![[Solved] What Debt-to-Income Ratio is Needed for a Mortgage?](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/6a056583727fb01173eb93f8_what-debt-to-income-ratio-is-needed-for-a-mortgage-banner.png)

Written by

Eric

Share this article

.svg)

Subscribe to updates

When I first applied for a mortgage years ago, I constantly worried my debt-to-income (DTI) ratio would instantly disqualify me. If you're feeling that same anxiety right now, take a deep breath. As a homebuyer, you might fear your student loans or car payments are dealbreakers. But from a loan officer's perspective, DTI isn't just a hurdle. It's a vital tool to measure risk and ensure you can comfortably afford your new home without drowning in bills.

So, what DTI is actually needed? Traditionally, lenders preferred a DTI of 36% or lower, but many modern loan programs accept higher ratios, especially for borrowers with strong credit or assets. However, depending on your specific loan type, you can often get approved with a ratio between 43% and 50%. Let's break down exactly what lenders look for.

Key Takeaways

- The ideal DTI ratio is 36% or lower, giving you the best chance for favorable interest rates.

- Most conventional loans commonly allow DTIs up to 45%, but with automated underwriting approval, ratios can often go as high as 50% depending on the borrower's overall profile.

- Government-backed programs like FHA loans are more flexible than conventional loans. While the standard guideline is 43%, borrowers with strong compensating factors may qualify with DTIs up to around 50%.

- Paying down small balances and avoiding new credit checks are the fastest ways to improve your numbers.

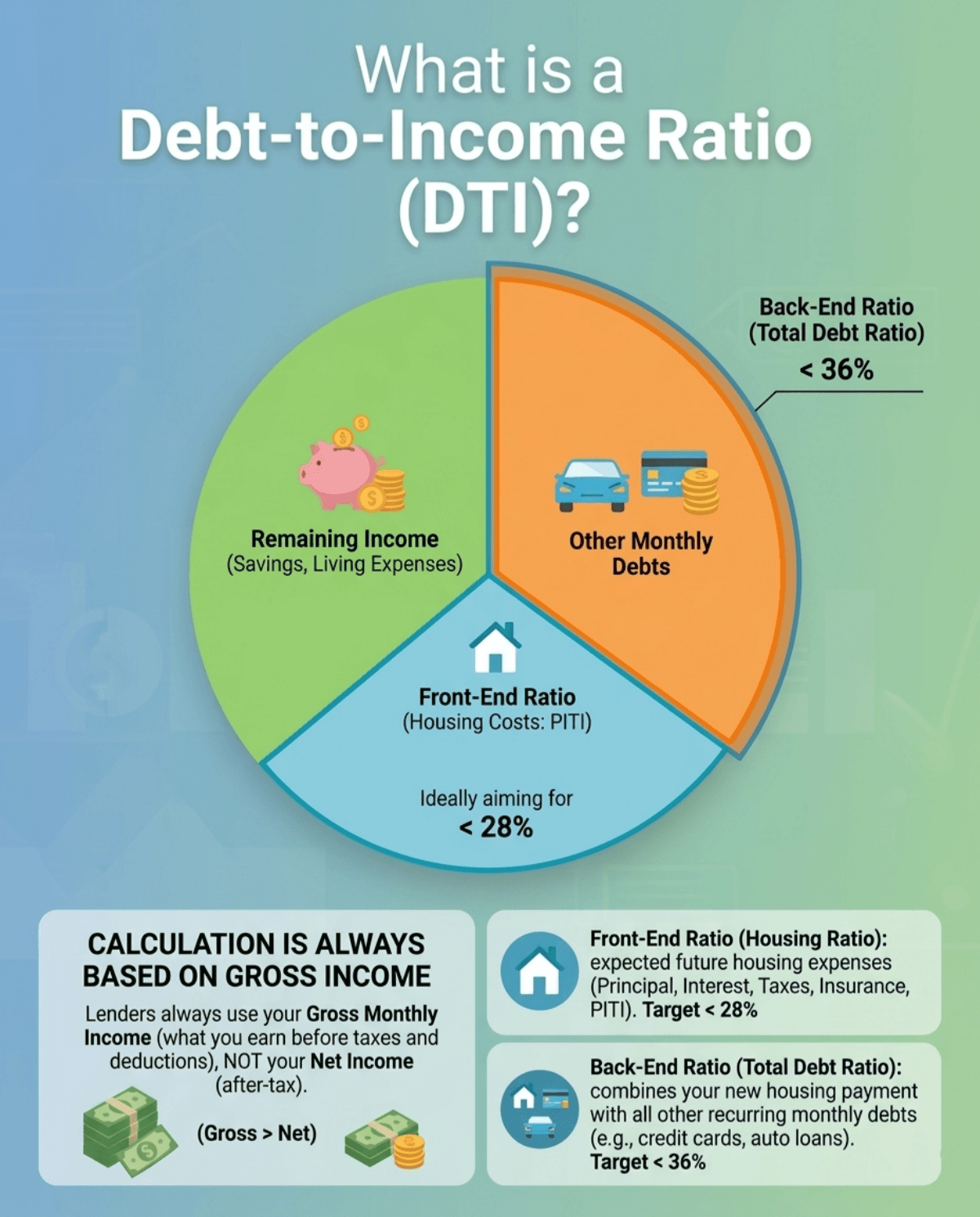

What is a Debt-to-Income Ratio (DTI)?

Think of your gross monthly income as a whole pie. Your DTI ratio is simply the slice of that pie already eaten up by your monthly debt obligations. Mortgage lenders care deeply about this metric because it directly predicts your default risk. If your debt slice is too large, adding a massive mortgage payment could push you over the financial edge.

One common mistake I see borrowers make is using their net income (after taxes) for this math. Lenders always use your gross monthly income, what you earn before taxes and deductions.

To accurately gauge your borrowing power, underwriters actually look at two distinct variations of this metric.

- Front-End Ratio (Housing Ratio): This number focuses strictly on your future housing expenses. It includes your expected mortgage principal, interest, property taxes, and homeowners insurance (often called PITI). In a perfect world, lenders prefer this specific slice to stay under 28% of your gross income.

- Back-End Ratio (Total Debt Ratio): This is the big one. It combines your new housing payment with all your other recurring monthly debts, like credit cards and auto loans. When loan officers quote DTI requirements, they are almost always talking about this back-end figure, ideally aiming for 36% or lower.

Also Read:

- Guide: How to Calculate Gross Income for a Mortgage?

- Zeitro Mortgage Affordability Calculator Free and Online

- Zeitro Mortgage Payment Calculator with Interest & Taxes

What Debt-to-Income Ratio is Needed for a Mortgage?

There isn't a single universal number that guarantees approval. Different mortgage products carry distinct rules. Here is what I usually tell house hunters to expect:

- Conventional Loans: Backed by agencies like Fannie Mae, these generally cap your DTI at around 43% to 45%. If your application requires manual underwriting, the strict cutoff is usually 36%.

- FHA Loans: These are incredibly flexible. The standard cap sits at 43%, but I've seen borrowers secure FHA approvals with ratios pushing 50%, and sometimes higher in rare cases.

- VA Loans: Designed for veterans, these don't strictly enforce a maximum front-end ratio. While the VA uses a 41% back-end benchmark, they care much more about your "residual income". The actual cash left over each month to feed your family.

- Non-QM Loans: If you are self-employed or have complex finances, non-qualified mortgages offer alternative qualifying methods. Some non-QM lenders allow DTIs well over 50% here.

Why is there so much wiggle room? It comes down to compensating factors. If your ratio is sitting at an uncomfortable 49%, a lender might still say yes if you bring a massive down payment, hold excellent credit scores, or have several months of cash reserves sitting in the bank. These strengths offset the perceived risk.

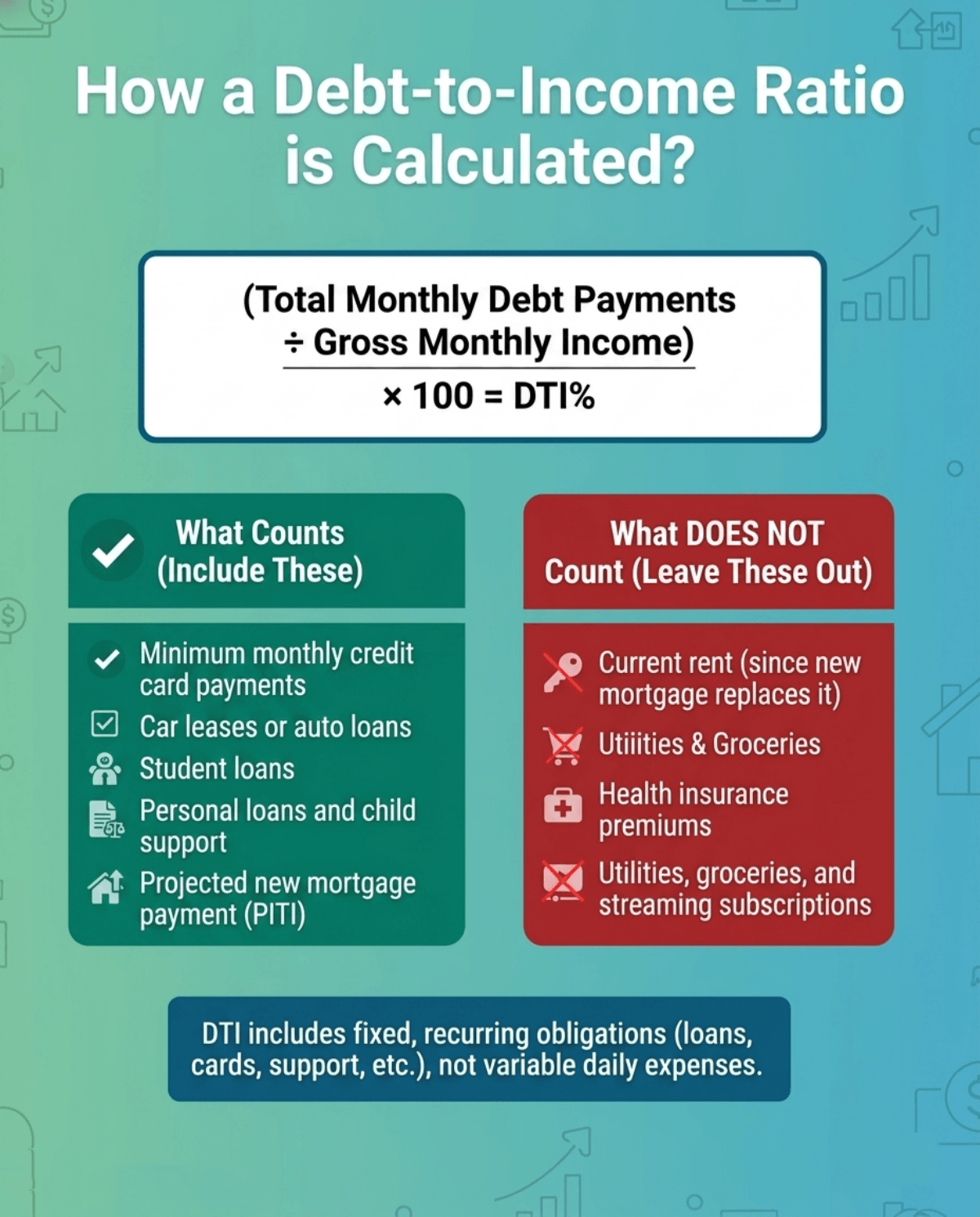

How a Debt-to-Income Ratio is Calculated?

Calculating your own ratio before talking to a bank is surprisingly straightforward. Grab a calculator and use this simple formula:

(Total Monthly Debt Payments ÷ Gross Monthly Income) x 100 = DTI%

You must know exactly what belongs in that top number.

What counts (Include these):

- Minimum monthly credit card payments (not the total balance)

- Car leases or auto loans

- Student loans

- Personal loans and child support

- Your projected new mortgage payment (PITI)

What DOES NOT count (Leave these out):

- Your current rent (since the new mortgage replaces it)

- Utility bills, groceries, and streaming subscriptions

- Health insurance premiums (may still be considered in a broader financial assessment)

I constantly see buyers needlessly panic because they included their $200 grocery bill or electric bill in their math. DTI includes fixed, recurring obligations, whether or not they appear on your credit report, such as loans, credit cards, child support, and other legally required payments.

[Tips] How to Improve Your DTI Before Applying?

If your math looks a bit scary right now, don't worry. You can actively reshape your financial profile before handing over an application.

- Pay down existing debts strategically: Don't just throw cash at large balances. Wipe out smaller credit cards or personal loans completely. Eliminating a $100 monthly minimum payment instantly improves your back-end ratio.

- Increase your gross income: Ensure you provide your loan officer with every possible income source. This includes documented part-time gigs, consistent annual bonuses, or freelance side hustles.

- Make a larger down payment: Putting more cash down shrinks your total loan size. A smaller loan means a lower monthly payment, which directly reduces your DTI.

- Add a co-borrower: Bringing in a spouse or trusted co-signer who has strong income and minimal debt can beautifully balance out your combined application.

FAQs About DTI Requirements

Q1. Is current rent included in the debt-to-income ratio when buying a house?

No. In most cases, your current rent is not included because it will be replaced by your new mortgage, though exceptions may apply if the property will not be vacated. The calculation focuses strictly on your future housing costs alongside existing long-term debts, assuming you will not be paying both simultaneously.

Q2. Does my spouse's debt count toward my DTI?

It depends. If your spouse is not listed on the mortgage application, their independent debts generally are not counted. However, if you reside in a community property state, the lender might legally have to include their obligations anyway, even if they aren't borrowing.

Q3. Are living expenses like groceries and utility bills included in DTI?

No, they are entirely excluded. Lenders only care about fixed debt obligations that appear on your official credit report, plus legally binding payments like child support. Your daily living expenses, health insurance premiums, cell phone bills, and groceries do not matter here.

Q4. Can I get a mortgage with a 50% DTI ratio?

Yes, it is entirely possible. Government-backed FHA loans frequently approve borrowers at the 50% mark. Some conventional loans may allow DTIs around 50% if the application receives automated underwriting approval and includes strong compensating factors, such as an exceptionally high credit score or substantial cash reserves in your savings account.

Q5. Does paying off a collection account improve my DTI?

It depends. If you are currently making a scheduled, required monthly payment toward that collection, paying it off removes that burden and lowers your DTI. If there is no active monthly payment reporting, clearing it helps your credit score but won't alter your DTI.

Final Word

Getting ready to buy a home can feel like navigating a maze, but understanding your numbers puts you in the driver's seat. While keeping your DTI in that 36% to 43% sweet spot is ideal, remember that this single percentage doesn't define your entire homebuying journey. Every borrower's financial fingerprint is unique, and lenders have various programs built to accommodate different situations.

Before you make any drastic financial moves, like draining your emergency savings just to wipe out a car loan, I highly recommend running your numbers through an online DTI calculator.

Better yet, reach out to an experienced loan officer. We can review your specific scenario and map out a customized plan to get your mortgage approved.

People Also Read

- Income Needed for Mortgage: Methods, Examples & Requirements

- Explained: What is a Bank Statement? Everything to Know

- What is a WVOE Form: Meaning, Purpose & Use

- How to Calculate Mortgage Interest: Manually & Automatically

- Ultimate Guide: How to Calculate Monthly Mortgage Payment?

![[Solved] How to Calculate Commission Income for Mortgage?](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/6a3ce1b02009d0aba39b3174_how-to-calculate-commission-income-banner.png)