountain of tax paperwork. You must meticulously compile all your scattered income sources, complete a highly detailed Schedule C to claim those precious business expenses, and calculate your exact self-employment tax liability on Schedule SE. To avoid severe IRS underpayment penalties, you also need to accurately estimate your yearly earnings and submit quarterly tax payments four times a year. The administrative burden is heavy.Winner for Easy Filing: W-2

Legal Protections

I always advise my ambitious friends to deeply consider worst-case scenarios. If a struggling company lays off its staff, W-2 workers can immediately apply for state unemployment benefits to stay afloat. They are also federally guaranteed a minimum wage, time-and-a-half overtime pay for grueling weeks, and workers' compensation if they ever get injured on the job site. Independent contractors are completely excluded from these general labor laws. If a major client suddenly terminates your contract, you cannot collect a dime of unemployment. If a flat-fee project takes twice as long as expected, no legal authority will step in to demand overtime pay. You assume 100% of the operational risk.Winner for Legal Safety: W-2

Work Type

Your current career phase usually dictates the best choice. A W-2 role is absolutely ideal if you highly value predictability, want to steadily climb a structured corporate ladder, or urgently need reliable monthly income to support a growing family without enduring sleepless nights. It provides deeply comforting stability. On the other hand, a 1099 setup is the ultimate financial playground for aggressive side hustlers, specialized project consultants, and globe-trotting digital nomads. It uniquely allows you to scale your income infinitely because your earnings aren't arbitrarily capped by a fixed salary band. If you possess an entrepreneurial spirit and prefer betting on your own skills, independence is the way forward.Winner for Entrepreneurial Growth: 1099

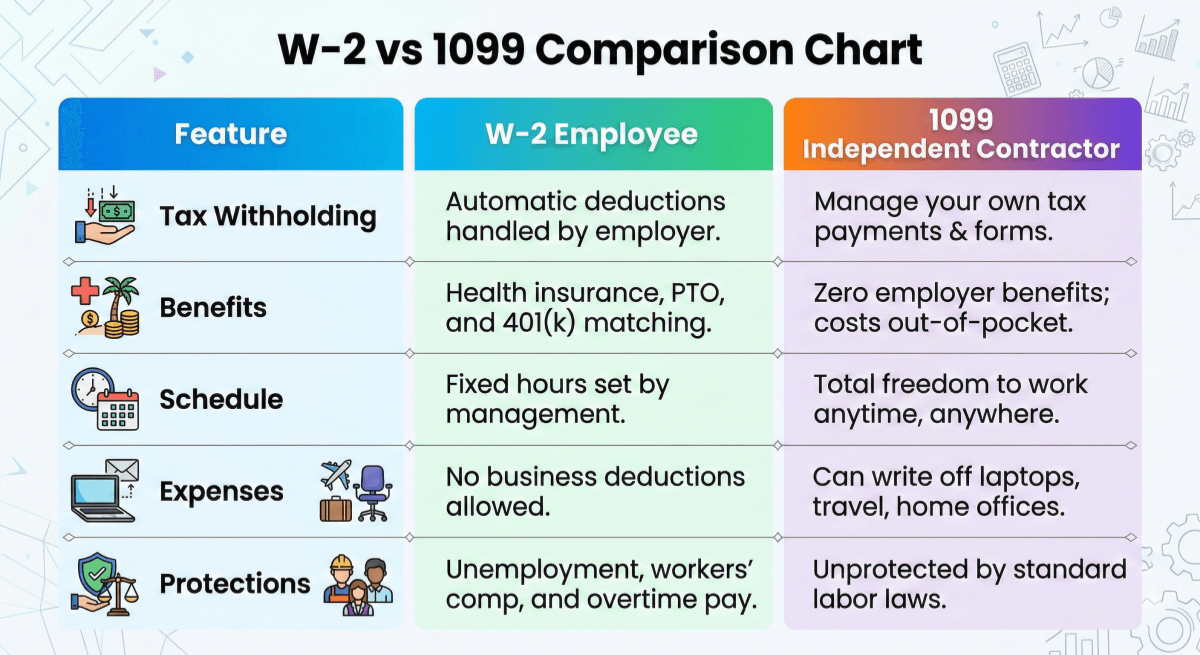

W-2 vs 1099 Comparison Chart

To make things crystal clear, I've put together a quick cheat sheet. Review this table to instantly compare the everyday realities, tax obligations, and legal boundaries of both employment types.

FAQs About 1099 Form vs W-2

Q1. Is it better to be a W-2 employee or 1099?

There is no absolute right answer. If you strongly prioritize peace of mind, reliable corporate benefits, and legal workplace protections, choose the W-2 path. If you desire unlimited earning potential, massive tax write-offs, and the freedom of being your own boss, go 1099.

Q2. Are 1099 taxes higher than W-2?

Typically, yes. As an independent worker, you are forced to pay the full 15.3% self-employment tax burden entirely alone. Traditional employees only pay 7.65% because their company covers the remaining half. However, smart contractors use heavy business deductions to aggressively lower their taxable base.

Q3. Why do companies do 1099 instead of W-2?

Businesses often heavily prefer utilizing contractors to slash their operational overhead costs. Hiring freelancers saves them from paying expensive health insurance premiums, matching payroll taxes, and providing paid leave. It also grants them short-term flexibility to scale their workforce up or down instantly.

Q4. What are the disadvantages of a 1099 job?

The main drawbacks include unpredictable income swings and absolutely zero paid time off. You also carry the heavy administrative burden of calculating quarterly taxes, hunting for private health insurance, and facing a significantly stricter underwriting process when applying for mortgages or personal loans.

Q5. How badly does a 1099 affect my taxes?

If you don't proactively save roughly 25-30% of every single client payment, the impact can be devastating. Missing quarterly estimated deadlines or failing to track your deductible expenses correctly usually leads to massive, unexpected tax bills and harsh IRS penalties come April.

Q6. How much tax do I pay on a 1099?

Beyond your standard federal and state income tax brackets, you owe a flat 15.3% self-employment tax on your net business profit. For example, self-employment tax is 15.3% on 92.35% of net earnings, so for $100,000 net profit, it's approximately $14,130 (half deductible from income tax).

Q7. Can an employer force me to be a 1099?

Absolutely not. The IRS uses extremely strict behavioral and financial control tests to determine proper worker classification. If a company strictly dictates your daily schedule, tools, and methods, you are legally an employee. Intentional misclassification is illegal and usually a tactic to dodge taxes.

Final Word: When to Use Which?

At the end of the day, a W-2 provides genuine safety and security, while a 1099 grants you total freedom and entrepreneurial power. The right choice simply depends on what phase of life you're navigating.

However, I cannot stress this enough: your classification matters immensely when big life events happen. If you are an independent contractor trying to buy a house, lenders won't just look at a simple pay stub. They typically demand two full years of complex tax returns to verify your fluctuating income, making the underwriting process notoriously strict. Want to know exactly how your contractor revenue impacts your home-buying eligibility? I highly recommend checking out the Zeitro to verify 1099 form mortgage guidelines. Getting familiar with the latest lending policies ensures your dream home doesn't slip away over a paperwork technicality.

People Also Read

- Best DSCR Loan Lenders: Which to Choose from?

- What Does a Loan Officer Do? Duties, Pros, Cons, and Outlook

- 8 Best Non-QM Mortgage Lenders: Which to Choose?

- Ultimate Guide: How to Get a 1099 Form Online?