Written by

Eric

Share this article

.svg)

Subscribe to updates

Last checked and updated in July, 2026

When I first applied for down payment assistance (DPA), I had no idea my eligibility hinged on a single number: the Area Median Income (AMI). If you are looking to buy a home in 2026, understanding AMI is the key to unlocking thousands in state grants. Fortunately, you don't have to navigate government tables alone. Tools like Zeitro Strata can instantly show your Area Median Income by Zip Code.

Quick answer: Area Median Income, or AMI, is the midpoint income HUD calculates each year for a specific county or metro area. Half the households there earn more, half earn less. Lenders and housing agencies use percentages of that number — usually 80% or 120% — to decide who qualifies for low-down-payment loans and down payment assistance grants.

Key Takeaways

- AMI Defines Eligibility: Area Median Income determines who qualifies for down payment assistance and low-down-payment mortgages.

- Location & Household Size Matter: Limits shift based on where you buy and how many people live with you.

- Easy Lookup: You can bypass manual government charts by using automated tools like Zeitro Strata.

- HUD updates these numbers every spring, and the dollar figures can shift meaningfully from one year to the next — so last year's chart won't always match this year's.

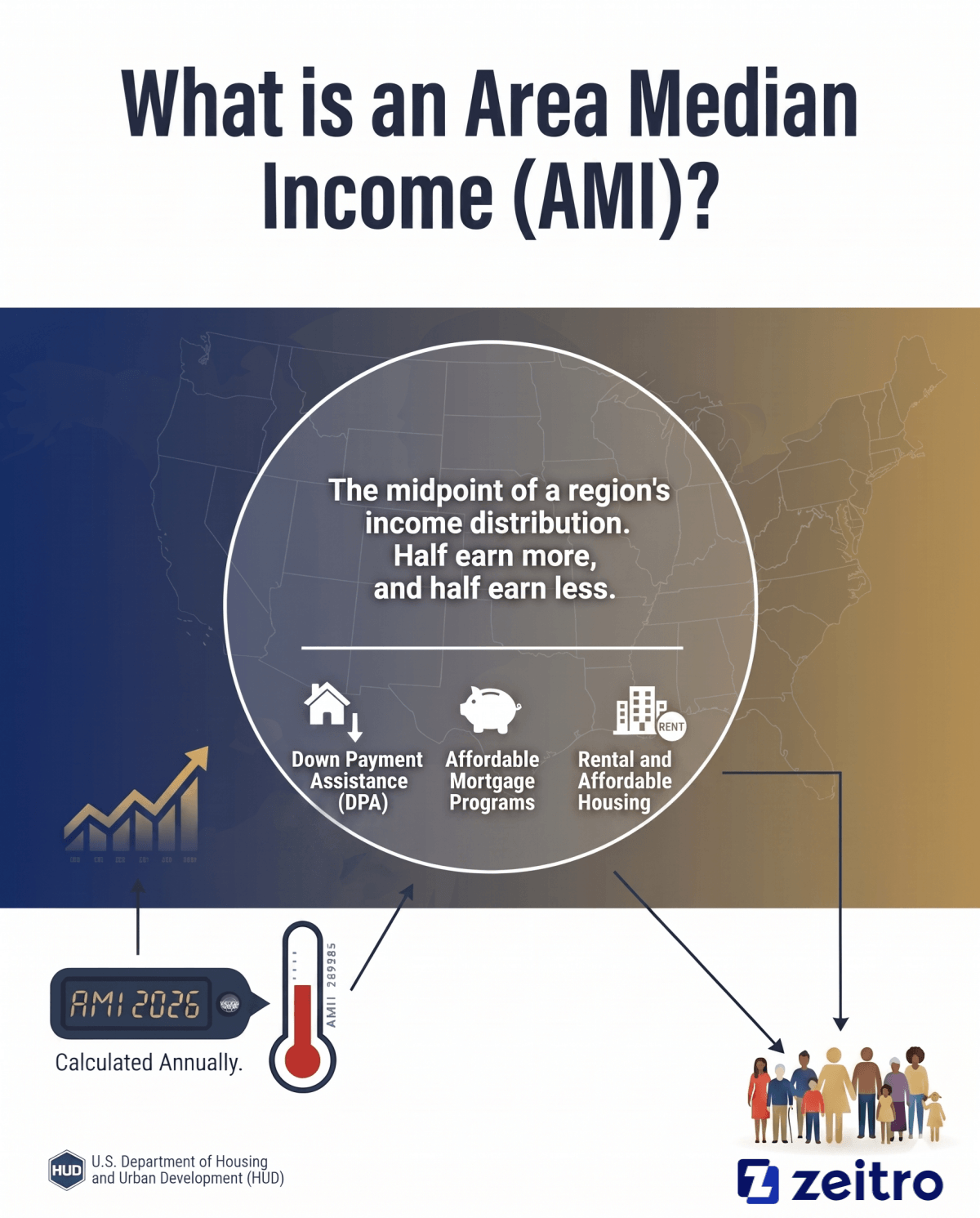

What is an Area Median Income (AMI)?

I like to think of the Area Median Income (AMI) as the economic thermometer of a local housing market. Calculated annually by the U.S. Department of Housing and Urban Development (HUD), the AMI is the midpoint of a region's income distribution—half of households (or families, depending on the dataset) in that area earn more, and half earn less.

✏️ One detail that trips people up: HUD's version of "median income" is technically based on family income, not household income. That's a narrower Census measurement that leaves out single people living alone and unrelated roommates. It's why the AMI figure you see on a HUD chart sometimes looks different from the "median household income" you'd find on a general Census website for the same city — they're measuring slightly different things, even though people use the terms interchangeably.

- Down Payment Assistance (DPA): Most local grants require your income to fall below a certain percentage of the AMI.

- Affordable Mortgage Programs: Loans like Fannie Mae's HomeReady use AMI to set borrower income caps.

- Rental and Affordable Housing: It determines eligibility for subsidized housing and rent-restricted developments.

Also Try: Zeitro DPA Program Finder

Why This Year's Numbers Look a Little Different

Here's something worth knowing if you're comparing this year's chart to last year's: HUD's 2026 income limits didn't come out on schedule. They're normally released around April 1, but a delay in Census Bureau data pushed the release back to May 1, 2026. Nationally, the average increase across HUD areas landed around 3.4%, though the change wasn't even everywhere — some metro areas actually saw their limits dip slightly this year, which hasn't happened much in recent cycles. For 2026, the national four-person median family income benchmark HUD uses as a ceiling is $107,900.

The takeaway: don't assume your city's AMI moved the same direction or by the same amount as the national average. It's worth checking your specific county every year rather than remembering last year's number.

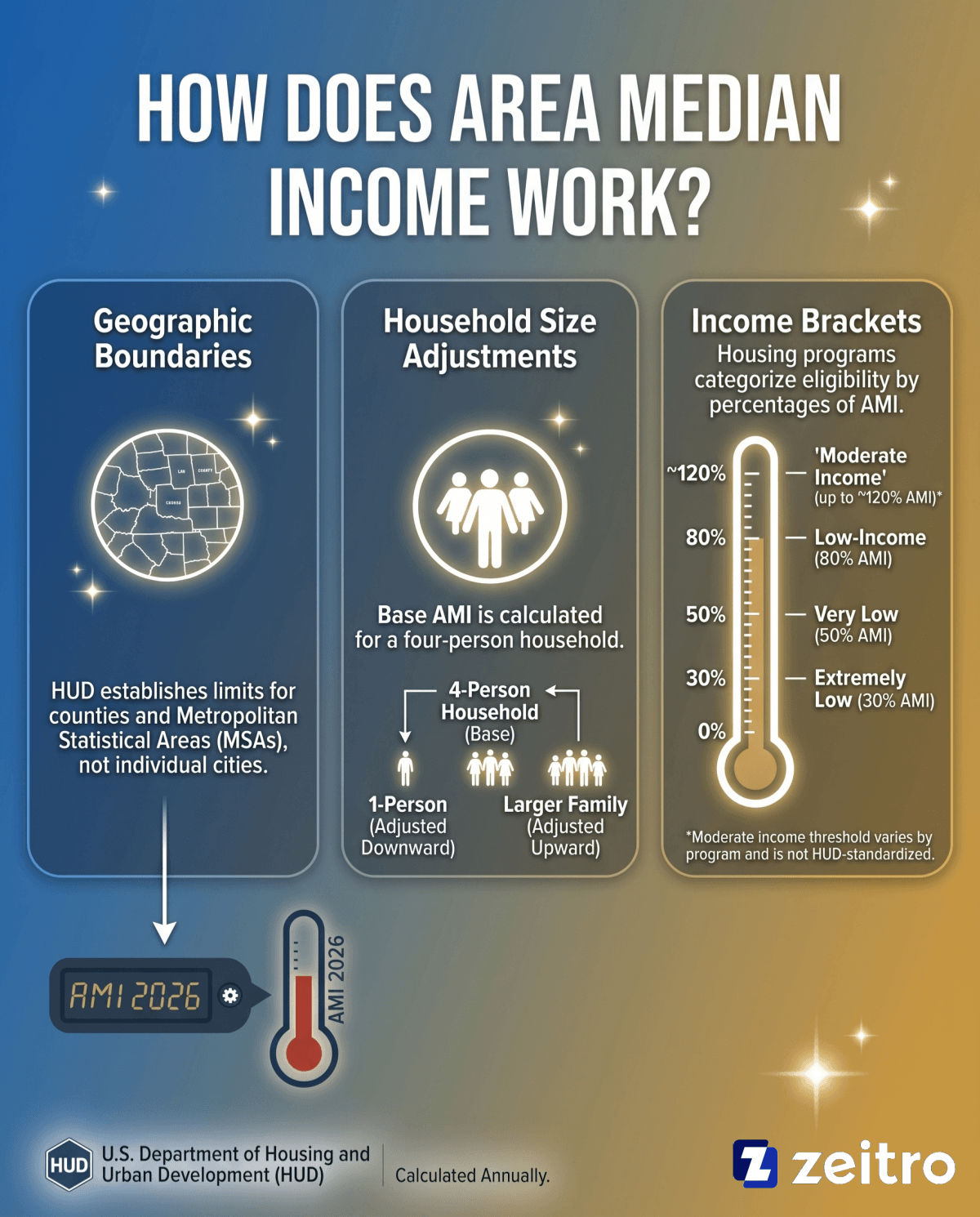

How Does Area Median Income Work?

AMI isn't a static number. In my work advising homebuyers, I always emphasize that your personal AMI limit is highly dynamic, shifting based on several variables. Here is how HUD calculates and applies these limits in practice:

- Geographic Boundaries: HUD establishes limits for counties and Metropolitan Statistical Areas (MSAs) rather than individual cities.

- Household Size Adjustments: The base AMI is calculated for a four-person household. If you live alone, your income limit is adjusted downward. If you have a larger family, it goes up.

- Income Brackets: Housing programs categorize eligibility by percentages of AMI. For example, "Extremely Low" is 30%, "Very Low" is 50%, "Low-Income" is 80%, and some programs define "moderate income" as up to around 120% of AMI, though this threshold varies by program and is not standardized by HUD.

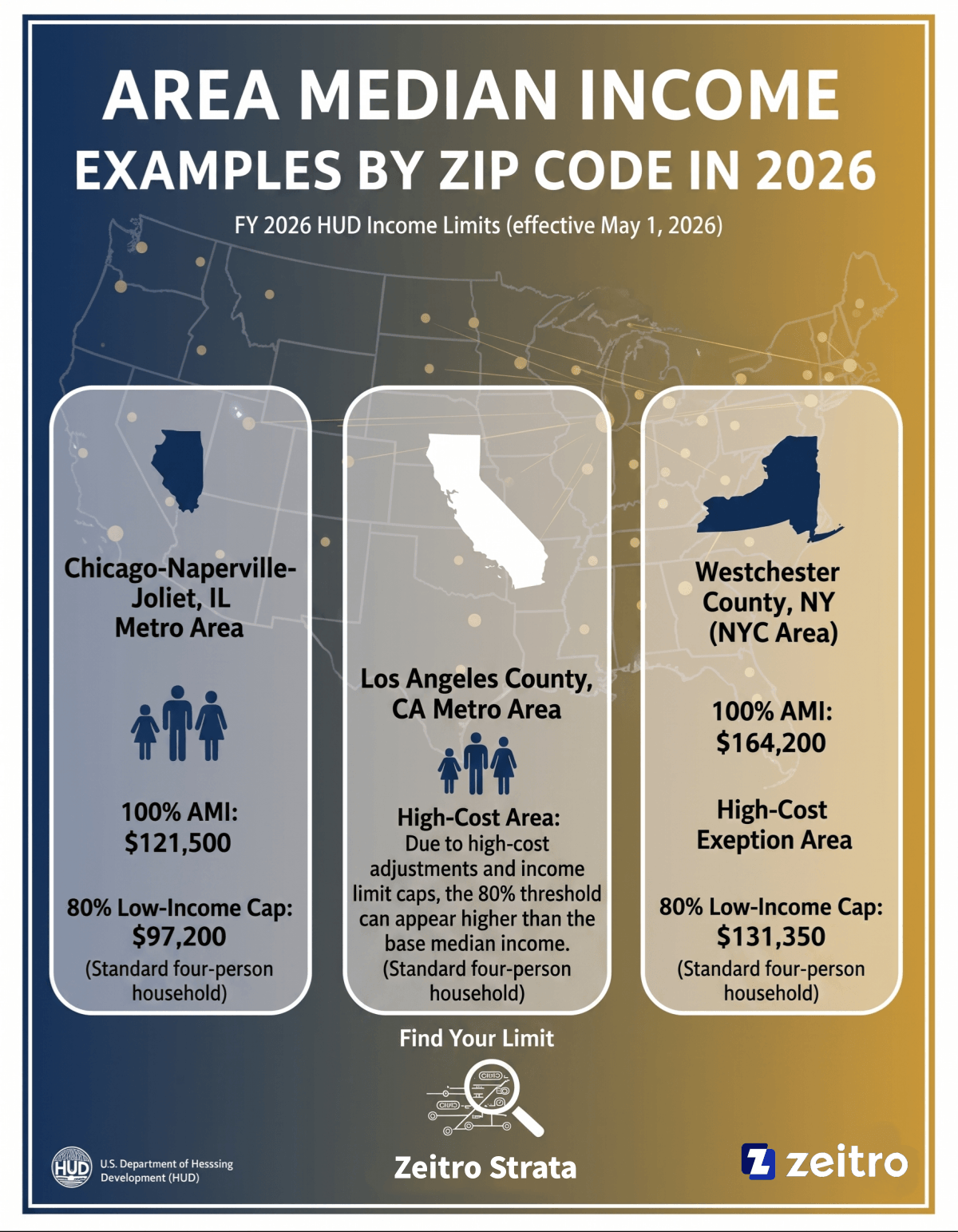

Area Median Income Examples by Zip Code in 2026

While HUD technically publishes AMI limits at the county or metropolitan level, almost every buyer I talk to wants to search by their exact Zip Code. Because zip codes often cross county lines, advanced mortgage tools map these postal codes to the correct government regions.

To give you a clear picture of what these limits look like, here are the official FY 2026 HUD income limits (effective May 1, 2026) for a standard four-person household in several major metropolitan areas:

- Chicago-Naperville-Joliet, IL Metro Area: The 100% AMI is $121,500. To qualify for 80% AMI low-income programs here, a family of four cannot exceed $97,200.

- Los Angeles County, CA Metro Area: Due to high-cost adjustments, due to HUD's high-cost adjustments and income limit caps, the 80% threshold can appear higher than the base median income in some regions.

- Westchester County, NY (NYC Area): Known as a high-cost exception area, the 100% AMI is $164,200, making the 80% low-income cap a generous $131,350.

Because these thresholds change dramatically between neighboring streets, using a tool like Zeitro Strata is essential for finding your exact local limit.

What Role Does AMI Play in a Mortgage?

When you apply for a home loan, lenders compare your qualifying income (based on documents like pay stubs, W-2s, and tax returns) against local AMI thresholds. If your household income is at or below 80% of the AMI, you gain access to massive financial perks.

Conventional programs like Fannie Mae's HomeReady and Freddie Mac's Home Possible are specifically designed for buyers under this threshold, offering down payments as low as 3%. Furthermore, qualifying under the 80% AMI limit often waives certain loan-level pricing adjustments. This may result in better pricing, such as reduced loan-level pricing adjustments, which can lower overall borrowing costs, saving you thousands over the life of your mortgage.

How to Check Your Local AMI?

Finding your specific income limit doesn't have to be a guessing game. You can easily verify your numbers using these four reliable resources:

- HUD Income Limits Database: The ultimate source of truth, offering comprehensive annual spreadsheets organized by county.

- Fannie Mae AMI Lookup Tool: A user-friendly lookup tool where you can input a property address to check eligibility for HomeReady loans.

- Freddie Mac AMI Tool: Similar to Fannie Mae, this tool checks address-specific thresholds for Home Possible qualifying limits.

- Zeitro Strata: The most streamlined option for homebuyers seeking grants. It automatically maps your Zip Code and family size to calculate your exact AMI percentage and matches you with active down payment assistance programs.

Also Read: How to Look Up Area Median Income (AMI): A Guide for Homebuyers

FAQs About Area Median Income

Q1. What are the common AMI percentage thresholds (e.g., 80% vs. 120%)?

The 80% AMI threshold is the standard cap for low-income housing programs and low-down-payment conventional mortgages. In contrast, 120% AMI represents the moderate-income cap, which is frequently used by state and local governments to qualify working-class buyers for down payment grants.

Q2. What is the AMI required for down payment assistance?

There is no single "required" AMI. Instead, each DPA program sets its own ceiling. While many strict government grants require you to earn 80% AMI or less, many local Housing Finance Agencies (HFAs) offer programs that allow buyers to earn up to 120% or even 140% of the AMI.

Q3. Does household size affect my AMI limit?

Absolutely. HUD scales income limits based on the number of people living in your home. A single buyer will face a much lower income ceiling than a family of four in the same county. It is vital to include all household members when calculating your limit.

Q4. How often does HUD update Area Median Income limits?

HUD updates these limits annually, typically releasing the new figures in April or May. For 2026, the updated thresholds took effect on May 1. These annual adjustments account for regional inflation and shifts in local wage data.

Q5. What is the difference between Median Household Income and AMI?

While median household income is a raw census stat reflecting middle-of-the-pack earnings, HUD's AMI is a regulatory metric adjusted for local housing costs and family size. AMI is a key eligibility benchmark for many housing assistance and affordable lending programs, though not all mortgage products rely on it.

Q6. What do 30% and 50% AMI mean?

These are lower-income tiers used mainly for rental assistance and subsidized housing rather than conventional mortgages. HUD defines 30% AMI as "extremely low income" and 50% AMI as "very low income." You'll mostly encounter these two brackets if you're applying for public housing or Section 8, not a standard home purchase.

Q7. What counts as low income for a single person in my area?

Since HUD scales limits by household size, a one-person household typically qualifies at around 70% of the four-person 100% AMI figure for that county. The exact dollar amount varies significantly by location, so it's worth checking your specific county rather than assuming a national figure applies.

Conclusion

Navigating the homebuying process can feel overwhelming, but understanding where your income stands relative to the Area Median Income is a powerful first step. Knowing your local AMI doesn't just tell you if you qualify for a home loan.

It can open the door to vital down payment assistance programs that make homeownership affordable. Rather than drowning in confusing government databases and manually adjusting for your family size, I highly recommend letting technology do the heavy lifting. You can use Zeitro Strata to instantly check your local 2026 AMI limits by Zip Code and see exactly which grants you are eligible for today.