Written by

Eric

Share this article

.svg)

Subscribe to updates

When I sit down with a first-time buyer, "Area Median Income" is one of the first terms that trips them up. It sounds like a Census Bureau statistic, but for mortgage purposes, it's actually the gatekeeper number behind some of the best low-down-payment programs on the market.

If your household qualifies under the local AMI threshold, you could unlock a 3% down payment through Fannie Mae's HomeReady program, or similar savings through Freddie Mac's Home Possible. In this guide, I'll walk through exactly how I help my own clients find their correct AMI figure, which tools are worth your time, and a few pitfalls that catch even experienced buyers off guard.

Key Takeaways

- AMI matters: Your local Area Median Income is used to determine income eligibility for affordable conventional loan programs that may offer down payments as low as 3%.

- Multiple tools exist: You can search via official GSE portals, HUD raw datasets, or an AI-powered mortgage assistant like Zeitro Strata.

- Accuracy is key: Always confirm your exact household size, and use a full street address rather than just a ZIP code, since AMI boundaries rarely line up neatly with ZIP code borders.

What is the Area Median Income (AMI)?

Area Median Income (AMI) is the midpoint income for a specific geographic area defined by HUD, typically a metropolitan area (MSA) or a non-metropolitan county. Calculated annually by the U.S. Department of Housing and Urban Development (HUD), it means half of the households in that region earn more than this figure, and half earn less.

Mortgage institutions use AMI to ensure that subsidized housing benefits actually reach low-to-moderate-income families. For instance, conventional programs like HomeReady cap household income at 80% of the local AMI. Because these figures adjust based on your family size and geographic location, they are highly localized. What counts as "middle income" in a rural town differs greatly from a major city, making precise lookup crucial.

[4 Ways] How to Look up Area Median Income for Your Area

Fortunately, you do not have to calculate these complex statistics yourself. I have gathered the four best methods, ranging from official federal lookup tools to advanced AI assistants, to find your exact local AMI in seconds.

Method 1: Fannie Mae Area Median Income Lookup Tool

If you are eyeing Fannie Mae's HomeReady program, the official Fannie Mae Area Median Income Lookup Tool is your starting point. Users simply type in a property's street address or ZIP code to receive instant, localized data. Its biggest advantage is absolute accuracy for conventional lending underwriting. It tells you exactly if a specific address qualifies for the 80% AMI cap.

However, the limitation of this tool is its single-program focus. It won't help you compare guidelines across other federal programs or alternative loan portfolios, requiring you to manually check other platforms.

Method 2: Freddie Mac Area Median Income and Property Eligibility Tool

Alternatively, if your loan officer is routing your application through Freddie Mac, you should use the Freddie Mac Area Median Income and Property Eligibility Tool. It operates similarly to Fannie Mae's portal, utilizing a clean, map-based interface to deliver results. The primary benefit of this tool is its instant determination of eligibility for Freddie's Home Possible program.

Unfortunately, it shares the same drawback as its competitor: it operates in a silo. You cannot use it to cross-reference non-conforming or state-specific assistance guidelines, meaning you'll need to run separate searches for non-Freddie programs.

Method 3: Dataset HUD Income Limits

For those who want to see the foundational raw data, the official HUD Income Limits Dataset is the ultimate source. Because both Fannie Mae and Freddie Mac base their tools on HUD-published income limits, accessing this database directly offers maximum transparency. Its main strength is that it breaks down income brackets (low, very low, and extremely low) by exact household size, from one to eight people.

However, the downside is its steep learning curve. Navigating the manual state-and-county drop-downs can feel overwhelming if you are just looking for a quick, straightforward household limit.

Method 4: Zeitro Strata - AI Chat to Check AMI

If you are tired of juggling multiple official tabs, a highly efficient modern alternative is Zeitro Strata. This AI-powered mortgage assistant acts as a digital guideline analyst, allowing you to ask specific questions about AMI and mortgage rules in a natural chat interface. Instead of manually digging through PDFs, you can ask direct or vague questions and get exact, cited answers in seconds.

Also Try: Zeitro DPA Program Finder

Here is what makes this tool a standout for both buyers and loan officers:

- DeepSearch Capabilities: It cross-checks over 1,000 guidelines from 100+ mainstream investors (including major names like AAA Lending, AD Mortgage, and CMG Financial), instantly slashing search times from 30 minutes to seconds.

- Diverse Guidelines: It covers Conventional, FHA, VA, and complex Non-QM programs (like DSCR, Bank Statement, and ITIN).

- 100% Citation-Backed: Every answer features clickable sources to eliminate AI hallucinations, boosting your underwriting confidence.

- Smart Calculation: You can upload financial documents to calculate your qualifying income and instantly match with local down payment assistance programs.

Please note: The daily free tier grants you 10 queries. While there is an 'Explain' feature to clarify complex clauses, it submits a new search behind the scenes, which counts against your daily query limit.

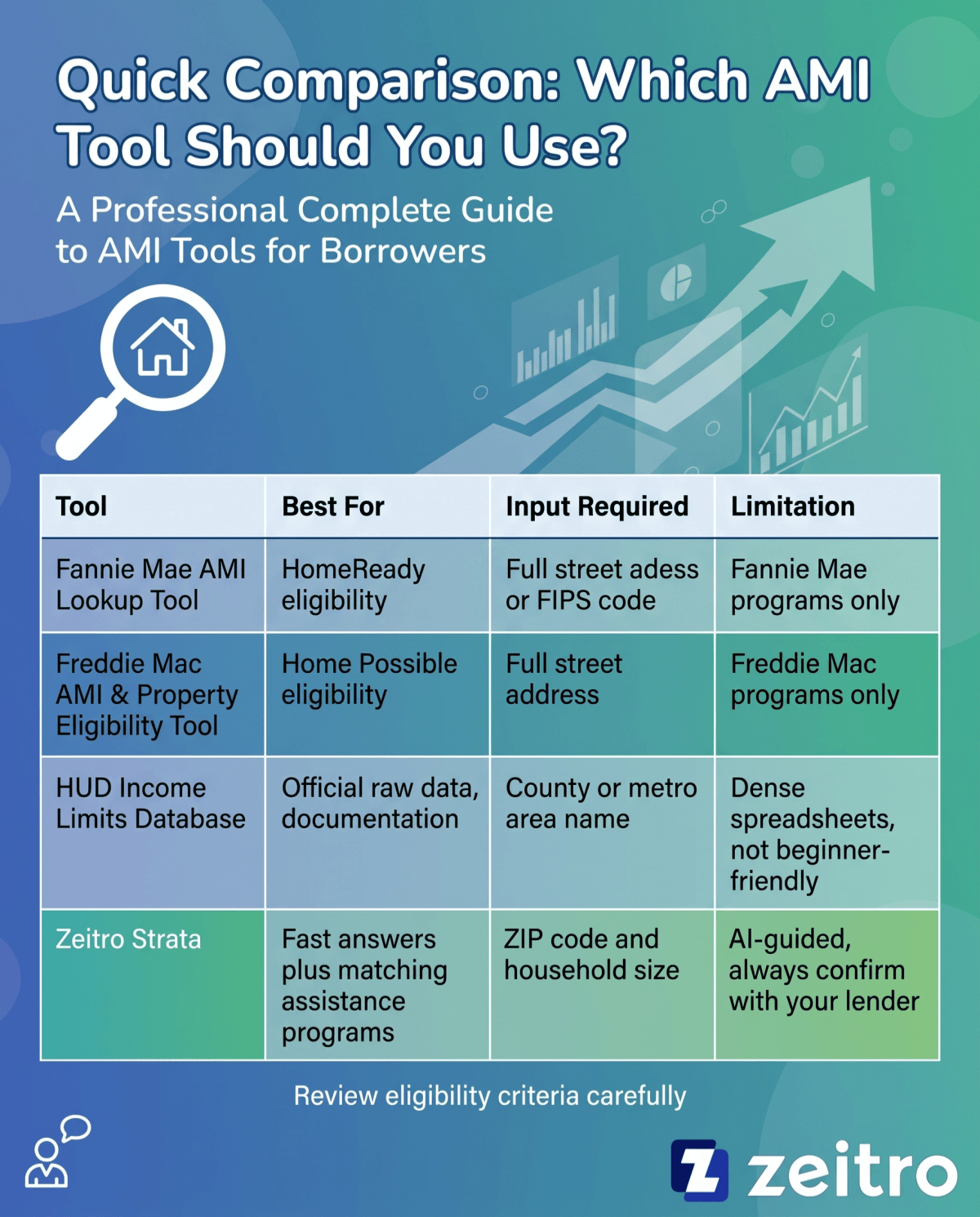

Quick Comparison: Which AMI Tool Should You Use?

Suggestions: Which Method to Choose?

Choosing the right search method depends on your current stage in the buying process. Based on my experience, I suggest matching your goals to these specific avenues:

- Fannie Mae or Freddie Mac Tools: Best if your loan officer has already locked you into a HomeReady or Home Possible application and you just need to verify address eligibility.

- HUD Dataset: Best if you are a real estate researcher or need a complete family-size matrix for public housing audits.

- Zeitro Strata: Best if you are shopping around, exploring Non-QM options, comparing multiple lenders, or need to calculate exact household eligibility across multiple local assistance programs instantly.

Why "AMI by ZIP Code" Isn't Always Accurate

Here's something that catches a lot of buyers off guard: ZIP codes and AMI boundaries don't actually line up. A ZIP code is a mail-routing area defined by USPS, while HUD sets income limits by county, metro area, or census tract. It's entirely possible for one ZIP code to stretch across two different counties, each with its own AMI figure.

I've seen buyers pull a number from a general income-by-ZIP-code website, assume it applies to their exact address, and then get a different figure back from their lender's underwriting system. To avoid that mismatch, always run your full street address through the Fannie Mae or Freddie Mac tool rather than relying on a ZIP-code-level estimate. If you only have a general area in mind and haven't picked a specific address yet, a ZIP-level search is a fine starting point, just treat it as a ballpark rather than a final answer.

A Real-World Example: New York City

According to HUD's 2026 data, the Area Median Income for the New York City region sits at $152,700 for a three-person household, which represents the 100% AMI baseline. For a single-person household, that 100% figure drops to $118,800. These numbers apply across all five boroughs and the surrounding HUD-designated metro area.

For HomeReady specifically, the qualifying income cap sits at 80% of that local AMI. Since 2019, this 80% cap applies to every property, including homes located in what used to be called "low-income census tracts." Earlier HomeReady guidelines allowed an exception in those tracts with no income cap at all, but that carve-out was removed years ago. So regardless of where the property sits, if your qualifying income lands above the 80% threshold, you'll need to look at standard conventional financing instead of HomeReady's discounted terms.

How Do You Determine Your Household Income Relative to the AMI?

To check where you stand against the AMI, you should estimate your total household income as defined by program guidelines, which may differ from the underwriting "qualifying income" used for loan approval. Lenders evaluate specific parameters when underwriting your application. I always advise clients to gather their W-2s, paystubs, or tax schedules first.

For self-employed individuals, qualifying income is based on net business income after write-offs, not gross revenue. Additionally, bonus or commission pay typically requires a two-year track record of stability to be counted. Once calculated, divide your total qualifying income by the area's 100% AMI. This percentage determines your eligibility for specific affordable lending programs, helping you save money.

FAQs About Area Median Income Lookup

Q1. How to calculate your AMI level?

To calculate your AMI percentage, divide your annual qualifying household income by the local 100% AMI for your household size. For instance, if your underwriting qualifying income is $60,000 and the HUD 100% AMI limit for a single-person household in your county is $80,000, your level is 75% ($60,000 / $80,000), which successfully falls under the standard 80% HomeReady threshold.

Q2. What is the AMI for NYC?

According to HUD's official data, the 2026 Area Median Income (AMI) for the New York City region is set at $152,700 for a three-person family (which represents the 100% AMI baseline). For a single-person household, the 100% AMI limit is $118,800. These limits apply across all five boroughs and adjacent HUD-designated metropolitan areas to determine affordable housing and mortgage assistance eligibility.

Q3. What are the HomeReady income limits?

For Fannie Mae's HomeReady mortgage program, the household income limit is capped at 80% of the local AMI. This cap generally applies nationwide. However, in designated low-income census tracts, the income limit restriction may be waived. If your qualifying income exceeds this 80% limit in your specific census tract, you will not qualify for the program's discounted rates and will need to look at standard conventional options.

Q4. Why does Area Median Income (AMI) matter for mortgage approval?

AMI acts as a baseline benchmark for affordable lending programs. Government-sponsored enterprises (GSEs) and local agencies use it to target financial assistance to buyers who need it most. Staying under designated AMI limits unlocks significant perks, including lower interest rates, reduced down payment requirements down to 3%, and capped mortgage insurance costs, making homeownership far more accessible.

Q5. How often do HUD and GSEs update AMI limits?

HUD releases updated income limits annually, typically in April or May. Following this, Fannie Mae and Freddie Mac usually implement these updated AMI limits into their automated underwriting systems and eligibility tools by early June. For example, HUD's 2026 limits took effect on May 1, 2026, and Freddie Mac implemented them into its systems on June 13, 2026.

Q6. Can I still qualify for a conventional loan if my income exceeds the 80% AMI limit?

Yes, absolutely. Exceeding 80% AMI simply means you do not qualify for targeted low-income conventional programs like HomeReady or Home Possible. You can still apply for standard conventional loans, which do not impose any household income limits, or explore FHA alternatives. However, you will be subject to standard risk-based interest rates and private mortgage insurance pricing.

Q7. Is AMI based on gross or net income?

Gross income. Lenders compare your pre-tax qualifying income against the local AMI threshold, not your after-tax take-home pay.

Q8. Do Fannie Mae and Freddie Mac update these limits at the same time?

Not exactly. HUD typically releases updated income limits annually each spring. Fannie Mae and Freddie Mac then roll those updated figures into their own underwriting systems and lookup tools within a few weeks afterward, so there's occasionally a short lag between HUD's release and the GSEs' updated tools.

Q9. What happens if my income is above 80% of the AMI?

You simply won't qualify for targeted affordable programs like HomeReady or Home Possible. Standard conventional loans remain available with no household income cap, though you'll be subject to regular risk-based pricing and mortgage insurance rates rather than the discounted terms these programs offer.

Conclusion

Finding your local Area Median Income is a vital step toward securing an affordable mortgage. Whether you are using traditional HUD databases or automated GSE tools, keeping an eye on your local county's threshold ensures you don't leave valuable mortgage discounts on the table.

In my daily workflow, I find that relying solely on manual lookup portals often leads to overlooked options, especially if you qualify for state programs. If you want to simplify this process, I highly recommend checking out Zeitro Strata. It combines multi-investor guidelines with real-time AMI checks, helping you navigate your financing path with absolute confidence, clarity, and ease.