Written by

Eric

Share this article

.svg)

Subscribe to updates

Last checked and updated on July, 2026.

As loan professionals, we see homebuyers struggle with income math every day. Nailing this calculation accurately is the critical first step to getting approved.

While manual math can lead to stressful errors, we highly recommend Zeitro Strata. It safely allows you to verify income requirements and simply upload your documents to auto-calculate everything, making the entire approval process incredibly easy and secure.

Key Takeaways

- Lenders qualify you on gross income — your pay before taxes — not your take-home amount.

- The one exception: self-employed borrowers are qualified on net profit after business write-offs.

- Calculation methods differ by pay type: salaried, hourly, commission, or self-employed.

- Bonuses and overtime are usually averaged over 24 months, though some programs accept a shorter history if the income is stable.

- Non-taxable income, like Social Security, can often be "grossed up" to count for more than the check you actually receive.

- Have your pay stubs and tax documents ready early — it's the single biggest thing that speeds up underwriting.

How Gross Income is Used in a Mortgage?

Why do lenders care so much about your top-line number? Put simply, your gross earnings—the money you make before taxes and health insurance deductions—serve as the absolute foundation of your loan application.

We use it to evaluate your repayment ability and establish your Debt-to-Income (DTI) ratio. This ratio tells our underwriting team if you can comfortably afford a new housing payment alongside your current credit cards and car loans. Ultimately, your pre-tax pay is the primary metric for meeting specific mortgage income requirements and determining the maximum loan amount you qualify for.

Also Read: Gross vs. Net Income for a Mortgage: What Lenders Use & Why

Also Try: Zeitro Mortgage Employment Income Calculator for Loan Pros

Gross or Net? Clearing Up the Confusion

This is the question we field most often, and it's worth answering plainly: mortgage lenders qualify almost every borrower on gross income, not net.

The logic makes sense once you see it from an underwriter's chair. Net pay varies too much — one person's 401(k) contribution or extra tax withholding shouldn't make them look poorer on paper than a neighbor earning the same salary. Gross income levels the playing field, so DTI limits mean the same thing for everyone.

The one carve-out is self-employed borrowers, where we work from the net profit shown on filed tax returns, not gross business revenue. We'll walk through why below.

Most conventional loans cap back-end DTI around 43–45%, and some stretch to 50% with strong credit, reserves, or automated underwriting approval. FHA loans typically work with a 43% back-end ratio and a 31% front-end guideline, though compensating factors can push both higher. For a full breakdown by loan type, see our Max DTI for Mortgage guide.

How to Calculate Gross Monthly Income by Type?

Lenders don't treat every paycheck the same way. Here's how the math changes based on how you're paid.

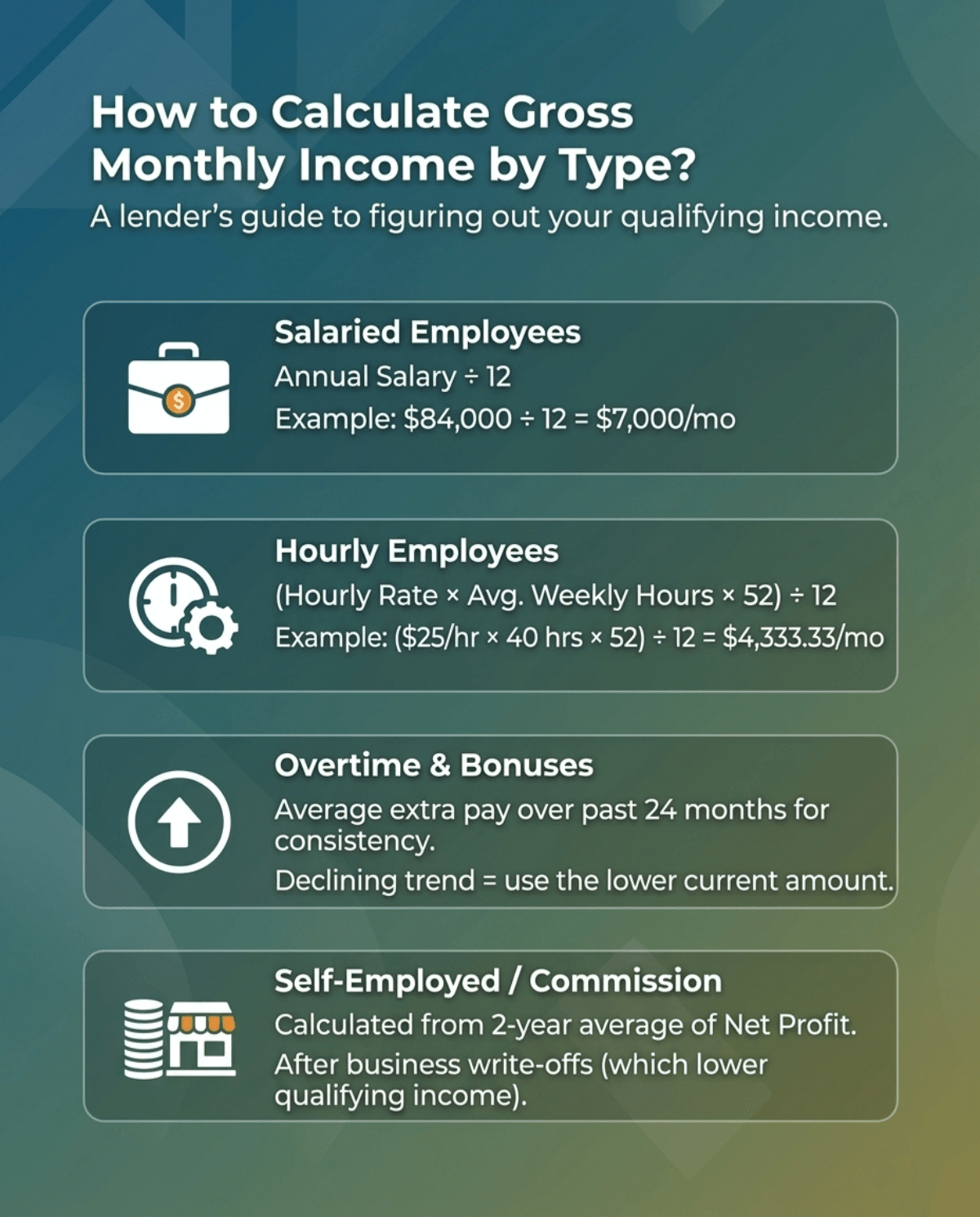

- Salaried Employees: The simplest case when you're figuring out how to calculate employment income. Take your annual salary and divide by 12. A $84,000 salary works out to $7,000 a month ($84,000 ÷ 12).

- Hourly Employees: Don't just multiply a strong week by four — your pay period changes the formula. For a weekly paycheck, multiply your hourly rate by average weekly hours, then by 52, then divide by 12 ($25 × 40 × 52 ÷ 12 = $4,333.33 a month). For biweekly pay (26 checks a year), multiply by 26 instead of 52 before dividing by 12. For semimonthly pay — two fixed paychecks a month, 24 a year — just multiply your per-paycheck gross by 2. Mixing these up is one of the most common mistakes we see borrowers make on their own.

- Overtime and Bonuses: We look for a consistent pattern, generally averaged over the past 24 months. If your overtime has been trending down lately, guidelines require us to use the lower, current figure instead of the historical average — better a realistic number now than a surprise at closing.

- Self-Employed, 1099, and K-1 Income: We don't count your gross business revenue or bank deposits. Qualifying income comes from your net profit after write-offs, typically calculated using Fannie Mae's Cash Flow Analysis worksheet (Form 1084) or an equivalent method. From there, we add back non-cash expenses like depreciation and amortization, since they lower your taxable income without actually reducing your cash flow, then subtract any one-time gains that won't repeat. Partnership or S-corp income from a Schedule K-1 counts too, as long as you can document your ownership share, and each business you own gets evaluated on its own. If you run a business or freelance full-time, how to calculate self-employed income is worth reading closely, since heavy deductions that help at tax time can quietly shrink your qualifying income.

- Gig and Contract Work: The same 1099 logic applies to rideshare drivers, delivery contractors, and freelancers. Lenders look at your net Schedule C profit over the past two years, not your total earnings before mileage and expense deductions.

Non-Taxable Income: How Grossing Up Works

Some income, like Social Security, disability benefits, or child support, isn't taxed. Because a non-taxable dollar goes further than a taxed one, lenders are allowed to "gross it up," counting it as slightly more than the amount you actually receive.

FHA loans typically allow a flat 15% gross-up on Social Security income with no extra paperwork. Conventional, VA, and USDA loans often allow up to 25%, provided you can document that the income isn't taxed. So $2,000 a month in Social Security could count as $2,300 to $2,500 in qualifying income, depending on the loan program. This is one of the most overlooked ways retirees and disabled borrowers boost their buying power, and it's worth raising with your loan officer even if no one mentions it upfront.

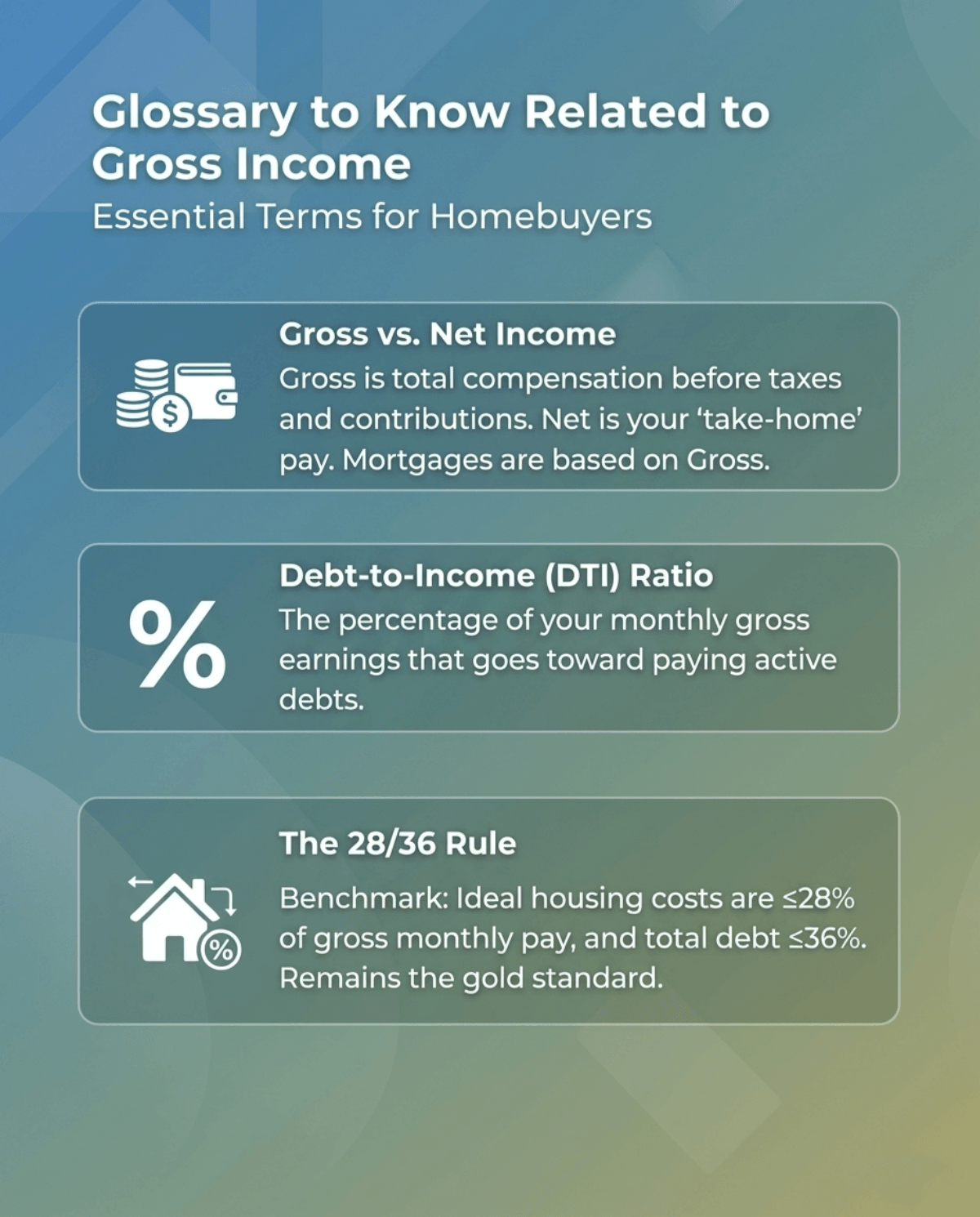

Glossary to Know Related to Gross Income

The mortgage world runs on its own vocabulary. Here are the terms we use daily on the processing floor:

- Gross Income: Your total pay before taxes, insurance, or retirement contributions are taken out. This is the figure lenders use, whether you're salaried, hourly, or paid by commission.

- Gross vs. Net Income: Gross is everything before deductions; net is your take-home pay. Mortgages are almost always based on the gross figure.

- Debt-to-Income (DTI) Ratio: The share of your gross monthly income that goes toward paying debts, including your new housing payment.

- The 28/36 Rule: A long-standing underwriting benchmark. Ideally, housing costs stay under 28% of gross monthly pay, and total debt stays under 36%. If you're wondering what percentage of income should go to a mortgage, this rule is still the standard starting point, even though many loan programs now approve higher ratios.

Documents Needed for Mortgage Verification

Whenever clients ask me how to speed up their clear-to-close, my answer is always the same: have your paperwork ready upfront. Providing clean, complete documentation prevents your file from sitting in limbo.

Here is a quick checklist of what you need to gather:

- W-2 Forms: The last two years for standard employees.

- 1099 Forms: The last two years if you are a freelancer or contractor.

- Recent Pay Stubs: Usually covering your most recent 30-day pay period.

- Tax Returns (1040s): Your complete personal and business returns for the past two years (especially vital for self-employed borrowers).

- Bank Statements: The last 60 days of active accounts to verify your cash reserves.

FAQs About Calculating Gross Income in Mortgage

Q1. Do mortgage lenders look at gross or net income?

We primarily use your gross earnings—the amount before taxes. The major exception is for self-employed borrowers, where we must evaluate the net profit shown on your filed federal tax returns.

Q2. Can I include overtime or bonuses in my gross income?

Yes, but it must be reliable. We require a consistent two-year history of receiving overtime or bonuses. If it is a one-time payout, we generally cannot count it toward your qualifying income.

Q3. How does rental income affect my gross monthly income?

For many loan programs, lenders count about 75% of gross rental income to account for vacancy, maintenance, and management expenses. The remaining 25% is automatically subtracted to account for potential vacancies and routine property maintenance.

Q4. At what income level do I lose the mortgage interest deduction?

Tax laws update frequently, and limitations are often tied to your total loan size. However, you can check specific IRS guidelines to see the exact income level you lose the mortgage interest deduction based on your tax filing status.

Q5. What if my income is variable or commission-based?

For variable income, underwriters often review two years of documentation, but some programs may accept shorter histories when the income is stable and expected to continue.

Q6. What are the 2026 mortgage interest deduction rules?

Recent tax legislation permanently locked in the $750,000 mortgage interest deduction limit ($375,000 if married filing separately) for loans taken out after December 15, 2017 — the cap was set to expire, but it's now here to stay. Mortgage insurance premiums are deductible again for 2026, phasing out once your adjusted gross income passes $100,000. The 2026 standard deduction is $15,000 for single filers and $30,000 for married couples filing jointly, so itemizing only pays off if your total deductions clear that bar. This isn't tax advice — check with a CPA before you file, since your specific situation can change the math.

Q7. How do lenders calculate income for self-employed or K-1 borrowers?

We start with your net profit or pass-through income from your tax returns, add back non-cash deductions like depreciation, and average the result over 24 months, or 12 months in some cases if the income is strong and stable. If your income dropped year over year, we typically use the lower figure and ask for an explanation.

Q8. Can Social Security or disability income be grossed up?

Yes. Since this income isn't taxed, lenders can count it as higher than the amount you receive. FHA typically allows a 15% gross-up with no documentation; conventional, VA, and USDA loans often allow up to 25% if you can show the income is non-taxable.

Conclusion

Getting your gross income right isn't just about passing the underwriter's desk. It dictates the loan amount and the interest rates you can actually secure. As mortgage professionals, we've seen too many buyers stress over scratching out math on a notepad, only to realize they miscalculated their usable earnings.

You don't have to do this the hard way. We strongly recommend Zeitro Strata. Instead of guessing, you can securely upload your pay stubs and tax forms in seconds. The platform automatically extracts the data and calculates your exact qualifying income based on current banking standards. It's fast, incredibly secure, and completely removes the guesswork from your homebuying journey.

People Also Read

- Income Needed for Mortgage: Methods, Examples & Requirements

- How to Verify Income for Mortgage: Detailed Guide for Loan Pros

- Income Verification Documents: A Complete Guide to Check

- How to Calculate Rental Income? Loan Officer's Guide