![[2026] Max DTI for Mortgage: Requirements By Loan Types](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/69cc7ab473923805b0152e34_max-dti-for-mortgage-banner.png)

Written by

Eric

Share this article

.svg)

Subscribe to updates

If you've been originating loans as long as I have, you know that finding the exact maximum Debt-to-Income (DTI) ratio in 2026 feels like hitting a moving target. Every single loan program and investor overlay seems to have its own strict ceiling. It is complex, time-consuming, and honestly, a massive headache for loan officers trying to pre-qualify borrowers quickly.

Instead of digging through hundreds of pages of PDF guidelines, I now use Zeitro Strata AI. It's a free, AI-powered mortgage assistant that instantly cross-checks different lender guidelines to give you exact max DTI requirements in seconds. Let's break down the 2026 standards and how you can stop wasting time on manual lookups.

Why Maximum DTI is Required?

Before we get into the exact numbers, let's take a quick step back. Why are we so bound by these DTI caps? As loan professionals, we know DTI isn't just a random hurdle. It's the ultimate metric for evaluating a borrower's default risk. Here is why the industry enforces maximum limits:

- Risk Management: Lenders need assurance that borrowers won't drown in debt. A strict ratio protects the lender's portfolio from defaults.

- Regulatory Compliance: The CFPB's Ability-to-Repay (ATR) rule legally requires us to verify that a borrower has sufficient income to handle their mortgage payments alongside existing obligations.

- Secondary Market Liquidity: To sell originated mortgages to government-sponsored enterprises like Fannie Mae or Freddie Mac, the files must precisely match their rigid acquisition standards.

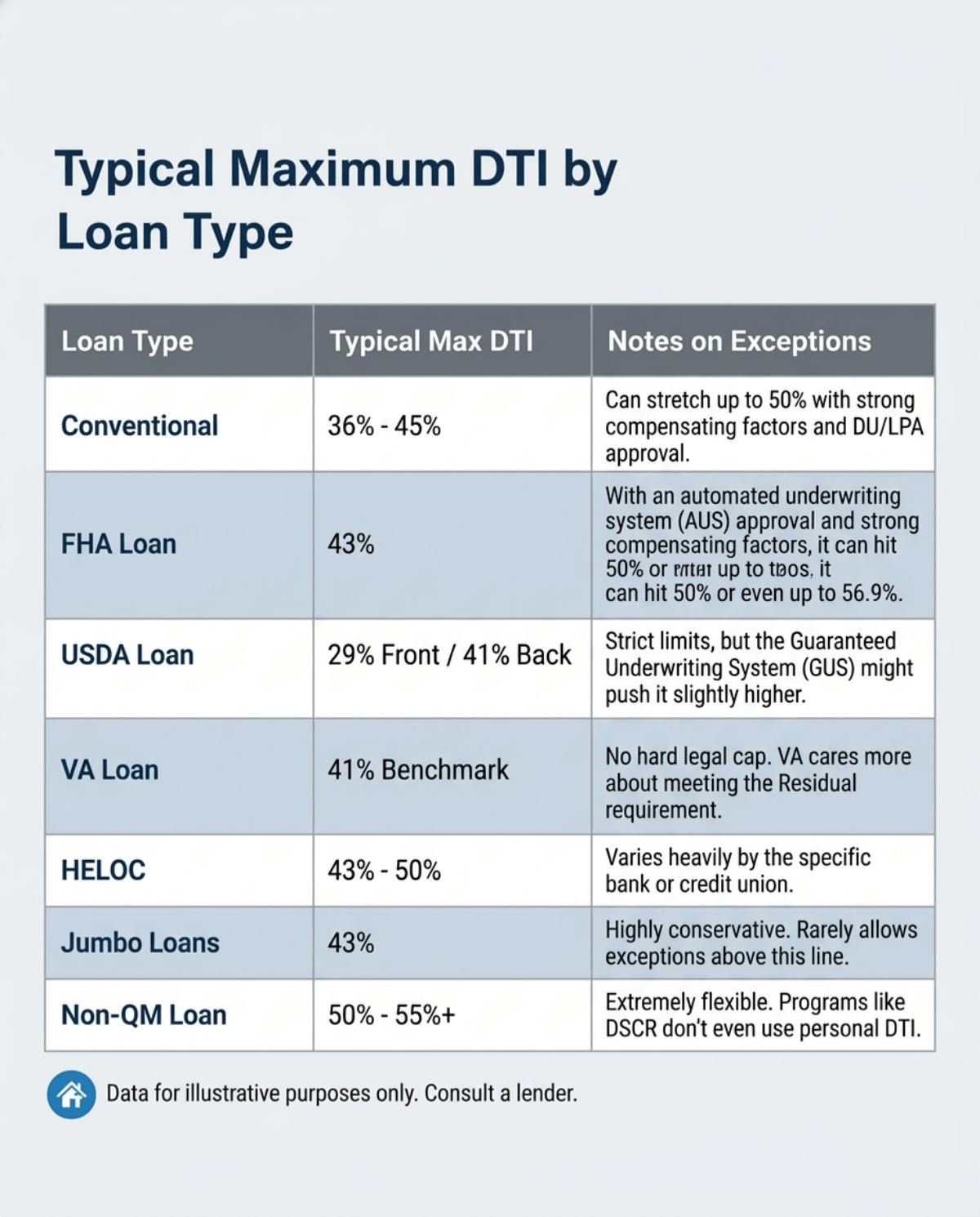

Typical Maximum DTI by Loan Type

Keep in mind, these baseline limits often change depending on specific lender overlays. But based on the 2026 landscape, here is the standard breakdown of maximum DTI by loan type:

- Conventional: 36% - 45%, can stretch up to 50% with strong compensating factors and DU/LPA approval.

- FHA Loan: 43%, with an automated underwriting system (AUS) approval and strong compensating factors, it can hit 50% or even up to 56.9%.

- USDA Loan: 29%, front / 41% Back, Strict limits, but the Guaranteed Underwriting System (GUS) might push it slightly higher.

- VA Loan: 41%, benchmark, No hard legal cap. VA cares more about meeting the Residual Income requirement.

- HELOC: 43% - 50%, varies heavily by the specific bank or credit union.

- Jumbo Loans: 43%, highly conservative. Rarely allows exceptions above this line.

- Non-QM Loan: 50% - 55%+, extremely flexible. Programs like DSCR don't even use personal DTI.

As you can see, the spread is massive. A borrower who gets denied for a Jumbo might easily slide into a Non-QM product if you know where to look.

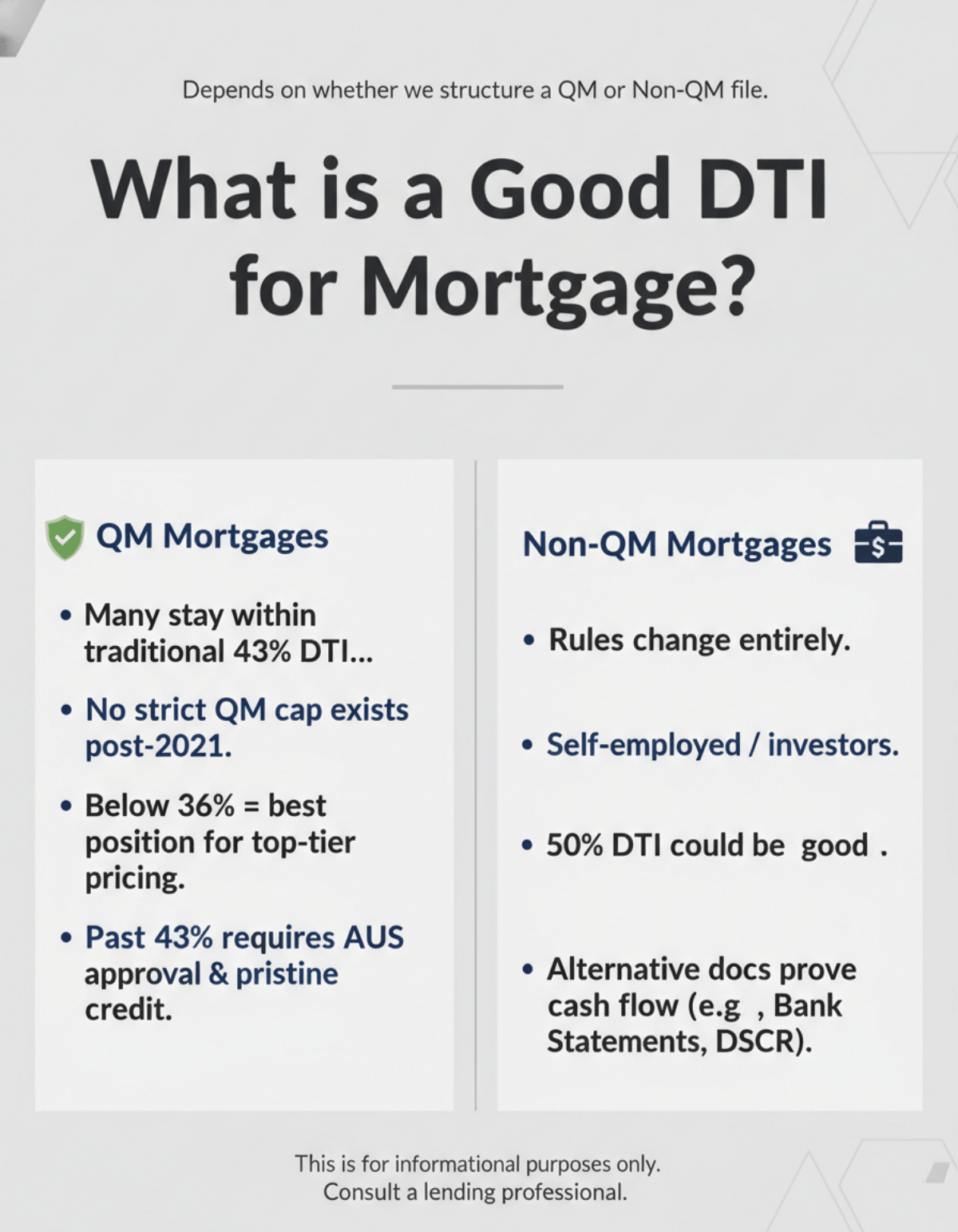

What is a Good DTI for Mortgage?

When a client asks me, "What's a good number?", my answer always depends on whether we are structuring a QM (Qualified Mortgage) or a Non-QM file.

- QM Mortgages: Many stay within traditional 43% DTI for conservative underwriting, though no strict QM cap exists post-2021 revisions. If your borrower stays at or below 36%, they are in the best position for top-tier pricing and a smooth clear-to-close. Pushing past 43% usually requires automated underwriting approvals and pristine credit.

- Non-QM Mortgages: The rules change entirely here. For self-employed borrowers or real estate investors using Asset Utilization or Bank Statement programs, a "good" DTI could easily be 50%. Since these products fall outside standard ATR guidelines, lenders rely on alternative documentation to prove cash flow rather than traditional backend ratios.

What Affects Your DTI Maximum?

You and I both know that a guideline maximum is rarely the final word. Several variables can instantly shift your borrower's DTI ceiling:

- Compensating Factors: High FICO scores, substantial down payments, and deep cash reserves can convince an underwriter to stretch the limits.

- Lender Overlays: This is the biggest hurdle. Fannie Mae might technically allow 50%, but your specific wholesale lender's internal policy might hard-stop at 45%.

- Automated Underwriting Systems (AUS): A DU (Desktop Underwriter) or LPA (Loan Product Advisor) "Approve/Eligible" finding often supersedes manual underwriting guidelines, unlocking higher thresholds automatically.

Understanding these nuances is exactly why quoting a single number to a borrower is risky without checking the exact investor guides first.

Tip: How to Check DTI Guidelines Quickly and Accurately?

Memorizing overlays for dozens of investors is impossible. I used to waste 30 minutes per file digging through PDFs just to verify a Non-QM DTI limit. Now, I use Zeitro Strata AI, the ultimate AI-powered mortgage guideline assistant.

Zeitro Strata AI has deeply indexed over 300+ guidelines from mainstream lenders—including AAA Lending, AD Mortgage, and CMG Financial—covering everything from Conventional to niche Non-QM (DSCR, Bank Statement, ITIN). You just type your scenario in plain English (or Chinese), and its DeepSearch instantly cross-checks 100+ investors. It delivers highly accurate answers in seconds, complete with direct Citations so you can trace the exact source page. Need clarification? Just use the Explain feature.

Beyond Strata AI, Zeitro offers a complete ecosystem to turbocharge your origination:

- GrowthHub: Launch a branded personal microsite to showcase your expertise on Bluerate, rank higher on local SEO, and capture leads directly.

- Digital 1003 (POS): Automate the application process. It pulls borrower data, instantly calculates DTI with AI precision, exports to FNM 3.4, and helps borrowers finish apps in just 5 minutes.

- Pricing Engine: Get up-to-the-minute rate quotes for both Conventional and Non-QM products, complete with customizable overlay adjustments.

Using this platform realistically saves 7+ hours per loan file and helps me close 30% more loans.

Frequently Asked Questions about MAX DTI

Q1. What is the 33% mortgage rule?

It's a traditional front-end ratio guideline suggesting that your total monthly housing expenses, including principal, interest, taxes, and insurance, should not exceed 33% of your gross monthly income. Sticking to this rule helps ensure borrowers remain comfortable and aren't "house poor."

Q2. What is the 28 DTI rule?

The classic 28/36 rule states that a maximum of 28% of your gross monthly income should go toward housing expenses, while no more than 36% should go toward all total debt obligations combined, including car loans and credit cards.

Q3. What is the maximum DTI for better mortgage?

To secure the most competitive interest rates and ensure a highly favorable underwriting decision, you should aim for a total DTI of 36% or lower. Lenders view this range as low-risk, which translates to better pricing and fewer required compensating factors.

Q4. Is 39 DTI too high?

Not at all. A 39% DTI is considered a very safe and acceptable range in the mortgage industry. It easily falls under the maximum limits for Conventional, FHA, VA, and USDA loans, usually without needing any extra compensating factors.

Q5. Is 35% of income too much for a mortgage?

If 35% is your front-end housing ratio, it is slightly elevated but manageable. However, if 35% represents your back-end total debt ratio, it is actually an excellent, healthy financial position that will easily qualify for almost any loan program.

Q6. Is 42 DTI bad?

No, a 42% DTI is incredibly common. It sits right below the standard 43% cap used by many lenders. You will comfortably qualify for FHA and VA loans, and most Conventional loans will approve it as long as your credit score is decent.

Conclusion

Navigating the 2026 mortgage landscape means accepting that the maximum DTI is never just one single number. It shifts drastically depending on the loan type, your borrower's profile, and the specific investor overlays you're dealing with. As originators, our job is to find the right home for the file, but we shouldn't have to burn hours doing manual guideline research.

If you want to escape the trap of outdated PDFs, I highly recommend checking out Zeitro. Their Explorer plan is completely free and gives you 3 daily Mortgage AI queries, access to the pricing engine, and your own personal website. Stop guessing on DTI limits. Sign up, reclaim your time, and start delivering faster pre-qualifications today.

People Also Read

- Mortgage Guidelines: What Are They? How to Verify?

- Non-QM Loan Guidelines: How to Check and Verify with AI Accuracy

- Best Mortgage Underwriter Certifications: Everything to Know Here

- Best Mortgage Underwriter Training Online: Improve Your Expertise

- What is Mortgage Eligibility Checker? Best Tool to Verify Guidelines

- [Guide] How to Calculate DTI Ratio for Mortgage?

- [Solved] What Debt-to-Income Ratio is Needed for a Mortgage?

![[Solved] How to Calculate Commission Income for Mortgage?](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/6a3ce1b02009d0aba39b3174_how-to-calculate-commission-income-banner.png)