Written by

Eric

Share this article

.svg)

Subscribe to updates

When I talk to hopeful homebuyers today, their biggest worry isn't the monthly mortgage payment—it's scraping together the upfront cash. With home prices still high in 2026, saving tens of thousands of dollars feels nearly impossible.

If you are in this position, down payment assistance (DPA) can help bridge that gap. I wrote this step-by-step guide to show you exactly how to find, qualify for, and secure these funds.

Key Takeaway

- DPA programs can save you thousands of dollars in upfront costs, with some programs offering assistance exceeding $10,000.

- Broad Eligibility: Over 38% of programs accommodate repeat buyers, not just first-time buyers.

- Approved Lenders: You must apply through a mortgage lender approved by the specific DPA program.

- Smarter Search: Chat-based tools like Zeitro Strata AI make matching with active programs simple.

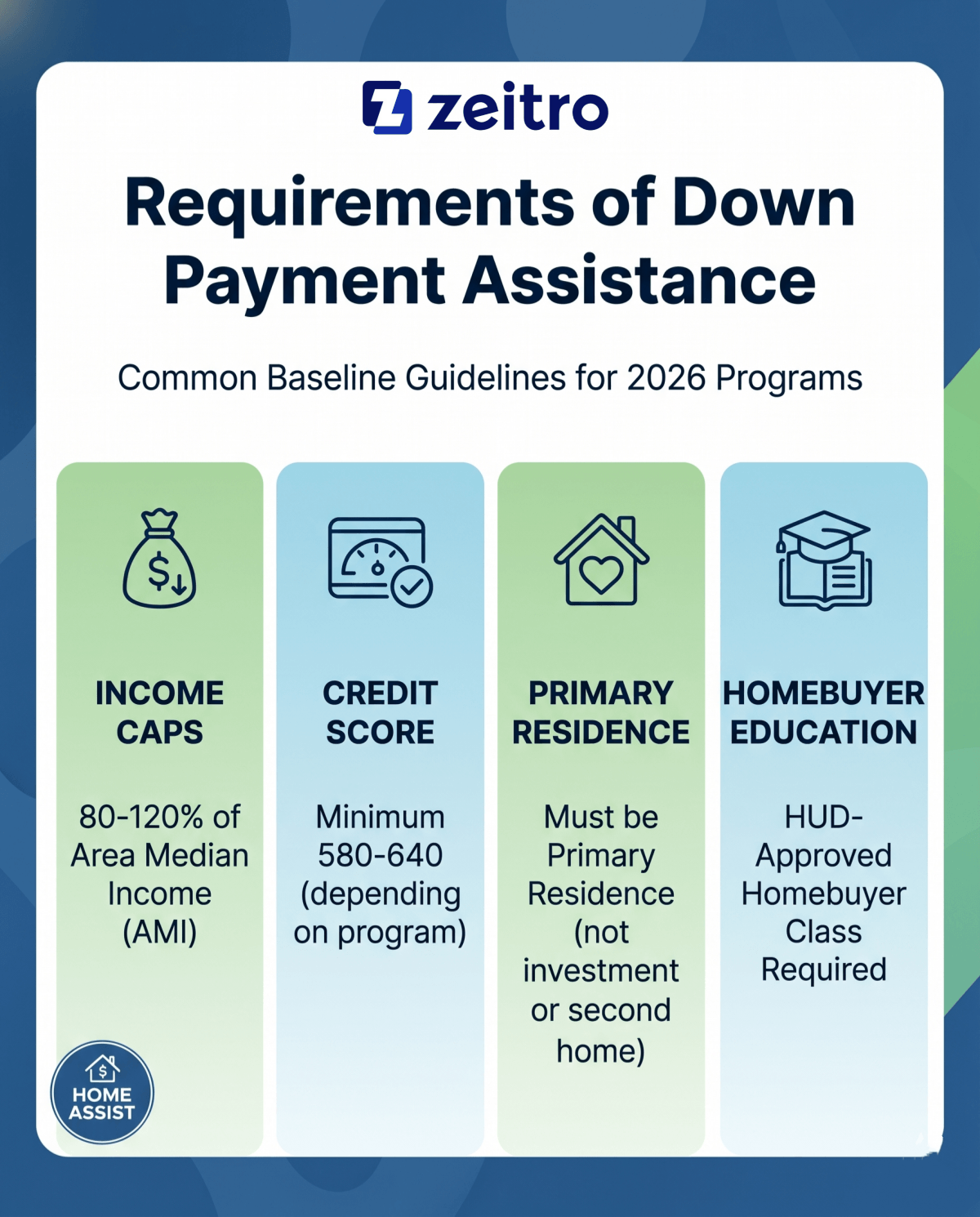

Requirements of Down Payment Assistance

In my experience, many buyers assume they will be rejected before they even look at the guidelines. While each of the 2,679 programs active across the U.S. in 2026 has its own unique rules, most share a few standard baseline requirements:

- Income Caps: Programs usually limit household income to between 80% and 120% of the local Area Median Income (AMI).

- Credit Scores: You generally need a minimum credit score of 580 to 640, depending on the loan program.

- Primary Residence: The home must be your primary residence, not an investment property or second home.

- Homebuyer Education: You will likely need to complete a quick, HUD-approved homebuyer class to receive the funds.

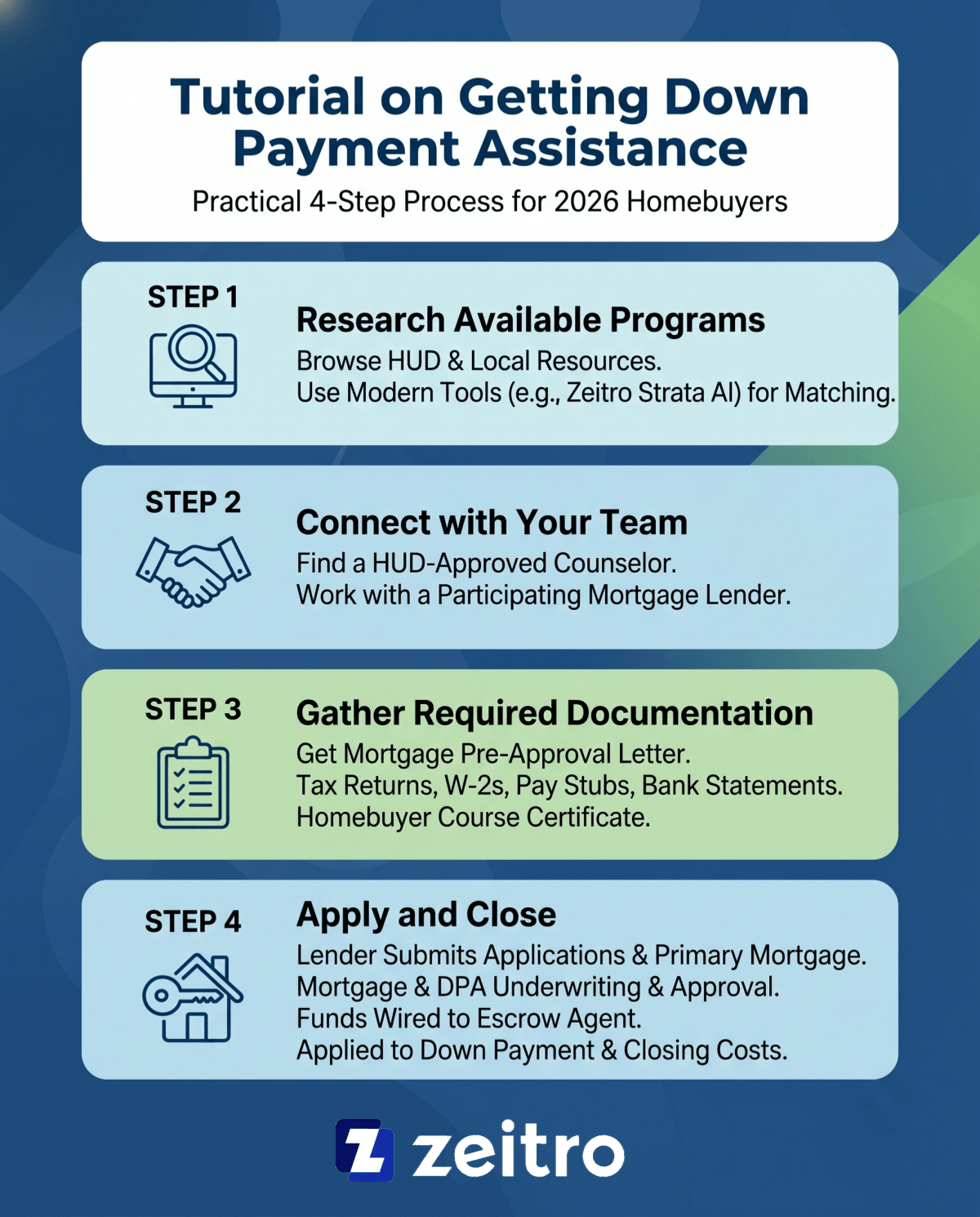

Tutorial on Getting Down Payment Assistance

Securing assistance requires a clear strategy. Navigating the process involves these four practical steps I use with my own clients:

STEP 1. Research Available Programs

With thousands of options nationwide, manual research can easily become overwhelming. To begin, you can browse traditional resources like the Department of Housing and Urban Development (HUD) website or local housing authority pages.

However, I highly recommend using a modern chat tool like Zeitro Strata AI. Instead of digging through endless PDF eligibility charts, you can simply chat with the AI to instantly find and match with the exact programs you qualify for based on your location, income, and profession. It saves hours of tedious searching and ensures you do not miss hidden local grants.

Also Try: Zeitro Down Payment Assistance Program Finder

STEP 2. Connect with Your Team

In most cases, you will need to apply through an approved lender or program partner. It must go through certified partners. First, find a HUD-approved housing counselor who can review your finances and verify your eligibility. Next, and most importantly, work with a participating mortgage lender.

When clients come to me, I check if their loan type aligns with the state or local housing authority offering the grant. If your lender is not approved by the specific program, you cannot use those funds. Always ask lenders upfront which DPA programs they are certified to write.

STEP 3. Gather Required Documentation

Because DPA involves state, local, or federal funding, the paperwork requirements are strict. I advise my clients to gather their documents early to avoid missing out on limited funds. You will need a solid mortgage pre-approval letter from your lender first.

Additionally, prepare your two most recent tax returns, W-2 forms, consecutive pay stubs, and bank statements. Finally, do not forget to sign up for your homebuyer education course. Most programs require a certificate of completion before they will release a single dollar to the closing agent.

STEP 4. Apply and Close

Once your team is assembled and your paperwork is in order, your lender handles the heavy lifting. They will submit your DPA application alongside your primary mortgage application. During the underwriting process, both your mortgage and DPA are reviewed and approved.

On closing day, you do not receive a physical check. Instead, the DPA grant or second mortgage funds are wired directly to the escrow agent. The money is applied straight to your down payment and closing costs, minimizing the cash you must bring to the closing table.

Considerations When Applying for Down Payment Assistance

While DPA is incredibly helpful, you need to understand the fine print before signing. It is not always "free money." Here is what you must watch out for:

- Repayment Clauses: Many programs utilize a second mortgage. While some are forgiven if you stay in the home for five to nine years, others require repayment if you sell or refinance sooner.

- Slightly Higher Rates: Some DPA-linked mortgages carry interest rates a fraction of a percent higher than standard market rates.

- Timeline Adjustments: DPA approvals require extra bureaucratic review, which can add two to three weeks to your closing timeline.

FAQs About Down Payment Assistance

Q1. What is the down payment assistance program income limit?

Limits vary significantly by county, but they are typically set at 80% to 120% of your Area Median Income (AMI). However, roughly 10% of nationwide programs actually have no income restrictions at all, making them accessible to moderate-to-high earners.

Q2. Do I have to pay back the assistance?

It depends on the program type. True grants never require repayment. Forgivable second mortgages are cleared after you live in the home for a set period. Deferred-payment loans, however, must be paid back when you sell, move, or refinance.

Q3. Can I use DPA with an FHA loan?

Yes, absolutely. In fact, programs like the Chenoa Fund are explicitly designed to pair with FHA loans, providing the 3.5% down payment requirement as a second mortgage to help you qualify.

Q4. Does down payment assistance delay the closing process?

Yes, it often does. Because government or nonprofit entities must verify your eligibility and documents, it can extend the closing timeline, sometimes by a few days to several weeks depending on the program. Work with your agent to write a longer closing window into your purchase contract.

Conclusion

Navigating homeownership in today's market is a journey, but you do not have to struggle to save every penny of your down payment alone. With 2,679 programs available in 2026, there is likely a local grant or forgivable loan that fits your financial profile.

To simplify this process, I highly recommend using Zeitro Strata AI. Whether you are a buyer trying to navigate the complex guidelines, or a loan professional looking to provide instant answers to your clients, this chat-based tool makes matching with the right program incredibly fast and straightforward. Start matching today and get one step closer to your new home.

People Also Read

- Guide: Loan Origination Points Explained in Mortgage

- Ultimate Guide: How to Get a 1099 Form Online?

- Fixed vs Adjustable Rate Mortgage: Full Differences to Compare

- Must-Read Tips for Paying Off Mortgage Early

- California Down Payment Assistance: All Programs & Application