![[Solved] At What Income Level Do You Lose Mortgage Interest Deduction?](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/69fc07a57884d2f1eb3382cb_income-level-lose-mortgage-interest-deduction-banner.png)

Written by

Eric

Share this article

.svg)

Subscribe to updates

As a loan professional, I hear the same anxious question every tax season: "Am I making too much money to deduct my mortgage interest?" Borrowers desperately want to maximize refunds, yet panic sets in when they fear a salary bump might strip away their homeowner benefits.

Let me give you some peace of mind. You don't just "lose" this valuable tax break merely by getting a raise. However, the interplay between your earnings, loan size, and the latest 2026 tax regulations can significantly alter how much you actually save. In this guide, I'll definitively answer how income limits affect your mortgage deduction and what you must know before filing.

Key Takeaway

- There is no direct, absolute income limit that completely disqualifies you from claiming the mortgage interest deduction.

- You must actively choose to itemize deductions rather than taking the standard route to utilize this benefit.

- The actual restriction comes from loan amount limits, which are permanently capped at $750,000 for recent mortgages.

- High earners in the top tax bracket face slightly reduced deduction values under the new 2026 tax laws.

At What Income Level Do You Lose Mortgage Interest Deduction?

The short answer is: you never entirely lose the mortgage interest deduction simply because your salary hits a certain threshold. The IRS doesn't enforce a direct income cap that strips away your eligibility. Instead, restrictions are heavily tied to your total loan amount.

However, high-income earners face a nuanced reduction. Under the recently passed One Big Beautiful Bill Act (OBBBA) impacting 2026 taxes, the old "Pease Limitation" was replaced. Now, if your earnings place you in the top 37% bracket (over $640,600 for single filers or $768,700 for joint filers in 2026), itemized deductions for those in the 37% bracket are reduced by 2/37 of the lesser of total itemized deductions or the amount by which income exceeds the 37% bracket threshold, effectively limiting the tax benefit to about 35 cents per dollar at the top marginal rate.

You aren't losing the write-off entirely, but its overall power is slightly watered down. Your Adjusted Gross Income (AGI) dictates the benefit's strength, not your right to claim it.

What is the Mortgage Interest Deduction?

Let's break this down into simple terms. The mortgage interest deduction is a lucrative tax incentive designed by the federal government to encourage homeownership. It allows eligible homeowners to subtract the interest they pay on their home loan directly from their taxable income, effectively lowering their annual tax bill.

To claim this write-off, the property must be your primary residence or a designated second home. You can't use it for a third house or purely investment properties. When tax season rolls around, you won't take the standard route. Instead, you must itemize your expenses using IRS Schedule A.

Your lender will send you a Form 1098, which clearly outlines exactly how much interest you paid over the prior year. By reporting this figure, you shield a portion of your hard-earned money from being taxed.

Itemized vs. Standard Deduction: How It Impacts Your Mortgage Interest

Many borrowers I work with are baffled when their accountant tells them they shouldn't write off their mortgage interest. The reason usually boils down to simple math: Itemized vs. Standard Deduction.

You can only claim housing interest if your total itemized deductions, which include mortgage interest, state and local taxes (SALT), and charitable donations, are greater than the IRS standard deduction. For the 2026 tax year, the standard deduction is $16,100 for single filers and $32,200 for married filing jointly.

If a married couple paid $20,000 in mortgage interest and has no other major deductions, their total itemized amount ($20,000) falls well short of the $32,200 standard threshold.

In this scenario, they will rationally choose the standard deduction to save more money. They didn't lose the benefit due to income. They voluntarily bypassed it because the standard deduction offered a better deal.

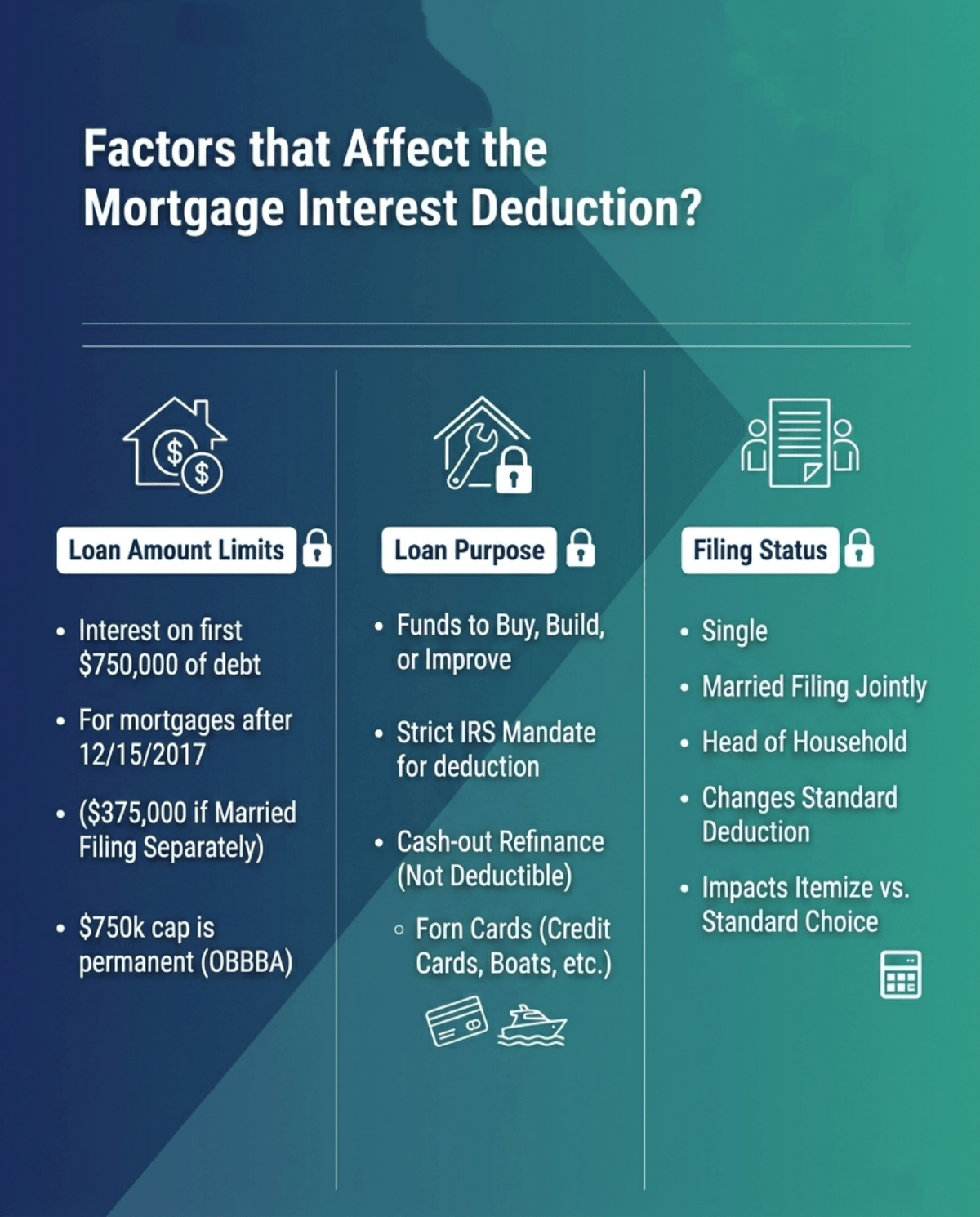

Factors that Affect the Mortgage Interest Deduction

While your salary doesn't directly disqualify you, several other critical elements absolutely dictate how much interest you can write off. Here are the true limiting factors:

- Loan Amount Limits: For mortgages originated after December 15, 2017, you can only deduct interest on the first $750,000 of your mortgage debt ($375,000 if married filing separately). The OBBBA made this $750k cap permanent.

- Loan Purpose: The IRS strictly mandates that the borrowed funds must be used to buy, build, or substantially improve the property securing the loan. If you do a cash-out refinance to pay off high-interest credit cards or buy a boat, that specific portion of the interest is not deductible.

- Filing Status: Whether you file as single, married filing jointly, or head of household changes your standard deduction baseline, which directly influences whether itemizing your mortgage interest is financially beneficial.

FAQs About Income Level Losing Mortgage Interest Deduction

Q1. Is there an income limit for deducting mortgage interest?

No, there is no hard income limit that entirely strips away your eligibility to deduct mortgage interest. However, if your income places you in the highest 37% tax bracket (over $640,600 for singles in 2026), new tax rules slightly reduce the value of your overall itemized deductions to 35 cents per dollar. You keep the deduction, but the relative tax-saving power is modestly restricted.

Q2. Why can't I claim my mortgage interest on my taxes?

The two most common reasons you can't claim it are math and loan purpose.

First, if your total itemized expenses don't exceed the generous standard deduction, it makes no financial sense to claim it.

Second, if you utilized a cash-out refinance for personal expenses like a vacation or a vehicle, rather than improving your home, that interest becomes completely ineligible for IRS tax benefits.

Q3. Can I write off 100% of my mortgage interest?

Yes, provided your situation fits within IRS guidelines. You can write off 100% of the interest paid if your total mortgage debt is under the permanent $750,000 cap, the loan was used strictly for purchasing or improving your primary or secondary home, and your total itemized deductions exceed your standard deduction. Any debt exceeding that $750,000 threshold will only yield a prorated deduction.

Q4. Is it worth it to deduct mortgage interest on taxes?

It strictly depends on your personal financial footprint. If your combined deductible expenses, like housing interest, substantial charitable contributions, and eligible state and local taxes, surpass the standard deduction ($32,200 for joint filers in 2026), it is absolutely worth the effort to itemize. Otherwise, taking the standard route is much faster, less complicated, and yields a larger tax return.

Q5. How much mortgage interest can I deduct on my taxes?

You can deduct the exact amount of interest paid on up to $750,000 of qualified principal debt for your home. You don't need to guess this number. Your loan servicer will mail you a Form 1098 early in the year detailing the precise interest paid. For 2026 returns, qualifying private mortgage insurance (PMI) premiums paid after December 31, 2025, are treated as deductible home mortgage interest.

Conclusion

Ultimately, your income level won't outright disqualify you from the mortgage interest deduction. The true deciding factors are the size of your loan, how you utilized the funds, and whether your total itemizable expenses surpass the standard deduction threshold. As tax codes continually evolve, navigating these rules can feel incredibly overwhelming for any homeowner.

If you are unsure how these complex IRS changes impact your household budget, I strongly recommend consulting a licensed CPA for personalized tax strategy. Additionally, I encourage you to reach out for a free consultation with a local loan officer. We can help you structure future home purchases or refinancing strategies to maximize your financial leverage and keep more money in your pocket.

People Also Read

- Ultimate Guide: How to Calculate LTV Ratio for Mortgage?

- [Guide] How to Calculate DTI Ratio for Mortgage?

- Max DTI for Mortgage: Requirements By Loan Types

- Max LTV: Check Maximum Loan-to-Value Ratios By Loan Types

- Mortgage Income Requirements 2026: Learn Before You Apply

- Ultimate Guide: How to Calculate Net Income for a Mortgage?

- Guide: How to Calculate Gross Income for a Mortgage?

- Income Needed for Mortgage: Methods, Examples & Requirements